- UMS stock is up 35% year-to-date, supported by robust 1H25 results with semiconductor revenue up 17% YoY and Malaysia revenue surging 250%.

- The global semiconductor industry is entering a new upcycle, driven by AI, high-performance computing, and advanced data storage. Southeast Asia’s growing role in the supply chain positions UMS to capture outsized benefits.

- Revenue visibility is underpinned by a major new customer ramp and a new product order from key partner Applied Materials (AMAT), both set to contribute meaningfully to earnings growth.

- Malaysia dual listing and MAS EQDP boost visibility, liquidity, and funding flexibility, enhancing UMS’s ability to pursue expansion and strategic investments.

- While UMS trades above historical averages, this aligns with a broader sector rerating. We raised the fair P/E multiple to 15x, deriving a 2027 target price of SGD 1.26 (adjusted for the 1-for-4 bonus issue effective 9 Jan 2026)

Solid growth momentum in 1H2025

UMS Integration (formerly known as UMS Holdings) delivered a strong set of results in 1H2025, underpinned by robust operational and financial performance. The stock has rallied 35% year-to-date, reflecting growing investor confidence. Group net profit rose 6% year-on-year to SGD 23.4 million, supported by a 14% increase in sales to SGD 125 million. Profitability also improved, with gross margins expanding to 55.1% from 53.3% in 1H2024, largely due to a more favourable product mix. The Group also maintained a healthy financial position, generating positive operating cash flow of SGD 15.2 million in 1H2025, up from SGD 14.3 million a year earlier.

The semiconductor segment remained the key growth driver, contributing 85.9% of total revenue and recording a 17% year-on-year increase. Aerospace and other businesses accounted for 9.2% and 4.8% respectively.

Figure 1: Semiconductor and aerospace segments reported year-on-year revenue increase in 1H25

Geographically, Singapore continued to dominate with 63% of revenue. Notably, Malaysia emerged as the second-largest market, overtaking the US with a sharp 250% year-on-year increase to 13.9% of revenue, driven by the ramp-up of a new customer. This shift underscores UMS’s success in broadening both its production base and customer mix.

Figure 2: Malaysia surges to become UMS’s second-largest market with revenue share rose from 4.5% in 1H24 to 13.9% in 1H25

Related Article: UMS Holdings: A hidden opportunity to ride on Singapore’s semiconductor upcycle

Global semiconductor upswing and Southeast Asia’s rising role

The semiconductor industry is in the midst of a strong multi-year upcycle, fuelled by structural demand for AI chips, high-performance computing, and advanced data storage. Industry bodies project strong momentum ahead: SEMI forecasts 18 new fab construction projects commencing in 2025, while wafer fab equipment (WFE) spending is expected to grow 2.8% in 2025 and accelerate by 15% to USD 69.3 billion in 2026, driven by next-generation device architectures such as gate-all-around (GAA) and capacity expansions. The Semiconductor Industry Association (SIA) also anticipates double-digit market growth in 2025, reinforcing the sector’s trajectory toward USD 1 trillion by 2030.

At the regional level, Southeast Asia is emerging as a key beneficiary of this global uptrend. The region’s share of the assembly, testing, and packaging (ATP) market is projected to rise from 20% in 2022 to 27% by 2032, supported by “China plus one” and “Taiwan plus one” diversification strategies as well as supply chain realignments prompted by US tariffs. Singapore and Malaysia, in particular, stand out as critical nodes in this ecosystem. Singapore enjoys the lowest baseline US tariff rate at 10% and continues to strengthen its competitiveness in chip design and advanced manufacturing. Malaysia, meanwhile, remains a global leader in ATP while attracting major equipment makers. Recent industry developments underscore this trend: in April 2025, United Microelectronics Corporation (UMC), one of the world’s top five foundries, opened a new plant in Singapore, which will expand its annual wafer capacity by nearly 50% once fully operational.

Against this constructive backdrop, UMS is well positioned to capture incremental growth. This positive outlook is further reinforced by encouraging 2025 guidance from UMS’s key semiconductor customers, underpinned by accelerating AI-driven investments and sustained end-market demand.

Related Article: Singapore Semiconductor Stocks Set to Shine on AI, 5G, and EQDP Tailwinds

Customer expansion and capital access driving growth visibility

UMS’s growth trajectory is underpinned by both new customer wins and deepening partnerships with existing clients. The Group’s Penang facility, which began operations in 2024, has quickly gained momentum with a major ramp-up from new customer Lam Research. This ramp generated approximately SGD 20 million in revenue in FY2024, and management expects contributions to more than double in FY2025. Based on the company’s projection of reaching SGD 1.5 million in weekly sales from this customer by end-2025, we expect revenue contribution to reach around SGD 40 million for FY2025, representing about 20% of UMS’s 2024 semiconductor revenue. The Penang site also offers scalability for future growth, with adjacent land already secured for potential expansion and improved new product introduction (NPI) throughput to drive operating leverage as volumes increase.

At the same time, Applied Materials (AMAT)—UMS’s most critical partner and the global leader in its segment with 60–80% market share—continues to anchor UMS’s revenue base. UMS currently supplies more than half of AMAT’s tool demand and has secured a new product order scheduled for production in 4Q2025. If successfully executed, this program could contribute up to 20% of UMS’s existing AMAT-related revenue, further diversifying income streams while reinforcing its strategic importance to AMAT.

Beyond semiconductors, UMS is also strengthening its aerospace division, supported by a post-pandemic recovery in air travel and record-high passenger load factors. The rebound in commercial aviation is driving demand for new aircraft and related services, with the aerospace industry projected to grow at a CAGR of 5.8% between 2024 and 2028. To capture this opportunity, UMS is deepening collaborations with existing aerospace clients, with several new components currently in the qualification stage and expected to move into full-scale production upon customer approval. This not only broadens its growth prospects but also enhances earnings diversification.

UMS also benefits from enhanced capital access and market visibility, which strengthen its ability to fund future growth. Its secondary listing in Malaysia broadens the investor base, improves liquidity, and positions the company to benefit from higher peer valuations, with Malaysian semiconductor companies often trade above 20x forward P/E—well above UMS’s Singapore multiple. This valuation gap underscores the potential for a rerating, particularly given UMS’s stronger margins relative to many Malaysian peers. In addition, UMS stands a strong chance of being a beneficiary of the MAS EQDP and enhanced GEMS programs, which would further elevate its visibility among global investors, lower its cost of capital, and improve funding flexibility. Collectively, these initiatives enhance UMS’s financial capacity to drive expansion and strategic investments while reinforcing investor confidence in its long-term growth trajectory.

Figure 3: Malaysian listed semiconductor and precision engineering companies often trade above 20x forward P/E

Related Article: 8 Potential EQDP Winners to Watch

Investment risks: customer dependence and margin pressures

Despite its strong growth prospects, UMS faces several risks that investors should monitor closely. The most significant is its high customer concentration with Applied Materials (AMAT), which has accounted for around 69% of Group revenue over the past four years. This dependence creates revenue vulnerability, as any slowdown or disruption in AMAT’s business might cascade into UMS’s order flow. This risk is amplified by AMAT’s significant exposure to Greater China and Taiwan—markets currently affected by escalating geopolitical tensions and US export restrictions on advanced semiconductor equipment. AMAT’s management has flagged near-term headwinds, citing capacity digestion in China and volatile demand from leading-edge customers, which could translate into weaker demand for UMS’s precision components. However, the onboarding of Lam Research marks a meaningful step toward diversifying UMS’s customer base and reducing reliance on a single demand source.

UMS is also contending with margin pressures from rising operating costs. Its Malaysian hub in Penang faces talent shortage as competition for skilled labour intensifies, driving higher personnel expenses, as reflected in 1H2025 results. The company is addressing this through factory automation and staff retention initiatives, though these will take time to fully mitigate cost escalation. On top of labour challenges, foreign exchange volatility adds another layer of risk. The Group’s sales are denominated across multiple currencies, while only around 30–40% of its production costs are in USD. This currency mismatch means that a sustained weakening of the US dollar may erode profit margins, as revenue translated into local currency may decline more sharply than the partial cost savings from USD-denominated inputs. And because contracts and competition limit price increases, it may be difficult for UMS to pass higher input costs onto customers. Consequently, the company’s operating margins face challenges if wage and FX pressures persist.

Attractive upside potential underpinned by earnings growth and multiple expansion

UMS currently trades at a price-to-earnings (P/E) ratio above its 10-year historical average, which at first glance may appear stretched. However, this premium should be viewed within the context of a broader sectoral re-rating rather than stock-specific speculation. Across the semiconductor value chain, both local and regional peers are trading well above their long-term averages, reflecting a structural shift in investor sentiment. The ongoing AI-driven upcycle has enhanced earnings visibility across the sector, leading investors to assign higher multiples to semiconductor names that were historically undervalued. UMS’s re-rating therefore appears justified, underpinned by its double-digit EPS growth outlook, expanding customer base, and increasing geographic diversification.

Figure 4: Singapore semiconductor supply chain companies are trading above their 10-year average P/E

Taking these factors into account, we raise our fair P/E multiple for UMS from 12x to 15x, one standard deviation above its 10-year forward average. We expect strong earnings growth in 2026, as revenue contribution from the new customer is still ramping up in 2025, and likely to be fully realised from 2026 onwards. Applying this to our estimated 2027 earnings, we derive a target price of SGD 1.26 (adjusted for the 1-for-4 bonus issue effective 9 Jan 2026), representing a 5.9% upside from the price of SGD 1.19 as at 12pm on 9 Jan 2026.

Figure 5: 10-year average forward P/E

Table 1: Valuation table (post 1-for-4 bonus issue)

|

2024 |

2025E |

2026E |

2027E |

|

|

P/E Ratio (X) |

22.6 |

22.2 |

17.5 |

14.2 |

|

Earnings Growth |

-34.7% |

17.5% |

26.9% |

23.5% |

|

Projected Earnings Per Share (EPS) |

0.046 |

0.054 |

0.068 |

0.084 |

|

Target Price (Based on 15x fair P/E Ratio) |

- |

- |

- |

1.26 |

|

Upside Potential |

- |

- |

- |

5.9% |

|

Source:

Bloomberg Finance L.P., iFAST Estimates |

||||

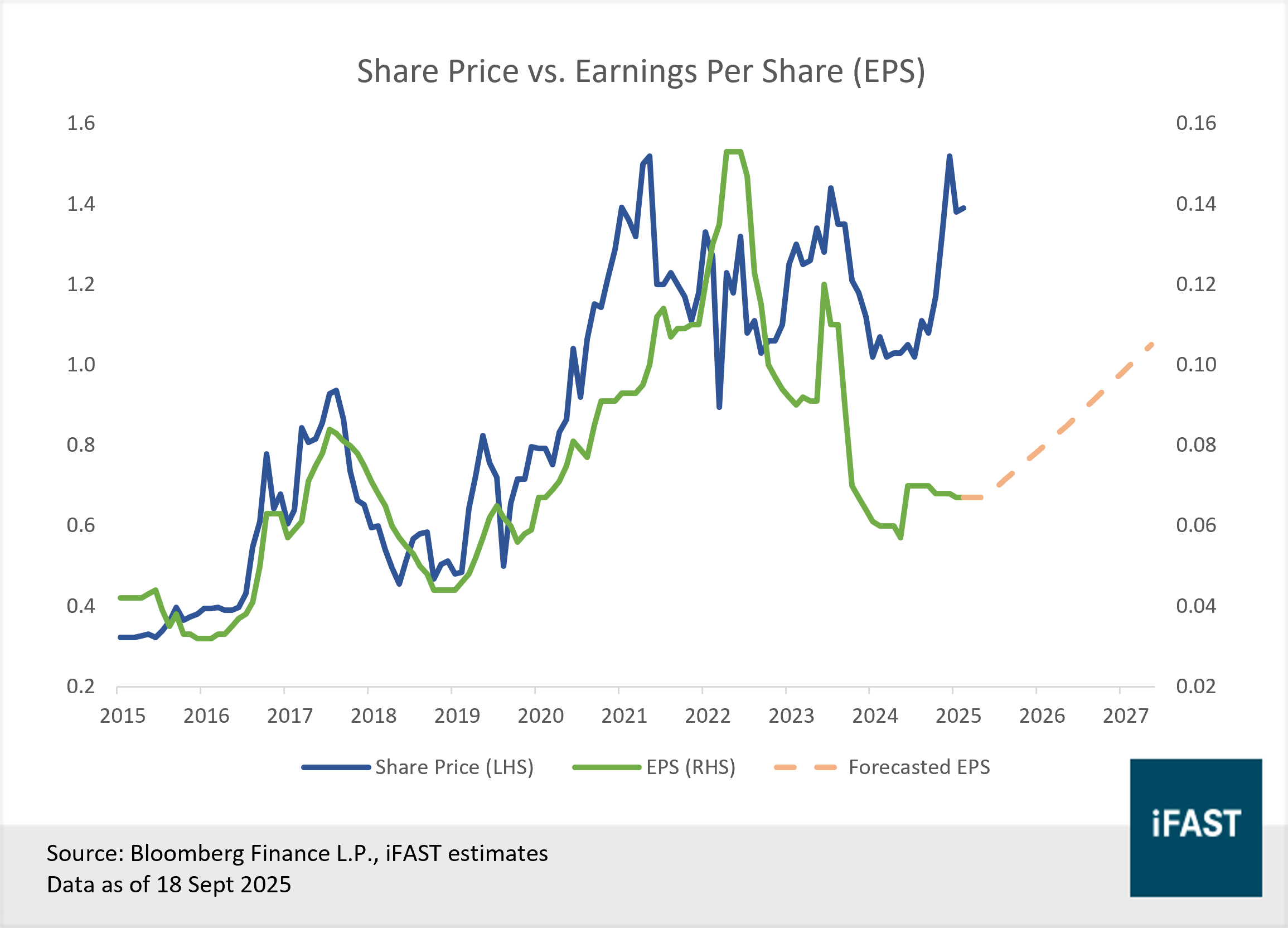

Figure 6: Share price vs. EPS (before 1-for-4 bonus share issue)

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.