- We initiate coverage on Keppel Infrastructure Trust, the only infrastructure trust listed on the SGX.

- KIT provides investors with stable distributions every quarter that are supported by long-term and defensive cash flows with governments and reputable counterparties. Distribution yield is attractive relative to most business trusts and REITs.

- Balance sheet is healthy with more than 90% of loans being non-recourse and debt obligations being refinanced at maturity.

- Future growth prospects looks promising with organic growth provided by evergreen businesses such as Ixom and City Gas due to favourable demand trends. There is also potential for more yield accretive acquisitions as net gearing ratio provides decent headroom for debt.

- We value Keppel Infrastructure Trust at $0.565, which translates to an upside potential of 7% based on the closing price of $0.530 on 29 November 2019.

Imagine living in a city without infrastructure: no electricity, no water supply and no waste treatment. There would be unlit streets, undrinkable water, garbage piling up like mountains, and the list goes on …

At this point in time, it is undeniable that infrastructure plays a critical role in our lives. This is why there are continuous investments into infrastructure no matter the state of the economy.

Investors can thus reap the benefits of infrastructure spending by investing in infrastructure stocks. In this article, we focus our attention on Keppel Infrastructure Trust (SGX:A7RU), the largest diversified business trust in Singapore with a portfolio of strategic infrastructure assets located in Singapore, Australia and New Zealand.

How infrastructure assets make money

As mentioned, infrastructure is not significantly exposed to economic cycles. In fact, it remains strong even during economic downturns. Infrastructure is the backbone of the economy – developing economies need infrastructure to grow, while developed economies need continuous investments in infrastructure to remain competitive.

Typical infrastructure assets include water treatment plants and power generators. Different infrastructure assets can have different revenue structures (Table 1).

Table 1: Main types of revenue structure for infrastructure assets

Revenue Structure | Description |

Availability | Investors will receive payments regardless of actual demand, as long as the asset is in the required condition and a certain level of capacity made available as specified in the concession agreement. Social infrastructure assets are common examples. |

Regulated | Assets are subjected to government regulation in areas such as consumer prices, economic returns, and quality of service. In exchange, the assets typically enjoy monopoly status. Energy and water utilities are typically regulated. |

Contracted | Contracts signed for the service provided gives a steady stream of revenue. Common examples are communication assets. |

Usage | Revenue streams vary with asset usage. Transportation assets such as toll roads are common examples. |

Merchant | Revenue streams are dependent on current market prices for their services. Power generation facilities that are uncontracted are common examples. |

Source: Mercer, iFAST Compilations | |

Delivering value through a large and diversified portfolio of assets

KIT merged with CitySpring Infrastructure Trust in 2015 to form the present Trust. Since then, KIT has been the only infrastructure trust listed on the SGX.

With $5.1 billion in infrastructure assets, KIT operates in 3 different segments: Distribution & Network, Energy, and Waste & Water (Table 2). You may be familiar with some its assets, such as City Gas, desalination and NEWater plants, since they have made an impact in our everyday lives.

Table 2: KIT’s portfolio

Asset | Description | Customer | Contract expiry | Revenue structure |

Distribution & Network | ||||

City Gas | Sole producer and retailer of piped town gas in Singapore | 856,000 residential and commercial customers | None | Fixed margin per unit of gas sold, with fuel and electricity costs passed through to customer (i.e. gas tariffs) |

Ixom | Industrial infrastructure business supplying key water treatment chemicals in Australia and New Zealand | Over 8,000 customers comprising municipals and blue-chip companies | None | Payments from customers for delivery of products and provision of services based on agreed terms |

Basslink | Basslink subsea interconnector which transmits electricity and telecoms between Victoria and Tasmania in Australia | Services Agreement with Hydro Tasmania | 2031 (with option for 15-year extension) | Monthly facility fee payments from Hydro Tasmania (HT) for the operation, based on the interconnector’s availability |

Energy | ||||

Keppel Merlimau Cogen (KMC) | 1,300MW combined cycle gas turbine power plant | Capacity Tolling Agreement with Keppel Electric | 2030 (with option for 10-year extension) Landlease till 2035 (with option for 30-year extension) | Monthly capacity payment for making available the full capacity of the plant, regardless of the actual power production of the plant |

Waste & Water | ||||

Senoko WTE Plant | Waste-to-energy plant with contracted incineration capacity of 2,310 tonnes per day | Senoko Incineration Services Agreement (ISA) with NEA | 2024 | Fixed Capacity Payments for the provision of incineration capacity |

Keppel Seghers Tuas WTE Plant | Waste-to-energy plant with contracted incineration capacity of 800 tonnes per day | Tuas Design Build Own Operate (DBOO) ISA with NEA | 2034 | Fixed Capacity Payments for the provision of incineration capacity |

Keppel Seghers Ulu Pandan NEWater Plant | One of Singapore’s largest NEWater plants which contracted warranted capacity of 148,000m3/day | NEWater Agreement with PUB | 2027 | Fixed Availability Payments for the provision of product capacity |

SingSpring Desalination Plant | Seawater desalination plant capable of supplying up to 136,380m3 of desalinated potable water per day | Water Purchase Agreement with PUB | 2025 Landlease until 2034 | Fixed monthly Capacity Payment for making available the output capacity of the plant to PUB |

Source: Keppel Infrastructure Trust, iFAST Compilations | ||||

Stable dividends and attractive dividend yield of 7%

Since most of KIT’s assets generate revenue based on availability-based payments, and are secured by long-term contracts with governments and reputable counterparties, the Trust is able to obtain a steady stream of cash flows.

While Ixom and CityGas are non-concession assets, with no long-term contracts in place, they are the only players in their respective business areas with a large and diversified customer base. CityGas is the sole retailer of piped town gas in Singapore, while Ixom is the dominant player in Eastern Australia for water treatment chemicals. Hence, their cash flows are recurring in nature and are highly visible.

Moreover, Ixom has a cost pass-through mechanism that gives them the ability to raise prices if their cost increases. CityGas also has no issues passing through their costs to consumers as gas tariffs are reviewed quarterly by the Energy Market Authority (EMA).

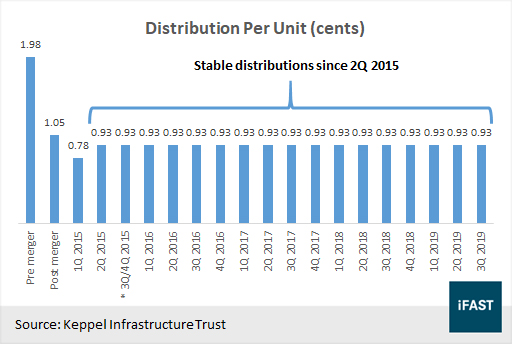

Such stable and long-term cash flows have translated into stable and attractive distributions to unitholders over the years (Figure 1), with its quarterly distribution of 0.93 Singapore cents unchanged since 2Q 2015. This translates into an estimated distribution yield of about 7%, which compares favourably to that of most Singapore-listed REITs and business trusts (Table 3).

Figure 1: Distribution Per Unit (DPU) has been stable since 2Q 2015

Table 3: KIT offers a high distribution yield relative to most SGX-listed Business Trusts

Name | *Distribution Yield | Gearing Ratio |

Eagle Hospitality Trust | 12.08% | 37.3% |

Hutchison Port Holdings Trust | 10.06% | 33.2% |

Accordia Golf Trust | 8.96% | 25.0% |

Dasin Retail Trust | 8.74% | 36.4% |

Ascendas Hospitality Trust | 8.00% | 33.8% |

Keppel Infrastructure Trust | 7.36% | 42.3% |

Asian Pay TV Trust | 7.02% | 54.0% |

Frasers Hospitality Trust | 6.24% | 35.1% |

CDL Hospitality Trust | 5.78% | 36.3% |

Far East Hospitality Trust | 5.54% | 39.6% |

NetLink NBN Trust | 5.38% | 15.0% |

Ascendas India Trust | 4.87% | 33.0% |

Median | 7.02% | 35.7% |

FTSE ST REIT Index | 5.24% | 34.5% |

Source: Bloomberg, Companies, iFAST Compilations *Based on consensus estimates for FY2020 | ||

Healthy balance sheet safeguards distributions

KIT’s current gearing ratio (debt-to-assets) of 42.3% is below the maximum 45% gearing limit, giving it some flexibility to make further yield-accretive acquisitions should the opportunity arise, although it must be noted that the gearing limit does not affect KIT as it applies only to REITs, and is used in this case as a benchmark to gauge its financial position.

While its gearing ratio rises to 48% if we factor in the SGD 300 million worth of perpetual securities that were issued in June 2019, we believe there is still room for management to make further yield-accretive acquisitions.

At this juncture, we must emphasise that KIT is in a healthy cash position, with its net gearing ratio (net debt-to-assets) coming down substantially to a more favourable 33.7% if we take into consideration its cash holdings.

Looking at the balance sheet, one can find that KIT has borrowings of SGD 2,156 million, of which 95.4% are non-recourse and ring-fenced at the asset level. This means that if any of KIT’s assets were to default on their loans, the lender is not able to seize the assets of KIT. The worst-case scenario, then, is that KIT writes these assets off its books.

KIT has some debt obligations that are due in a year or less. The SGD 700 million KMC loan due in June 2020 is to be refinanced upon maturity. Negotiations with banks are already in progress. As KIT is backed by Keppel Corp, we believe that the loans are likely to be successfully refinanced. Moreover, the Basslink loan due in November 2019 was recently given a 12-month extension.

Strong future growth prospects

The management has indicated that the Trust is able to borrow about SGD 1 billion for acquisitions – a key stock catalyst – to supplement future growth. The ample debt headroom puts KIT in a sufficient and comfortable positive to deliver inorganic growth.

Furthermore, the management has expressed their desire to acquire more evergreen businesses that not only provide essential products to their customers, but are also dominant players in their respective markets.

A prime example would be its latest acquisition of Ixom in 2019, which was DPU yield accretive and a strategic move that would give the Trust a foothold in the stable water industrial and specialty chemicals distribution. Such infrastructure-like businesses are potential acquisition targets for KIT.

Besides acquisitons, there is also organic growth potential in KIT’s existing portfolio due to favourable demand trends. Ixom, for instance, is likely to experience growth in demand for its chemicals due to population growth, high GDP growth in Australia and New Zealand and higher global dairy consumption per capita. Meanwhile, City Gas is expected to experience modest growth due to a steady stream of housing supply, supported by population growth.

Investment risks

Contract renewal risk: As most of KIT’s assets obtain their revenue from long-term contracts, there is the possibility of non-renewal once these contracts expire, the earliest being the Senoko WTE Plant concession (in 2024). While discussions of a renewal for the Senoko WTE plant concession have already started, there is no guarantee that the concession will be renewed, although it must be noted that some of KIT’s contracts have the option to extend for at least another 15 years.

Changes in government policies: Changes in government policies could affect KIT’s concessions. After the completion of the Deep Tunnel Sewage System (DTSS), existing water reclamation plants like the Keppel Seghers Ulu Pandan NEWater Plant would be decommissioned. The land would be cleared for other uses by the government. Hence, there is no guarantee that a concession would be able to last forever, as it is subjected to changes in government policies.

Performance risk: Concession-based assets have contractual obligations to make available a certain capacity. Otherwise, payments will not be received in full. There is a risk of KIT’s assets being unable to meet their service obligations.

From 2018 to 2019, Basslink suffered a few outages that caused it to be unable to receive full facility payments. While Basslink has maintained its position that the six-month outage in 2015 was a Force Majeure Event, the view was strongly disputed by Australian state government enterprise Hydro Tasmania. The arbitration is expected to conclude in 2020.

The good news for unitholders is that KIT is currently not dependent on Basslink’s cash flows for distributions. In the worst case scenario, Basslink will simply be written off from KIT’s books, with no downside to KIT, as Basslink’s loans are non-recourse and ring-fenced at the Basslink level.

On the bright side, should Basslink start contributing to distributable cash flows in the future, we will certainly see a decent increase in distributable cash flows.

KIT offers a potential total return of 14%

Since KIT has been paying out stable distributions every quarter, we use a two-stage dividend discount model (DDM) to value KIT (Table 4). In the first stage, we assumed that distributions will remain stable. The length of the first stage is seven years, after which we expect KIT to acquire additional evergreen assets to replace the Keppel Seghers Ulu Pandan NEWater Plant, which will be decommissioned.

In the second stage, we see potential for dividend growth, and have assumed a conservative growth rate of 1%, derived from the long-term growth estimates for KIT’s existing evergreen businesses.

Using a discount rate of 7.28%, we arrived at a target price of SGD 0.565, which translates to an upside potential of 7% based on last traded price of SGD 0.530 (as of 29 November 2019). Coupled with an estimated distribution yield of 7%, investors could potentially receive a total return of 14%.

Table 4: Dividend discount model for KIT

Key assumptions: | |

Dividends | SGD 0.0372 |

Discount rate | 7.28% |

First stage growth rate | 0.00% |

Second stage growth rate | 1.00% |

Target price | SGD 0.565 |

Current share price | SGD 0.530 |

Upside potential | 7% |

Source: Bloomberg, iFAST Estimates | |

Table 5: KIT’s valuation seems undemanding compared to its peers

Market Cap (SGD mil) | Forward EV/EBITDA | PB Ratio (X) | Dividend Yield (%) | |

Keppel Infrastructure Trust (SGX:A7RU) | 2,647.00 | 16.72 | 1.80 | 7.36 |

Hannon Armstrong (NYSE:HASI) | 2,619.68 | 44.93 | 2.18 | 4.53 |

Macquarie Infrastructure Corp (NYSE:MIC) | 4,977.42 | 10.44 | 1.27 | 9.49 |

CK Infrastructure Holdings (HKEX:1038) | 24,431.22 | 50.72 | 1.31 | 4.54 |

Brookfield Infrastructure Partners (NYSE:BIP) | 28,301.49 | 23.44 | 1.99 | 3.84 |

Source: Bloomberg, iFAST Compilations | ||||

All in all, we believe that KIT is a stock worth considering for income-seeking investors. Its portfolio of infrastructure assets, which offer defensive long-term cash flows, is able to translate into stable distributions to unitholders. KIT is also supported by a strong balance sheet, and is able to deliver value through a combination of organic growth and acquisitions.

(The article was updated on 3 Dec 2019 to include KIT’s reported net gearing ratio.)

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.