- Japan’s banking landscape is dominated by three mega banks: Mitsubishi UFJ Financial Group (NYSE:MUFG), Sumitomo Mitsui Financial Group (NYSE:SMFG), and Mizuho Financial Group (NYSE:MFG).

- In particular, MUFG and SMFG have achieved record-breaking net profits largely due to the growth in deposits and loans income from higher interest rates outside Japan. This prompted them to launch share repurchase programs, alongside an increase in dividend guidance.

- As the BOJ charts a course toward policy normalisation, the banking giants are anticipated to be the primary beneficiaries of higher Japanese government bond (JGB) yields due to their large and stable deposit bases as well as the flexibility to raise lending rates.

- As inflation prompts a shift in investor behaviour towards riskier assets, coupled with the resurgence of the domestic stock market, the mega banks can capitalise on increased trading activity and demand for investment products.

- Based on our fair PB ratios assigned to the mega banks, we project an average upside potential of around 17% (as of 29 January 2024). This comes alongside dividend yields of approximately 4% (pre-US withholding tax).

Japan’s banking sector has withstood significant challenges. In the 1990s, it grappled with a mountain of non-performing loans (NPLs) triggered by the burst of the real estate bubble and stock market. This contributed to several bank failures, and cast a shadow of economic stagnation and deflation over the country for decades. Such adverse conditions hurt loan growth, fuelled the re-emergence of NPLs, dampened non-interest revenue streams, while net interest margins (NIMs) were squeezed by an ultra-loose monetary policy.

Some banks underwent major transformations, mainly in the form of mergers, to weather the downturn. Today, Japan’s banking landscape is dominated by three mega banks, often referred to as the "Big Three": Mitsubishi UFJ Financial Group (NYSE:MUFG), Sumitomo Mitsui Financial Group (NYSE:SMFG), and Mizuho Financial Group (NYSE:MFG).

In this article, we explore the investment potential of Japan’s mega banks against the backdrop of an emerging economic narrative that is poised to reshape the sector’s growth trajectory.

Record profits buoyed by higher rates overseas

The mega banks delivered commendable performances in the first half of fiscal year 2023/24 ended September. In particular, the largest banking group, Mitsubishi UFJ Financial Group (MUFG), posted a record-breaking net profit of JPY 927.2 billion, marking an enormous increase of 301.4% year-on-year (Figure 1). This surge was mostly due to the absence of one-time losses recorded last year from the sale of its US banking unit Union Bank.

Figure 1: Record high profits from MUFG and SMFG

Beyond that, the major driving force behind MUFG’s highest-ever set of results was the improvement in customer segments, such as the growth in deposits and loans income from higher interest rates outside Japan. Supported by its solid profits, the bank announced a share repurchase program worth up to JPY 400 billion between November 2023 and March 2024, setting a new record for an interim period.

Meanwhile, the net profit of Sumitomo Mitsui Financial Group (SMFG) rose slightly by 0.2% y-o-y to JPY 526.5 billion – a record-high for the half-year period. This was underpinned by an expansion in domestic and overseas loan income, as well as an uptick in non-interest income attributed to the recovery of its brokerage unit SMBC Nikko Securities. Consequently, the management raised their dividend per share (DPS) forecast by 12.5% compared to the previous year. Alongside this dividend increase, SMFG unveiled a share buyback program of JPY 150 billion, underscoring its commitment to return excess capital to shareholders in a flexible manner.

Lastly, Mizuho Financial Group (MFG) saw a 24.4% y-o-y rise in net profit to JPY 415.7 billion. The bank benefitted from strong lending overseas and an increase in sales & trading revenues. As a result, it adjusted its full-year DPS guidance upwards, representing a rise of 18% from the previous year.

It is worth highlighting that the “Big Three” currently generate approximately 50% of their revenue from domestic operations, with the remaining portion primarily from countries/regions such as the US and Asia excluding Japan. We believe that even with rate cuts, interest rates outside Japan especially in the US will remain higher for longer when compared against the past decade. This supports the case for elevated net interest income (NII) overseas.

At the same time, we are witnessing the emergence of new economic trends within Japan, especially as the central bank gradually normalises its monetary policy. This, in our view, sets the stage for the mega banks to enter into a new era of heighted growth and profitability.

Higher rates at home would favour mega banks

In a pivotal move in October 2023, the BOJ discarded its explicit 1% ceiling for 10-year JGB yields. As mentioned in previous articles, signs of sticky inflation in Japan suggests that the yield curve control (YCC) is become increasingly unsustainable. Japan has also signalled a gradual move towards ending its ultra-easy monetary stance, with BOJ Governor Ueda acknowledging a rising probability of achieving the long-term inflation target. As such, we see more room for Japanese government bond (JGB) yields to adjust upwards.

Related articles:

The resurgence of Japan: A new era of multi-year tailwinds with upside potential of 30% by 2025

Japanese Yen will be one of the top performing currencies in 2024

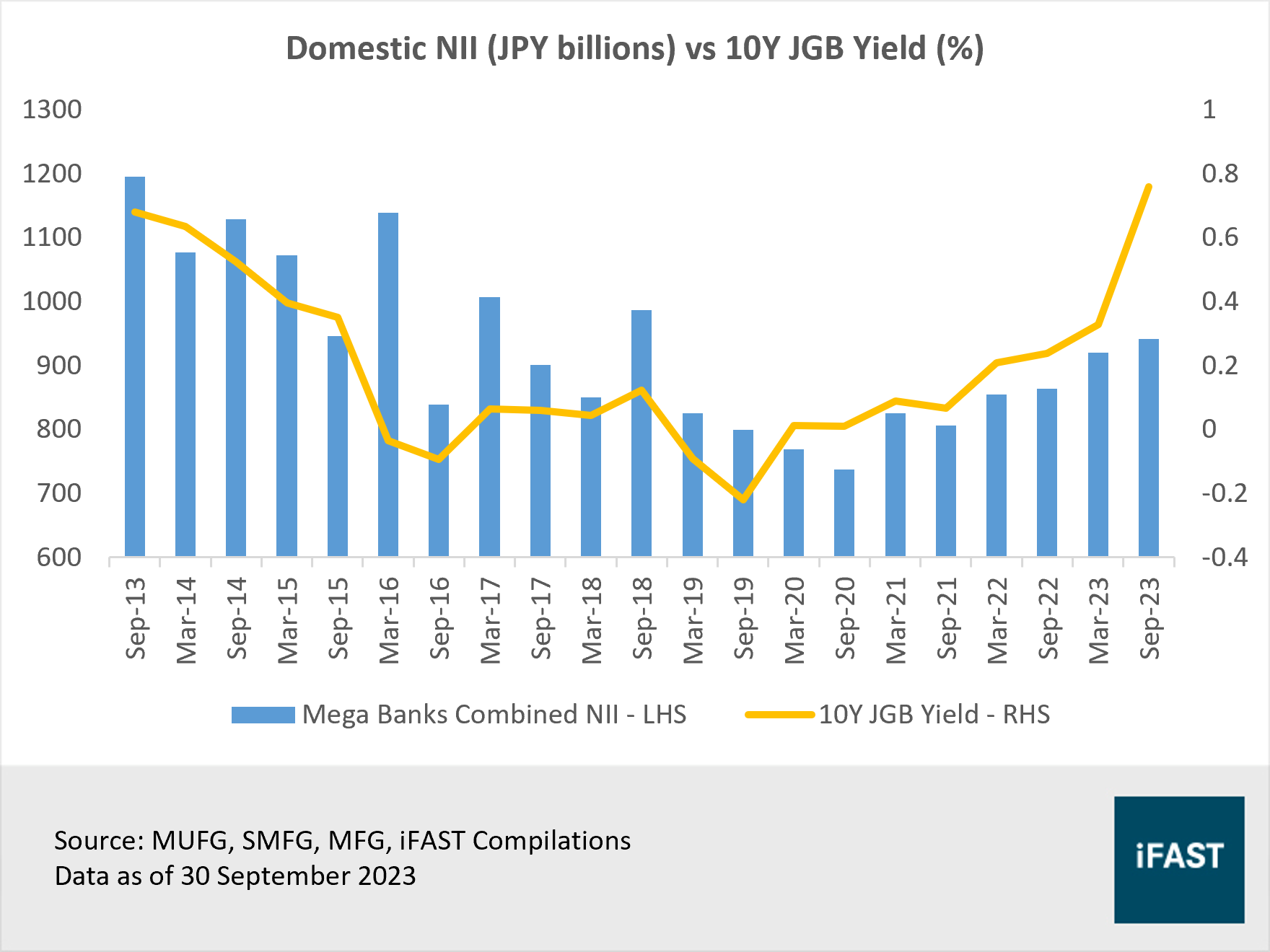

As JGB yields gradually rise, the banking sector is expected to experience an improvement in domestic NII as it is presented with an opportunity to earn more on interest-earning assets, such as loans (Figure 2). It is worth noting that Japan has a higher prevalence of floating-rate loans, especially in comparison to the US where fixed-rate loans are more common.

Figure 2: Domestic NII tends to move alongside JGB yield

For example, around 70% of new housing loan contracts in Japan are structured with floating rates. Homebuyers opting for floating-rate loans anticipate lower total repayments, even in the event of a policy rate increase by the BOJ. Zooming in onto the “Big Three” banking giants, 60% of their domestic JPY-denominated loans are floating-rate, with the remainder typically being fixed-rate or charged based on a prime rate.

As the BOJ charts a course toward policy normalisation, we believe the mega banks will stand to reap the lion’s share of benefits. They have large and stable deposit bases and possess greater flexibility to raise lending rates. In contrast, their smaller regional counterparts are reliant on customer segments that are more sensitive to interest rate changes (e.g. small local businesses). Consequently, they may find themselves constrained by the need to maintain their lending rates at rock-bottom levels.

The “Big Three” have also shown that they are ready to embrace higher rates. In November 2023, the trio raised the rates on their five to 10-year deposits. Notably, the 10-year deposit rate was lifted to 0.2% from 0.002%. This marks the first step in breaking free from an era of virtually zero deposit rates. More raises are likely to come as the mega banks strive to keep their deposit rates competitive so that they can extend more loans for a wider margin.

Currently, their NIMs are razor-thin, standing at less than 1%. As JGB yields climb and the yield curve steepens, there is ample room for margin expansion. In other words, deposits, which yielded minimal value in the prolonged low interest rate regime, would emerge into a potential source of profitability for the banking giants.

Based on assumptions, including a 10 basis point increase in short-term rates and the 10-year JGB yield reaching 1%, MUFG and MFG each anticipate a JPY 35 billion boost to their annual NIIs. This represents an increase of approximately 5% from their domestic NIIs in the last 12 months. At the same time, SMFG expects to earn an additional JPY 30 billion, also marking a growth of around 5%.

Non-interest income on track for further growth

While traditional banking activities such as loans constitute a substantial portion of the banking sector’s revenue, let’s not forget about non-interest income. Such fee-based income enables banks to diversify their income stream and contributes to overall financial stability. On average, the “Big Three” have a non-interest income ratio of around 40%, indicating that they generate a substantial portion of their total income from activities outside of interest-earning assets.

Over the last few quarters, their non-interest income recorded steady growth, and has now surpassed pre-pandemic levels (Figure 3). In particular, MUFG’s fees and commissions reached a historical high on the back of business expansion and cross-selling.

Figure 3: Non-interest income has recovered

Moving forward, non-interest income is poised to strengthen as the return to inflation influences investor behaviour. Domestic investors may increasingly explore riskier investments, such as stocks, to protect their asset values. After frustrating investors for decades, stock prices in Japan have recently touched a 34-year high. This roaring comeback of the Japanese stock market provides a compelling incentive for domestic investors to shift towards investments.

The mega banks should experience growth in fee-based income due to greater trading activity and increased demand for investment products. In addition, they could leverage on the revamped Nippon Individual Savings Account (NISA) program, a government-sponsored investment account, to strengthen their market presence. MFG, for instance, aims to acquire more NISA accounts together with online brokerage Rakuten Securities.

The Japanese government is encouraging more people in Japan to start investing to boost household wealth and asset holdings. From January this year, the investment limit of the NISA has been increased, while the period for tax exemptions on profits made from stock transactions is extended from a maximum of 20 years to an indefinite term (Table 1). This presents a new untapped opportunity for banks and their wealth and asset management divisions.

Table 1: Key points of the NISA changes

|

|

Old NISA |

New NISA |

||

|

Types of NISA |

Tsumitate NISA |

General NISA |

Tsumitate Quota |

Growth Quota |

|

Eligible Investments |

Investment funds suitable for long-term accumulation and diversification |

Stocks and investment funds |

Successor to Tsumitate NISA |

Successor to General NISA |

|

Eligible Persons |

Individuals aged 20 or older Junior NISA for individuals under 20 years old |

Individuals aged 18 or older (Junior NISA abolished) |

||

|

Annual Investment Limit |

JPY 400,000 |

JPY 1.2 million |

JPY 1.2 million |

JPY 2.4 million |

|

Total Investment Limit |

JPY 8 million |

JPY 6 million |

JPY 18 million (of which up to JPY 12 million for Growth Quota) |

|

|

Tax-Free Period |

20 years |

5 years |

No limit |

|

|

Source: QUICK, Nikko Asset Management |

||||

It is worth highlighting that cash holdings represent over 50% of Japanese household assets, reflecting a long-standing trend of individuals holding on tightly to their savings in response to deflation. As the shift towards investments gains momentum, some banks could see their deposits decrease faster compared to others. That said, in our view, this is likely to impact smaller regional banks more significantly than the banking giants. The latter tends to boast diversified and stable deposit bases, and are swift in adjusting their deposit rates to maintain competitiveness. This positions them as more resilient in the face of evolving market dynamics.

Key investment risks

Rapid interest rate surges: A sharp spike in interest rates could potentially squeeze the value of JGBs, resulting in unrealised losses on held-to-maturity securities. That said, the risks appear are more manageable for the mega banks compared to their smaller counterparts which have large portfolios of longer-term bonds. The “Big Three” have steadily reduced their JGB holdings over the past decade and maintain durations of less than three years for their JPY bond portfolios. They also boast robust liquidity positions, suggesting minimal pressure to hastily divest the securities to realise losses.

Potential for a re-rating

In a nutshell, we hold the view that Japan’s mega banks are well-positioned for a new phase of growth. The profitability of the “Big Three” is expected to improve due to a confluence of factors such as elevated NII from overseas operations, an uptick in domestic NII stemming from an impending rise in yields and interest rates, and steady growth in non-interest income amidst the shift towards inflation.

This underpins our conviction in the potential for a re-rating of share prices. It is worth noting that as part of their medium-term business plans, the banking giants are committed to enhance return on equity (ROE) and increase shareholder value sustainably.

Using estimated ROE figures ranging between 8% and 9% as well as cost of equity of around 10%, we have assigned fair PB ratios of 0.90X, 0.80X and 0.75X to MUFG, SMFG, and MFG respectively. Based on this, we project an average upside potential of approximately 17% (as of 29 January 2024) for the mega banks.

The ‘Big Three’ have also pledged to progressively increase their dividends in tandem with profit growth. At present, their targeted dividend payout ratios stand at 40%. We believe investors can expect to receive dividend yields of around 4% (before US withholding tax of 30%), adding an extra layer to attractive investment proposition of Japan’s mega banks.

Table 2: Japan mega banks valuations

|

Name |

Fair PB |

Target Price (USD) |

Current Price (USD) |

Upside Potential |

Forward Dividend Yield |

|

Mitsubishi UFJ Financial Group (NYSE:MUFG) |

0.90X |

10.60 |

9.24 |

15% |

3.3% |

|

Sumitomo Mitsui Financial Group (NYSE:SMFG) |

0.80X |

12.40 |

10.19 |

22% |

3.8% |

|

Mizuho Financial Group (NYSE:MFG) |

0.75X |

4.20 |

3.63 |

16% |

4.0% |

|

Mega Banks Average |

17% |

3.7% |

|||

|

Dividends are before US withholding tax of 30% Source: Bloomberg Finance L.P., iFAST Estimates Data as of 29 January 2024 |

|||||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.