- In the July policy meeting, the BOJ raised short-term interest rates to 0.25%, its second hike in 17 years. It also plans to halve monthly bond buying to JPY 3 trillion by the first quarter of 2026.

- We believe a gradual hike in interest rates won't significantly burden households or major corporations due to their strong balance sheets.

- The BOJ's second rate hike this year signals progress toward economic normalisation. Japan's inflation remains persistent, with services inflation accelerating in June. Higher wages would boost consumption which accounts for about 60% of Japan's GDP.

- We expect the yen to rise against major currencies by year-end due to narrowing yield differentials and a re-direction of flows back to the yen. This should not significantly impact the equity market since the yen is currently very weak.

- Japan remains one of our top equity market picks. We maintain our target price of 48,000 for the Nikkei 225 Index, indicating an upside potential of 26% as of 1 August 2024.

The Bank of Japan (BOJ) held its policy meeting on 30-31 July. In a significant move, the central bank raised short-term interest rates to 0.25% from a range of 0 to 0.1%, marking the second rate hike in 17 years. Additionally, the BOJ unveiled its first plan to reduce bond buying, signalling the start of quantitative tightening after more than a decade.

In this article, we highlight the key takeaways from the BOJ’s latest policy meeting and explain why investors should buy Japan after the recent market correction.

Key takeaways from BOJ’s July policy meeting

The BOJ announced it will reduce its monthly bond buying to around JPY 3 trillion by the first quarter of 2026, down from the current JPY 6 trillion. This plan is largely aligned with market expectations.

However, the timing of BOJ’s second rate hike may have surprised many. According to a Bloomberg poll, only 14 out of 48 economists predicted the hike would occur in July. Most economists did not anticipate the BOJ to conduct a rate hike concurrently with a reduction of bond purchases, as it is seen as an overly hawkish move.

In our market outlook published in early July, we suggested that the acceleration in inflation, alongside improving confidence among consumers and large Japanese manufacturers, could justify further rate increases as soon as the upcoming policy meeting.

(Related article: Market Outlook: Positioning your portfolio for the second half of 2024 and beyond)

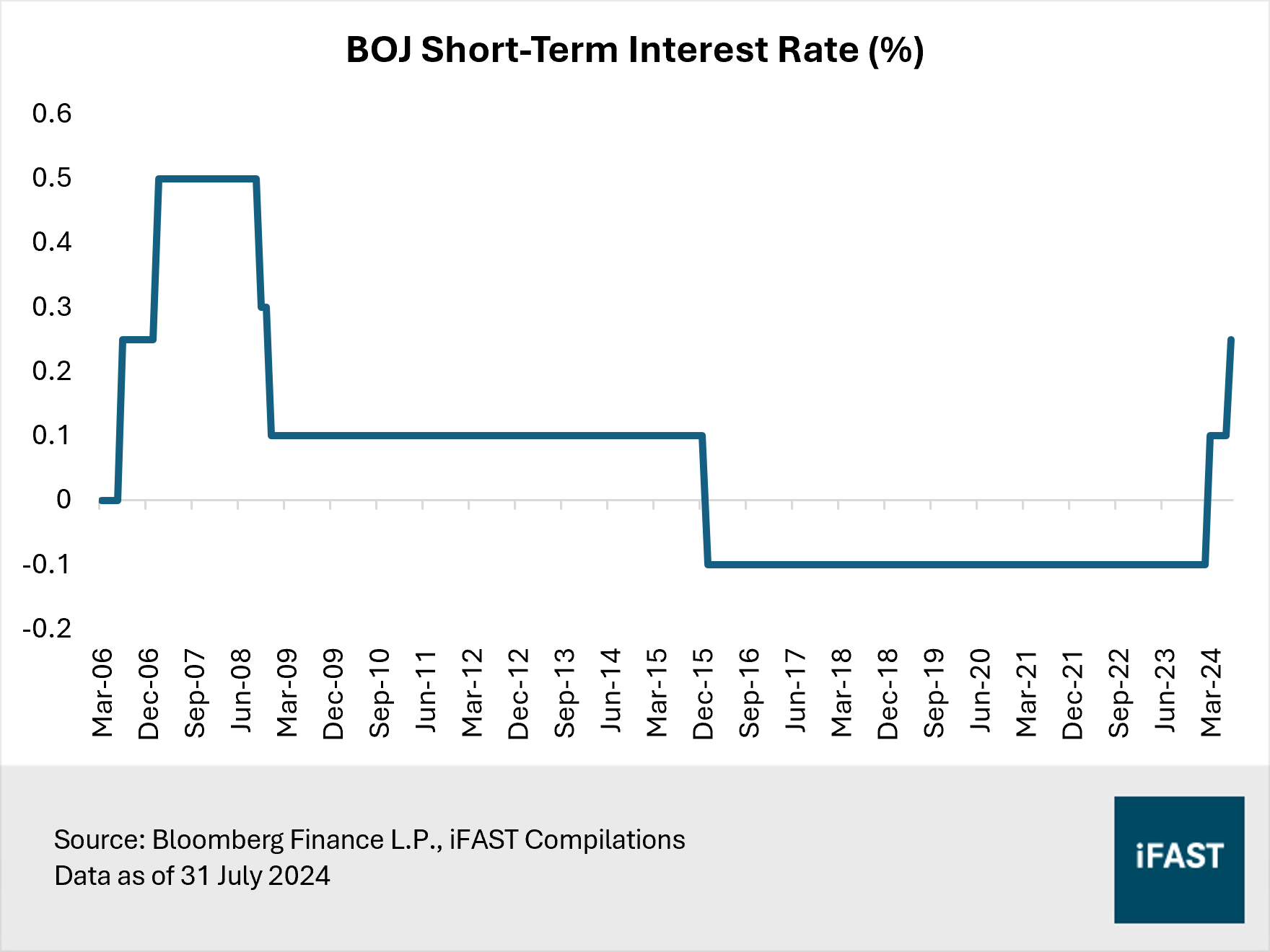

Following the latest rate hike, Japan is currently experiencing the highest interest rates since 2008 (Figure 1). Rates are likely to increase further. The BOJ said it will continue to raise interest rates and tighten the monetary policy, provided that growth and inflation remain on track.

Figure 1: Highest rates since 2008

In an updated quarterly inflation outlook, the BOJ largely maintained its core inflation forecast from April, predicting price growth to stay around 2% through March 2027. GDP growth projections also remained largely unchanged for the 2025 and 2026 fiscal year, with a median forecast of 1.0% for both years. The central bank is sticking to its view that the economy will sustain a recovery led by domestic demand.

Moving towards economic normalisation

We believe the second rate hike by the BOJ this year represents another step toward economic normalisation.

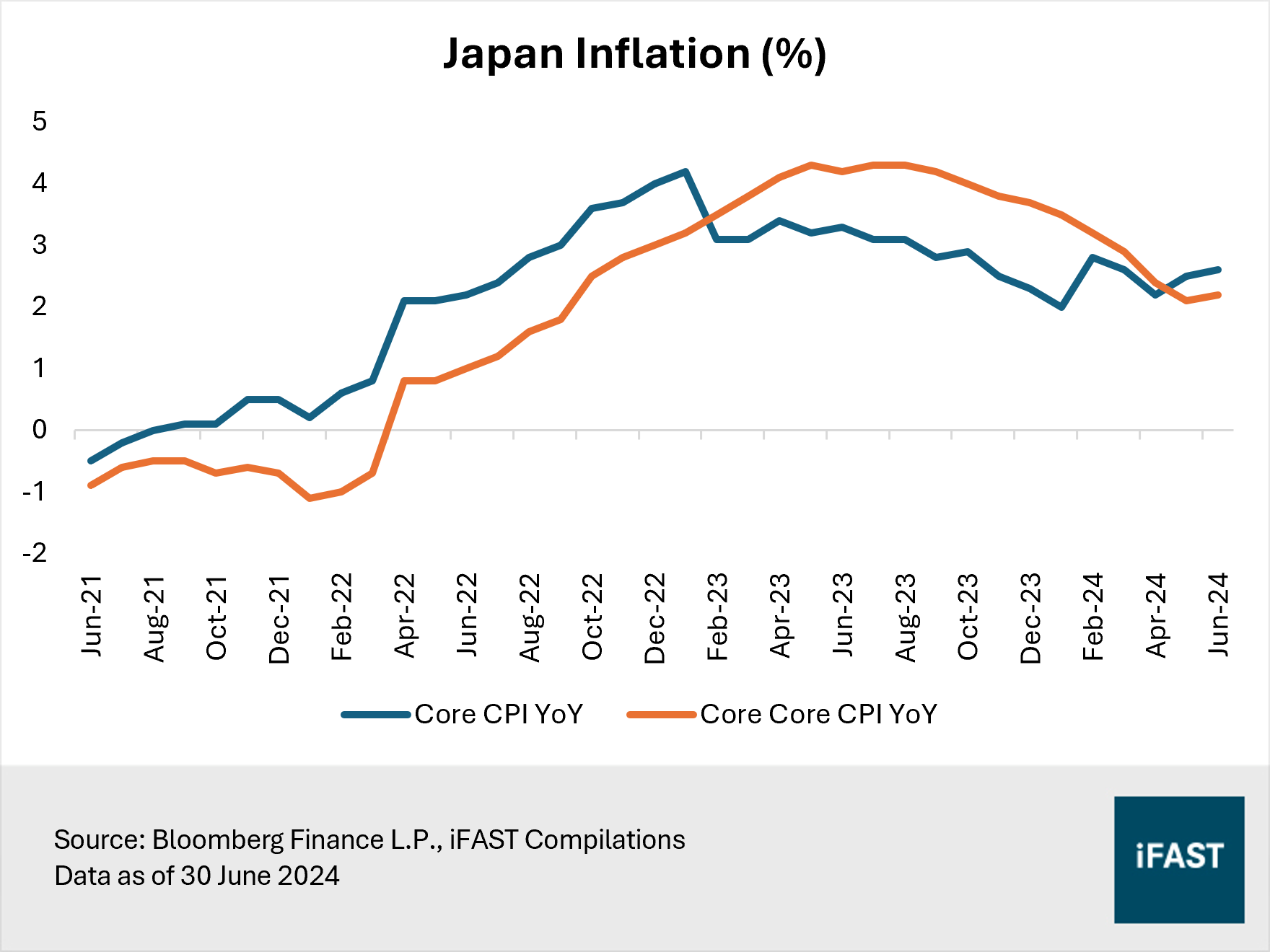

Inflation in Japan appears to be sticky. Core inflation which excludes fresh food but includes fuel costs accelerated to 2.6% year-on-year in June (Figure 2). The core-core inflation gauge that excludes the effects of fresh food and fuel costs, closely watched by the BOJ as a broader price trend indicator, rose 2.2% in June after a 2.1% reading in May. Meanwhile, services inflation picked up to 1.7% in June from 1.6% in May, in a sign that companies have continued to pass on rising labour costs through price hikes.

Figure 2: Inflation remains elevated

Large pay hikes at big firms have partly spread to small firms. According to Rengo (Japanese Trade Union Confederation), small and medium-sized firms in Japan offered an average monthly wage increase of 4.45% in the 2024 spring wage negotiations. While the number fell behind the 5.19% given out by big firms, higher wages overall are likely to help bring inflation-adjusted real wages into positive territory, boosting consumption which makes up roughly 60% of Japan’s total GDP.

We do acknowledge that smaller companies still find it hard to raise prices. They face pressure from customers, often bigger firms, to keep them low. But on a more positive note, the Japan Fair Trade Commission has been releasing names of Japan’s biggest enterprises that it considered to be abusing their dominant bargaining positions. It’s worth noting that naming and shaming is often an effective tactic in Japan.

Also, following significant wage gains this year, Japan’s labour ministry has proposed a record increase in the minimum wage for the fourth consecutive year. This would particularly benefit low-income households, which are most affected by inflation.

We remain optimistic about the prospects of Japan’s economy on the back of moderate inflation with solid wage growth. Meanwhile, borrowing costs rising at a gradual pace are unlikely to create a major burden on households and major corporations, given their strong balance sheets. As Japan’s economy normalises after decades of stagnation, corporate earnings are likely to strengthen, which should drive the stock market higher.

Stronger yen unlikely to hurt the long-term prospects of Japanese equities

At the time of writing, the yen has strengthened to around 150 per dollar. Meanwhile, the 10-year Japanese government bond (JGB) yield rose to as much as 1.07% on 31 July. That said, the dollar-yen is still up by around 6% since the beginning of the year.

After interventions in late April and early May, Japan stepped into currency markets again in July to strengthen a softening yen. Japan’s newly appointed top foreign exchange official remarked that recent yen weakness has done more harm than good for the economy. As such, we believe the likelihood of further FX interventions remains high, which would help prevent further downside for the yen.

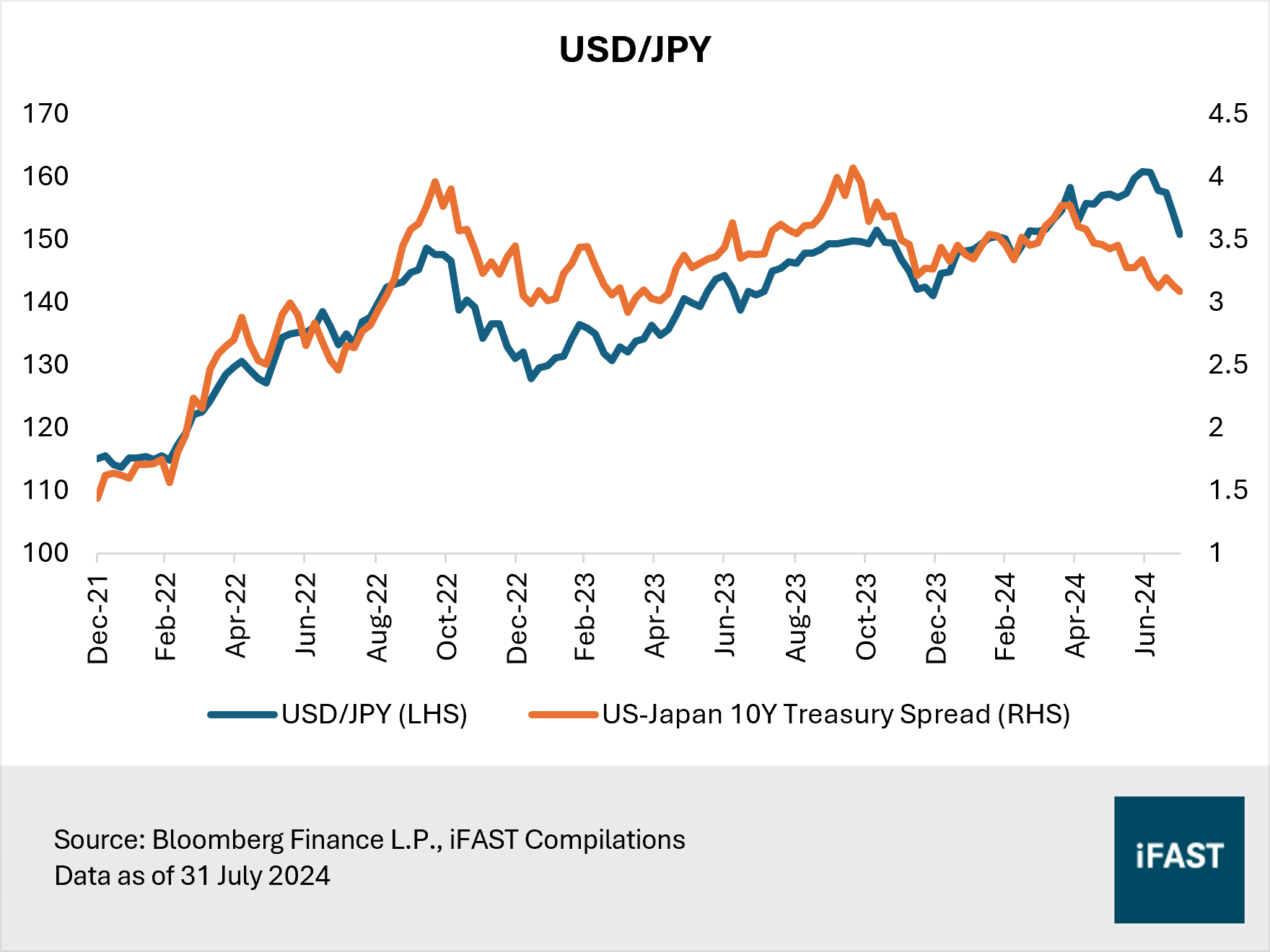

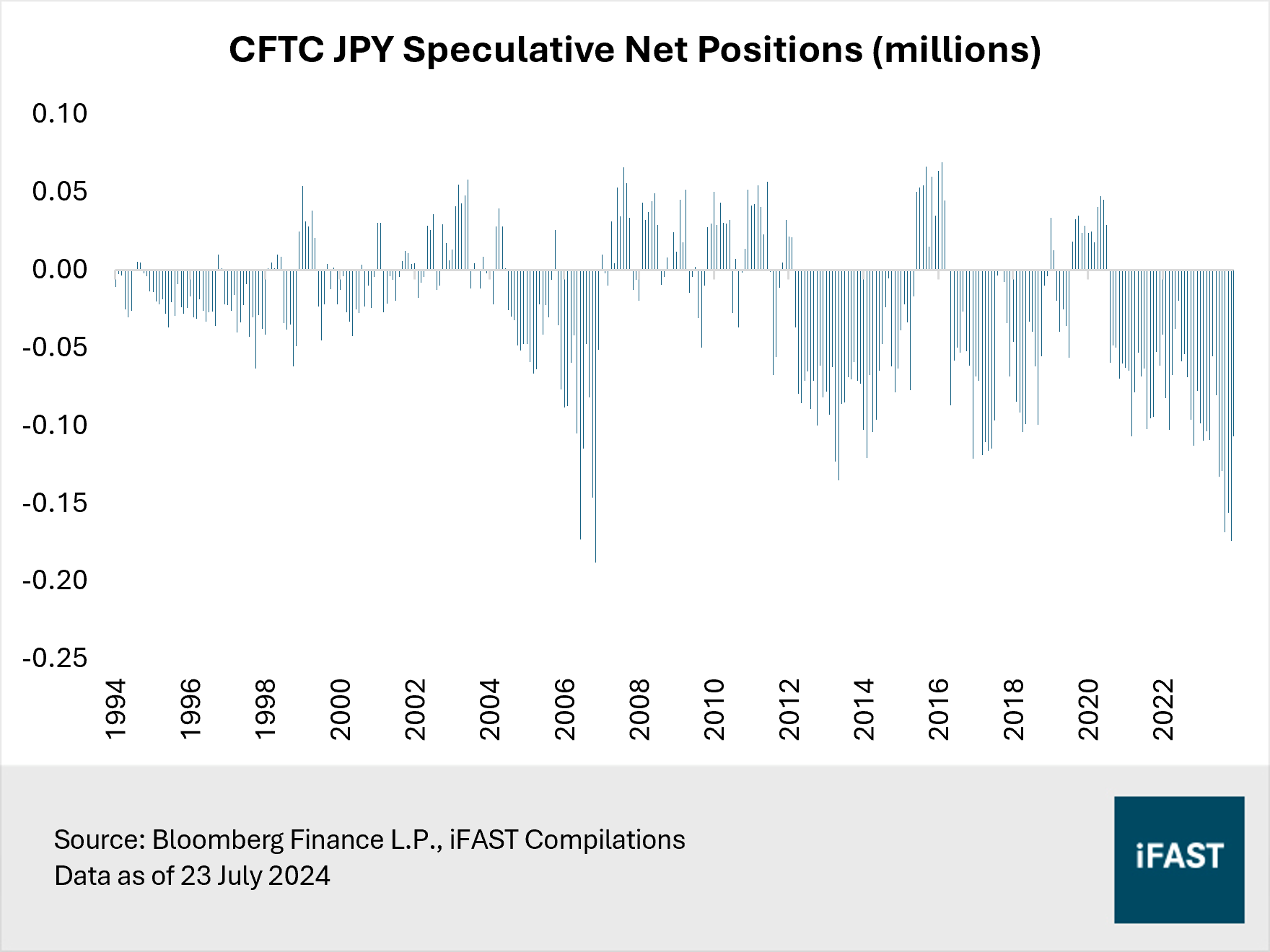

Fundamentally, higher rates and bond yields in Japan should eventually strengthen the JPY (Figure 3). We expect the yen to climb higher against major currencies by the end of the year, on the back of narrowing yield and rate differentials and a re-direction of flows back to the yen. Speculative short yen futures positioning is currently at extreme levels and have plenty more scope to unwind (Figure 4). Continued tightening of Japan’s monetary policy would close the interest rate gap and reduce the attractiveness of the carry trade against the yen.

Figure 3: The yen should move in tandem with yield differentials

Figure 4: Speculative short yen futures positioning is currently at extreme levels

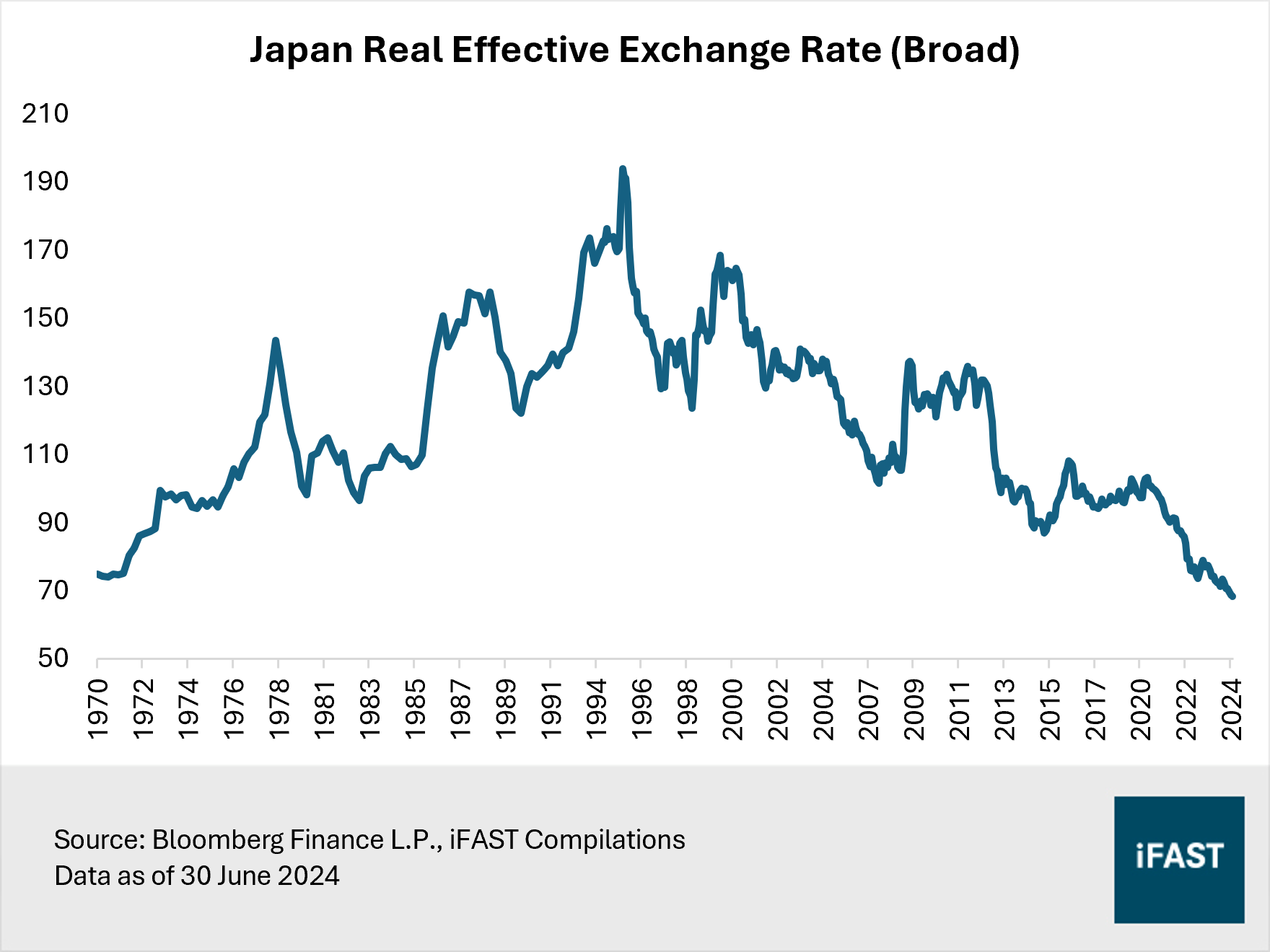

Historically, a weaker yen has been supportive for Japanese equities, largely through the boost in earnings for exporters. However, we believe a stronger yen is unlikely to significantly impact the equity market negatively this time round. This is because the yen's strengthening will be occurring at a time when the currency is exceptionally weak relative to history. The Japan real effective exchange rate (REER), which measures the value of the yen against a basket of peers adjusted by consumer prices, is at an all-time low since data inception in 1970 (Figure 5).

Figure 5: The yen is exceptionally undervalued

Besides, economic conditions and corporate governance are improving, which supports Japanese stocks. As of 30 June 2024, 81% of companies listed on the Prime section (the market division with the highest listing standards) of the TSE have responded to calls to enhance capital efficiency. This is a large jump from the 31% recorded in July last year. As part of plans to improve capital efficiency, Japanese companies are increasing dividends and share buybacks at a record pace, boosting returns for shareholders.

(Related article: This market’s stock rally is likely far from over)

Japan: Our top equity pick

In a nutshell, Japan remains as one of our top equity picks, and for good reasons.

Our optimism is underpinned by a solid long-term investment case for Japan, driven by several key factors like the ongoing shift towards inflation, improvements in economic growth, and corporate governance reforms. In previous articles, we also emphasised Japan’s potential resurgence as a semiconductor powerhouse, driven by government subsidies and the nation’s ambitious plan to produce two-nanometre chips by 2027. In addition, renewed interest from both domestic and foreign investors would drive capital flows into the market. These positive dynamics should outweigh the impact of a strengthening yen.

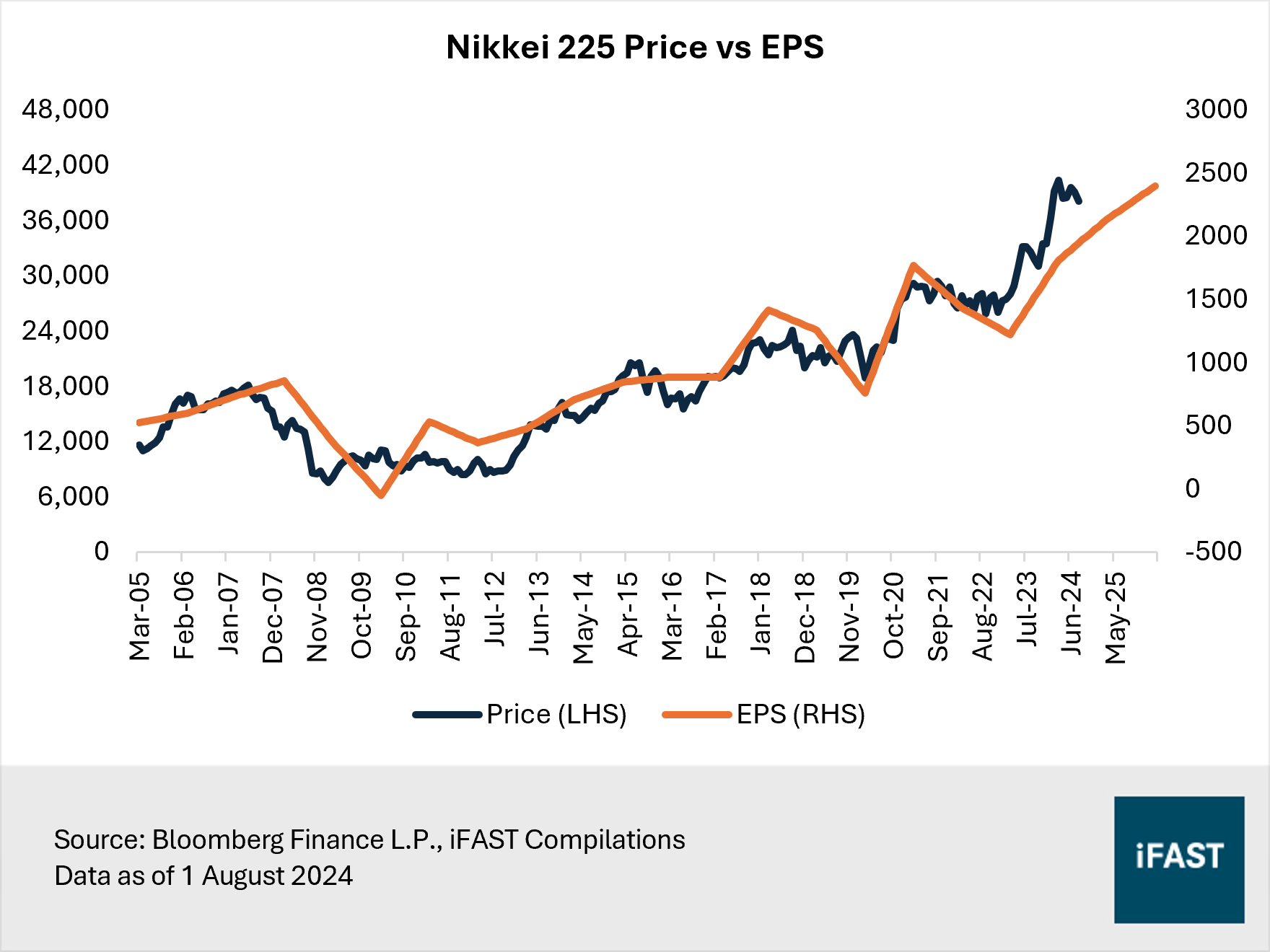

Equity valuations remain attractive. Over 30% of companies in the Nikkei 225 Index are trading below their book values. As corporations continue to report stronger earnings growth and demonstrate higher earnings quality, we expect this to support multiple expansion.

In our view, Japan is only at the start of a multi-year uptrend. Structural drivers are poised to propel Japanese equities to new heights. We maintain our target price of 48,000 for the Nikkei 225 Index, derived from a fair PE ratio of 20X. This target surpasses the all-time high set in mid-July, and indicates a potential upside of 26% as of 1 August 2024.

We recommend investors to maintain exposure to the yen through an unhedged share class. This way, any appreciation of the yen would contribute to the total returns received by investors.

(Related article: Japanese Yen: Too cheap to ignore, potential to break out of its long slump)

Figure 6: Share prices are driven by earnings

Table 1: Projections for the Nikkei 225 Index

|

|

2023 |

2024 |

2025 |

2026 |

|

PE Ratio (X) |

25.9 |

21.0 |

17.9 |

15.9 |

|

EPS |

1,292 |

1,813 |

2,135 |

2,400 |

|

Earnings Growth |

-11.5% |

40.3% |

17.8% |

12.4% |

|

Target Price (based on 20X Fair PE) |

48,000 |

|||

|

Potential Upside |

26% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 1 August 2024 |

||||

Table 2: Recommended products

|

Market |

Product |

|

Japan |

|

|

Japan (Small Cap) |

|

|

Japan (Dividend Paying) |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.