- The recent pullback in share prices of Japanese equities presents a prime opportunity for long-term investors to add to their positions.

- As the semiconductor industry undergoes revolutionary changes due to AI adoption, we anticipate significant benefits for the Japanese economy and equity market.

- Japan is witnessing signs of improvements in economic fundamentals. Corporate earnings are expected to strengthen, propelling the stock market higher.

- Improvements in corporate governance in Japan's stock market are underway, poised to unlock greater shareholder returns.

- Japan remains one of our top equity picks for compelling reasons. Based on a fair PE ratio of 20X, we project a 2026 target price of 48,000 for the Nikkei 225 Index, indicating a 22% upside potential as of 27 June 2024.

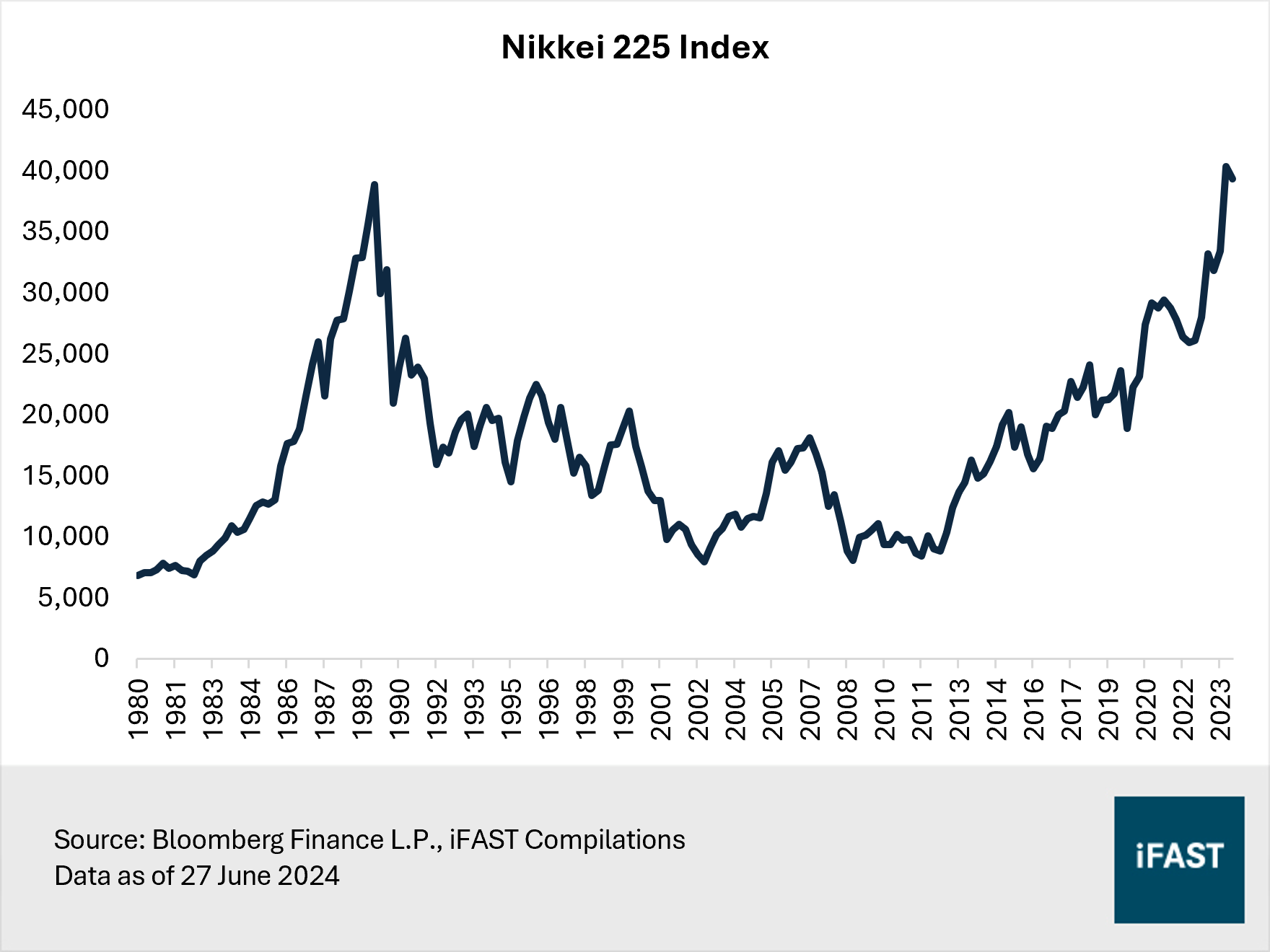

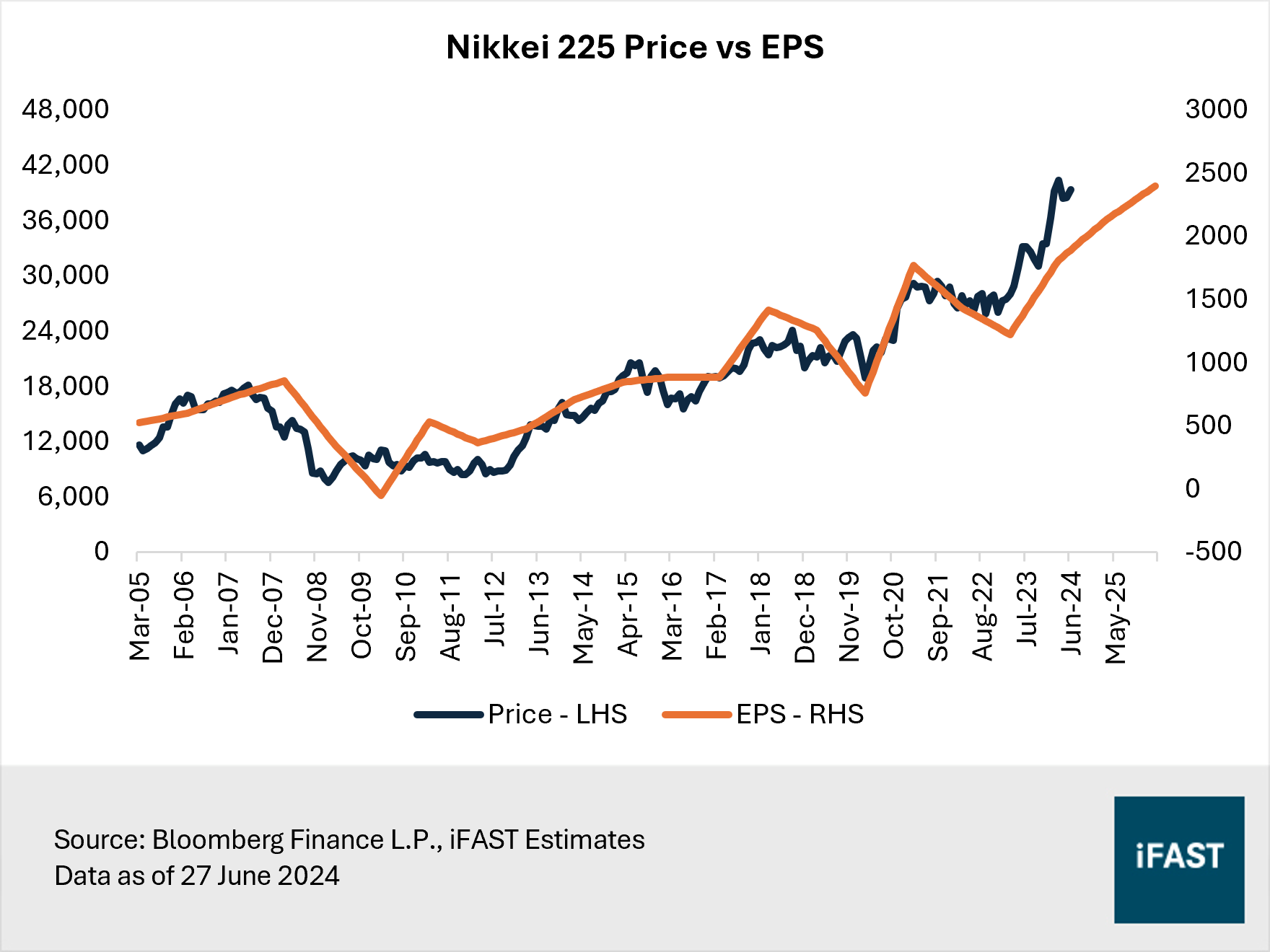

Japan’s equity market has made a stunning comeback after more than three decades. In February this year, the Nikkei 225 Index surpassed its previous all-time high set on December 1989, and then shattered through the 40,000 level in March (Figure 1).

As this exciting new chapter unfolds for the market, we maintain our bullish stance on Japanese equities. Furthermore, the recent pullback in share prices partly due to profit-taking by market participants offers an opportunity for long-term investors to add to their positions in Japanese equities.

Figure 1: The Nikkei 225 Index remains at a three-decade high

(Related article: Reasons to buy Japan and the yen after BOJ’s first hike in 17 years)

Japan and the AI boom

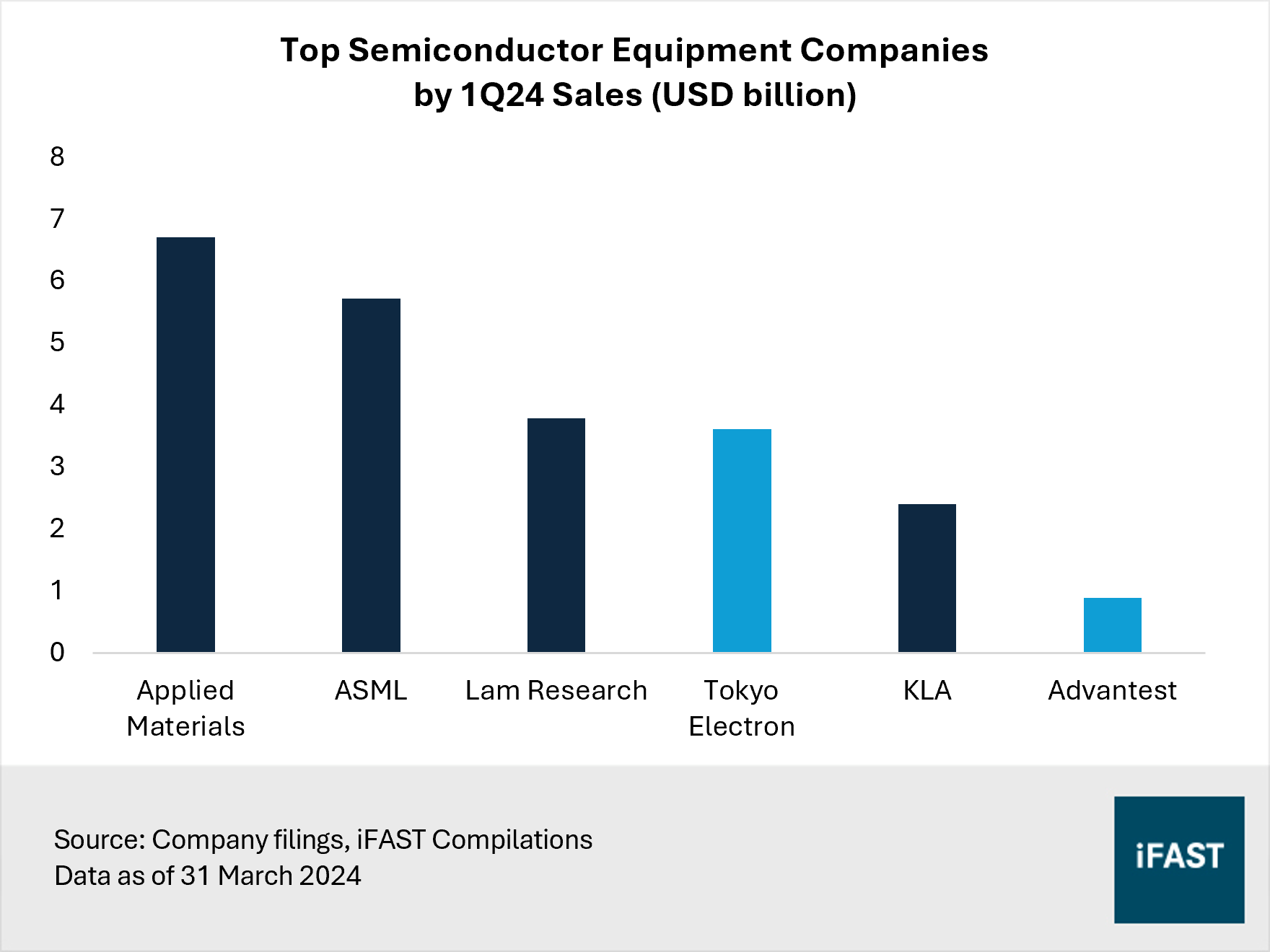

Beyond markets like the US and Taiwan, Japan has emerged as a beneficiary of the powerful artificial intelligence (AI) rally. Prominent Japanese companies whose share prices have surged substantially include Tokyo Electron and Advantest. Notably, gains in Tokyo Electron (TEL) alone have driven nearly 20% of the Nikkei 225’s year-to-date performance.

TEL and Advantest are among the world’s largest makers of semiconductor production equipment, serving chip giants like Intel, TSMC, Samsung, Micron, and NVIDIA (Figure 2). Despite reporting negative earnings growth during the latest earnings season due to lower sales, these semiconductor companies are forecasting a gradual recovery, in line with the global manufacturing upswing.

Figure 2: World’s chip-making equipment giants

Moving forward, TEL is allocating JPY 250 billion for research and development (R&D) for this year as demand recovers. The company has projected double-digit percentage growth in the production of wafer fab equipment (WFE), which is central to its business, helped especially by AI-linked demand. Meanwhile, Advantest's core business revolves around designing and manufacturing chip-testing equipment. It expects sales for semiconductor testers to pick up and reach consecutive record peaks in 2025 and 2026, underpinned by insatiable demand relating to high-performance computing (HPC) and AI.

Beyond TEL and Advantest, Japan's ties with semiconductors run deep. On a national level, Japan is aiming to restore its semiconductor industry to its former glory. Back in the 1980s, Japanese semiconductor manufacturers had dominated the global stage, contributing to over 50% of world production.

As Japan fires on all cylinders, the government has provided substantial subsidies to support the Japanese projects of global chip giants like TSMC, Samsung, and Micron. Furthermore, in a bold move, Japan established Rapidus, which has announced plans to build a plant in Hokkaido to mass produce two-nanometre chips by 2027. In response to the rapid growth of the AI market, Rapidus recently upgraded its revenue target to more than JPY 1 trillion by 2030, up from the initial target of around JPY 1 trillion by 2040.

The ongoing revival of the semiconductor industry has the potential to propel Japan's long-term growth and enhance its self-sufficiency. The country’s critical automotives and electronics industries are reliant on a stable, long-term supply of chips to sustain their growth.

With the semiconductor industry on the cusp of revolutionary change driven by the widespread adoption of AI, we anticipate that the Japanese economy and equity market will reap significant benefits.

Stronger economy supports corporate outlook

Improvements in underlying economic fundamentals will also bolster the Japanese equity market.

While the economy contracted by 1.8% year-on-year from January to March 2024, we recognised that it was due to temporary factors such as the Noto Peninsula earthquake and a reduction in automobile production related to a safety test scandal. Additionally, forward-looking data reveals a resilient outlook among Japanese consumers and businesses.

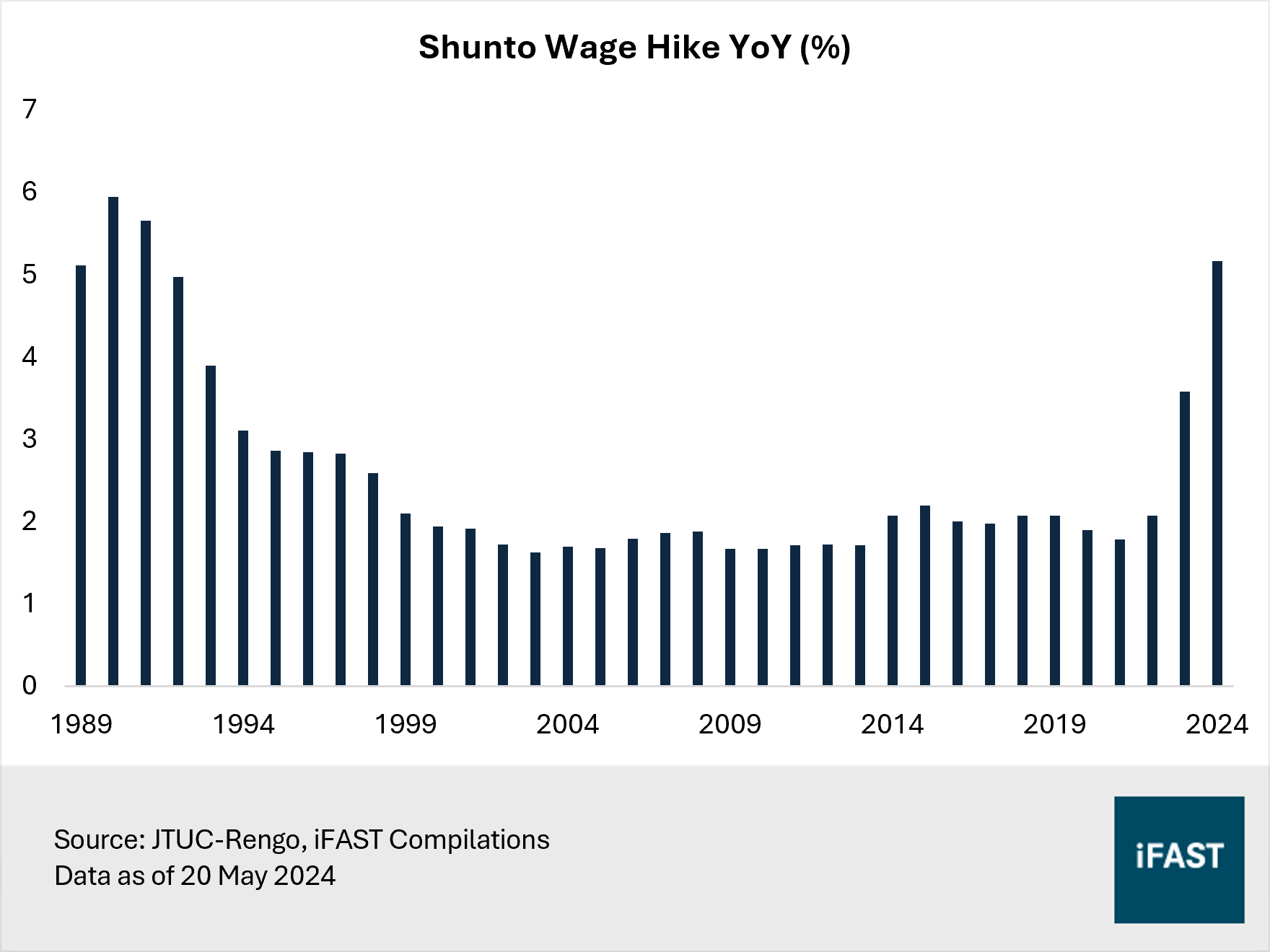

For instance, personal consumption, which makes up around half of the Japanese economy, appears encouraging. According to the latest available data, retail sales have seen the 26th consecutive month of expansion as a recovery in consumption gains momentum following signs of rising wages. In this year’s shunto wage negotiations, unions managed to secure the highest wage increases in over three decades.

Figure 3: This year’s wage hikes are the highest since 1991

Meanwhile, business confidence, gauged by the Reuters Tankan sentiment index, remained in positive territory for the fourth straight month in June. This index is a leading indicator for the Bank of Japan's closely watched Tankan quarterly business survey. As rising wages are expected to underpin consumer spending, business confidence should strengthen in the service sector.

Positive business sentiment often leads to increased investment and hiring. Companies would also be more inclined and able to pass higher costs onto their customer through prices increases, thus boosting corporate margins and earnings. Japanese authorities are hopeful that a virtuous cycle will emerge, where companies boost pay while passing on rising costs to consumers via price hikes.

On the price front, inflation appears to be persistent with the core consumer price index (CPI), which excludes volatile fresh food costs, matching or exceeding the central bank’s 2% target consecutively for more than two years consecutively.

We remain optimistic about the prospects of Japan’s economy on the back of moderate inflation with solid wage growth. As the economy normalises after decades of stagnation, corporate earnings are likely to strengthen, driving the Japanese stock market higher.

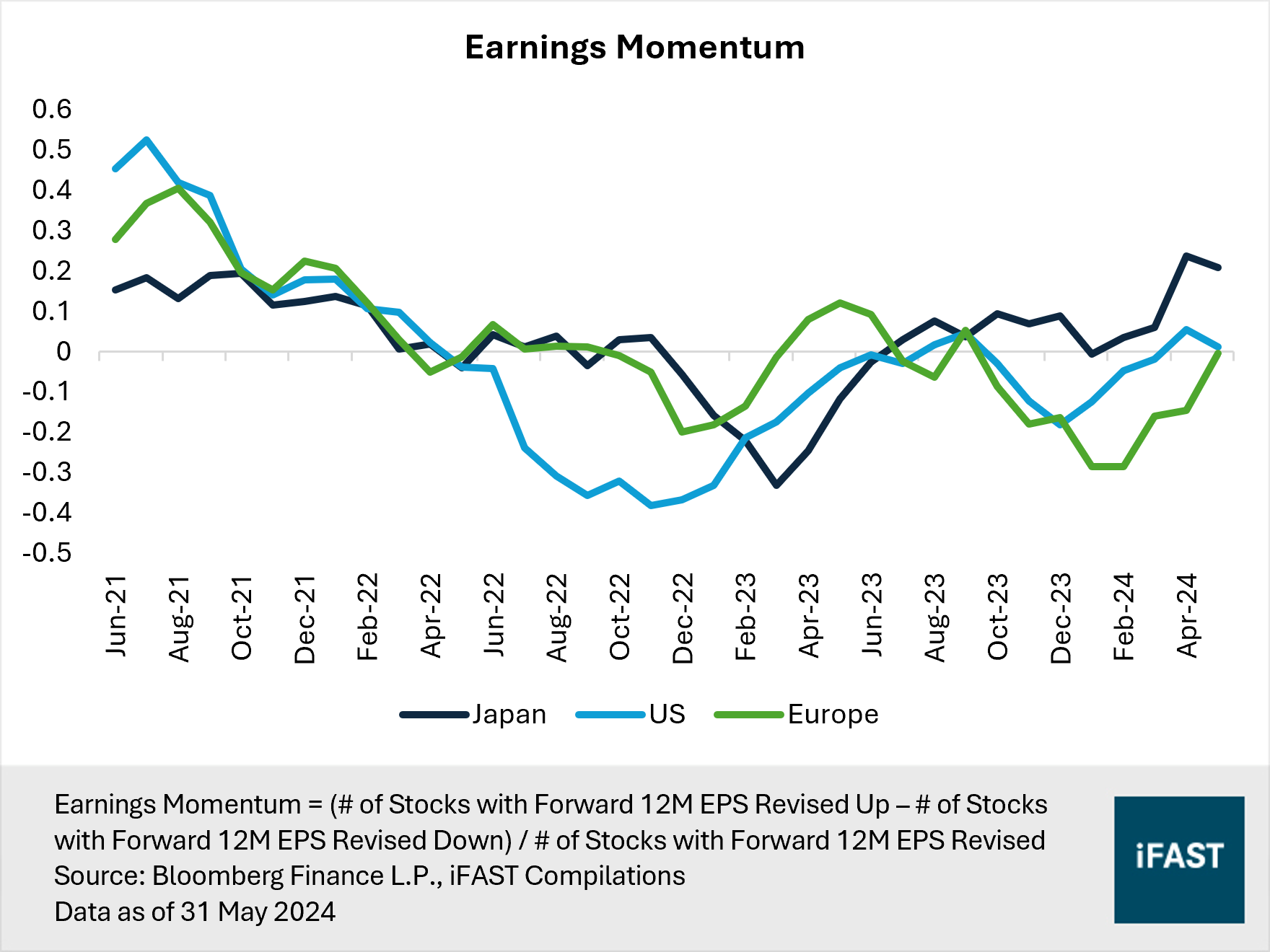

We also note that Japan has outpaced its developed market peers like the US and Europe in terms of earnings momentum (Figure 4). A significant proportion of stocks have experienced upward EPS (earnings per share) revisions. As these upward revisions continue, driven by an improving economy and heightened expectations of future profitability, they are poised to serve as a strong catalyst for driving up share prices.

Figure 4: Japan has seen an overall positive earnings revision since last year

Improvement in corporate governance

Lastly, the wave of improvements in corporate governance within Japan’s stock market are underway, which are set to unlock greater returns for shareholders.

Japanese corporations, known for their large cash reserves accumulated during the Lost Decades, are now primed to put this capital to better use. Over the past decade, the cash and cash equivalents of companies in the Nikkei 225 Index have surged by nearly 200%. The return of inflation presents an ideal opportunity for Japanese companies to optimise their capital utilisation and drive significant growth.

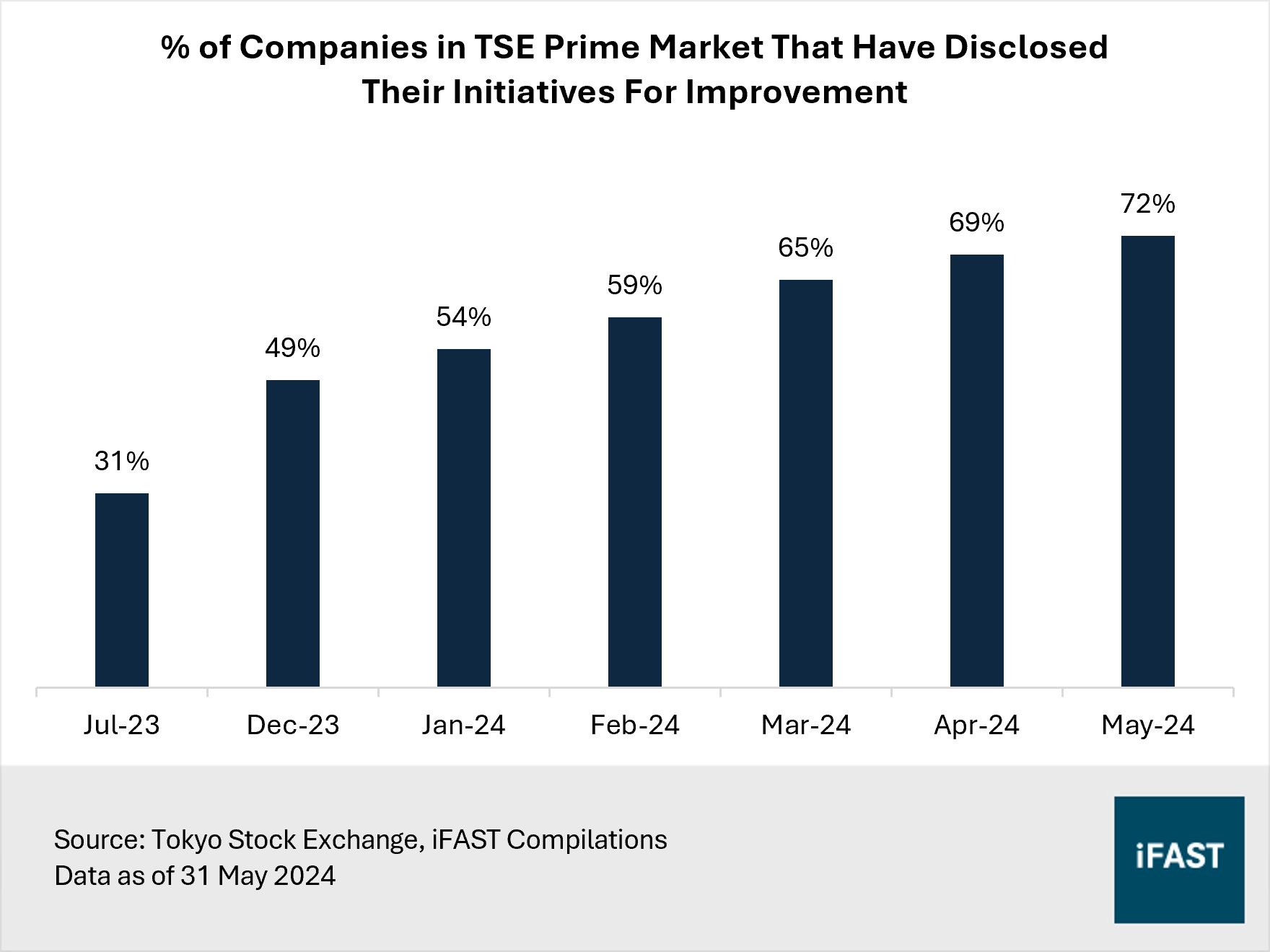

Following pressure from the Tokyo Stock Exchange (TSE) last year, an increasing number of corporations have disclosed long-term plans to improve capital efficiency. Consider this: as of May 2024, a substantial 72% of companies listed on the Prime section (the market division with the highest listing standards) of the TSE have responded to calls to enhance capital efficiency. This represents a large jump from the 31% recorded in July last year.

Figure 5: Corporate reforms are making progress

For some colour, Dai-chi Life Holdings plans to reallocate capital from mature segments, mainly its domestic life insurance business, to areas with high-growth potential, such as asset management.

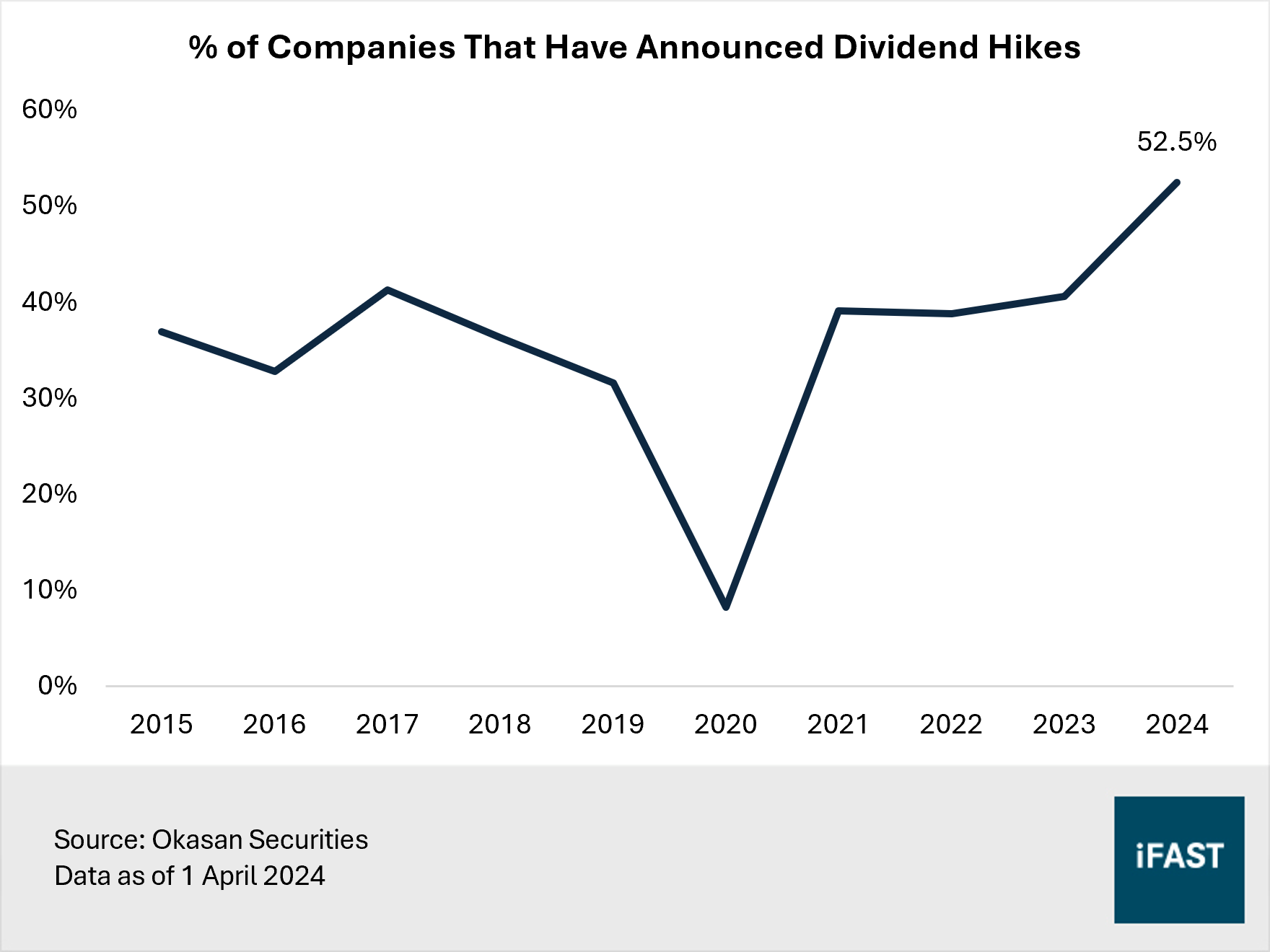

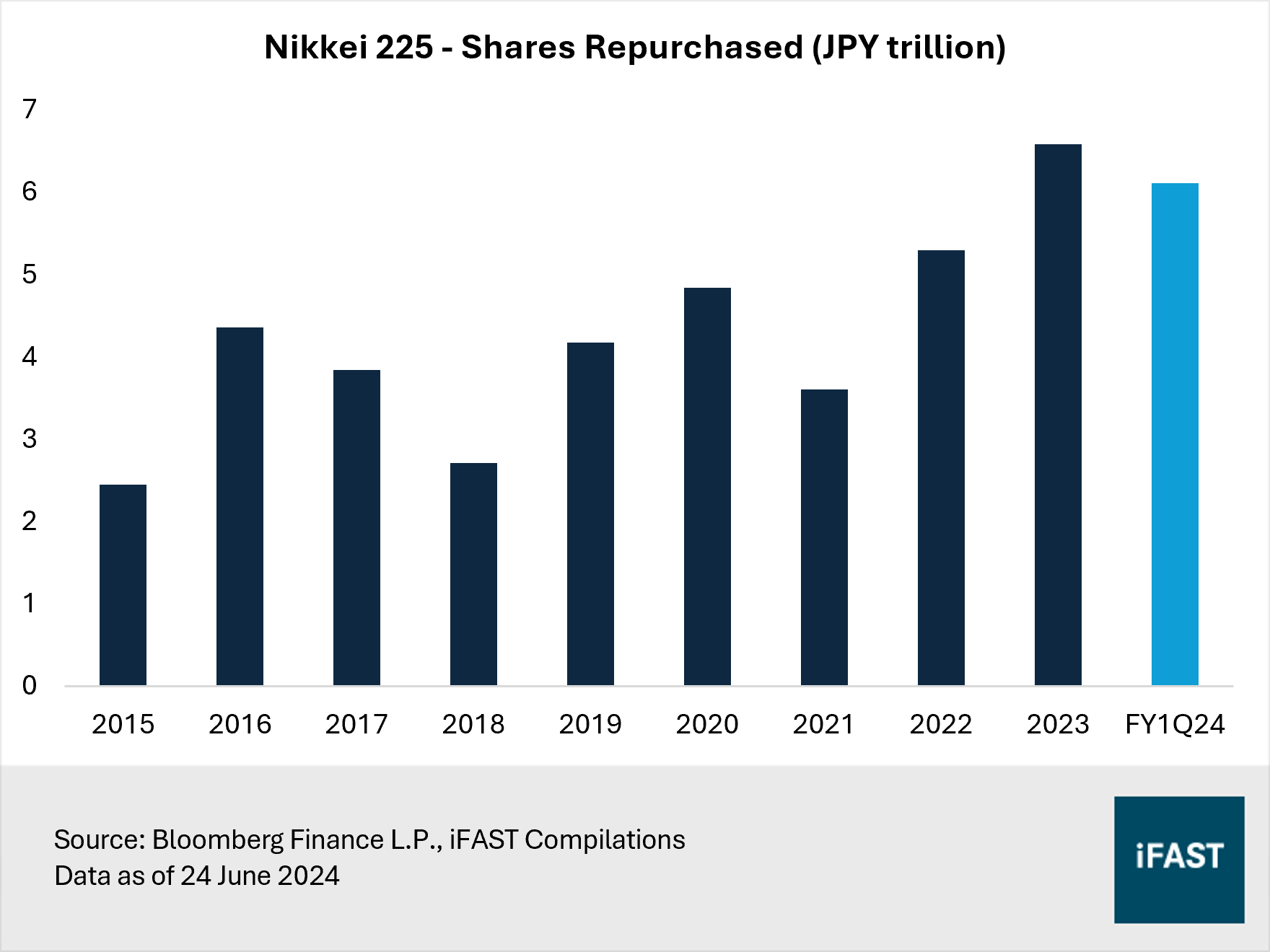

Besides that, Japanese companies are increasing dividends and share buybacks at a record pace. Slightly over 50% of corporations have announced plans to raise dividends in the current fiscal year ending March 2025 – a historic high (Figure 6). Share buybacks have also gained prominence, with the value of repurchases doubling as compared to 2015 (Figure 7). This momentum shows no signs of slowing down. The total amount of share buybacks announced in the first three months of the current fiscal year is already close to the total share buybacks during the entire previous fiscal year. Notable companies that have announced buybacks for the current fiscal year include Itochu, one of the Japanese trading houses backed by Warren Buffett’s Berkshire Hathaway, and Japanese carmaker Toyota Motor.

Figure 6: More dividends

Figure 7: More share buybacks too

Another emerging trend is the reduction of cross shareholdings. Cross shareholdings occurs when firms take strategic stakes in each other to fend off hostile takeovers and maximise control over corporate decisions, often to the detriment of shareholders’ interest. Recognising this, the TSE and regulators have urged companies to reduce cross shareholdings and use the proceeds to improve returns for shareholders. Additionally, Japan's governance code now mandates that companies annually assess the appropriateness of cross-shareholdings.

A case in point would be Japanese regional bank Kyoto Financial Group which faces pressure to deny its president a new term due to the bank’s holdings in major customers. Meanwhile, megabanks Mitsubishi UFJ Financial Group (MUFG) and Sumitomo Mitsui Financial Group (SMFG) plan to start divesting their strategic shareholdings in Toyota Motor, worth a combined JPY 1.3 trillion. These moves highlight a significant shift towards better corporate governance and shareholder value in Japan.

Japan’s surge is far from over

Japan remains as one of our top equity picks, and for good reasons. In our view, the stock market is strongly supported by several structural factors. These include the wave of improvements in corporate governance and the regaining of the country’s lost status as a semiconductor powerhouse amidst the AI boom. Alongside the transformation in underlying economic fundamentals, we believe Japan is set to deliver a solid EPS outlook, which will likely ensure a long runway of growth for the market.

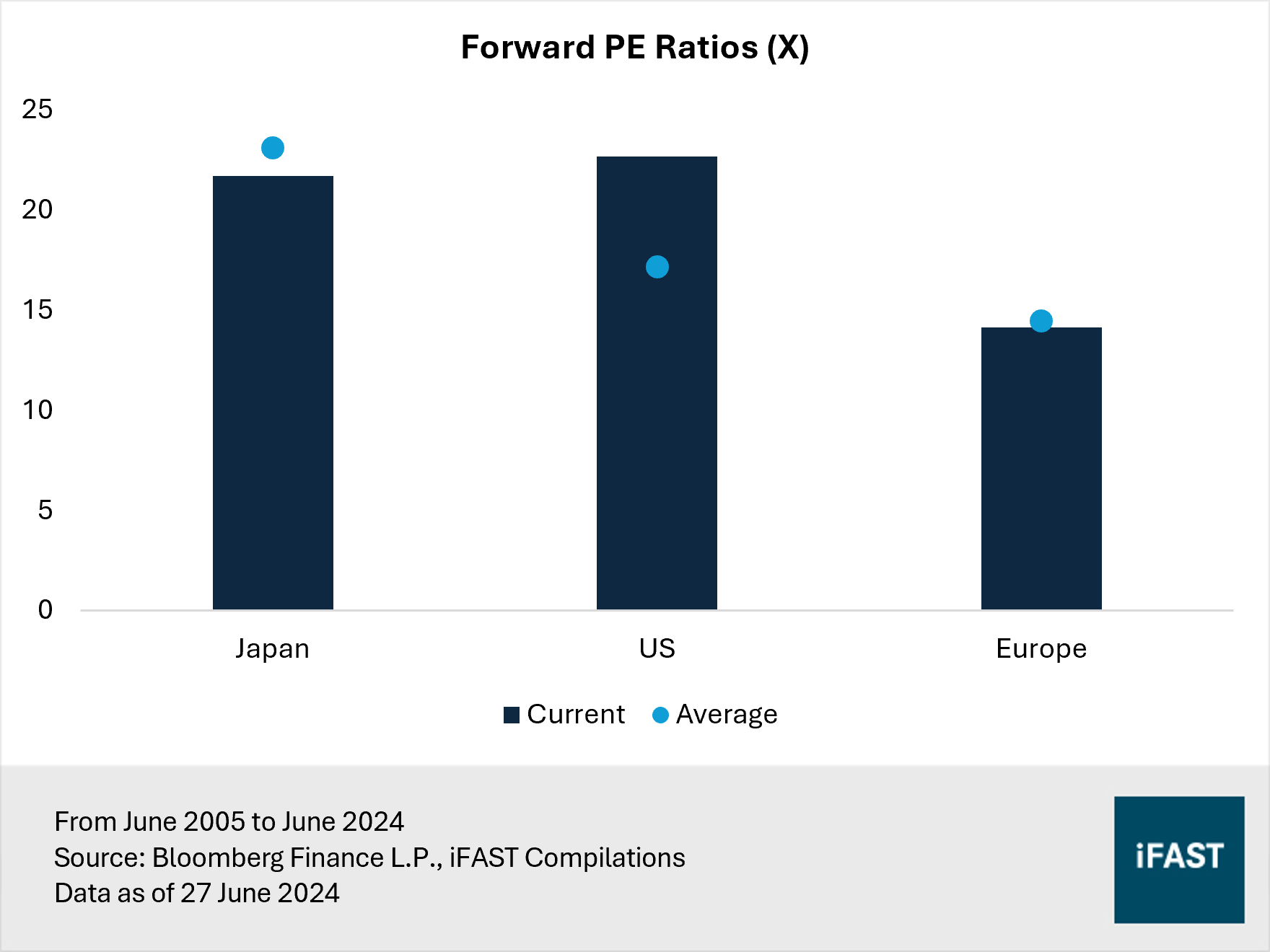

Despite the market’s rise in recent years, Japanese equities remain inexpensive compared to their developed market peers (Figure 8). Besides, more than 30% of companies in the Nikkei 225 Index are still trading below their book values. As companies continue to report stronger earnings growth and demonstrate higher earnings quality following corporate reforms, it supports multiple expansion.

Figure 8: Japan’s valuations do not appear stretched

For those who missed the initial rally, the recent pullback in share prices after reaching the 40,000 level is a golden opportunity to capitalise on what could be a multi-year uptrend. Based on a fair PE ratio of 20X, we project a 2026 target price of 48,000 for the Nikkei 225 Index. This represents an upside potential of 22% as of 27 June 2024.

Figure 9: Share prices are driven by earnings

Table 1: Projections for the Nikkei 225 Index

|

|

2023 |

2024 |

2025 |

2026 |

|

PE Ratio (X) |

25.9 |

21.7 |

18.4 |

16.4 |

|

EPS |

1,292 |

1,813 |

2,135 |

2,400 |

|

Earnings Growth |

-11.5% |

40.3% |

17.8% |

12.4% |

|

Target Price (based on 20X Fair PE) |

48,000 |

|||

|

Potential Upside |

22% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 27 June 2024 |

||||

Table 2: Recommended products

|

Market |

Product |

|

Japan |

|

|

Japan (Small Cap) |

|

|

Japan (Dividend Paying) |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.