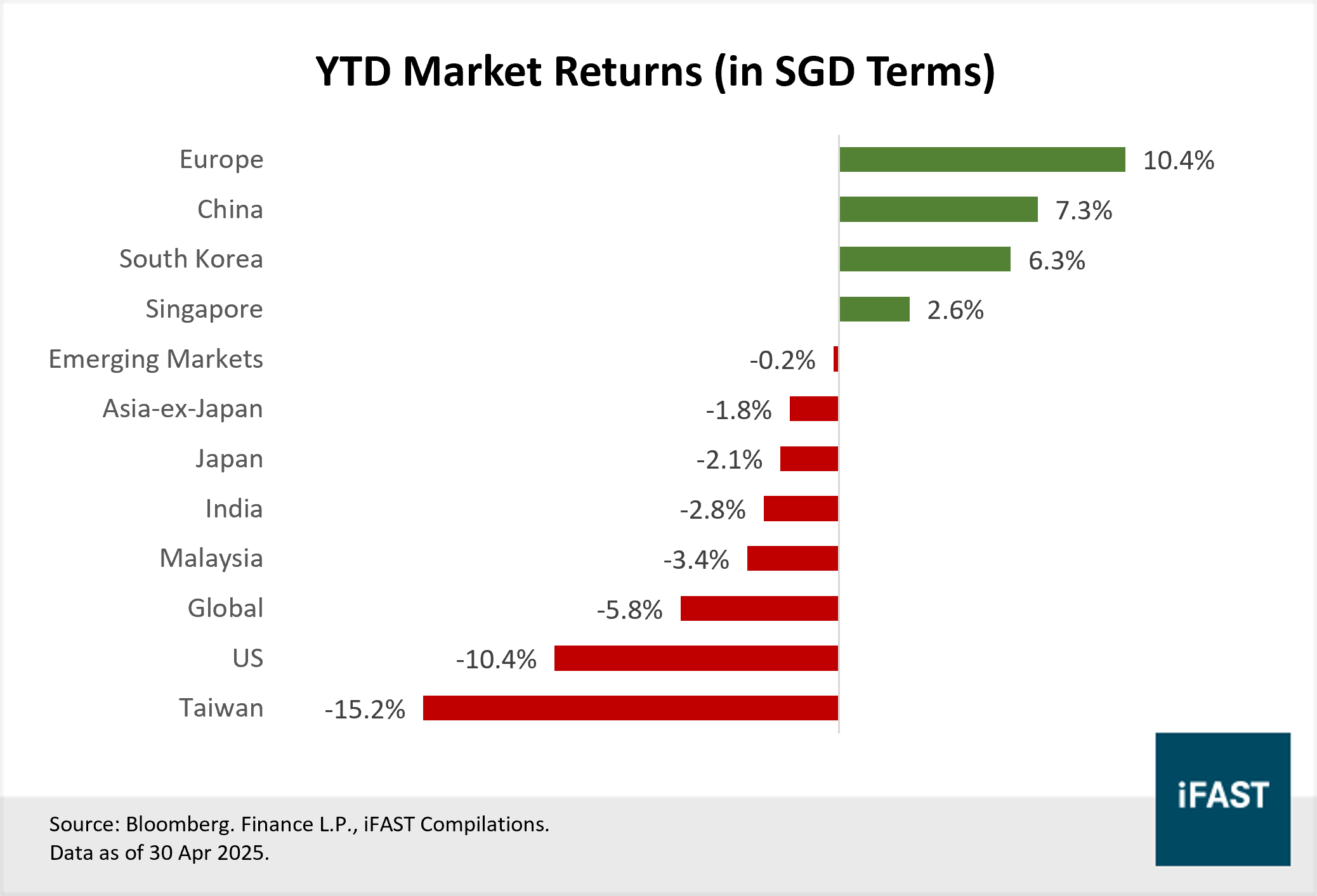

- Global markets experienced a sharp sell-off following Trump’s announcement of reciprocal tariffs. Among the markets that we cover, Chinese equities proved more resilient, posting a YTD return of 7.3%.

- China’s “fight to the end” stance has strongly resonated with the public. Rising patriotic sentiment has boosted consumption and supported market performance.

- The 145% tariff is expected to trim one percentage point off China’s GDP growth in 2025. However, Trump’s hardline approach may open the door to new trade alliances for China.

- Chinese companies remain domestically focused, with relatively low international revenue exposure. PDD is likely the most vulnerable due to Temu’s heavy reliance on US sales.

- We continue to see China as a potential dark horse market. The MSCI China Index offers a 10.2% upside by FY2027, even after accounting for tariff risks.

The global market has seen a sharp downturn following the US’s implementation of reciprocal tariffs. Among the few countries that responded with retaliatory tariffs against the US, China has been hit the hardest, facing a blanket tariff rate of 145% with rates soaring to 245% on goods such as electric vehicles and syringes.

The MSCI China Index has since given up roughly three-quarters of its earlier gains, which were fuelled by investor enthusiasm around AI developments and renewed domestic stimulus measures. As of 30 April 2025, the index still recorded a decent year-to-date return of 7.3%. Compared to the broader global market, Chinese equities appear to be showing greater resilience during this downturn (Figure 1).

Figure 1: Chinese stocks have shown greater resilience compared to many other markets

Patriotic sentiment drives support for China’s economy and markets

China’s “fight to the end” stance, with its retaliatory tariffs against the US, has resonated widely among its public. The extraordinarily high tariffs imposed on Chinese goods have unexpectedly helped accelerate the recovery of investor and consumer confidence, both of which had been heavily damaged in recent years by political uncertainty and a sluggish economic outlook.

Expressions of anti-US sentiment have emerged across Chinese society, with calls to boycott American products and impose higher prices on US consumers in China. At the same time, a surge in patriotism has encouraged many citizens to support the domestic equity market and increase consumption as a form of national solidarity, viewing the trade dispute not just as an economic challenge but as a shared national mission.

In parallel, China’s state-backed funds have injected billions into state-owned enterprises, technology firms, and ETFs to stabilise the equity market. Although state-driven capital injections have historically provided only short-term market support, they remain a crucial psychological boost. The message is clear: China is mobilising its resources and public resolve to confront and cushion the impact of trade pressures.

Tariffs will pose a drag, but also create opportunities for China’s economy

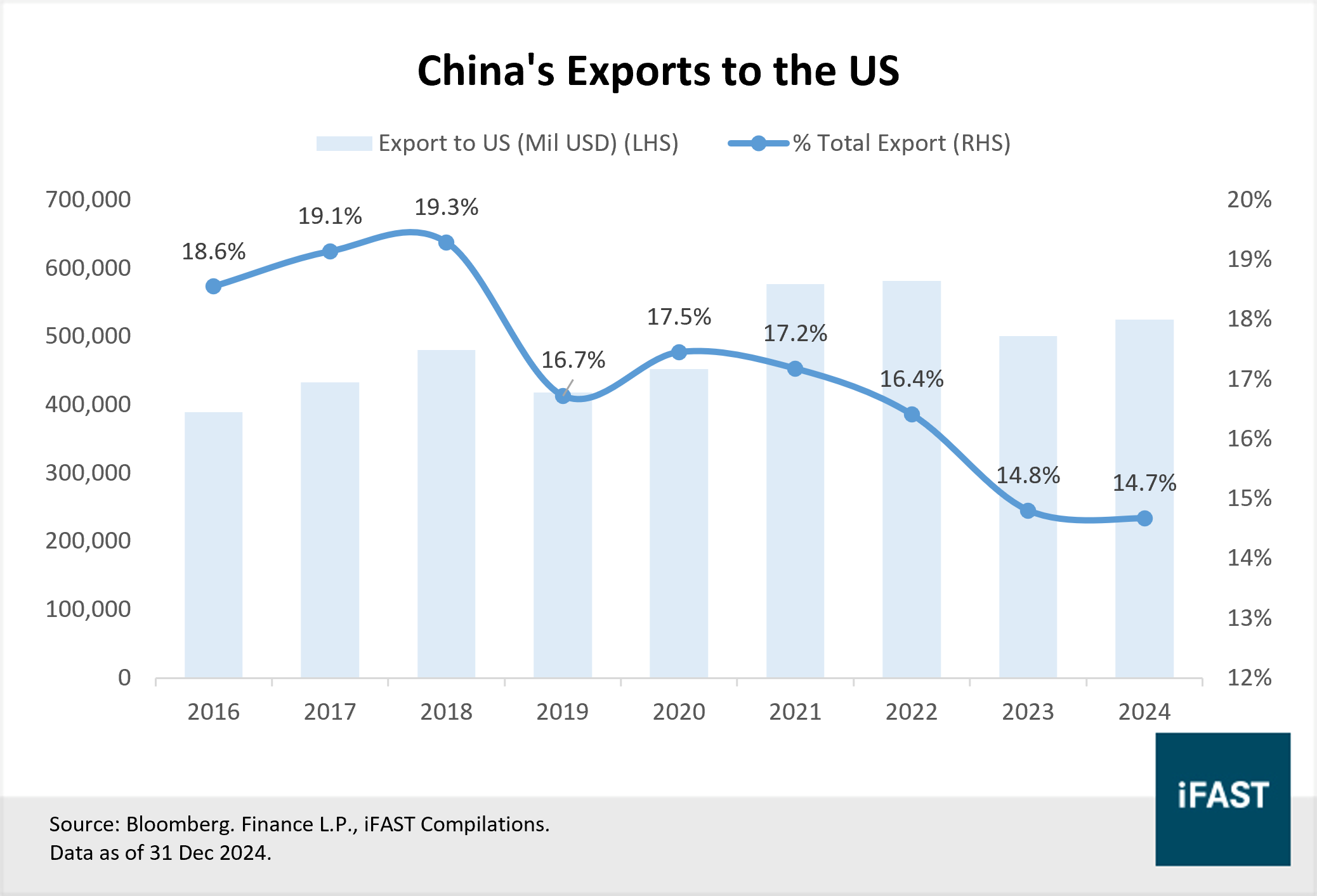

While public sentiment has been in China’s favour during this round of tensions, the economic cost of the trade conflict remains significant. Despite China's ongoing efforts to reduce its reliance on the US - a strategic shift initiated during the first term of President Trump in 2018 - the US continues to be China’s largest single-country export destination. Nevertheless, progress has been made: the share of Chinese exports destined for the US has declined from 19.3% in 2018 to 14.7% as of 2024 (Figure 2).

Figure 2: China’s exports to the US have steadily declined since 2018

Based on our estimates, China’s exports to the US could drop to zero under the current tariff regime, effectively signalling a trade decoupling. If this level of tariffs persists, it could shave one percentage point off China’s GDP growth this year, posing a challenge to the government’s “around 5%” growth target for 2025.

To counter this, Chinese policymakers are actively deploying a range of strategies to fill the void left by the loss of US market access. One key approach is the acceleration of trade diversification efforts. China is expanding its network of trading partners and establishing new free trade zones. In the week of 14 April 2025, President Xi embarked on diplomatic visits to three ASEAN countries—Vietnam, Malaysia, and Cambodia—all of which have also faced high double-digit reciprocal tariffs from the US. During his stop in Vietnam, 45 cooperation agreements were signed.

As trade tensions with the US escalate, we anticipate an increase in regional trade collaboration, especially given Trump’s continued hardline stance. US negotiations with Vietnam and Europe have so far failed to generate significant progress, with mutual tariff removal seen as falling short of his “phenomenal” deal standard. Should these talks fail after the 90-day suspension period, many countries will turn to alternative trade alliances, offering China a strategic opportunity to position itself as a more reliable partner and build new economic coalitions.

China has launched several retaliatory measures as bargaining chips, including tariffs on US agricultural goods and the suspension of soybean import licenses. Given that China accounted for roughly half of US soybean exports in 2024, this move is likely to inflict significant pressure on American farmers. To mitigate the shortfall, China has shifted its sourcing to Brazil. In addition, China restricted the export of rare earth elements, putting pressure on critical industries such as automotive, aerospace, and defence in the US.

In the meantime, we believe the key to sustaining economic stability lies in China’s ability to pivot toward a more consumption-driven growth model. With inflation at -0.1% YoY as of March 2025, real borrowing costs remain elevated at 3.2%, leaving ample room for monetary easing. Both the reserve requirement ratio and the loan prime rate offer flexibility for further cuts. In addition, expanded issuance of consumption vouchers and ongoing initiatives like consumer goods trade-in programs are expected to support domestic demand.

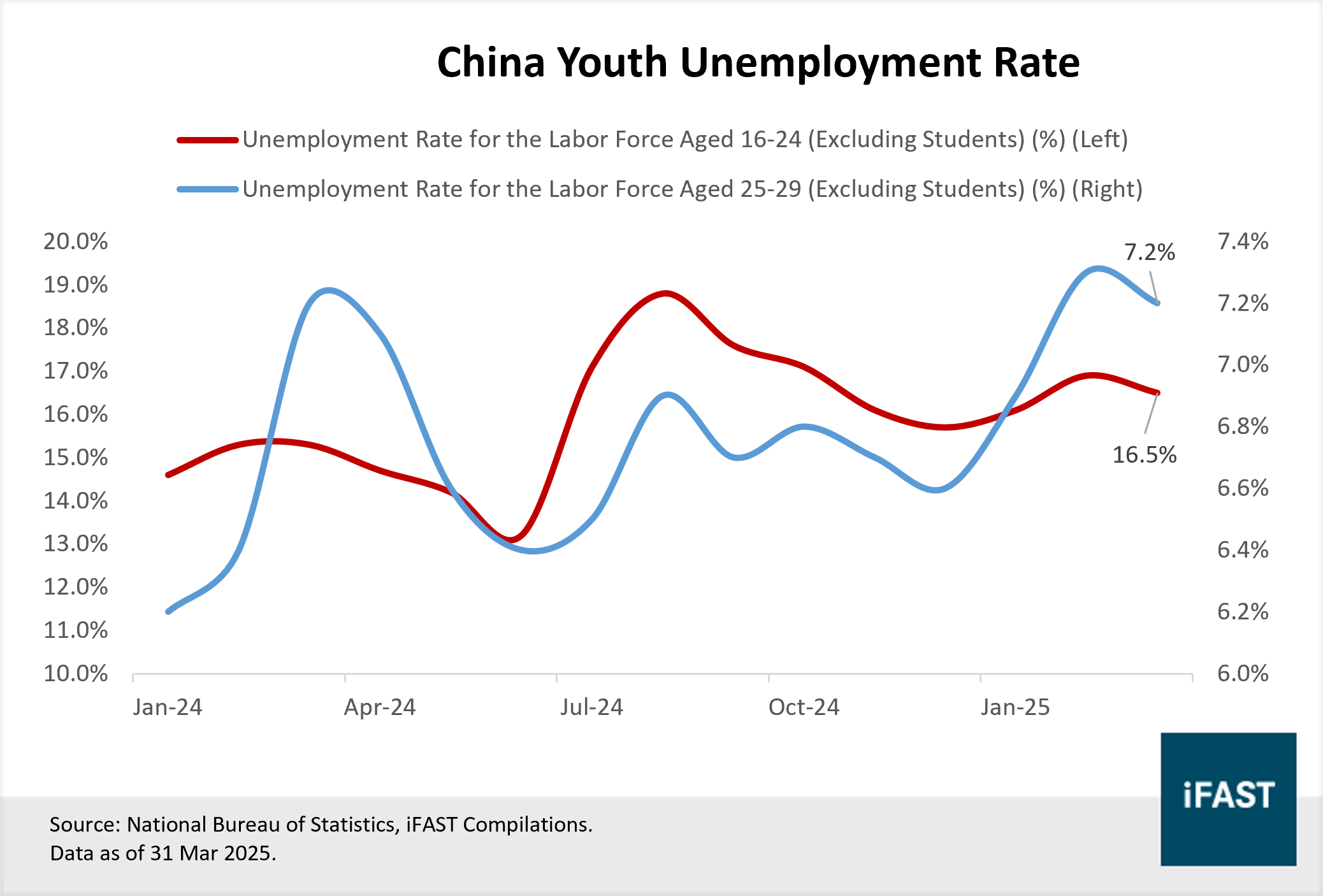

Nonetheless, China faces persistent challenges in the labour market. The youth unemployment rate remained at high levels (Figure 3), reflecting underlying weaknesses in job creation. In our view, restoring labour market confidence and improving household income will be essential to unlocking more sustainable, broad-based consumption growth.

Figure 3: Youth unemployment ticked up in February 2025

Chinese companies rely less significantly on international revenue

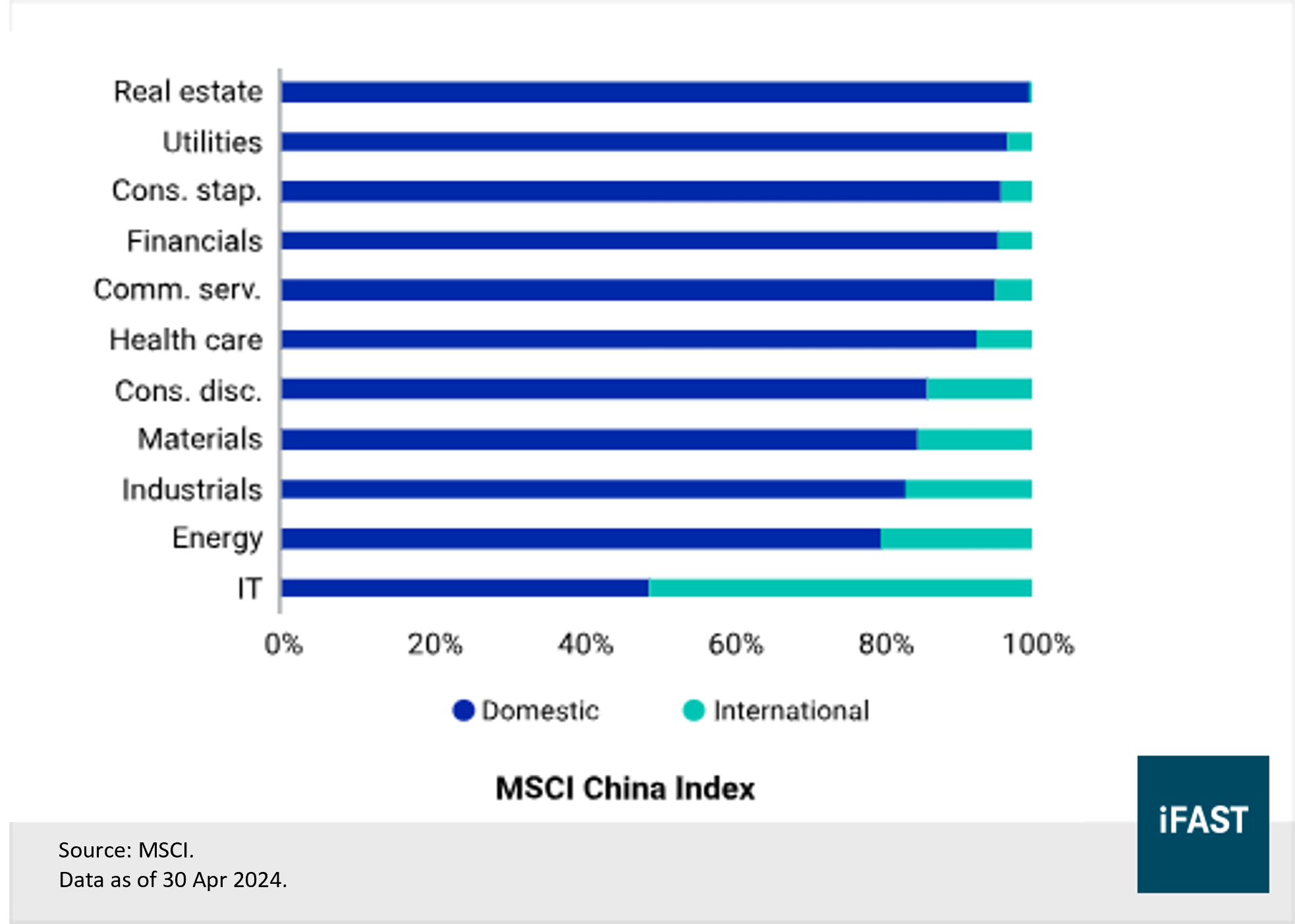

According to MSCI, companies in the MSCI China Index generate only around 15% of their revenue from international markets, significantly lower than MSCI Emerging Markets ex-China (29%) and MSCI Japan (47%). This domestic focus offers Chinese companies greater insulation from trade disruptions.

Within the MSCI China Index, IT has the highest international revenue exposure, followed by energy and industrials. In contrast, communication services and consumer discretionary - two sectors we believe will benefit from both AI advancements and a shift toward consumption-driven growth - have lower international exposure, at under 10% and 20% respectively (Figure 4).

Figure 4: The IT sector had the highest revenue exposure to the international market

Among the top ten holdings in the MSCI China Index, PDD is likely to be the most affected due to its North America-focused e-commerce platform, Temu, which accounted for roughly 45% of its revenue in 2024 (Table 1). Temu’s business model—relying on price arbitrage and service fees—is highly vulnerable to the 145% tariff hike and the removal of the de minimis rule.

Xiaomi ranks second in the table, with 41.9% of its revenue generated from international markets. Despite its global presence, the company’s focus on emerging markets limits its exposure to the US. Its affordable smartphone models have gained strong traction in regions such as India and the Middle East, mitigating the impact of tariffs.

Move down the table, domestically focused firms like Alibaba and Tencent are also less exposed to tariff risks. Given this, we believe the recent broad-based equity sell-off may offer selective buying opportunities, particularly among leading technology names with stronger domestic fundamentals.

Table 1: PDD faces the greatest tariff exposure among major index constituents in the MSCI China Index

|

Top 10 Securities |

Sector |

International Revenue Exposure in 2024 |

|

PDD Holdings Inc |

Consumer Discretionary |

Temu contributed ~45% |

|

Xiaomi Corp Class B |

Information Technology |

41.9% |

|

BYD Co Ltd H Share |

Consumer Discretionary |

28.6% |

|

Alibaba Group Holding Ltd |

Consumer Discretionary |

10.9% |

|

Tencent Holdings Ltd |

Communication Services |

9.8% |

|

Industrial & Commercial Bank of China Ltd H Share |

Financials |

9.6% |

|

Bank of China H |

Financials |

4.7% |

|

China Construction Bank Corp H Share |

Financials |

2.8% |

|

JD.com Inc Class A |

Consumer Discretionary |

NA |

|

Meituan Class B |

Consumer Discretionary |

NA, but the core business is still domestic delivery in China |

|

Source: Bloomberg Finance L.P., Internet sources, company financial reports, iFAST Compilations. Data as of 31 Mar 2025. |

||

Chinese equities are still worth investing in

Tariffs will inevitably weigh on China’s economy, but under the current circumstances, the US is unlikely to escape unscathed either. Given the high degree of uncertainty surrounding the trajectory of tariff policies in the coming months, panic selling of Chinese equities may not be the wisest course of action.

China still holds several strategic cards in this standoff and is actively deploying a multi-pronged approach to cushion the potential impact of trade losses. These measures include rerouting trade flows, imposing controls on strategic materials, implementing targeted stimulus, and tapping into a wave of national pride to bolster domestic demand and market sentiment. Furthermore, China is also exploring the possibility of trade talks with the US, paving the way for a potential de-escalation of trade tensions. We maintain our view that China could be this year’s dark horse market.

Since the sharp sell-off in Chinese equities on 7 April 2025, signs of a rebound have already begun to emerge. Defensive, dividend-paying stocks, domestically focused businesses, and consumer discretionary names aligned with a consumption-driven economy are all well-placed to capture upside opportunities as sentiment stabilises.

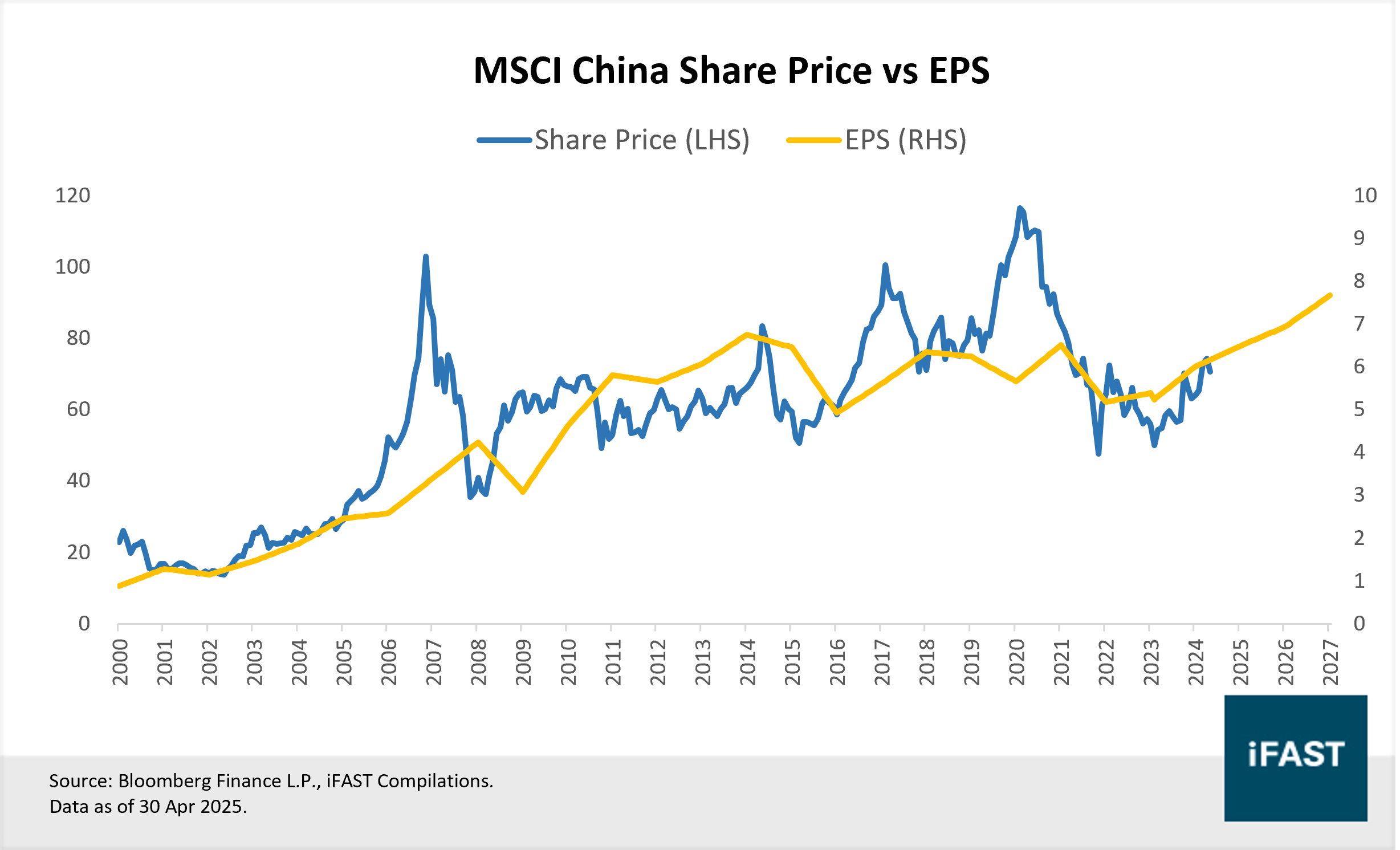

Based on a fair P/E ratio of 10x, we estimate a target price of HKD77.9 for the MSCI China Index by FY2027, reflecting a 10.2% upside after factoring in tariff impacts.

For investors looking to increase their exposure to China, the current market sell-off presents an attractive entry point. To capture the potential rebound, we recommend the iShares Hang Seng Tech ETF (HKEX: 3067 / 9067), which is well-positioned to benefit from the growth of Chinese technology stocks. Its top holdings include Xiaomi, Alibaba, and SMIC—companies that are relatively insulated from US tariffs—while notably excluding US-listed firms such as PDD.

Alternatively, investors seeking broader market exposure may consider the iShares Core MSCI China ETF (HKEX: 2801), the iShares MSCI China ETF (NASDAQ: MCHI), or the Fidelity China Focus A-SGD, which has demonstrated resilience during past economic downturns.

Table 2: MSCI China’s earnings projections till FY2027

|

2024 |

2025E |

2026E |

2027E |

|

|

PE Ratio |

11.2 |

10.4 |

9.6 |

8.65 |

|

Earnings Growth |

24.2% |

8.0% |

8.6% |

10.5% |

|

EPS |

6.01 |

6.49 |

7.05 |

7.79 |

|

Projected Fair Price (Based on fair PE ratio of 10X) |

77.9 |

|||

|

Upside |

10.2% |

|||

|

Source: Bloomberg Finance L.P., iFAST

Compilations. |

||||

Figure 5: MSCI China Index vs. EPS

Declaration:

For specific disclosure, at the time of publication of this report, the analyst who produced this report holds positions in iShares Core MSCI China ETF (HKEX: 2801).

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.