- Among the new additions to our Recommended Funds List this year is the Janus Henderson Horizon Japanese Smaller Companies A2 USD.

- The abundance of mispriced opportunities, excess balance sheet capital, and the potential benefits of a stronger yen are key reasons why investors might consider adding Japanese small caps to their portfolios.

- The fund capitalises inefficiencies in the under-researched Japanese small-cap space by leveraging on a strategy that is anchored in rigorous stock analysis, a deep understanding of company management, and disciplined management of a high-conviction portfolio.

- The fund has shown consistent strength over the past five calendar years, outperforming its benchmark, the Russell/Nomura Small Cap Index.

In August, we unveiled the 2024/25 edition of our Recommended Funds List, spotlighting funds that have delivered strong and consistent risk-adjusted returns relative to their peers.

Among the new additions to the list is the Janus Henderson Horizon Japanese Smaller Companies A2 USD. This fund dives deep into the under-researched Japanese small-cap market to uncover hidden gems, aiming to deliver long-term outperformance.

(Related article: Recommended Funds List 2024/25: Discover The Best-In-Class Equity Funds Here)

Why Japan small caps?

There are a few reasons why investors might want to consider adding Japanese small caps into their portfolios through an active fund.

Abundance of mispriced opportunities: Unlike large-caps, Japanese small-caps receive significantly less sell-side coverage. According to findings from Janus Henderson Investors as of 31 December 2023, on average, only 0.9 sell-side analysts cover mid to small-caps with market capitalisations between JPY 10 and 200 billion. These companies often provide limited investor relations (IR) disclosure, with information not always available in English. This creates opportunities for active managers who possess Japanese language skills and have the resources to conduct in-depth research to uncover mispriced opportunities in this under-researched segment of the market.

Excess balance sheet capital: Japanese companies have historically retained a significant portion of their earnings as cash, leading to strong balance sheets. Nearly 60% of companies within the Russell/Nomura Small Cap Index, a proxy for small-cap companies listed on the Tokyo Stock Exchange (TSE), are in net cash positions. With Japan's ongoing corporate governance reforms, these cash-rich small caps are well-positioned to thrive. Their excess capital could lead to higher capital expenditures, increased dividends and share buybacks, creating favourable conditions for growth and shareholder returns.

Potential beneficiaries of a stronger yen: Small-caps are domestically oriented; their revenues are generated primarily within Japan. The appreciation of the Japanese yen would lead to a reduction of import costs for such companies, which should generally have a positive impact on earnings.

Janus Henderson Horizon Japanese Smaller Companies

The Janus Henderson Horizon Japanese Smaller Companies A2 USD aims to exploit inefficiencies in the Japanese small-cap market to deliver long-term outperformance. The strategy invests at least two-thirds of total assets in smaller Japanese companies, which are usually companies falling within the bottom 25% of their relevant market by way of market capitalisation or those with a market cap of JPY 10 to 200 billion.

Its representative benchmark is the Russell/Nomura Small Cap Index which contains the bottom 15% of the Russell/Nomura Total Market Index in terms of adjusted market cap.

The fund is driven by thorough stock analysis, deep understanding of company management, and the careful monitoring of a concentrated, high-conviction portfolio.

The portfolio manager believes that it is important to have open and regular meetings with senior management of smaller companies, as there is a direct link between the actions of key stakeholders and a company’s performance. To ensure alignment, the investment team holds regular meetings with senior management, meeting multiple times before taking a position and conducting quarterly follow-ups to validate the investment thesis and adjust position sizes.

The fund typically holds between 40 - 70 stocks. As of 31 July 2024, there are a total of 53 holdings with a weighted-average market cap of JPY 150.66 billion. The top 10 holdings make up about 37% of the portfolio (Table 1).

Table 1: Top 10 holdings

|

Name |

Sector |

Description |

Weight |

|

JINS |

Consumer Discretionary |

Eyewear |

4.64% |

|

Taiyo Yuden |

Information Technology |

Development and manufacturing of electronic components such as inductors |

4.37% |

|

Aiful |

Financials |

Consumer finance |

4.02% |

|

Harmonic Drive Systems |

Industrials |

Design and manufacturing of precision motion control equipment |

3.94% |

|

Park24 |

Industrials |

Parking operator |

3.83% |

|

Septeni |

Communication Services |

Digital advertising |

3.39% |

|

CyberAgent |

Communication Services |

Digital advertising |

3.27% |

|

dip |

Industrials |

Online recruitment and job search services |

3.19% |

|

Fujitsu General |

Consumer Discretionary |

Air conditioners |

3.18% |

|

Daio Paper |

Materials |

Paper manufacturer |

3.12% |

|

Total |

- |

36.95% |

|

|

Source: Janus Henderson Investors, iFAST Compilations Data as of 31 July 2024 |

|||

Long-term outperformance against peers

We compared the fund’s performance against the rest of the Japan small cap funds available on our platform, including the PineBridge Japan Small Cap Equity Fund, the United Japan Small And Mid Cap Fund, and the BNP Paribas Funds Japan Small Cap Fund. It is worth highlighting that these peers typically invest in companies of slightly higher market capitalisation, though they are still considered as small and mid-caps.

For instance, the PineBridge Japan Small Cap Equity Fund invests at least 50% of its assets in companies whose market cap at the time of acquisition is less than JPY 400 billion. The BNP Paribas Funds Japan Small Cap Fund, it aims to hold at least 75% of its assets in companies with a market cap below JPY 500 billion. In contrast, our recommended Janus Henderson Horizon Japanese Smaller Companies Fund targets at least two-thirds of assets in companies with a market cap of not more than JPY 200 billion.

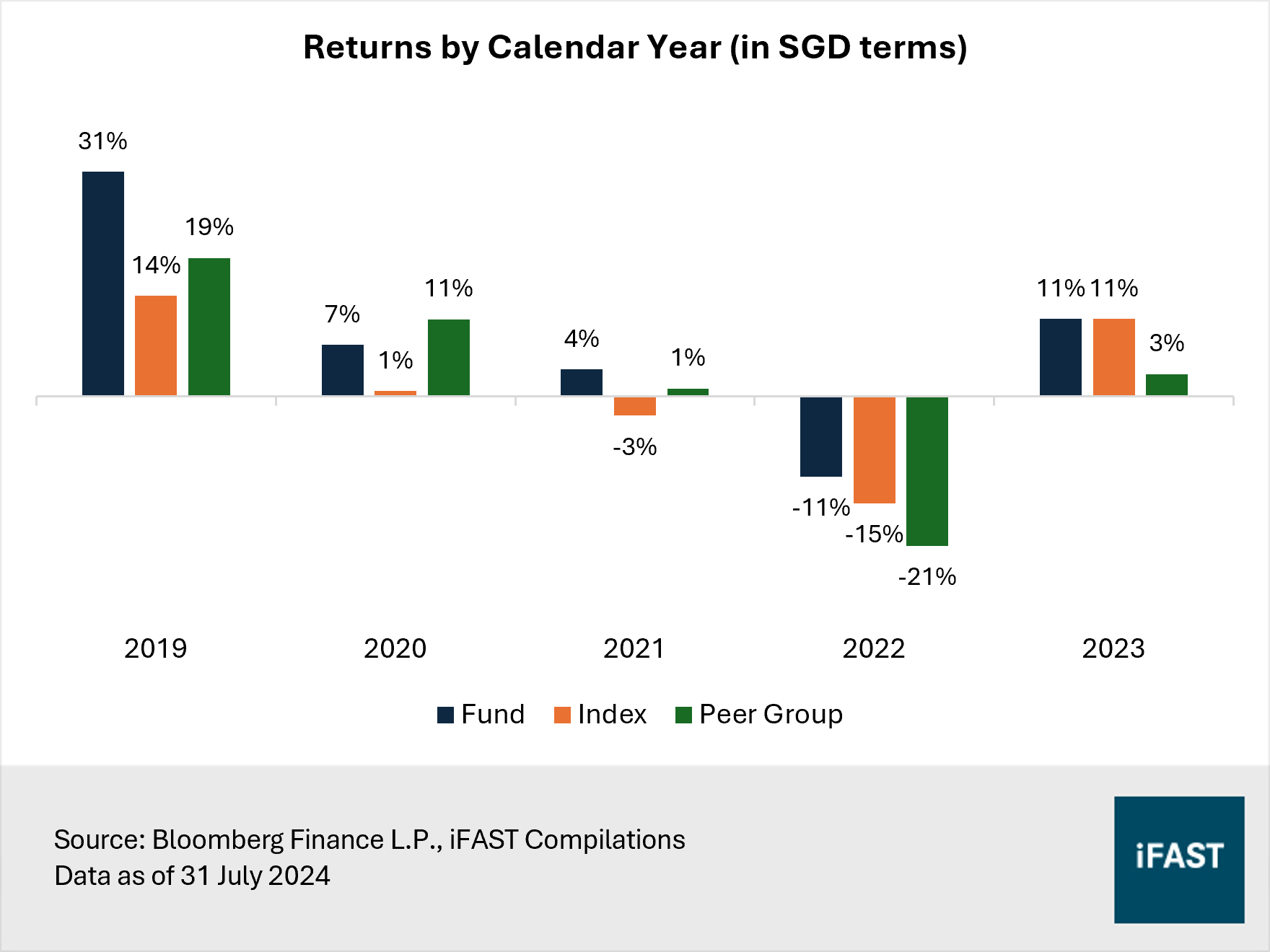

On a calendar year basis, the fund demonstrates impressive consistency in the strength of its returns. Over the last five calendar years (2019-2023), the fund has consistently delivered excess returns against its benchmark, the Russell/Nomura Small Cap Index (Figure 1). The fund has also outperformed its peer group in four out of those five calendar years.

In calendar year 2023, the fund recorded returns of 11% (in SGD terms), in line with the benchmark while substantially surpassing its peers. The key contributors to the fund’s performance in 2023 were its positions in Nitto Boseki and Ibiden.

Nitto Boseki produces advanced glass materials designed to meet the specific needs of applications related to artificial intelligence (AI). Meanwhile, NVIDIA is a client of Ibiden – whose high-density PCBs (printed circuit boards) and semiconductor packaging substrates are key components in the manufacturing of AI chips and electronic devices.

The portfolio manager has since closed positions of Nitto Boseki and Ibiden as he believes the risk-adjusted returns are not attractive anymore after the surge in share prices. In 2023, Nitto Boseki and Ibiden delivered returns of over 140% and 60% respectively in local currency terms. This decision aligns with the portfolio manager’s pragmatic approach, which emphasises valuations as a critical factor in investment decisions.

Figure 1: Strong and consistent returns

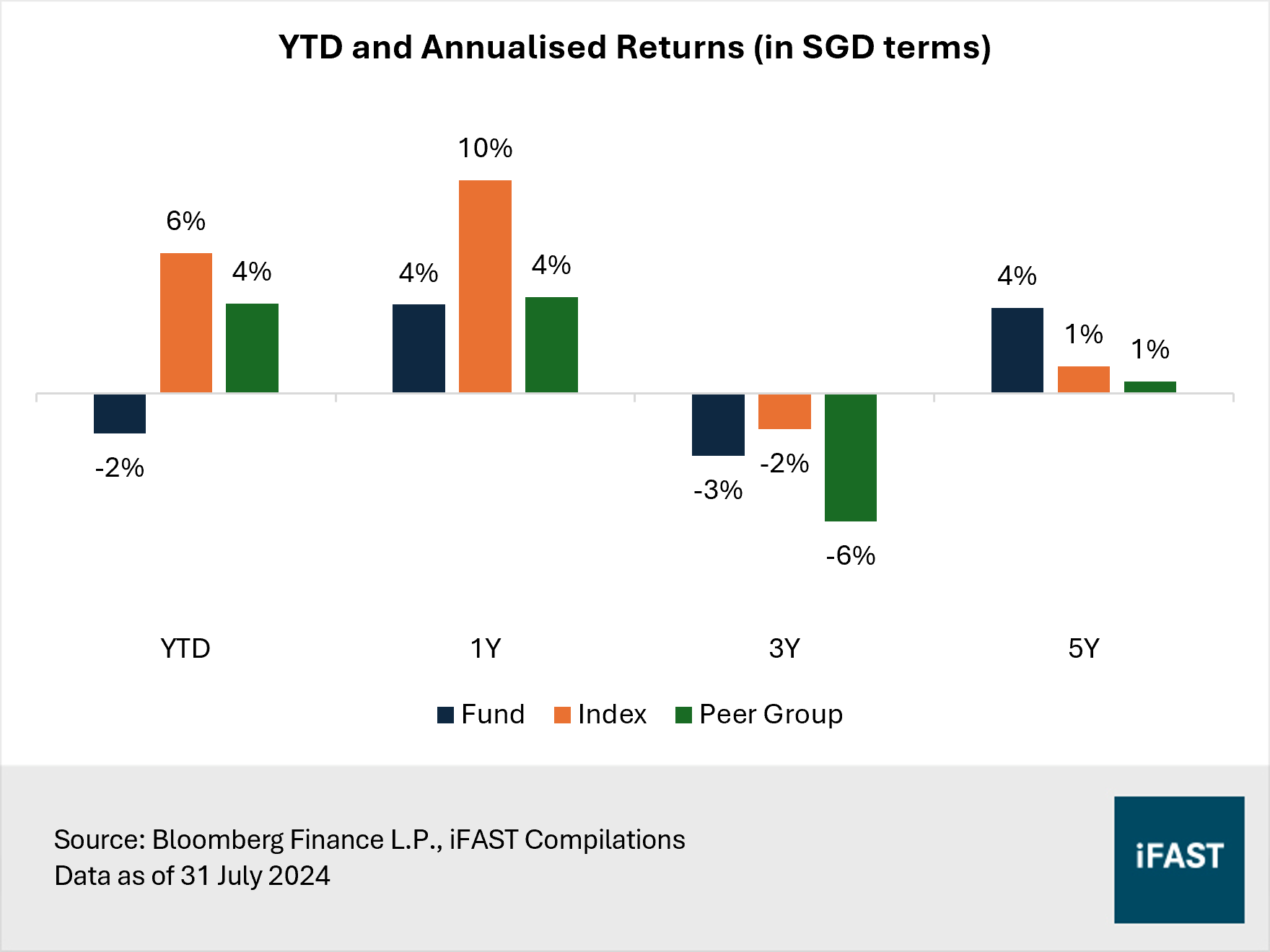

The Janus Henderson Horizon Japanese Smaller Companies Fund’s long-term track record remains strong despite the underperformance year-to-date. It notably delivered stronger three-year and five-year returns relative to its peers (Figure 2). It also compares well against its benchmark over the same periods.

The fund recorded a maximum drawdown of -31.2% over the last five years, slightly less than the benchmark’s -31.7%. This drawdown was also substantially lesser than that of -36.5% average of its peers, highlighting the fund’s effective risk management despite its exposure to companies with smaller market cap.

Figure 2: Outperformance over the three and five-year periods

Final thoughts

In a nutshell, investors might consider adding Japanese small caps to their portfolios through active funds for several compelling reasons. These include the potential to uncover mispriced opportunities with the help of active management, the significant excess capital of Japanese small caps which could drive growth and greater shareholder returns amidst ongoing corporate governance reforms, and the positive impact on corporate earnings from a strengthening Japanese yen.

We like the Janus Henderson Horizon Japanese Smaller Companies Fund which has shown consistency in the strength of its returns. The fund is positioned to capitalise on inefficiencies in the Japanese small-cap market, leveraging a strategy that is anchored in rigorous stock analysis, a deep understanding of company management, and the disciplined management of a high-conviction portfolio.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.