- Keppel Infrastructure Trust has two evergreen infrastructure assets, City Gas and Ixom, which provide potential for organic growth.

- Acquired in 2019, Ixom is a leading infrastructure business in Australia and New Zealand that supplies chemicals in various industries like water treatment and food & beverage. Ixom’s growth is supported by favourable trends, such as population growth and rising global dairy consumption per capita.

- Meanwhile, piped town gas which Singaporeans use for cooking is supplied solely by City Gas. It is also expected to register modest growth due to a steady stream of housing supply, supported by population growth.

- KIT’s ample debt headroom provides room for inorganic growth, and potential acquisition targets may include evergreen infrastructure assets that are yield-accretive.

- As of 17 December 2019, coupled with a distribution yield of around 7%, our target price of SGD 0.565 represents a potential total return of 12.5%.

You may not have realised it, but whether it is the clean water that you drink, or the food that you consume, Keppel Infrastructure Trust (SGX:A7RU) is part of our everyday lives in one way or another.

When we think about infrastructure assets, the first few things that come to mind are probably water treatment plants, transportation infrastructure and power generators, the revenue from which are mostly protected by concessional agreements or long-term contracts.

However, the definition of infrastructure has broadened over the years to include a plethora of non-concessional assets – also known as evergreen assets – that do not have an end life.

Evergreen infrastructure assets typically have the following attributes:

- They provide an essential service;

- They generate stable and defensive cash flows without the need for long term contracts; and

- They operate in industries where there are high barriers to entry e.g. government regulation, natural monopolies.

In this article, we focus on the two evergreen infrastructure assets in KIT’s portfolio: Ixom and City Gas. Ixom provides chemicals used in various industries such as water treatment, while City Gas supplies the piped town gas that many Singaporeans use for cooking.

(Related article: Investors seeking stable and regular income must have this 7%-yielding stock in their portfolios)

Ixom: Leading producer and distributor of chemicals in Australia

A monopoly in Eastern Australia, Ixom is amongst the leading industrial infrastructure businesses in Australia and New Zealand, supplying and distributing water treatment chemicals, as well as various other industrial and specialty chemicals (Table 1).

Table 1: Key chemicals manufactured and distributed by Ixom

|

Key chemical |

Description |

Key end market |

|

Liquefied chlorine |

Water treatment chemical |

Water |

|

Caustic soda |

Used in the ‘cleaning-in-place’ process in hygiene critical industries |

Food & beverage |

|

Hydrochloric acid |

Used in the nickel refining process |

Mining |

Ixom

is the sole Australian manufacturer of liquefied chlorine. Liquefied chlorine

is added into water as a disinfectant. In essence, it helps to ensure that the

water delivered to consumers is safe for consumption. Since water is essential

in our everyday lives, liquefied chlorine, which is a critical component in the

water treatment process, is also an essential product.

You may be surprised, but Ixom is involved in the food and beverage industry as well. It is a market leader in manufactured caustic soda (sodium hydroxide), an alkali detergent used to remove fatty oils and protein solids in dairy products.

‘Cleaning-in-place’, which uses caustic soda, is a critical process in guaranteeing food safety. It ensures that the dairy products being produced are not contaminated. Thanks to caustic soda, we are able to safely enjoy our favourite indulgence foods, such as ice cream, chocolates and cakes.

Ixom’s defensive business has strengthened KIT’s distributable cash flows

There are very few Australian manufacturers manufacturing specialty chemicals for water treatment, food and beverages, and mining. Apart from Ixom, another major player in Australia’s specialty chemicals industry would be Coogee Chemicals. Its main presence, however, is in Western Australia. Hence, there is minimal direct competition with Ixom, which operates mainly in Eastern Australia.

The specialty chemicals industry is also one that has high barriers to entry. Not only do businesses like Ixom require large capital investments, they also need to secure hundreds of licenses before they can manufacture and distribute specialty chemicals.

Moreover, Ixom’s manufacturing and logistics facilities are well-positioned throughout key regions in Australia and New Zealand, allowing it to support its large and diversified customer base of over 8,000 customers. Hence, there is little incentive for Ixom’s customers to switch to another competitor.

Due to the essential nature of the products it distributes, a sticky customer base, high barriers to entry preventing increased competition in the industry, and the ability to raise prices if cost increases, the cash flows generated by Ixom are very defensive and consistent.

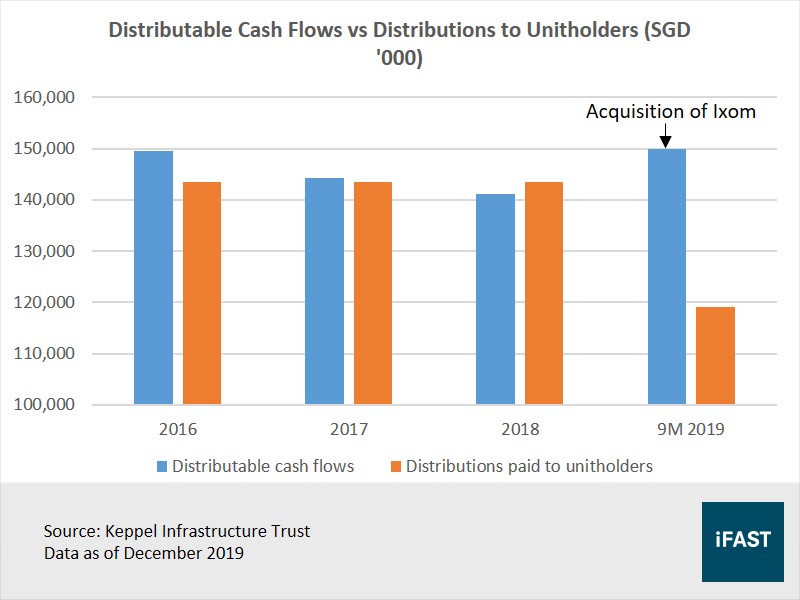

As such, the acquisition of Ixom has strengthened KIT’s ability to pay sustainable distributions, with distributable cash flows in 9M 2019 more than enough to offset the distributions paid out to unitholders (Figure 1).

Moving forward, we believe that KIT will be able to sustain its quarterly distributions of 0.93 cents, supported by the strong and visible cash flows generated by its concession assets, as well as the market-leading positions held by its evergreen businesses.

Figure 1: Increase in distributable cash flows in 9M 2019

Ixom’s growth supported by favourable trends

If current trends in life expectancy, migration and fertility were to continue, the population in Australia can almost double from 2017 to 2066 (Figure 2). As population grows, the need for water treatment will increase, which will in turn drive demand for liquefied chlorine manufactured by Ixom.

Figure 2: Steady growth in Australia’s population

Global milk demand is forecasted by IFCN Dairy to increase by 35% from 2017 to 2030 (which translates to 2.3% CAGR per year) due to population growth and higher dairy consumption per capita. Since New Zealand and Australia contribute a total of 46% to the world’s estimated milk production, this would have a favourable impact on the demand for caustic soda, especially for a market leader like Ixom.

City Gas: Monopoly town gas retailer in Singapore

You may recognise City Gas as the piped town gas retailer that Singaporeans turn to for their daily cooking and heating needs, but more importantly, City Gas holds the sole license from Energy Market Authority (EMA) for the production and retailing of town gas. In other words, it is the monopoly town gas retailer in Singapore.

City Gas derives its revenue from the town gas tariffs paid by consumers. The tariffs are determined based on factors such as the cost of producing and transporting town gas, and are reviewed and approved every quarter by the EMA. Since City Gas provides an essential service in a monopoly with the ability to pass on its costs, its cash flows are highly stable and defensive.

There are, of course, other competing alternatives to piped town gas, including cylinder liquefied petroleum gas (LPG) and induction cooking, which may dampen future demand for town gas. However, we believe consumers are unlikely to replace piped town gas with LPG.

City Gas provides an uninterrupted supply of town gas through its pipeline network, whereas the gas in cylinder LPGs can run out after a certain level of usage. Therefore, City Gas provides a much higher level of convenience.

Similarly, induction cooking is unlikely to be of a major concern to City Gas, as the amount of electricity that has to be used for induction cooking typically translates to a hefty electricity bill. Hence, piped town gas remains a cost-savvy choice for consumers.

City Gas still has room for growth

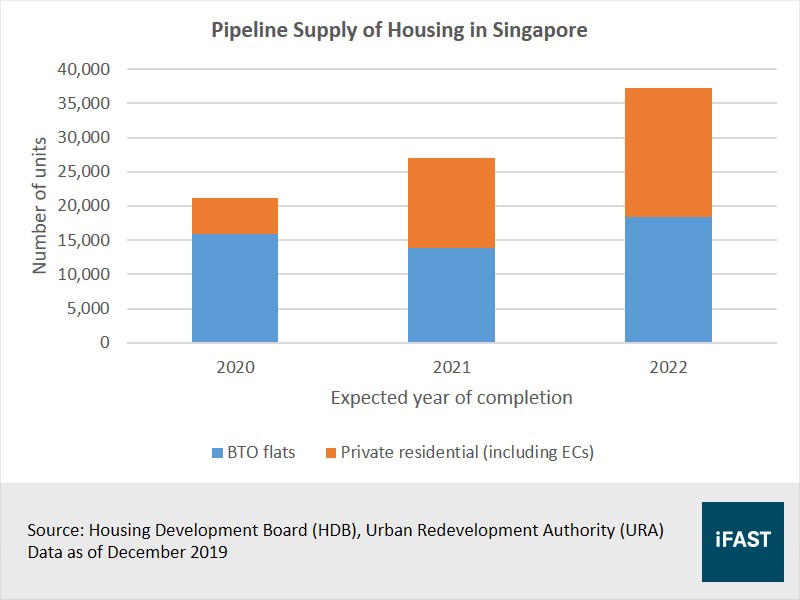

In 2018, City Gas’s customer base grew 3.5% year-on-year due to the newly-constructed Build-To-Order (BTO) flats. We believe City Gas is likely to experience organic growth due to a steady stream of housing supply in areas such as Punggol and Tampines.

An increasing number of BTO flats and private residential units are expected to be completed over the next few years (Figure 3). There are also some older housing estates that will be rejuvenated through the Selective En bloc Redevelopment Scheme (SERS).

The new homes and rejuvenated housing estates are likely to be connected to the town gas pipeline network, which would increase the demand for town gas. City Gas has served more than 90% of new housing units. Assuming this percentage remains constant, we would likely see a modest CAGR of approximately 3% in City Gas’s customer base for the next few years.

With slightly less than two-thirds of the households in Singapore currently using piped town gas, there still remains room for City Gas to grow in the future. The increasing adoption of piped town gas will probably be at the expense of cylinder LPG, the sales for which have been falling over the years. Supported by new housing units, we believe that City Gas is able to achieve a higher penetration rate in Singapore.

Figure 3: Demand for town gas is underpinned by a steady housing supply

Attractive dividend yield with decent upside potential

Unlike infrastructure assets that are concession-based, evergreen businesses have the potential for growth due to demand factors that help the business stay relevant. They do not have an end life, and there is also a constant need for their products – people don’t stop eating or drinking just because the economy is not doing well. This gives rise to long-term cash flows that are defensive.

With such long-term and defensive cash flows, KIT has been paying out stable distributions to its unitholders. Its quarterly distribution of 0.93 Singapore cents has remained unchanged since 2Q 2015. This translates into an estimated distribution yield of 7% (based on 17 December 2019’s closing price), which has further upside given the growth potential of Ixom and City Gas.

Moreover, KIT’s ample debt headroom of SGD 1 billion puts the Trust in a sufficient and comfortable position to deliver inorganic growth, with yield-accretive evergreen businesses likely to be potential acquisition targets.

Using a two stage dividend discount model, we arrived at a target price of SGD 0.565. Based on its last traded price of SGD 0.535 as of 17 December 2019, KIT has a total return potential of around 12.5%.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.