- Japan’s banking landscape is dominated by three mega banks: Mitsubishi UFJ Financial Group (NYSE:MUFG), Sumitomo Mitsui Financial Group (NYSE:SMFG), and Mizuho Financial Group (NYSE:MFG).

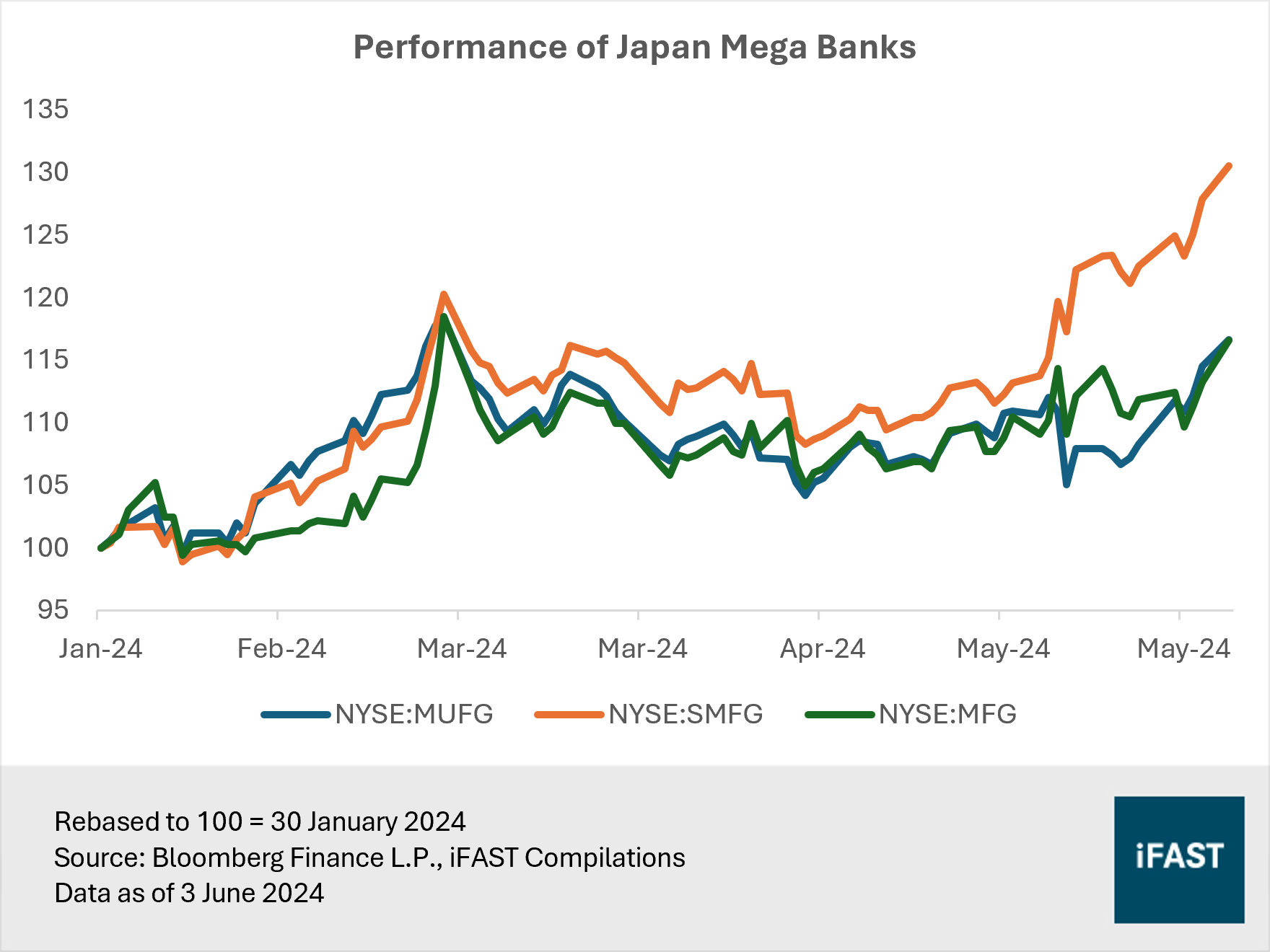

- Since our article on 30 January highlighting the re-rating potential of Japan’s mega banks, their share prices have surged by up to 28%. We believe they remain an attractive investment with room for share prices to climb.

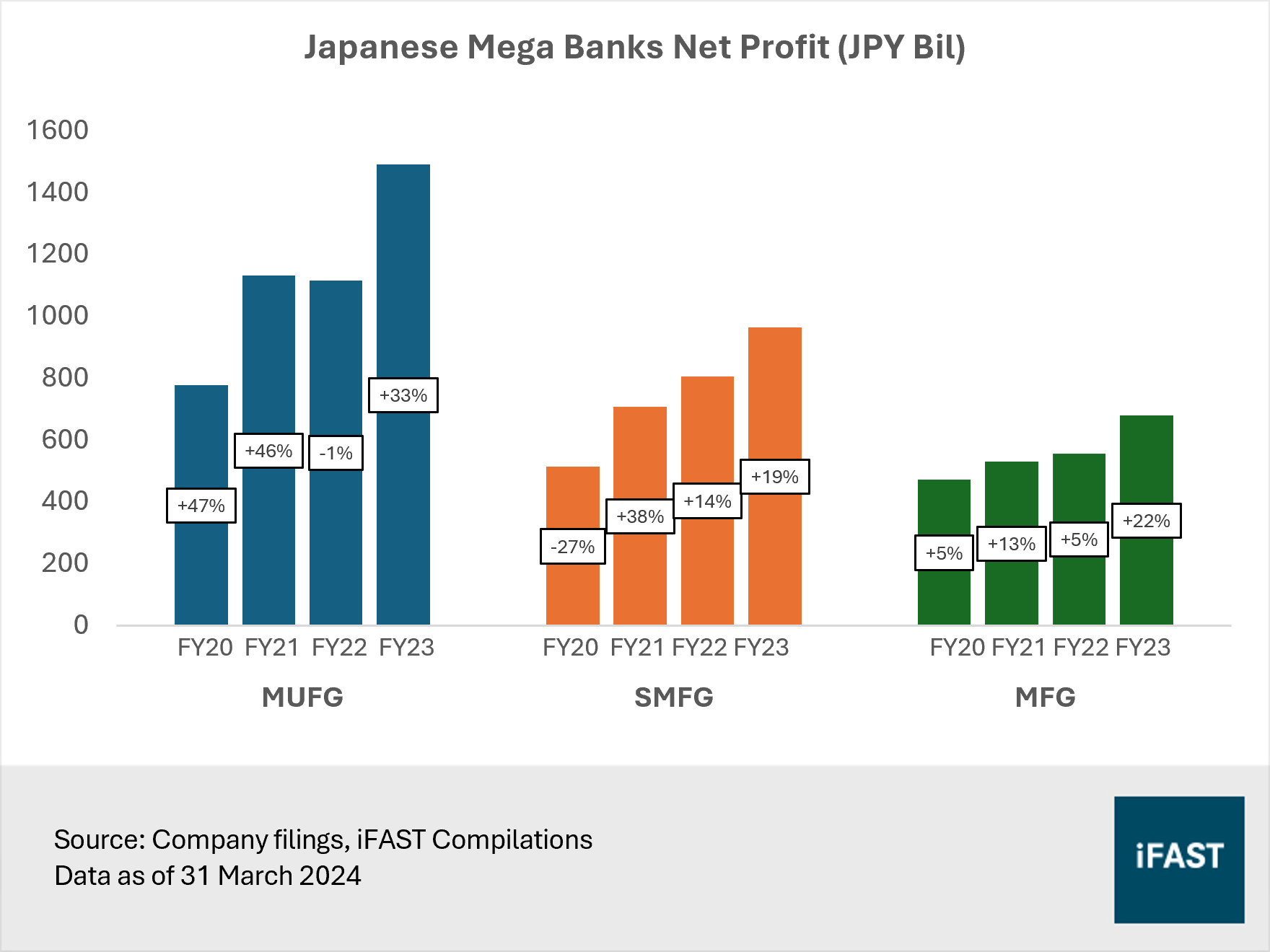

- In the fiscal year ended 31 March 2024, the Big Three's profits reached historic highs. They aim for even higher profits ahead, driven by higher domestic net interest income as the Bank of Japan began normalising monetary policy in March.

- As Japan's economy improves, the banks are also set to experience significant growth in fee-based income. Favourable stock prices and government initiatives further support this trend.

- Based on our fair PB ratios for the mega banks, we project an average upside potential of 15% as of 3 June 2024, along with dividend yields of approximately 3.6% (pre-US withholding tax).

After a downturn sparked by the burst of the real estate bubble and stock market in the 1990s, Japan’s banking landscape witnessed a string of mergers. Today, the sector is dominated by three mega banks. Often referred to as the “Big Three”, they are Mitsubishi UFJ Financial Group (NYSE:MUFG), Sumitomo Mitsui Financial Group (NYSE:SMFG), and Mizuho Financial Group (NYSE:MFG).

In our previous article about Japan’s banking sector on 30 January 2024, we emphasised the significant investment and re-rating potential of the banking giants amidst a transformative phase in the Japanese economy. Since then, their share prices have surged by 17% to 31% in USD terms, now surpassing our 2025 price targets.

In this article, we share why the Japanese mega banks remain an attractive investment proposition with room for share prices to climb.

Figure 1: Share prices of mega banks have risen

Top three banks’ profits hit all-time high, while smaller banks struggle

In the Big Three’s fiscal year ended 31 March 2024, profits reached historic highs since the series of mergers that created these three institutions decades ago.

Mitsubishi UFJ Financial Group (MUFG) reported a net profit of JPY 1,490.7 billion, marking a staggering 33% year-on-year increase and about 30% above its previous record (Figure 2). These robust results were driven particularly by the growth in deposits and loan income due to higher interest rates outside Japan.

Sumitomo Mitsui Financial Group (SMFG) saw profits rise by 19% from the previous year, reaching JPY 962.9 billion. This growth was attributed to the recovery of its brokerage unit, SMBC Nikko Securities, as well as higher domestic and overseas loan income.

Mizuho Financial Group (MFG) experienced a 22% year-on-year increase in net profits, totalling JPY 678.9 billion. This growth was primarily driven by increases in both interest and non-interest income.

Figure 2: Net profits of the mega banks

In our view,

the record-breaking profits of the mega banks underscore their unwavering

strength. It also represents a significantly different narrative compared to

relatively smaller Japanese peers like Aozora and Norinchukin.

For example, Aozora Bank recorded a net loss of JPY 49.9 billion for FY2023 ended March 2024. This was mainly due to the disposal of securities at a loss and the additional booking of reserve funds to prepare for potential losses arising from US commercial real estate loans.

Meanwhile, Norinchukin Bank, Japan’s primary agricultural bank, recorded massive paper losses of JPY 2.2 trillion at end March 2024 from investments in US and European sovereign bonds. The bank had invested in such bonds to seek extra yields, but the aggressiveness of central bank rate hikes and the prolonged duration of high rates exceeded expectations, resulting in significant losses. Norinchukin now plans to realise these losses.

In stark contrast, the mega banks have already sold off their foreign bonds over the past few years, effectively mitigating their risk exposure.

Next leg of growth to be driven by Japan’s monetary policy normalisation

Moving forward, the Big Three are not resting on their laurels and are targeting for profits to hit new highs. For instance, SMFG aims for bottom-line profits to surpass JPY 1 trillion for the fiscal year ended 31 March 2025. This growth is expected to be driven by higher domestic net interest income (NII) as the Bank of Japan (BOJ) began normalising monetary policy this March.

That said, we believe the estimates are fairly conservative, as they assume no further rate hikes in Japan. Furthermore, MUFG, in particular, has factored in substantial reductions in the US policy rate from the current 5.5% to 3.0%.

Our profit outlook for the mega banks is relatively bullish compared to the guidance. We anticipate profits to grow at an average pace of over 9% in the near term. In our view, there are factors driving higher Japanese government bond (JGB) yields and interest rates, which will, in turn, boost the domestic NII of the banking sector.

Table 1: Our estimates for net profits

|

Net Profit (In JPY trillions) |

FY23 (Actual) |

FY24E |

FY25E |

FY26E |

|

MUFG |

1.49 |

1.53 |

1.70 |

1.89 |

|

SMFG |

0.96 |

1.13 |

1.24 |

1.36 |

|

MFG |

0.68 |

0.75 |

0.78 |

0.82 |

|

Source: Company filings, iFAST Estimates Data as of 31 March 2024 |

||||

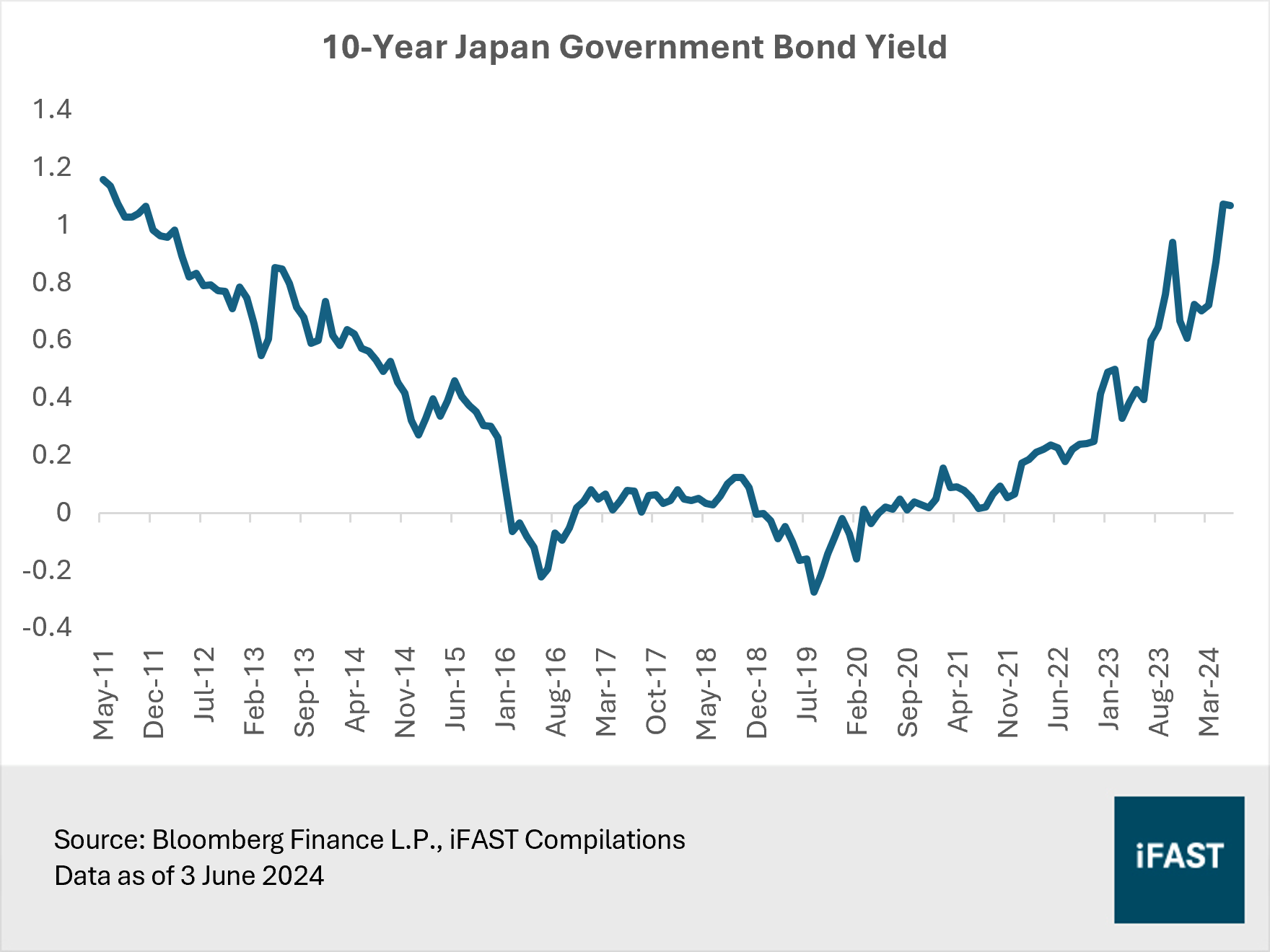

First, the BOJ has scope to gradually increase interest rates, given current projections that inflation could remain at or above the 2% target. Second, we anticipate the central bank to steadily reduce its government bond purchases, paving the way for quantitative tightening. This shift will allow market forces to influence long-term interest rates and bond yields.

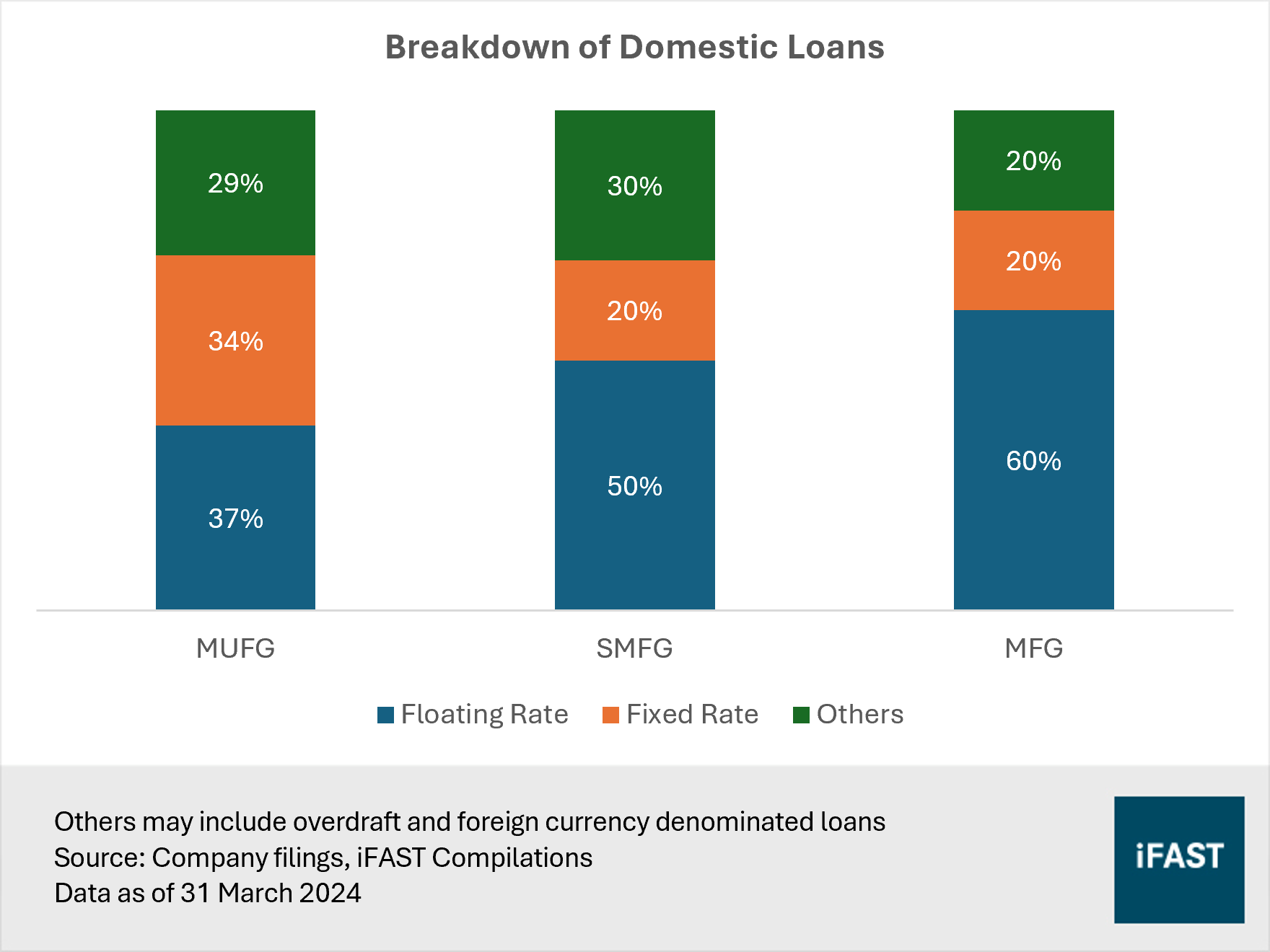

The 10-year JGB yield recently hit a 12-year high of slightly above 1.0%, driven by rising expectations of rate hikes and the reduction of bond purchases (Figure 3). As yields continue to rise, steepening the yield curve, banks should have the opportunity to earn more on loans. With at least 37% of domestic loans at the mega banks being floating rate, they are well-positioned to benefit directly from rising bond yields and interest rates (Figure 4). Coupled with large and stable deposit bases, this would contribute to an improvement in domestic NII.

Figure 3: Yields have hit a 12-year high

Figure 4: A substantial portion of domestic loans are floating rate

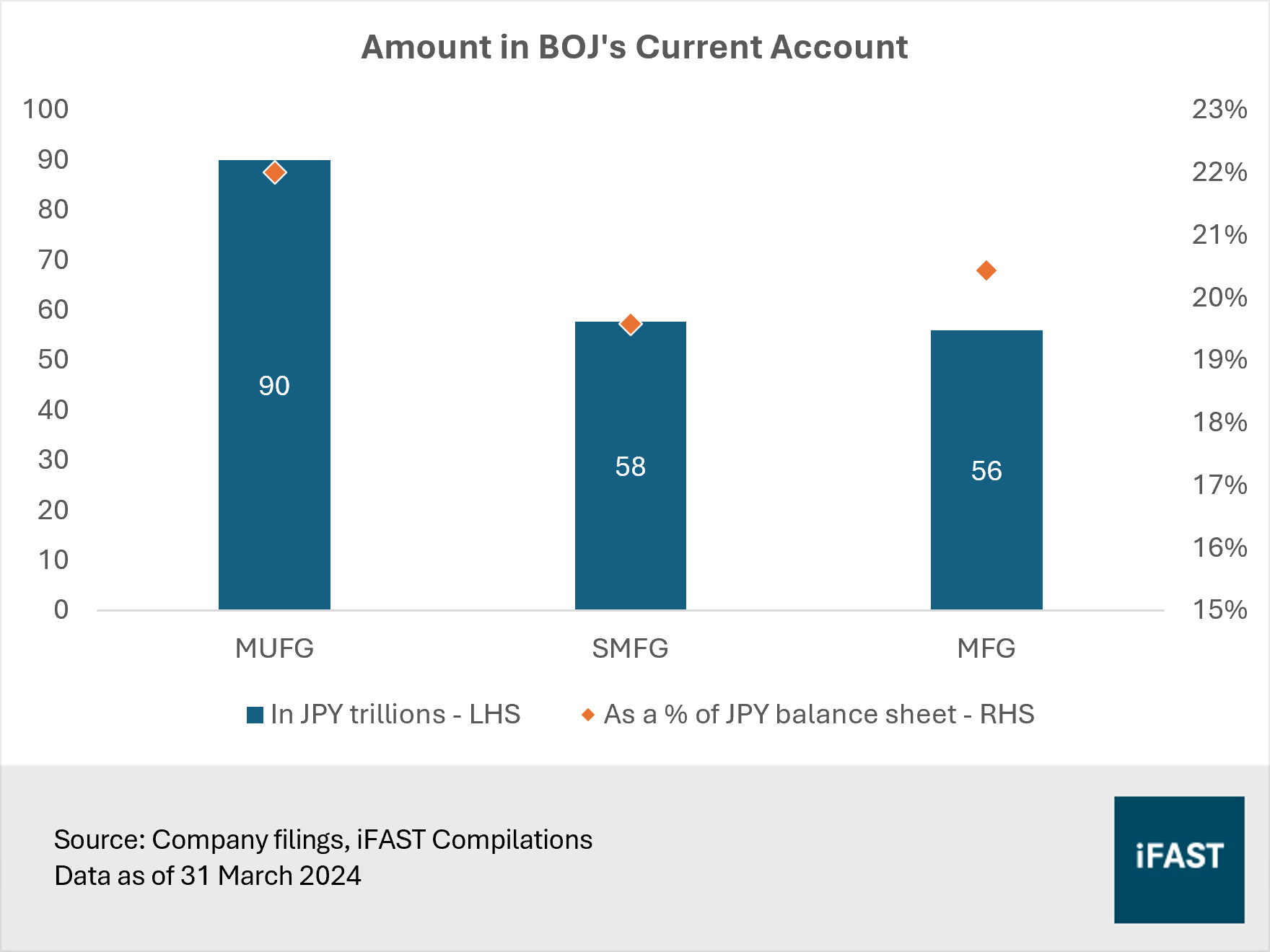

Higher interest rates also mean that the Big Three could earn higher returns on their sizable deposits parked at the BOJ, which had previously incurred negative interest rates before the rate hike in March. At present, the mega banks have a combined JPY 204 trillion parked at the BOJ’s current account, representing at least 20% of the banks’ total assets (Figure 5). With the current interest rate of 0.1%, they collectively earn over a whopping JPY 200 billion from interest, roughly translating to 6% of their net profits on a group level. This underscores the substantial positive impact of rising rates on the banks’ profitability.

Figure 5: The mega banks have substantial assets parked at the BOJ

Wealth & asset management is also a potential driver

As economic conditions in Japan show signs of improvement and normalisation, the Big Three are poised to experience significant growth in fee-based income, driven by increased disposable income and heightened investment activities. Favourable stock prices and government initiatives add to the supportive backdrop.

The strong rebound of the Japanese stock market incentivises domestic investors to shift towards investments as sustainable inflation returns. Moreover, Japan is actively encouraging personal savings and investment. In January this year, the government revamped the Nippon Individual Savings Account (NISA), allowing Japanese citizens to grow their money tax-free indefinitely. This makes it easier and more attractive for people to build their wealth over time, presenting a substantial opportunity for banks’ wealth & asset management divisions.

In fact, SMFG is capitalising on this opportunity, aiming to expand its wealth management business. The bank targets gross profits from this division to grow from JPY 299.6 billion to JPY 320 billion by March 2027, representing a robust compound annual growth rate (CAGR) of 10%.

On the other hand, MUFG and MFG have laid out targets for their asset under management (AUM). MFG anticipates AUM to rise from JPY 29.6 trillion to JPY 32 trillion by FY2025, translating to a CAGR of 4%. MUFG aims to boost AUM from JPY 123 trillion to JPY 200 trillion by FY2029, achieving a solid CAGR of 8%.

Key investment risks

Contagion from smaller banks: Stress seen at smaller Japanese banks like Norinchukin and Aozora have led to concerns about a potential banking crisis in Japan, akin to what happened in the US last year. This could lead to contagion effects at a broader level, as seen when large US banks had to pay hefty fees to help recoup costs incurred following the failures of regional banks like Silicon Valley Bank and Signature Bank.

Despite this, we recognise that the banking giants maintain strong capital buffers. The common equity tier 1 (CET1) ratios of MUFG, SMFG, and MFG stand at 10.1%, 9.9%, and 9.8% respectively. These are well in excess of the regulatory minimum of 4.5%, providing considerable cushion against potential losses.

Pick-up in non-performing loans and BOJ's reluctance to tighten further: Higher rates could lead to an uptick in non-performing loans and a deterioration in asset quality, especially considering that a substantial portion of loans in Japan are floating rate. Additionally, Japan may be cautious of the economic impact of higher rates. This could result in the BOJ's reluctance to tighten further, potentially negatively affecting the growth of banks.

15% upside potential even after this year’s strong gains

Overall, we are confident that Japan’s banking giants may experience stronger earnings momentum compared to many of their global peers, who are already facing peak interest rates. Japanese mega banks are well-positioned for a new phase of growth during this transformative period in the domestic economy, driving profits to new heights. This growth is supported by higher domestic net interest income (NII) from rising yields and interest rates, as well as increased fee-based income driven by opportunities in the wealth and asset management sectors.

Using estimated ROE figures ranging between 8% and 9% as well as cost of equity of around 10%, we have assigned fair PB ratios of 0.90X, 0.80X and 0.75X to MUFG, SMFG, and MFG respectively. Based on this, we project new target prices that translate to an average upside potential of approximately 15% for the mega banks in the next two years (Table 2). That said, we believe SMFG’s upside potential has narrowed substantially after a gain of nearly 40% this year.

As part of their medium-term business plans, the mega banks are committed to enhance return on equity (ROE) and increase shareholder value sustainably. Both MUFG and SMFG have announced share buybacks of JPY 100 billion each.

In addition, the banking giants have pledged to progressively increase their dividends in tandem with profit growth. With a target payout ratio of 40%, investors can expect to receive dividend yields of around 3.6% (before US withholding tax of 30%), adding an extra layer to compelling investment proposition of Japan’s mega banks.

Table 2: Our target prices for Japan’s mega banks

|

Name |

Fair PB |

Target Price (USD) |

Current Price (USD) |

Upside Potential |

Forward Dividend Yield |

|

0.90X |

12.70 |

10.84 |

17% |

3.5% |

|

|

0.80X |

14.70 |

13.38 |

10% |

3.6% |

|

|

0.75X |

5.00 |

4.22 |

18% |

3.9% |

|

|

Average |

15% |

3.6% |

|||

|

Dividends are before US withholding tax of 30% Source: Bloomberg Finance L.P., iFAST Estimates Data as of 3 June 2024 |

|||||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.