• The Fed has cut rates by 50bps in September. Even so, we expect interest rates to stay higher for longer. The US economy remains robust and multiple upside risks to inflation still exists.

• GDP rose 3% in 2Q24 powered by an acceleration in consumer spending as well as private inventory investment. Both the labour market and consumer balance sheets remain in good health.

• We reiterate our stance that US equities are one of the most desirable to own because of their wide competitive moats, strong balance sheets, diversified revenue streams and a favourable business environment.

• We expect multiple expansion and positive earnings revisions to support future share price appreciation. Our target price for the S&P 500 Index is 6,818, which translates to an upside potential of close to 20% (as of 3 Oct 2024).

Key takeaways from September’s Fed meeting

Back in September, the US Federal Reserve concluded its sixth meeting of the year. In a highly anticipated move the FOMC delivered its first interest rate cut since the early days of the pandemic, lowering the Fed Funds Rate by 50 basis points to a range of 4.75% to 5.00%. In a post meeting statement, Fed Chair Jerome Powell said that the decision to lower rates reflects the committee’s commitment to maintain a low unemployment rate now that inflation is moving sustainably towards their 2% target.

The Fed also updated its summary of economic projections, estimating that rates could fall as low as 3.4% by the end of next year, and the neutral long-term interest rate at 2.9%. Meanwhile, markets are way more aggressive as always, pricing in as many as eight cuts by the end of 2025 (equivalent to a Fed Funds Rate of 2.75% to 3.00%). Powell also reiterated that interest-rate policy is not on a preset path, and there is no hurry to cut rates.

Related Article: The Fed has cut rates by 50bps – what should you do?

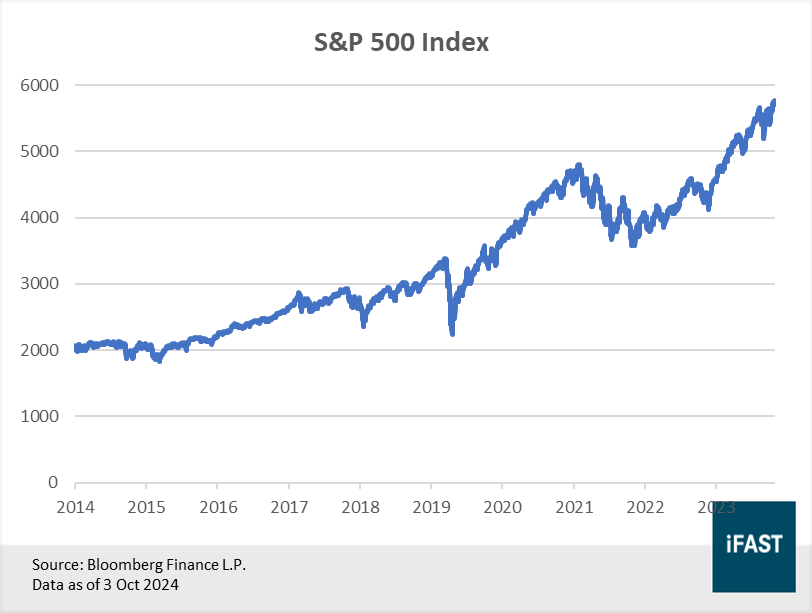

Markets cheered the move, sending the S&P 500 index to a record high of 5,767 points (Figure 1). Digital economy stocks were among the biggest winners of the recent rally, as Invesco Nasdaq Internet ETF and the Vaneck Semiconductor ETF are up by 44.7% and 22.1% year-to-date respectively.

Figure 1: The S&P 500 Index has reached a new record high post rate cuts

Our thoughts on the latest Fed move and the state of the US economy

Even though slashing policy rates by 50 basis points may seem like an overly aggressive move, we believe that it was made out of prudence rather than an expectation of a weak US economic outlook. The US economy has proven to be remarkably resilient despite the fact that interest rates have been held at their highest level since the beginning of the global financial crisis for more than a year.

According to the third and final estimate by the Bureau of Economic Analysis (BEA), the US economy expanded 3.0% in the second quarter of 2024, up from 2.8% in the preliminary estimate and 1.6% in the first quarter (Figure 2). The increase in GDP figures was predominantly driven by an acceleration in consumer spending as well as private inventory investment. Despite some moderation, consumption remains a bright spot for the US economy. Retail sales rose 2.1% year-on-year in August, while personal consumption expenditures rose 2.5% in the second quarter.

Figure 2: The US economy expanded 3.0% in 2Q24, revised up from the initial estimate of 2.8%

With regards to the labour market, while we note that certain indicators such as the unemployment rate has deteriorated, other measures (e.g. initial jobless claims) have fallen to its lowest level since June. According to data published by the Bureau of Labour Statistics, the number of job openings still exceeds the number of jobseekers, suggesting that the labour market is becoming more balanced after a period of intense demand for workers during the early post pandemic days.

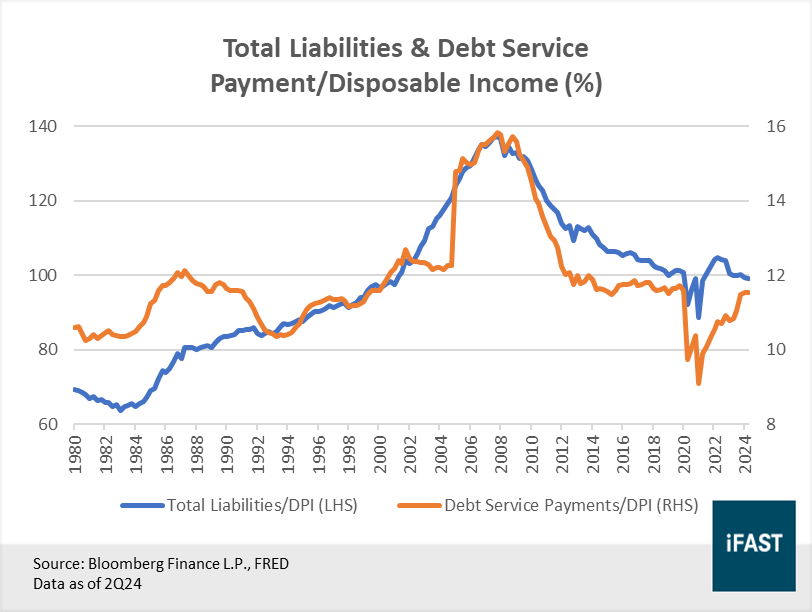

Consumer balance sheets remain in good health, backed by robust wage growth and the extensive use of fixed rate mortgages (which are unaffected by changes in interest rates). And with rates expected to go down even further, consumption should remain relatively strong, and that should help to sustain the economy going forward.

Figure 3: Despite a sharp rise in interest rates, consumer balance sheets remain in good health

Likewise, rate cuts should also have a positive impact on the corporate sector, as firms have more room to raise debt and pursue capex plans going forward. Federal spending programs such as the Inflation Reduction Act (IRA) and the CHIPS and Science Act will spark a new wave of investment within the US. Aside from the direct impact, greater business investment also supports the economy through other channels such as job creation, which should in turn have a positive effect on consumption.

By most accounts the US economy remains sound, hence we do not consider the latest rate cut as a move back to near-zero interest rates, a notion that Jerome Powell himself has explicitly countered. In other words, the higher for longer interest rate environment is here to stay.

While the Fed has pencilled in a couple more rate cuts this year, there is no guarantee that they will materialise as the committee said that they would continue to adopt a data-dependent approach. Even though inflation has cooled, there are still plenty of upside risks such as rising tensions in the Middle East (especially between Israel and Lebanon), port strikes in the US and deglobalisation, which may complicate things further.

US equities are still one of the most desirable to own

Although US equities have had a strong run in the recent weeks and are currently trading close to their record high, there are still compelling reasons for investors to maintain exposure to this market. First and foremost is the fact that most of the industry leaders that we see today are US firms.

A striking example would be how the Magnificent Seven companies dominate the tech sector, across multiple segments ranging from cloud computing, digital advertising and even the development and commercialisation of AI technology.

But it does not end there.

The dominance of US companies often extends beyond the realm of tech, to other sectors such as healthcare and financial services. Many of these companies also operate on a global scale, holding leading positions not only in the US but also in various international markets. They often possess strong competitive advantages (e.g. network effects) which allows them to stay ahead of the competition.

The country’s rich culture of innovation and well-developed capital markets also helps to ensure that the next tech success story is likely to come from the US, rather than anywhere else. This stands in stark contrast to China, where years of government intervention & regulatory crackdowns have stifled innovation and driven many venture capital investors away.

By investing in US equities, investors are essentially investing in some of the most innovative and highest quality companies that exists today. Additionally, investors also receive the benefit of global diversification, as US companies often provide indirect exposure to international markets given that many of them generate a significant part of their revenue abroad. This helps to mitigate the impact of a downturn in one market by balancing it with stronger performance in others.

Related Article: Why the US equity market deserves to be trading at a higher earnings multiple

Expect better long-term performance driven by earnings growth and multiple expansion

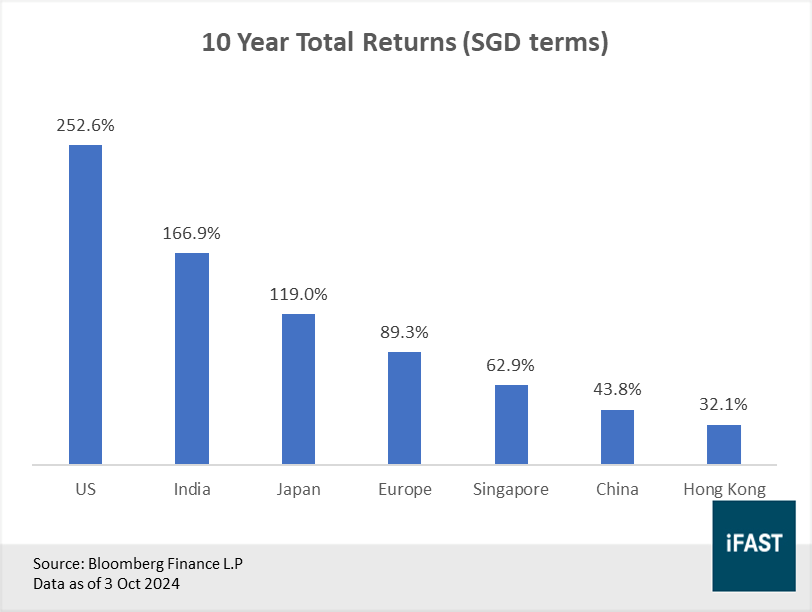

Over the past 10 years, US equities (gauged by the S&P 500 index) has delivered total returns of 252%, far outpacing the returns of other major markets such as China, Japan and Europe (Figure 4). Looking ahead, we believe that US equities still have substantial potential to continue delivering superior long-term share price performance.

Figure 4: The US has done exceptionally well among major equity markets

Over the years, the average PE ratio of the S&P 500 Index across various five-year periods has increased, from roughly 13X back in 2009-2014 to nearly 21X today. With a large proportion of the index made up of tech/tech-adjacent stocks (which often trade at higher multiples), multiple expansion is likely to be one of the key sources of returns as these companies continue to evolve.

Besides that, the ability of tech companies to consistently generate strong earnings growth (often in the double digits) is another key factor that contributes to their long-term appeal and supports future share price appreciation. Going forward, as more technology megatrends take hold, US tech companies are likely to experience positive earnings revisions, which should bolster the overall earnings outlook for the market.

Although some investors may be put off by the idea of investing in a market while it is trading close to its all-time high, it's important to look ahead and focus on the long-term potential. By doing so, we can see that valuations for the S&P 500 Index look way more appealing, trading at just 17.6X of 2026 estimated earnings. If more positive revisions occur, valuations are likely to be even more attractive. Using our fair PE multiple of 22X, this translates to an upside potential of close to 20% and a target price of 6,818 (as of 3 Oct 24).

Table 1: US equities have strong earnings growth potential, courtesy of the higher weighting of tech stocks

|

S&P 500 Index |

2023 |

2024E |

2025E |

2026E |

|

Earnings Per Share (EPS) |

221.10 |

250.00 |

277.00 |

310.00 |

|

Earnings Growth YoY |

-1.24% |

13.07% |

10.80% |

11.91% |

|

PE Ratio (X) |

21.57 |

22.80 |

20.58 |

18.39 |

|

Upside Potential (based on a fair PE Ratio of 22X) |

- |

- |

- |

19.65% |

|

Source: Bloomberg Finance L.P., iFAST Compilations. Data as of 3 Oct 2024 |

||||

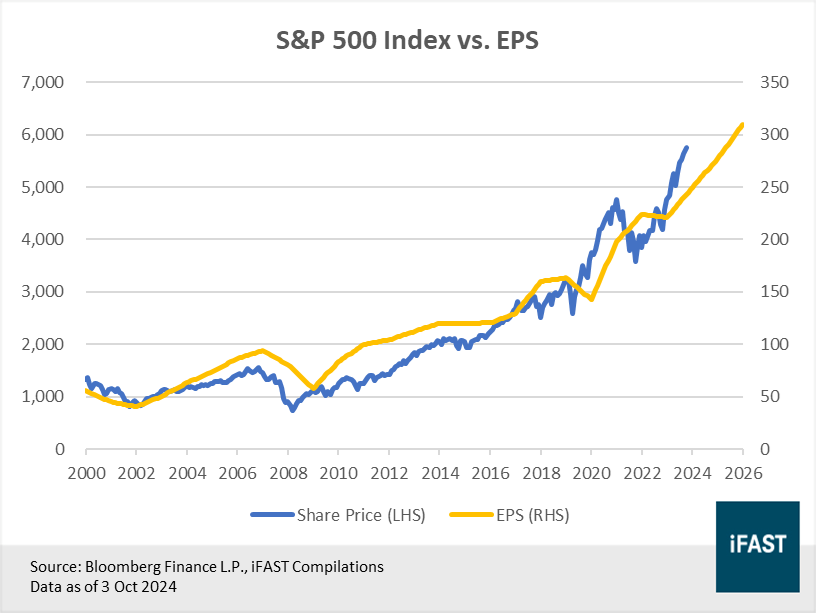

Figure 5: Share prices are predominantly driven by earnings in the long term

In summary, we continue to hold a positive view on US equities and firmly believe that US market will be one of the top performing markets in the coming years. We see multiple expansion and earnings growth to be a key contributors of future share price returns. And with interest rates likely to stay higher for longer, this environment is also favourable to US companies, many of which have rock solid balance sheets and sustainable earnings.

For exposure to the US, investors may consider the following products.

Table 2: Recommended products

|

Recommended Products |

|

|

ETF |

Vanguard S&P 500 ETF (NYSE:VOO) |

|

JPMorgan U.S. Quality Factor ETF (NYSE:JQUA) |

|

|

Unit Trust |

|

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.