- While Asian exports have plunged across this year, promising signs of a recovery in exports have starting to flash across the region, driven by two main catalysts that we believe will progressively materialise over the next few months.

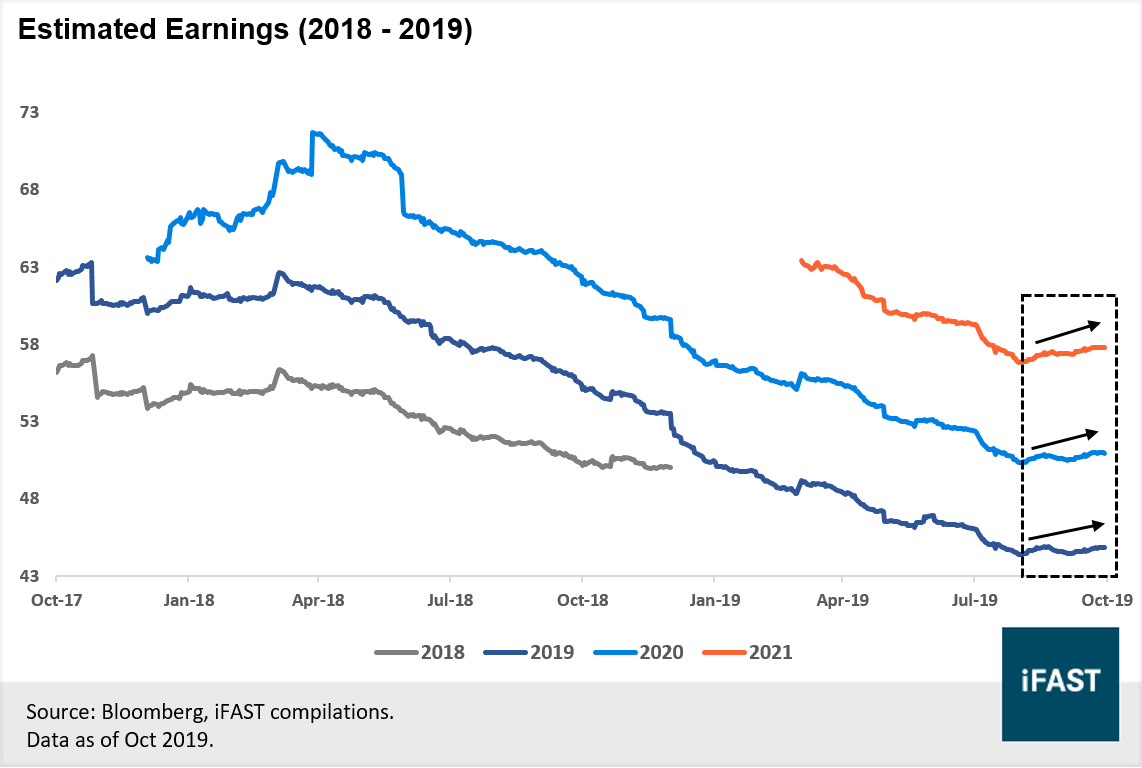

- Profit outlook expected to improve for Asian companies. Earnings estimates across FY 2019, 2020 and 2021 have reversed from their downtrend and have since been revised upwards in September.

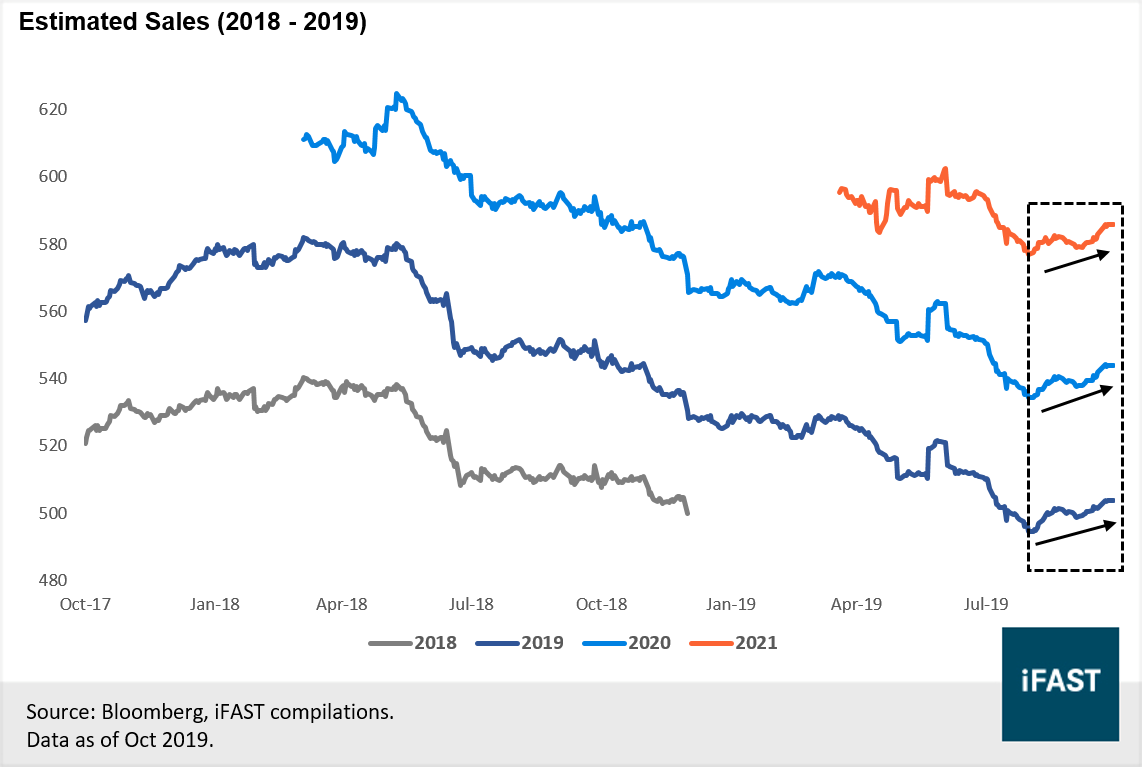

- This is supported by similar trend in sales estimates where estimates for FY 2019, 2020 and 2021 were revised upwards in early September. The improvement in earnings are supported by a fundamental boost in revenue.

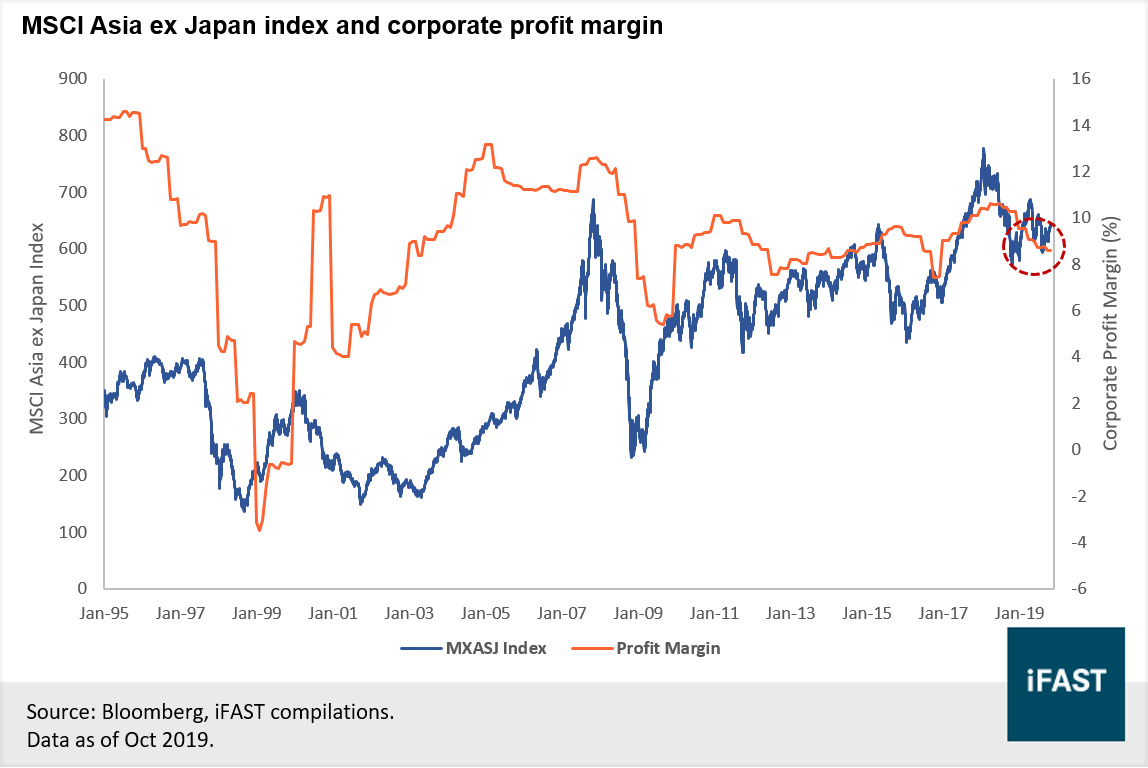

- Profit margins for Asian companies have bottomed out and are expected to rebound. Current level is below ten-year average and significantly below its cycle high. With profit margin at 31 percentile, we believe there is ample headroom to expand thus driving equity prices higher.

- Valuations for MSCI Asia ex Japan remains cheap while supported by robust double-digit earnings growth. Asia ex Japan equity market offers an attractive upside potential of over twenty percent by FY2021.

- Overall, we maintain our star ratings of 4.5 stars “Very Attractive”. It is a good time to build position in Asian equities at the current juncture, ahead of its expected exports recovery and while valuation remains cheap.

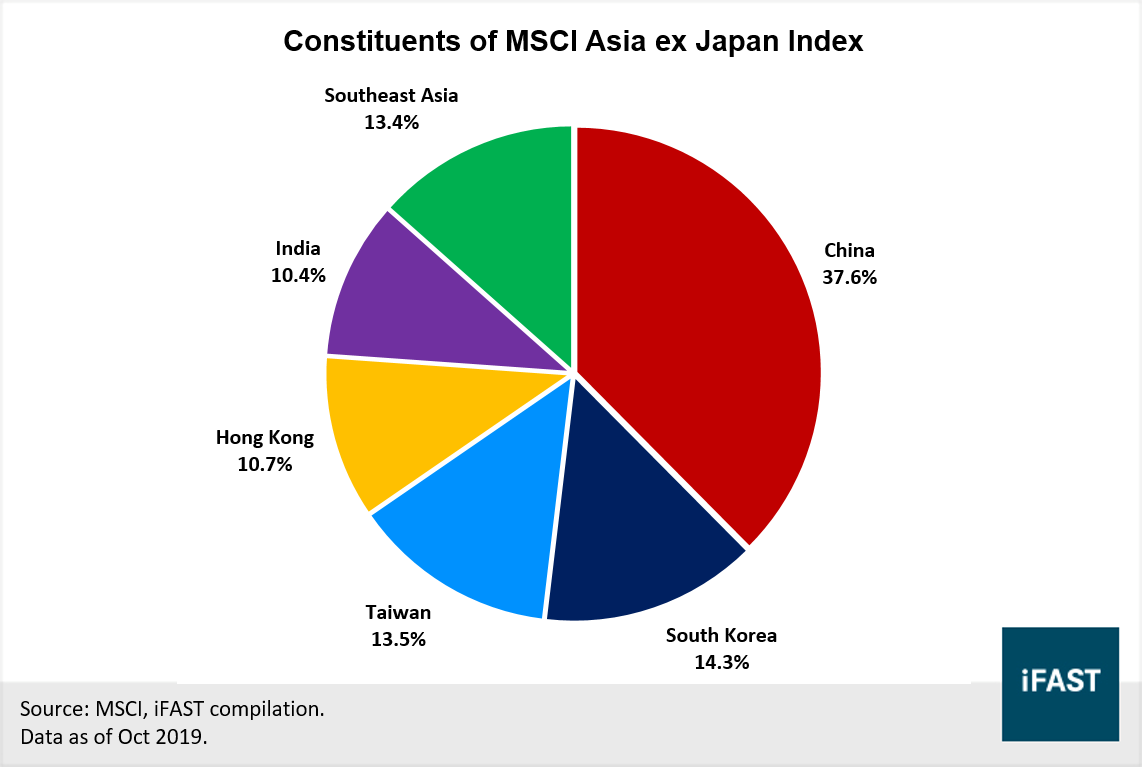

Chart 1: Constituents of MSCI Asia ex Japan Index

|

Markets |

FY2021 |

|

China (A-Shares) |

33% |

|

Hong Kong |

66% |

|

South Korea |

34% |

|

Taiwan |

17% |

|

India |

7% |

|

Southeast Asia |

18% |

|

Source: Bloomberg, iFAST estimates. |

|

Outlook for individual Asian markets

China – Highly Attractive (4.0-4.5 stars of 5; China-A and China-H respectively)

Hong Kong – Highly Attractive (4.5 stars of 5)

South Korea – Highly Attractive (4.5 stars of 5)

Taiwan – Highly Attractive (4.0 stars of 5)

India – Attractive (3.0 stars of 5)

Southeast Asia – Attractive (3.0-4.0 stars of 5)

Profit outlook expected to improve for Asian companies

Chart 2: Earnings estimates for FY 2019, 2020 and 2021 have rebounded

Chart 3: Sales estimates for FY 2019, 2020 and 2021 have also rebounded

Profit margin for Asian companies likely to expand

Chart 4: Profit margin are almost at cycle-low and have likely bottomed out

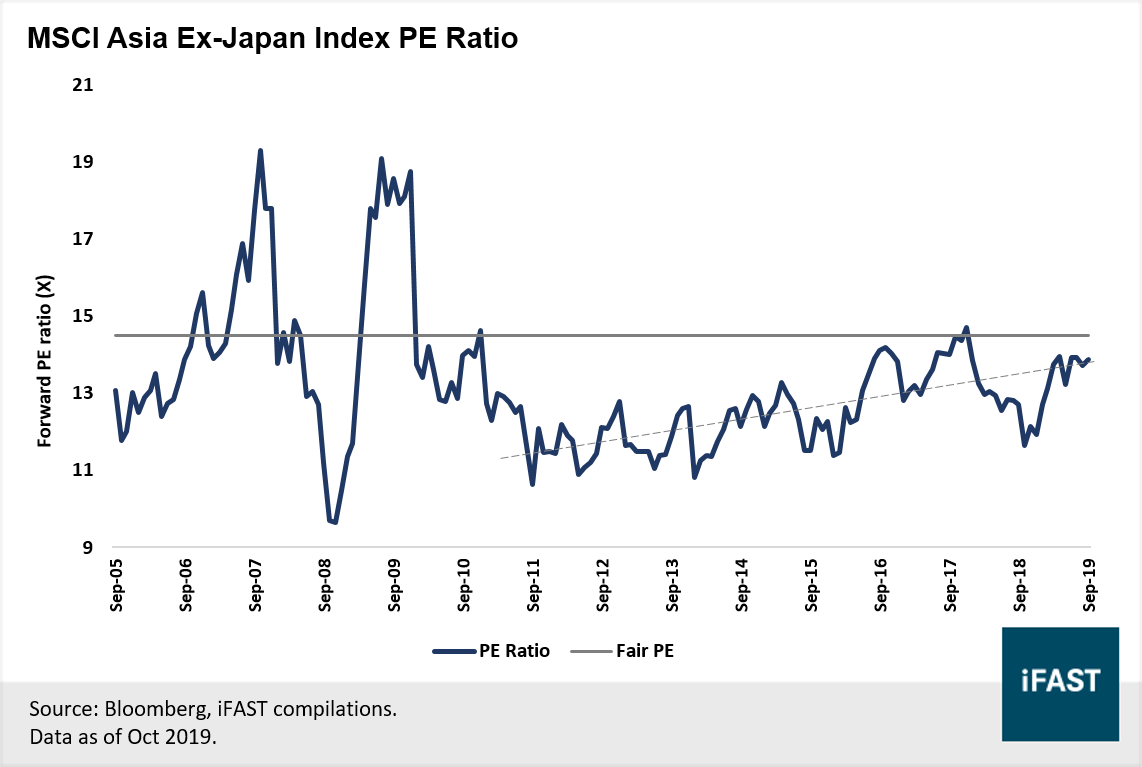

Attractive Valuation and Earnings Growth

Table 2: Asia ex-Japan index offer decent upside potentials, thanks to its reasonable valuation and robust earnings growth

| MSCI Asia ex-Japan Index | FY2018 | FY2019 | FY2020 | FY2021 |

| Price-Earnings Ratio (X) | 13.5 | 14.7 | 12.9 | 11.4 |

| Expected Earnings Growth YoY% | 2.6% | -8.4% | 13.9% | 13.5% |

| Earnings Per Share (EPS) | 47.3 | 43.3 | 49.4 | 56.0 |

Projected

Fair Price (Based on Fair PE ratio of 14.5X) |

- | - | 716 | 812 |

| Potential Upside from Today (%) | - | - | - | 26% |

| Source: Bloomberg, iFAST estimates. | ||||

Chart 5: Asia ex-Japan index current trades below our fair PE valuation

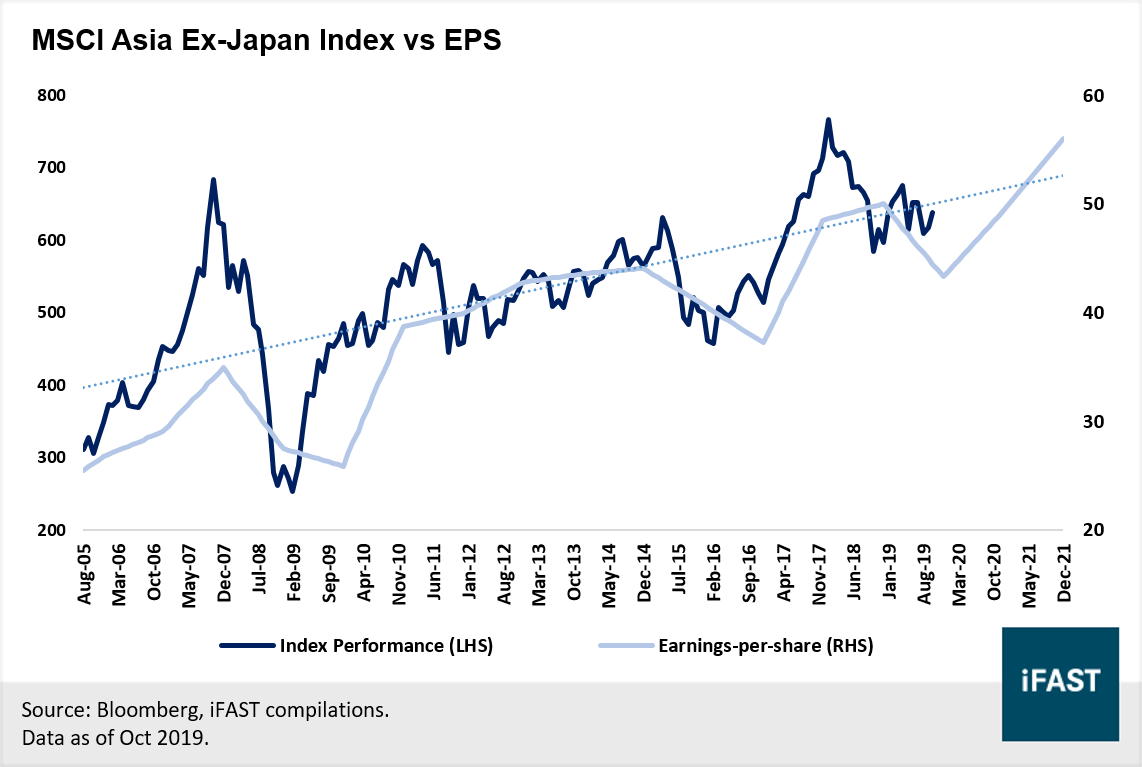

Chart 6: MSCI Asia ex-Japan index and its underlying earnings trend upwards across the longer term

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.