- On 12 May, the US slashed tariffs on Chinese goods to a combined 30% from a previous peak of 145%, triggering a broad rally in Chinese equities.

- Both China and US appear to recognise that full trade decoupling would be mutually damaging. China’s strategic use of rare earth export controls, agricultural import restrictions, and trade diversification likely strengthened its negotiating hand.

- While trade tensions have temporarily eased, future risks remain. Trump’s unpredictable trade stance and misaligned objectives between the US and China suggest that negotiations ahead will be more complex.

- With the current 30% tariff level, China’s 2025 GDP growth is projected to be trimmed by just 0.3 percentage points — significantly less than the previously estimated 1-point drag.

- Chinese technology firms remain well-positioned, with limited exposure to international markets and strong domestic earnings momentum driven by consumption policies and AI development.

- Chinese equities remain investable. The MSCI China Index is projected to reach HKD 85.8 by FY2027, representing a 13.2% upside.

Global markets roared on 12 May 2025 after US and China unveiled a surprise tariff rollback. In a move that far exceeded market expectations, the US announced a sweeping cut in tariffs to 30% on Chinese imports. The figure includes a 10% “reciprocal” tariffs and a 20% tied to fentanyl concerns.

China responded in kind, slashing duties on US goods to 10% and rolling back a swathe of non-tariff barriers. While the full details of China's easing have yet to be disclosed, the broad outlines were enough to send risk assets soaring.

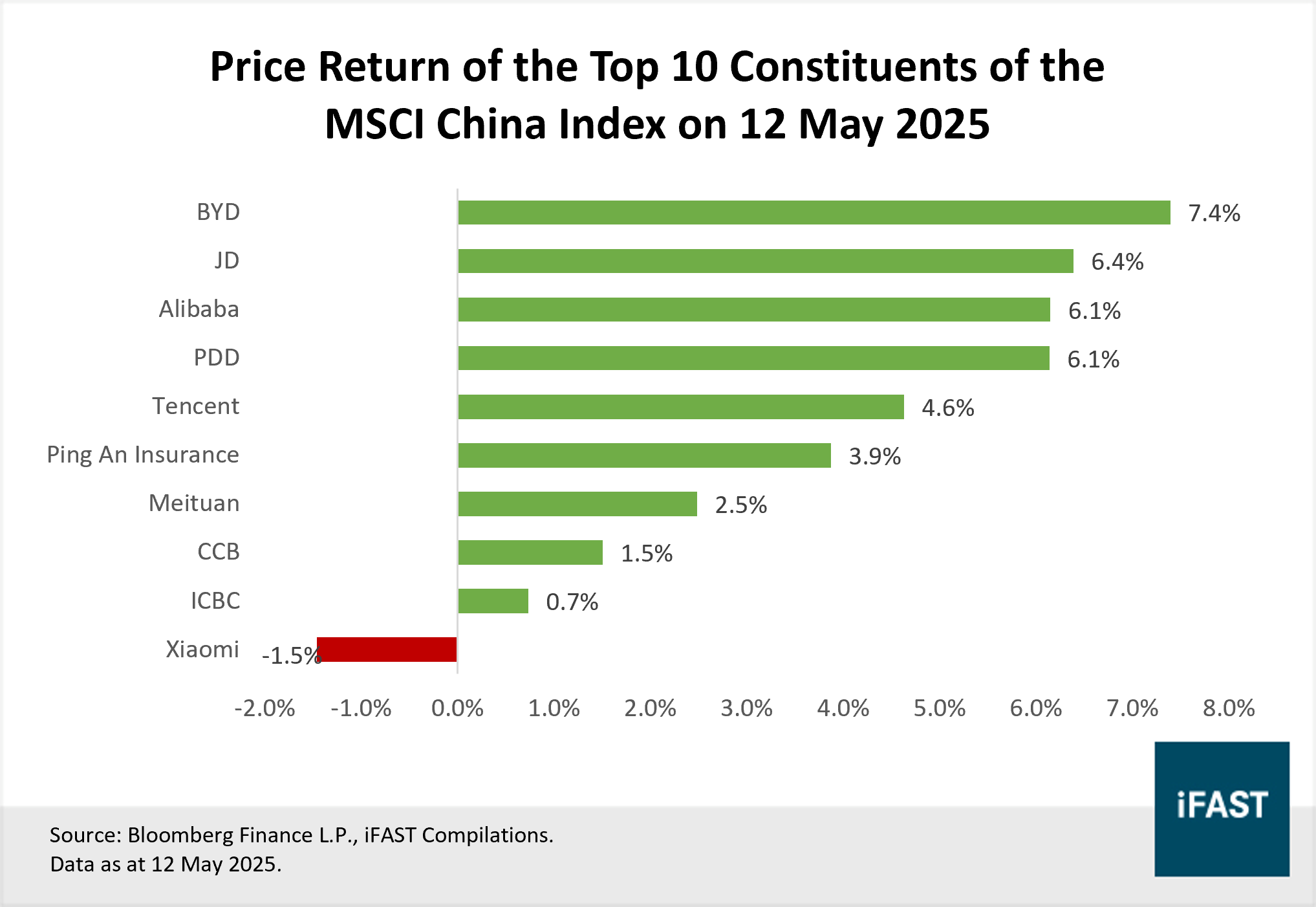

The MSCI China Index surged 3.4% at the close on 12 May, staging a rally despite the tariff breakthrough only hitting headlines around 3 p.m. — leaving barely an hour for the market to digest and react. The late-session surge was enough to erase much of April’s losses, which had been driven by escalating trade war concerns.

The rebound was broad-based, with nine of the index’s top 10 constituents ending the day in the green. Gains were led by big moves in the technology and consumer discretionary sectors (Figure 1).

Figure 1: China’s equity market staged a broad recovery on 12 May

China’s Tough Stance Yielded Positive Negotiation Outcome

The scale and speed of the tariff reductions took markets by surprise — but they reflect a growing consensus on both sides that elevated duties have become mutually damaging. The triple-digit tariffs imposed earlier signalled a complete trade decoupling, a scenario that neither US nor China ultimately wants to see. This shared recognition helped accelerate negotiations toward a rare moment of alignment.

As highlighted in our earlier coverage on China, Beijing had maintained a defiant posture against US tariff pressure, vowing to “fight to the end.” That rhetoric was not empty posturing — it was backed by concrete preparations. China had been actively diversifying trade ties, deepening economic collaborations with ASEAN countries and deploying monetary easing to buffer domestic demand.

At the same time, Beijing was amassing a toolkit of non-tariff countermeasures to sharpen its bargaining position. These included export restrictions on rare earth elements — critical to industries ranging from electric vehicles to aerospace and defence — as well as suspensions of soybean import licences, a move designed to exert pressure on US agriculture.

Related article: China Can Better Withstand the Impact of Tariffs This Time

With these strategic levers in hand, Beijing entered the talks from a position of strength. The resulting agreement — which significantly rolls back tariffs without requiring China to commit to expanded purchases of US goods or investment — can be seen as a diplomatic win for China, enabling it to preserve its hardline stance while securing favourable terms.

Tariff De-risking May Be Short-Lived

In the near term, further tariff reductions appear unlikely. The “reciprocal” tariff has already been brought down to 10% — a level that Trump had accepted in past negotiations with allies such as the UK, and one that now seems to serve as a de facto floor.

China, meanwhile, remains firm in its position on fentanyl. Beijing has pushed back strongly against Washington’s framing of the issue, asserting that fentanyl is a domestic problem for the US, not a bilateral matter. The 20% tariff component linked to fentanyl has been described by Chinese officials as “disrespectful” and a move that could erode trust and impede future dialogue. With Beijing unwilling to soften its stance on fentanyl-related claims, the current combined tariff rate of 30% could prove sticky — at least in the absence of a broader diplomatic breakthrough.

Despite the current thaw, the risk of a renewed tariff escalation remains on the table — especially given Trump’s unpredictable track record on trade policy. History offers a cautionary tale: in 2018, both sides similarly agreed to pause hostilities after initial negotiations, only for the US to abruptly walk away, triggering over 18 months of tariff escalations and strained diplomacy before reaching the "Phase One" trade deal in January 2020.

Progress in future talks is likely to be slower and more complex. As seen in US trade negotiations with other countries, progress has been slow and limited over the past 30 days. Similarly, the next phase of US-China talks — expected to occur during this suspension period — will be even tougher than the one just concluded.

Beijing is pushing for a full rollback of US tariffs. Supported by its perceived success in the current round of negotiations, China appears more convinced than ever that maintaining a tough stance is the most effective approach when dealing with the US. Meanwhile, the US has yet to achieve one of its goals of reducing the trade deficit. With fears of full trade decoupling now receding, the US may pivot to pressuring China to increase imports of US goods.

Given this dynamic, we see a high likelihood that tariffs will remain around the 30% level or potentially edge higher. The current tariff level avoids full-scale decoupling while giving US some space to narrow the trade gap. Future tariffs, we expect, will likely become more targeted — focusing on strategic sectors such as aluminium rather than broad-based hikes.

US companies are likely to rush to get orders from China within the current 90-day window of relative tariff stability. While the 30% rate is lower than previous peaks, it remains elevated enough to pressure margins — particularly for small and mid-sized businesses with limited pricing power or supply chain flexibility. This potential wave of frontloading could temporarily inflate trade volumes in the coming months, but it also underscores how far both sides remain from reaching a durable, comprehensive trade framework.

Tariffs Weigh on Growth, but Risks Are Contained

China’s economy has already felt the sting of triple-digit US tariffs. The official NBS Manufacturing PMI slipped to 49.0 in April — the fastest contraction in 16 months — as sentiment deteriorated across both domestic and external-facing industries.

In a bid to safeguard economic stability amid renewed trade tensions, Beijing has turned to its macroeconomic playbook. Ahead of the tariff talks, the People’s Bank of China cut the required reserve ratio by 50 basis points and trimmed the seven-day reverse repo rate by 10 basis points to 1.4%, injecting fresh liquidity into the financial system. The easing cycle continued on 20 May, with the central bank lowering both the one-year and five-year Loan Prime Rates by 10 basis points to stimulate consumer and corporate borrowing. The consecutive policy moves underscore Beijing’s intent to reinforce domestic growth as external pressures mount.

Meanwhile, evidence of China’s efforts to re-route trade flows is starting to show. April’s trade data revealed a robust 8.1% year-on-year increase in exports, well above the market consensus of 1.9%. While shipments to the US plunged by 21.0%, that shortfall was offset by strong gains in exports to ASEAN (+20.8%), Taiwan (+15.5%), and Japan (+7.8%).

Tariffs will remain a structural headwind, but China appears increasingly well-positioned to buffer the impact. With tariffs now dialled back to 30%, the estimated drag on GDP for 2025 is expected to narrow to just 0.3 percentage points — a decent improvement from the projected 1 percentage point hit under the prior 145% rate. The current burden appears far more manageable, better positioning China to meet its “around 5%” GDP growth target for the year.

Strong Fundamentals In China’s Tech Sector Provide A Buffer Against Tariff Headwinds

In a macro environment where tariffs remain elevated at 30% or potentially rise further, Chinese companies with a domestic focus appear well-positioned to weather trade-related disruptions. On average, constituents of the MSCI China Index derive just 15% of their revenue from international markets — significantly lower than their counterparts in MSCI Emerging Markets ex-China (29%) and MSCI Japan (47%).

Among the top ten holdings in the MSCI China Index, PDD is likely to be the most affected due to its US focused e-commerce platform, Temu, which accounted for roughly 45% of its revenue in 2024 (Table 1). Temu’s business model—relying on price arbitrage and service fees—is highly vulnerable to the tariff hike and the removal of the de minimis rule.

Table 1: PDD faces the greatest tariff exposure among major index constituents in the MSCI China Index

|

Top 10 Securities of the MSCI China Index |

Sector |

International Revenue Exposure in 2024 |

|

PDD Holdings Inc - Depositary Receipt |

Consumer Discretionary |

Temu contributed ~45% |

|

Xiaomi Corp Class B |

InfoTech |

41.9% |

|

BYD Co Ltd H Share |

Consumer Discretionary |

28.6% |

|

Alibaba Group Holding Ltd |

Consumer Discretionary |

10.9% |

|

Tencent Holdings Ltd |

Communication Services |

9.8% |

|

Industrial & Commercial Bank of China Ltd H Share |

Financials |

9.6% |

|

Bank of China H |

Financials |

4.7% |

|

China Construction Bank Corp H SHARE |

Financials |

2.8% |

|

JD.com Inc Class A |

Consumer Discretionary |

NA |

|

Meituan Class B |

Consumer Discretionary |

NA, but core business centred around China domestic delivery |

|

Source: Bloomberg

Finance L.P., Internet sources, company financial reports, iFAST

Compilations. |

||

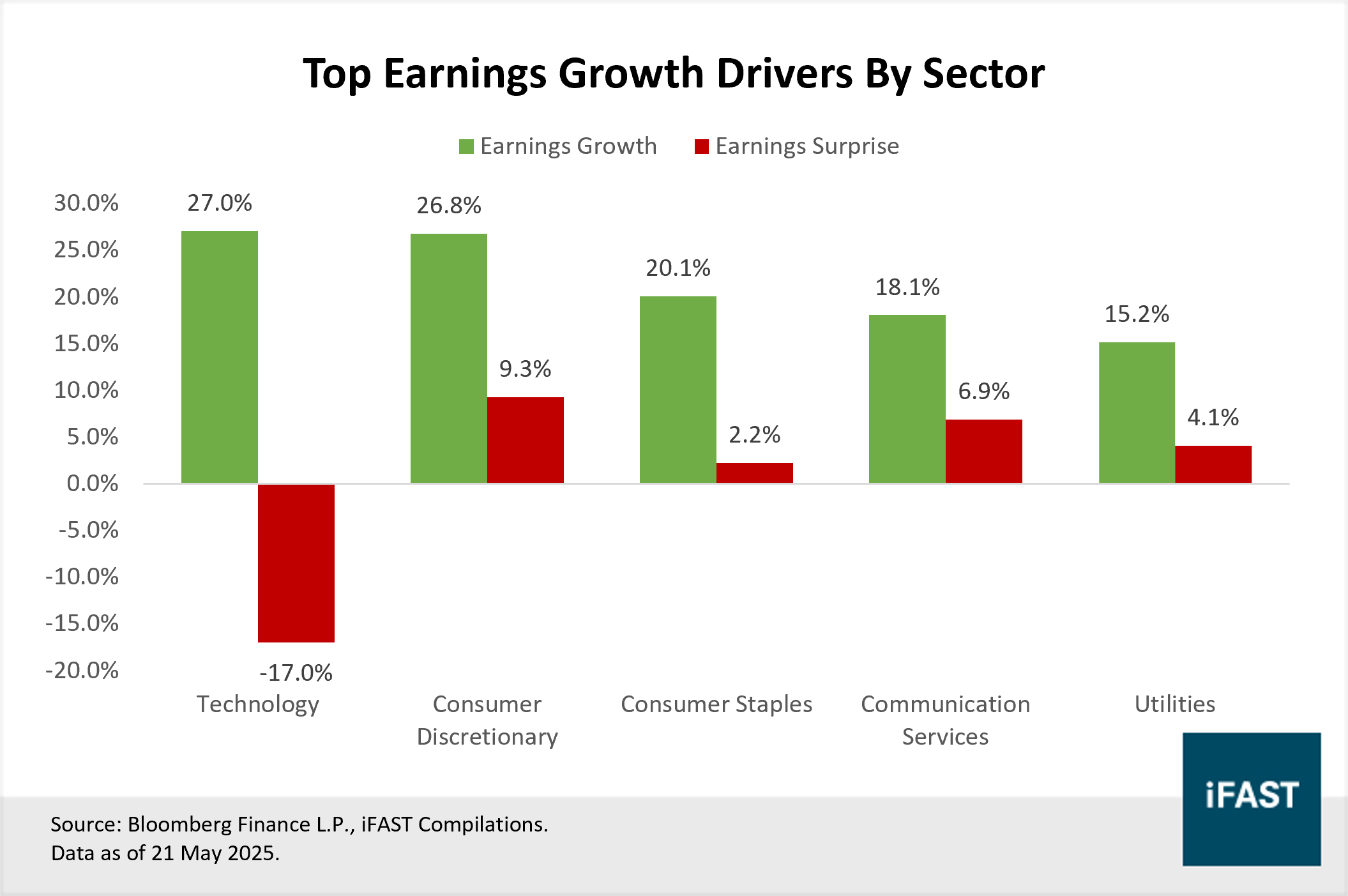

In contrast, domestically focused players such as Alibaba, JD.com, and Tencent generate 10% or less of their revenue from overseas markets, offering a natural hedge against external shocks. These companies have also delivered stronger-than-expected earnings for the quarter ended 31 March 2025, with the consumer discretionary and communication services sectors posting positive earnings surprises of 9.3% and 6.9%, respectively (Figure 2).

Figure 2: Consumer discretionary and communication services led with strong earnings and the biggest upside surprises

Operational momentum among China’s technology heavyweights has remained strong. Tencent reported a 14% year-on-year increase in net profit, underpinned by solid performance in its core online gaming segment and growing contributions from AI-powered advertising. Meanwhile, e-commerce leaders JD.com and Alibaba posted standout earnings results, with net profit surging 53% and a staggering 1,203% respectively. Even after stripping out gains from equity investments, Alibaba’s operating income still jumped 93% — a testament to recovering consumer demand and robust growth in AI-linked product revenue.

The strong earnings come as Beijing intensifies its efforts to steer the economy toward a consumption-led growth model. A raft of stimulus measures, coupled with a revival in consumer and business confidence, is laying the groundwork for a sustained recovery. At the same time, China’s strategic focus on artificial intelligence is providing new momentum for tech leaders. Against this backdrop, the country’s leading technology and consumer-facing firms are emerging as key beneficiaries — well-positioned to deliver steady growth even as global trade uncertainties linger.

Chinese Equities Hold Investment Appeal Amid Trade Tensions

China’s economy appears prepared to withstand future trade tensions. Beyond the resilience of its technology sector, the broader economy continues to benefit from diversified trade flows and proactive policy stimulus aimed at stabilising growth. Against this backdrop, we maintain our view that China remains a strong contender to surprise on the upside — a potential dark horse in global markets for 2025.

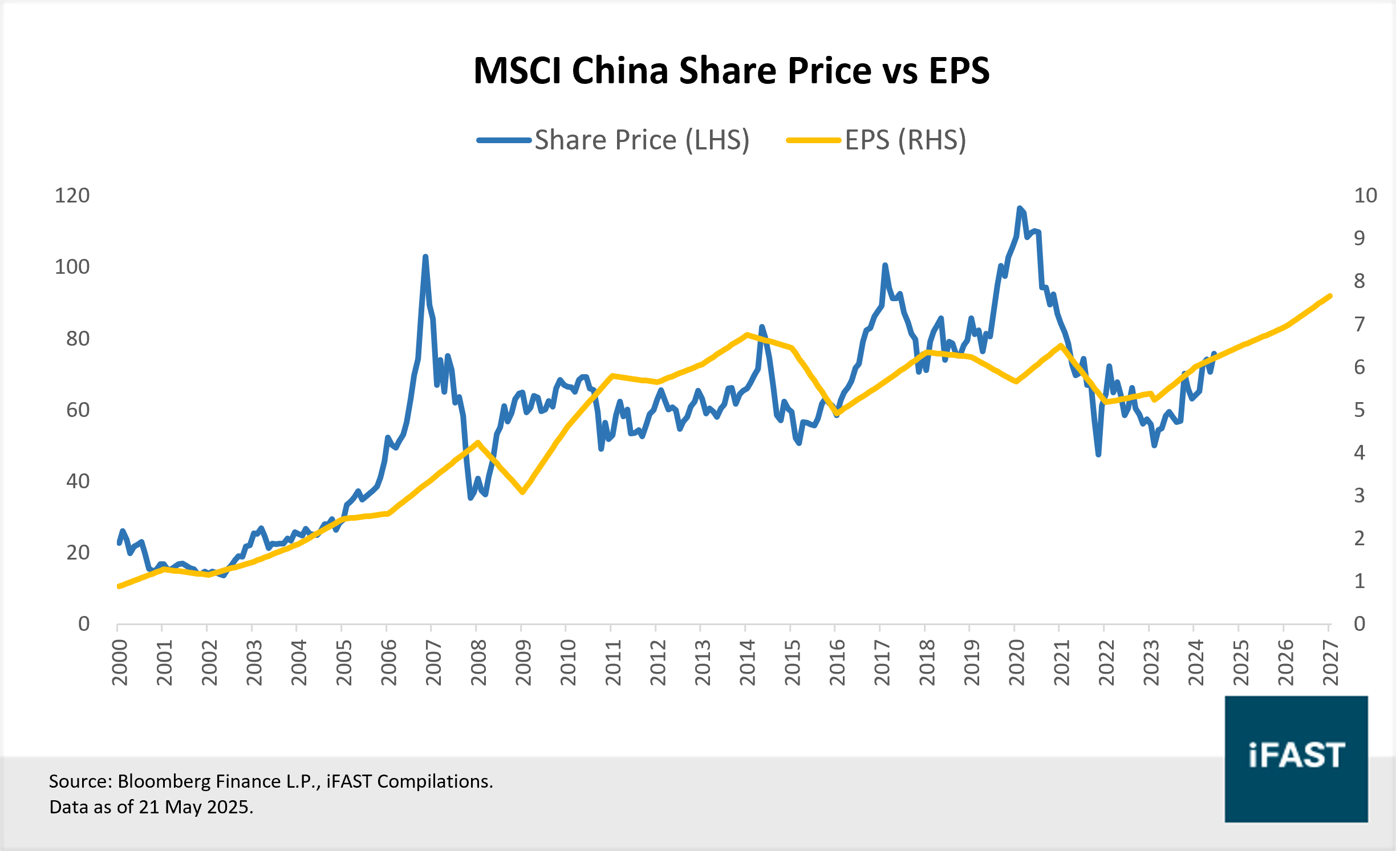

Looking ahead, we forecast a target price of HKD 85.8 for the MSCI China Index by FY2027, based on a fair valuation of 10X PE. This reflects a 13.2% upside from current levels. We have revised up our earnings forecast from the previous update, reflecting two key developments: a significantly reduced risk of full trade decoupling, and strong first-quarter results from leading consumer companies — signalling improving sentiment and a rebound in domestic consumption.

Within equities, technology shares that align with domestic consumption trends are particularly well-positioned to deliver steady growth. To tap into this opportunity, we recommend investors consider the iShares Hang Seng Tech ETF (HKEX: 3067 / 9067). The ETF’s top holdings — including Xiaomi, Alibaba, and SMIC — are relatively insulated from US tariffs, while it excludes US-listed firms such as PDD, mitigating geopolitical risk exposure.

Investors seeking broader market exposure may consider the iShares Core MSCI China ETF (HKEX: 2801), the iShares MSCI China ETF (NASDAQ: MCHI), or the Fidelity China Focus A-SGD which has demonstrated resilience during past economic downturns.

Table 2: MSCI China’s earnings projections till FY2027

| MSCI China Index | 2024 | 2025E | 2026E | 2027E |

| PE Ratio | 12.6 | 11.0 | 9.8 | 8.8 |

| Earnings Growth | 24.2% | 14.3% | 13.0% | 10.5% |

| EPS | 6.01 | 6.87 | 7.76 | 8.58 |

| Projected Fair Price (Based on fair PE ratio of 10X) | 85.8 | |||

| Upside | 13.2% | |||

| Source:

Bloomberg Finance L.P., iFAST Compilations. Data as of 21 May 2025. |

||||

Figure 3: MSCI China Index vs. EPS

Declaration:

For specific disclosure, at the time of publication of this report, the analyst who produced this report holds positions in iShares Core MSCI China ETF (HKEX: 2801).

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.