- Hong Kong, one of Asia’s most prominent financial centre, has been embattled with waves of protests and public demonstrations in the past three month.

- While the protests remain the biggest drag on sentiment, we believe their impact on Hong Kong’s economy and its underlying corporate earnings are fairly limited. Current weakness in Hong Kong’s equities are better explained by the soft macroeconomic conditions within the Greater China region, evident via a moderating GDP growth.

- Across this year, China has started to ramp up efforts in boosting liquidity, retail consumption and industrial output. Looking ahead, we expect to see signs of improvement in economic data for the Greater China region in the next few quarters, which in turn will progressively lend support to greater optimism ahead.

- We think investors’ concerns for the current political unrest and its impact on Hong Kong equities are overblown. The combination of an attractive valuation (currently near its historical low), easing trade tensions and stimulus measure from Beijing will help lift the Hang Seng Index (HSI).

- The risk-reward ratio of an investment in Hong Kong stocks is currently skewed towards the upside, with HSI presenting potential upsides of about 22% and 31% by end-2020 and end-2021 respectively.

- Thus, we maintain our star ratings of 4.5 stars “Very Attractive” rating for Hong Kong equity market.

Political uncertainty tainted macro outlook

(i) A dampening of consumer confidence and thus weakening domestic demand which is reflected by moderating retail sales (Chart 1);

(ii) Decline in business investments as companies lose confidence in Hong Kong’s prospects;

(iii) Fall in tourist arrivals and consequently a contraction in tourism-oriented sales.

Chart 1: Retail sales suffered due to social unrest

Consumption to remain resilient in the face of headwinds

Chart 2: Investments have also decelerated but consumption remains resilient

Chart 3: Quarterly GDP growth fell and is expected to remain muted

Impact of social unrest largely isolated to tourism-oriented industries

Chart 4: Real Estate and Consumer Discretionary sector account for total weightage of 15% in Hang Seng Index.

Chart 5: Share prices of Hong Kong retail mall operators were badly beaten down since start of the protests.

Limited impact of social unrest on overall corporate earnings

Chart 6: Majority of HSI’s underlying revenue is derived from Mainland China region

Chart 7: The substantial earnings downgrades meant that negatives are mostly priced in

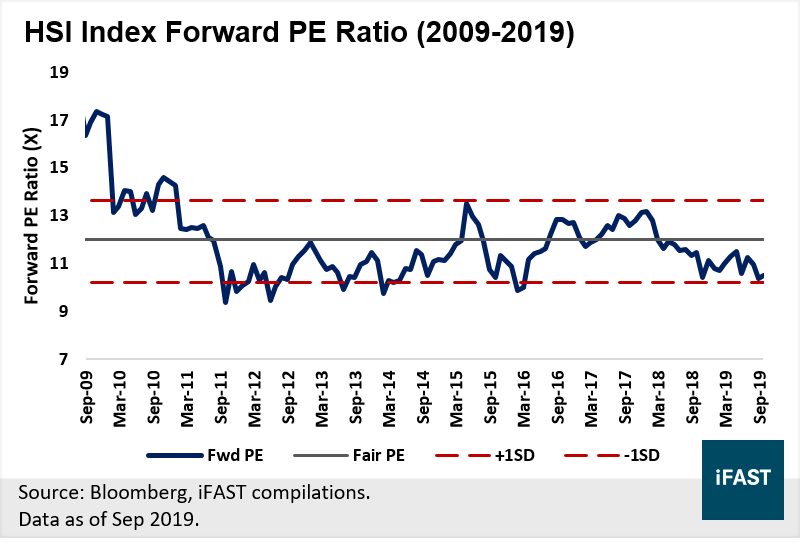

Beaten down valuation offers attractive upside potential for Hong Kong equities

Chart 8: HSI Index is currently trading at one standard deviation below its ten-year average.

Table 1: Upside Potential of Hang Seng Index

|

Hang Seng Index |

FY2018 |

FY2019 |

FY2020 |

FY2021 |

|

12M Forward PE Ratio (X) |

10.8 |

10.4 |

9.9 |

9.1 |

|

Expected Earnings Growth YoY |

8% |

4% |

6% |

8% |

|

Earnings Per Share (EPS) |

2398 |

2501 |

2663 |

2879 |

|

Projected Fair Price (HKD) |

- |

- |

31,957 |

34,545 |

|

Potential Upside from Today (%) |

- |

- |

+22% |

+31% |

Source: Bloomberg, iFAST compilations.

Take part in the attractive upsides offered by Hong Kong equity market!

Chart 9: Resiliency in HSI earnings lend support to a near-term recovery in HSI index performance

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.