- We think the recent rate cut was made out of prudence rather than because of an expectation of a weak US economic outlook.

- Data dependence continues to be key for the Fed. We do not expect this cut to be the start of a typical easing cycle but will monitor incoming data over the next few months.

- We expect interest rates to remain elevated over the longer term.

- Overall, we continue to prefer shorter-duration over longer-duration bonds despite the rate cut.

A recap of what happened

The Fed recently cut rates by 50bps in its September meeting in line with market expectations. This was a near-unanimous decision (11 to 1) with Fed Governor Bowman voting for a 25bps cut instead. Bowman was seen as a more hawkish voice within the Fed committee, stating as recently as May and June that she was open to further rate hikes if necessary (based on the incoming data).

Related article: Incoming Fed rate cut? Here is how to position for it.

Looking at the latest Summary of Economic Projections by the Fed (Table 1), the Fed now expects end-2024 inflation to come in lower than previously expected, and end-2024 unemployment to come in higher than previously expected. They have also shifted their end-2024 and end-2025 policy rate expectations down and are now expecting about 3 more cuts than before.

We think the cooling US labour market and the decline in inflation emboldened policymakers’ decision to cut rates, with risks now more balanced between employment and inflation as seen from the meeting minutes (Table 2). However, we highlight that (i) inflation expectations remain above the 2% target; and (ii) more importantly, the Fed continues to reiterate its data-dependent approach: any further moves (including cuts) will clearly depend on whether economic data continues its current trend or otherwise.

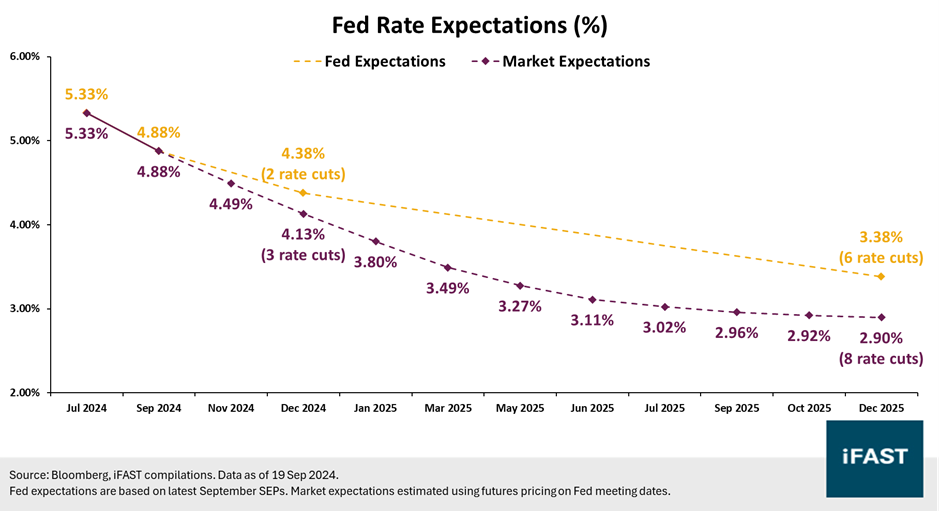

Meanwhile, markets are now pricing in even more aggressive rate cuts compared with the Fed: they expect 3 more rate cuts by end-2024 and 8 more rate cuts by end-2025 (Chart 1). In addition, compared with the close on 17 Sep, we also saw a slight steepening of the UST yield curve: short-end yields saw a sizeable decline of over 10bps, while longer-end yields increased by about 5bps (Chart 2).

Table 1: Fed’s Summary of Economic Projections

| Median

Expectations (End-2024) |

June Summary | September Summary | Change |

| Real GDP Growth | 2.1% | 2.0% | -0.1% |

| Unemployment | 4.0% | 4.4% | 0.4% |

| PCE Inflation | 2.6% | 2.3% | -0.3% |

| Core PCE Inflation | 2.8% | 2.6% | -0.2% |

| Fed Funds Rate Expectations (end-2024) | 5.1% | 4.4% | -0.7% |

| Fed Funds Rate Expectations (end-2025) | 4.1% | 3.4% | -0.7% |

| Source:

Federal Reserve, iFAST compilations. Data as of 19 Sep 2024. Data is taken from Fed official policy statement and press conference transcript. Key points and differences are bolded/underlined by us. |

|||

Table 2: Summary of Fed meeting

| Source | July | September | Our thoughts |

| Policy Statement (Labour Market) | Job gains have moderated, and the unemployment rate has moved up but remains low. |

Job gains have slowed, and the unemployment rate has moved up but remains low. | The Fed's decision was likely driven by the cooling of labour market conditions. |

| Press Conference (Labour Market) | In the labor market, supply and demand conditions have come into better balance ... Overall, a broad set of indicators suggests that conditions in the labor market have returned to about where they stood on the eve of the pandemic—strong, but not overheated. | In the labor market, conditions have continued to cool ... Overall, a broad set of indicators suggests that conditions in the labor market are now less tight than just before the pandemic in 2019. | |

| Policy Statement (Inflation) | The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance. | The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance. | While the Fed has judged inflation to be moving closer to its 2% target, they have retained their observation that inflation remains above 2%. |

| Press Conference (Inflation) | Inflation has eased notably over the past two years but remains somewhat above our longer-run goal of 2 percent. | Inflation has eased notably over the past two years but remains above our longer-run goal of 2 percent. | |

| How the Fed will act ahead | In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. | We are not on any preset course. We will continue to make our decisions meeting by meeting. | The Fed continues to emphasise its data-dependent approach, so any further moves (including cuts) will depend on whether inflation continues to decline and/or the labour market continues to weaken. |

| Source:

Federal Reserve, iFAST compilations. Data as of 19 Sep 2024. Data is taken from Fed official policy statement and press conference transcript. Key points and differences are bolded/underlined by us. |

|||

Chart 1: Fed Funds Rate expectations – Market vs the Fed

Chart 2: UST yield curve steepened following Fed decision

Our thoughts, and what you should expect

1. We think this was a ‘risk-management’ 50bps cut that was made out of prudence rather than a result of an expectation of a weak US economic outlook. This is clear from the Summary of Economic Projections and the comments from Fed officials, including Chairman Powell. Looking at economic data, we also find that key US macro indicators remain resilient for now.

- For instance, US GDP continued to grow at a solid rate of 3.0% (QoQ, annualised) in 2Q24, marking the 10th consecutive quarter of positive growth since 2Q22. We also observe that the US consumer remains resilient based on the relatively steady growth in retail sales (Chart 3), while the services sector also continues to be a bright spark for the US economy.

- While US unemployment has ticked up (most recently to 4.2%) and Fed expectations (4.4%) indicate it could continue going up, we highlight that these figures are coming off a record low (3.4% in Jan 2023). The Fed itself has described the labour market back then as ‘extremely tight’ and ‘overheated’. Based on several indicators, the labour market appears to be stabilising from post-COVID lows rather than entering a drastic downturn (Chart 4).

2. We think the key takeaway from Powell was that of data dependence, and that this cut is unlikely the start of a typical rate cut cycle. Specifically, Powell emphasised they were not committing to any rate cuts down the line (in November or December).

Investors should not assume the descent of inflation will be smooth sailing: as we explained previously, multiple upside risks to inflation continue to linger in the backdrop including (i) a rebound in shelter inflation; and (ii) longer-term factors arising from geopolitical tensions and deglobalisation.

Consequently, our views on rates will depend on incoming data, particularly on inflation and the labour market. If economic data continues to weaken, we see the possibility of further rate cuts down the line.

3. Interest rates are likely to remain elevated over the longer term, as we have highlighted throughout the year. Powell himself explicitly pushed back against the thought of a return to the zero interest rates (or even negative rates) environment seen just a few years ago. Furthermore, the Summary of Economic Projections also showed neutral (long-run) rates expectations at 2.9%, markedly higher than what was expected before rate hikes in 2022 (2.4%).

Chart 3: Retail sales continued to expand in August 2024

Chart 4: Labour market appears to be stabilising rather than deteriorating significantly

Recommendation – Short Duration

We continue to prefer shorter-duration over longer-duration bonds.

First, yields for shorter-dated bonds generally remain elevated helped by the inverted yield curve, and can provide a comparable level of income to longer-dated bonds. In other words, we think investors are not getting compensated sufficiently for taking on additional maturity and duration risks (in the case of a yield curve inversion, the nominal yields are lesser for greater maturity and duration risks).

Second, we reiterate that longer-end yields have more limited room to fall even if Fed rate cuts materialise. As stated previously, long-end yields like the 10y UST have already dropped drastically in anticipation of the rate cuts (e.g. 4.7% in late April to about 3.7% today), and we think that further declines in longer-end yields might require the pricing in even more rate cuts in 2024 and 2025. In fact, the recent rate cut has validated this thesis for now, with medium to long-end UST yields (2y and above) increasing following the rate cut.

Third, given the aggressiveness of rate cut expectations, we think there is a larger scope for things to go wrong in the coming months, including surprises to incoming inflation or labour market data, changes in the Fed’s tone, as well as upcoming election risks (e.g. any post-election fiscal stimulus). These could result in markets re-pricing expectations for Fed cuts as well as long-term yields, which in turn could lead to larger mark-to-market losses. We experienced such re-pricings earlier in 2Q24 when markets started to push back on their expectations of Fed cuts.

Our shorter-duration product recommendations include the Nikko AM Shenton Short Term Bond Fund and the United SGD Fund within our Singapore-Centric category. Investors looking for an even shorter duration exposure while remaining high in quality can consider our Money Market recommendations – Fullerton SGD Cash Fund and Amundi Funds Cash USD. For a slightly longer duration alternative, investors can consider our recommended Allianz Global Opportunistic Bond Fund, which is our top pick for Global Bond funds (duration: 4.29y).

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.