Key Points

- For decades, there has been no bigger winner on the global stage than the US. However, with a new world order taking shape, diversification has taken on added importance.

- With no real clarity over tariffs, US businesses are faced with an unprecedented level of uncertainty, which has been further compounded by other factors.

- Correlations have changed dramatically this year, helping to enhance the appeal of diversification as a risk-mitigation strategy.

- For investors seeking global diversification away from the US, a simple and highly cost-effective option is the Vanguard FTSE All-World ex-US ETF (NYSE:VEU).

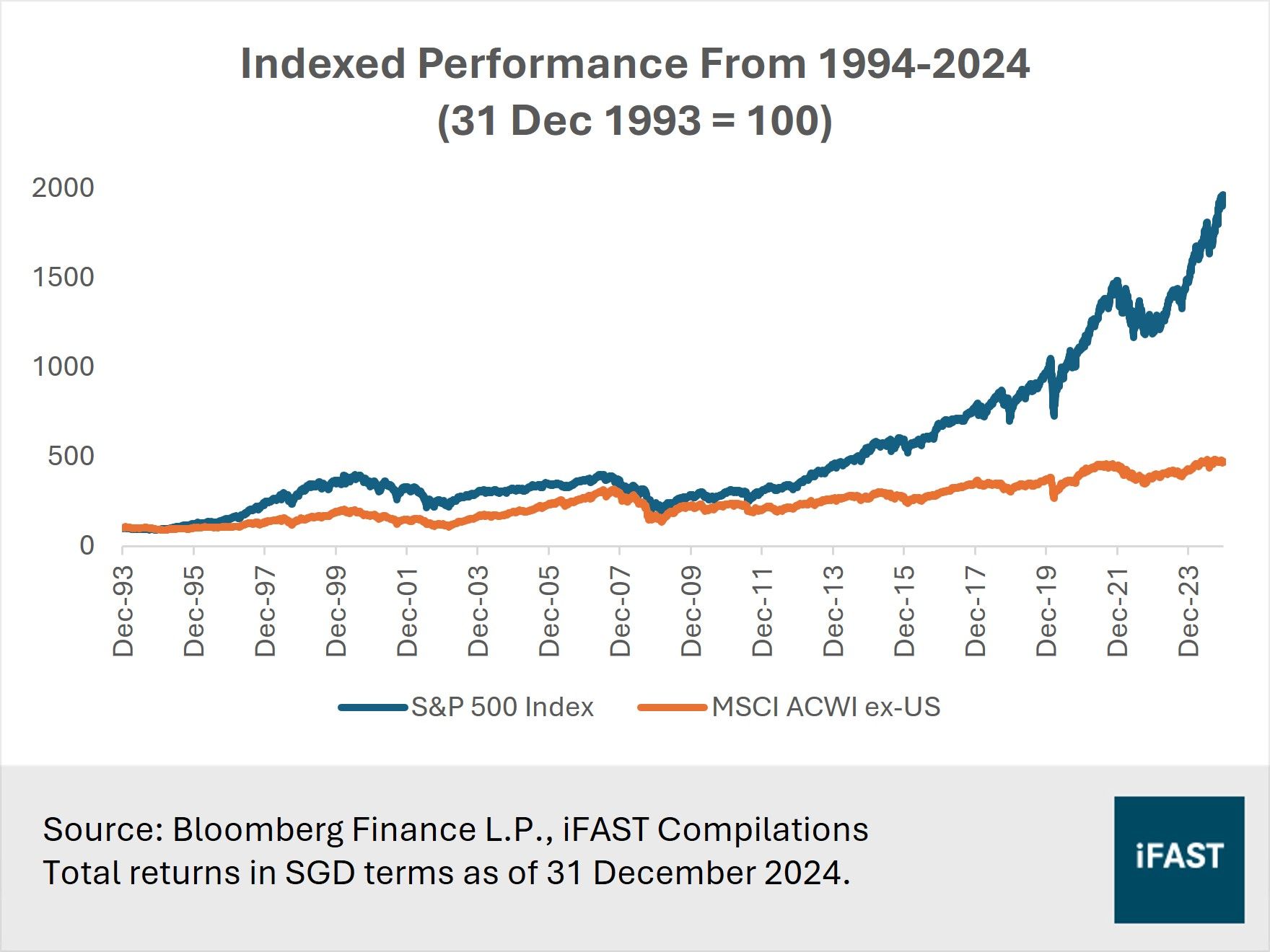

For the past three decades, global diversification has underwhelmed.

Over the period from 1994 to 2024, US equities have consistently outperformed their international counterparts (Chart 1). The S&P 500 has delivered an annualised return of 10.0%, compared to just 5.1% for non-US equities (in SGD terms). For many young investors, it’s hard to recall a time when the US did not dominate global markets. As a result, global diversification has long been a losing strategy for most investors.

Chart 1: US has consistently outperformed non-US equities

Not this year.

The ‘Liberation Day’ market crash sparked by Donald Trump’s tariffs has coincided with rallies in other global markets, including Europe and China. While the S&P 500 is nursing a loss of -4.6% year-to-date, the MSCI AC World ex-US Index is up by 8.0% over the same period. Meanwhile, the STOXX 600 and the MSCI China Index have delivered far superior returns of 14.7% and 6.9% respectively (returns in SGD terms as of 31 May 2025). While periods of underperformance by the US are not unusual, the gap this year has been particularly pronounced.

Is global diversification finally back in vogue?

Admittedly, it is difficult to draw any firm conclusions from just a few months of performance. However, a significant catalyst for global diversification this year has been Trump’s chaotic trade war, particularly between the US and China, which has not only been highly unpredictable but also deeply disruptive to global markets. While we are not calling for an end to US exceptionalism, we believe there is now a stronger case for investors to consider greater global diversification in their equity allocations.

A new world order is taking shape

For decades, there has been no bigger winner on the global stage than the US market, with its stellar performance over the years leading to an approximate 63.7% weighting in the MSCI AC World Index (as of 30 April 2025), up from 43.3% back in 2011.

And rightfully so. Investors were drawn to America’s exceptionalism: its technological dominance, deep and liquid financial markets, leadership in free trade, willingness to underwriting global security, and a government historically seen as a wise steward of the economy.

However, President Trump’s erratic policies – including his on-again, off-again tariff announcements and escalating trade tensions with China – along with his transactional approach to diplomacy, suggest a significant shift in America’s position on the world stage. This has prompted the rest of the world to diversify trade partners, forge new alliances, and pursue long-delayed economic reforms to boost growth and economic resilience.

The European Union (EU), for instance, has launched a charm offensive to diversify its trade alliances in Asia and beyond. The bloc has resumed long-stalled negotiations with several countries, including India, Malaysia, and Thailand.

The clearest sign of the EU’s renewed urgency is its revived deal with MERCOSUR, a South American trade bloc that includes Brazil and Argentina. After 25 years of delay, an agreement was finally reached in December last year. While major European countries such as France and Poland remain opposed, Trump’s tariffs could push them towards ratification. Austria, a staunch critic of the deal, has already abandoned its long-standing resistance to the trade agreement.

Furthermore, with the US now stepping back from European security, the continent has significantly ramped up its defence spending. Even German lawmakers have voted to loosen the purse strings, allowing for a huge increase in defence and infrastructure investment – a seismic shift for a country traditionally known for its pacifism and fiscal restraint. The recently concluded UK-EU deal has also drawn a line under Brexit, signalling the start of a much closer relationship.

While Europe has long been criticised for its excessive bureaucracy, Trump’s assault on the rule of law in the US has suddenly made European institutions more attractive to businesses – Europe’s checks and balances are at least not in doubt.

Related articles:

European defence stocks rally amid growing transatlantic divide: A paradigm shift?

Neutral on Europe, But Bright Spots Remain

Changes are afoot in China too.

Five years ago, regulators in China launched a sweeping crackdown on technology companies, casting a chill over the private sector. Now, the mood is shifting. Amidst China’s economic challenges, the government has recognised that revitalising the private sector is crucial to achieving an economy recovery – a task made even more urgent by Trump’s tariff war. President Xi Jinping’s handshake with Jack Ma – widely seen as the face of China’s private sector but sidelined by authorities since the crackdown – at a symposium this year is the surest signal that the party wants the private sector to thrive again.

China has also intensified its efforts to steer the economy toward a consumption-led growth model. A raft of stimulus measures, coupled with a revival in consumer and business confidence, is laying the groundwork for a sustained recovery. The government’s strategic focus on artificial intelligence is also providing new momentum for tech leaders. Meanwhile, the recent revival of China’s economic dialogues with Japan and South Korea – both of which have aligned more closely to the US in recent years – suggests that regional powers are reassessing their relationships in response to Trump’s tariff-induced uncertainty.

Related article:

China Scores Early Gains in the US Tariff Dispute: The Dark Horse of 2025?

At the same time, the economic transformation in Japan continues, with inflation, wage increases, and interest rate hikes all becoming entrenched. A virtuous cycle of rising wages and prices will stimulate consumption and capital expenditures, opening up a pathway for stronger economic growth in the longer term.

Besides, Japan has shown that it can and will step up to provide international economic leadership. In the absence of the US, Japan has picked up the mantle of leadership in the Regional Comprehensive Economic Partnership (RCEP) and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). As the US retreats from its traditional role as champion of free trade, Japan will likely step up to fill the void and provide trade leadership together with other open-market allies.

As a new world order takes shape, the global economy likely to become more balanced, with Europe and Asia shouldering more responsibilities for driving growth and providing international leadership. Against this backdrop, diversification has taken on added importance in our portfolios.

An unprecedented level of uncertainty persists

Another reason for diversification: a great deal of uncertainty persists.

Start with the tariffs. In just a matter of days, Trump’s ‘Liberation Day’ tariffs have injected the global economy with extraordinary levels of volatility and uncertainty. Trade decisions – along with a slew of other major policy decisions – are now made on Truth Social, often catching even his own advisers off guard.

While the tariffs have since been paused, they have not been cancelled. The outcome of ongoing trade negotiations remains uncertain, and there’s a possibility that the punishingly high tariff rates could be reinstated once the deadline passes. The situation looks increasingly fragile. The US-China truce is already at risk of falling apart, with both sides trading accusations of wrongdoing. Trump’s recent decision to double steel tariffs has also thrown bilateral trade talks into disarray.

As if that weren’t enough, the legal wrangling over the tariffs have added yet another layer of uncertainty. Most recently, a US trade court blocked the tariffs, ruling that Trump had overstepped his authority – only for them to be reinstated a day later, pending the appeal process. Trade talks will now be complicated by doubts over the administration’s authority to follow through on its threats. Rather than offering relief, the development has introduced new complications at the worst possible time. Besides, even if trade deals are struck before the deadline, there’s no guarantee they will hold. Given the unpredictable – and often arbitrary – nature of Trump’s decision-making, he could very well renege on these deals.

With no real clarity ahead, US businesses are faced with an unprecedented level of uncertainty, which has been further compounded by other factors.

Trump has publicly condemned companies that have expressed concerns over his tariffs, including Apple – with proposed tariffs on iPhones made outside of the US – and Mattel, threatening the company with a 100% tariff. At the same time, Trump’s bullying of countries has also severely damaged the reputation of US firms, prompting a backlash against US brands by international consumers. Tesla is perhaps the most prominent example: sales of new Tesla cars in Europe plunged 49% in April from a year ago, even though overall electric car sales rose 27.8%.

Lower market correlations help enhance diversification

As a risk-mitigation strategy, diversification only reduces volatility if the markets involved have low or negative correlations. If all markets move in lockstep, it doesn’t matter how many geographic regions you invest – diversification won’t reduce risk. This has certainly been the case over the past two decades, as correlations between US and non-US stocks have risen significantly. In other words, most international markets have moved in tandem with the broader US market.

Correlations have changed dramatically this year.

Over the past 20 years, the correlation in weekly returns between US and non-US equities stood at 0.81. In the first five months this year, that correlation has dropped to 0.60. The correlations of major markets to the S&P 500 Index have also fallen across the board (Table 1). Admittedly, it is difficult to draw any firm conclusions from just a few months of data. Still, if recent events are any indication, there is now a stronger case for investors to consider greater global diversification in their equity allocations, especially against the backdrop of Trump’s erratic policy agenda.

Table 1: Correlations with the US market have fallen this year

|

Correlation To US (Jan 04 – Dec 24) |

Correlation To US (Jan 25 – May 25) |

|

|

Non-US Stocks |

0.81 |

0.60 |

|

Europe |

0.81 |

0.65 |

|

Japan |

0.64 |

0.63 |

|

Asia ex-Japan |

0.64 |

0.39 |

|

Emerging Markets |

0.70 |

0.29 |

|

China |

0.49 |

0.06 |

|

Source: Bloomberg Finance L.P., iFAST Compilations. US = S&P 500 Index; Non-US Stocks = MSCI ACWI ex-US; Europe = STOXX 600 Index; Japan = Nikkei 225 Index; Asia ex-Japan = MSCI AC Asia ex-Japan Index; Emerging Markets = MSCI Emerging Markets Index; China = MSCI China Index. |

||

Consider a global ex-US ETF

For investors seeking global diversification away from the US, one approach is to re-allocate capital to key markets like Europe, Japan, and China. However, a simpler and more efficient way to achieve diversification is to just invest in a global ex-US ETF like the Vanguard FTSE All-World ex-US ETF (NYSE:VEU).

This ETF seeks to replicate the performance of the FTSE All-World ex US Index, which includes large- and mid-cap stocks from developed and emerging markets outside the US. With an expense ratio of just 0.04%, VEU is a highly cost-effective option that closely tracks its underlying index. Another low-cost option is the Vanguard Total International Stock ETF (NASDAQ:VXUS), which offers similar exposure but also includes small-cap stocks. As a bonus, VXUS is included in our ETF Regular Savings Plan (RSP).

Table 2: Comparison of selected global ex-US ETFs

|

Name of ETF |

Expense Ratio |

Avg Daily Vol (mil) |

AUM (USD bil) |

|

Vanguard FTSE All-World ex-US ETF (NYSE:VEU) |

0.04% |

3.0 |

44.54 |

|

Vanguard Total International Stock ETF (NASDAQ:VXUS) |

0.05% |

4.5 |

92.68 |

|

iShares MSCI ACWI ex US ETF (NASDAQ:ACWX) |

0.32% |

1.6 |

6.28 |

|

iShares Core MSCI Total International Stock ETF (NASDAQ:IXUS) |

0.07% |

2.9 |

44.41 |

|

Xtrackers MSCI World ex USA UCITS ETF 1C USD (LSE:EXUS) |

0.15% |

1.3 |

2.86 |

|

Amundi MSCI World Ex USA ETF Acc (LSE:WEXU) |

0.15% |

0.1 |

0.51 |

|

Source: Bloomberg Finance L.P., iFAST Compilations Data as of 31 May 2025 |

|||

To conclude, we’re not suggesting an end to US exceptionalism. The US remains the largest and most liquid market in the world. It is also home to many high-quality companies that are dominant in the digital economy and semiconductor space. While it might be easy to boycott a company like Tesla due to the availability of alternatives, it's much harder to avoid companies like Google or NVIDIA. Therefore, maintaining exposure to the US remains important. However, for investors who already have a substantial US allocation, a global ex-US ETF can provide substantial diversification benefits.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.