- After a challenging performance last year, the Japanese yen (JPY) experienced another sharp selloff against major currencies in 2023. Nonetheless, we believe 2024 will mark a pivotal moment for the JPY.

- The signalling effect of verbal warnings by Japanese officials, even without direct FX intervention, will prove to be helpful in alleviating depreciation pressure.

- Besides, the yield curve control (YCC), designed to combat deflation by maintaining low policy rates and JGB yields, is becoming unsustainable. As wage growth strengthens in 2024, Japan is more likely to be getting out of its 25-year battle with deflation.

- We anticipate additional policy tweaks in 2024, paving the way for potential abandonment of the YCC. As many other central banks have opted to halt interest rate increases, we expect yield differentials to narrow, resulting in an appreciation of the JPY.

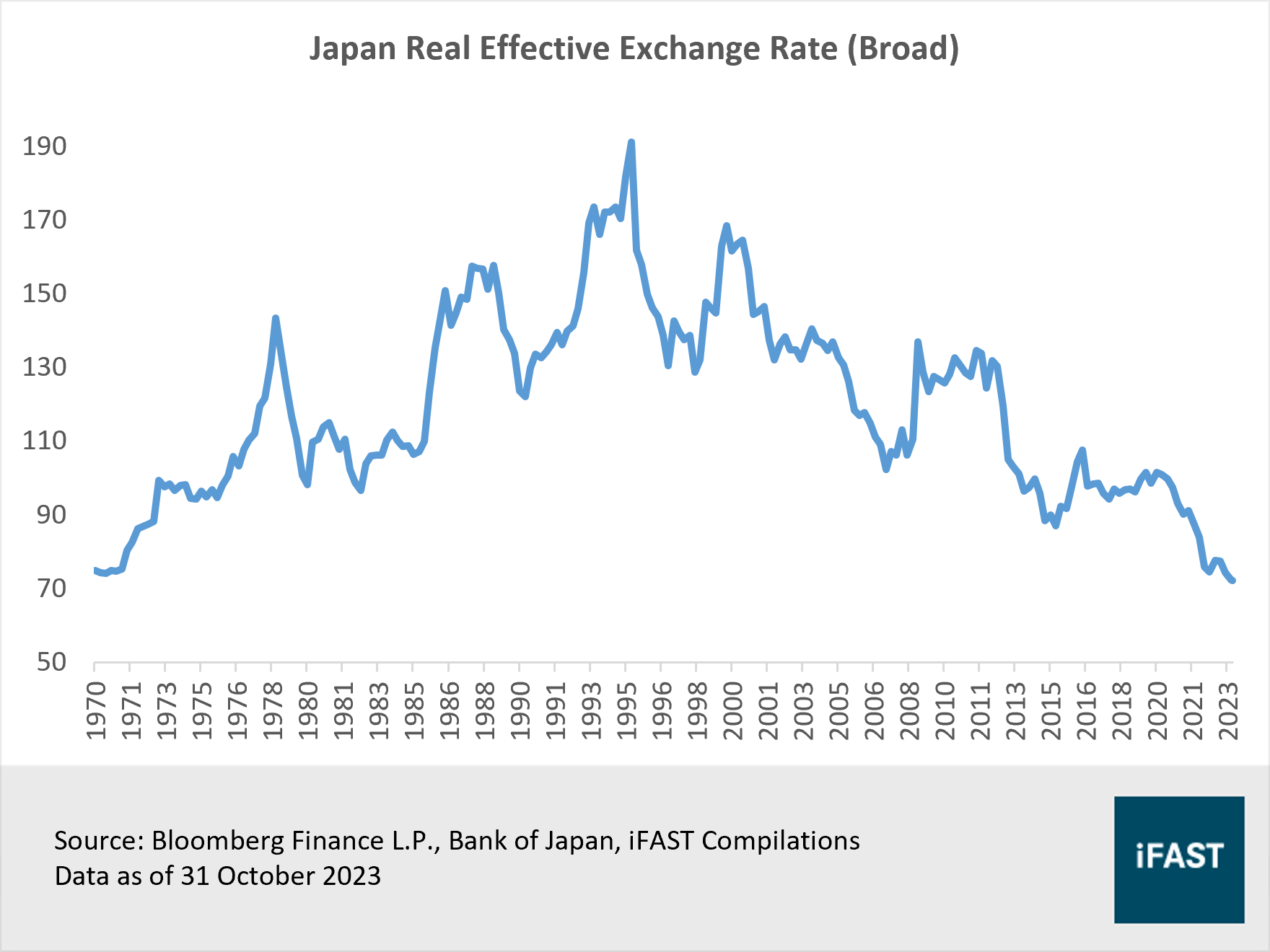

- Our optimism for strong JPY outperformance is also underpinned by the fact that valuations, as gauged by the Japan real effective exchange rate (REER), are at an all-time low since data inception in 1970.

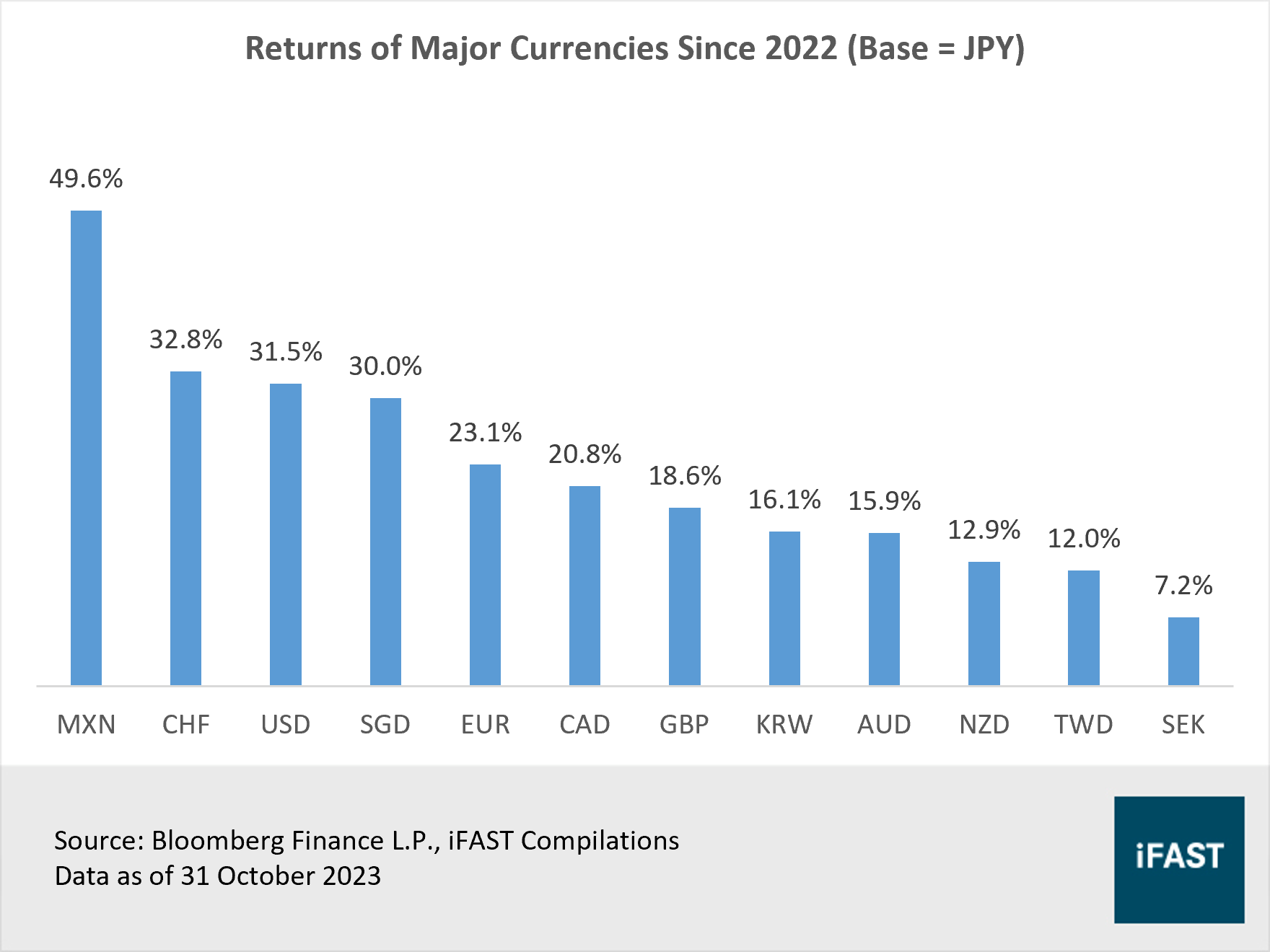

Yen bulls are still waiting. After a challenging performance last year, the Japanese yen (JPY) had experienced another sharp selloff against major currencies (Figure 1). Meanwhile, the USD/JPY surpassed 150, raising the risk of Japan stepping into the foreign exchange (FX) market to combat JPY weakness.

Figure 1: The JPY has depreciated substantially against major currencies

The weakness in the JPY can be attributed to the fact that the Bank of Japan (BOJ) has yet to give up on its ultra-loose monetary policy. Instead, the central bank opted for policy tweaks, underwhelming markets that anticipated more substantial adjustments amidst higher inflation in Japan.

Nevertheless, we believe the wait for yen bulls is about to pay off in 2024. The JPY is at a turning point, driven by potential FX intervention, an impending policy shift against high inflation, and cheap valuations.

Potential FX intervention to limit JPY downside

Japan’s Ministry of Finance intervened in the currency market in September 2022 to boost the JPY for the first time since 1998. It came after a BOJ decision to maintain its ultra-loose monetary policy while the Fed hiked rates by 75 basis points, causing the JPY to tumble as low as 145 per dollar (USD). Another intervention occurred in October 2022 when the JPY plunged to a 32-year low of 151.94.

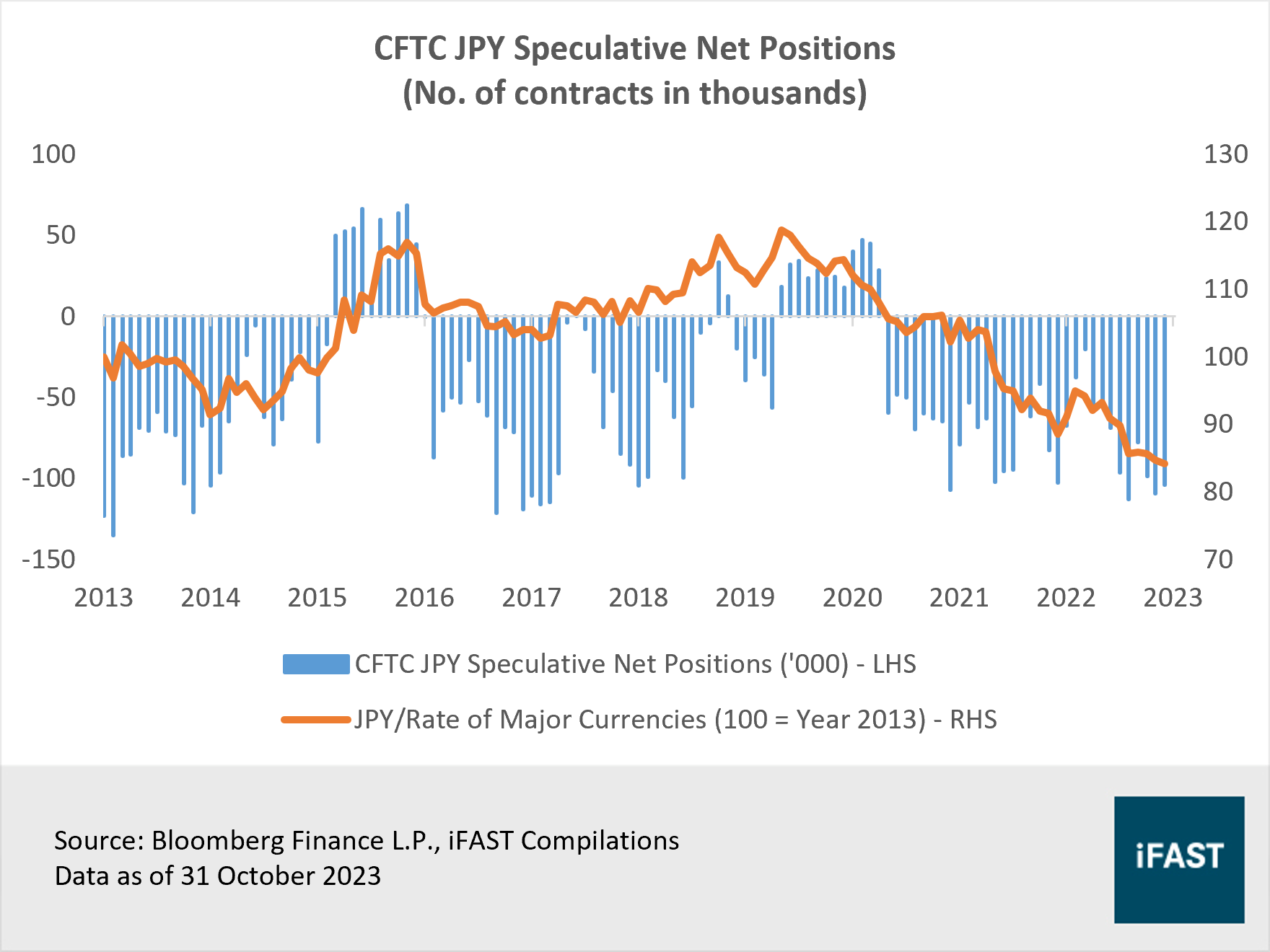

Despite multiple interventions last year, the JPY weakness persisted as the Fed hiked rates, prompting authorities to issue repeated verbal warnings against selling the currency. Even if direct FX intervention is not implemented, this signalling effect would prove to be helpful in alleviating depreciation pressure. According to latest Commodity Futures Trading Commission (CFTC) data, the speculative short exposure on the JPY remains large (Figure 2). The warnings create an incentive for traders to cover their short positions on the JPY as the risk-reward turns less favourable.

Figure 2: There are large speculative short positions on the JPY

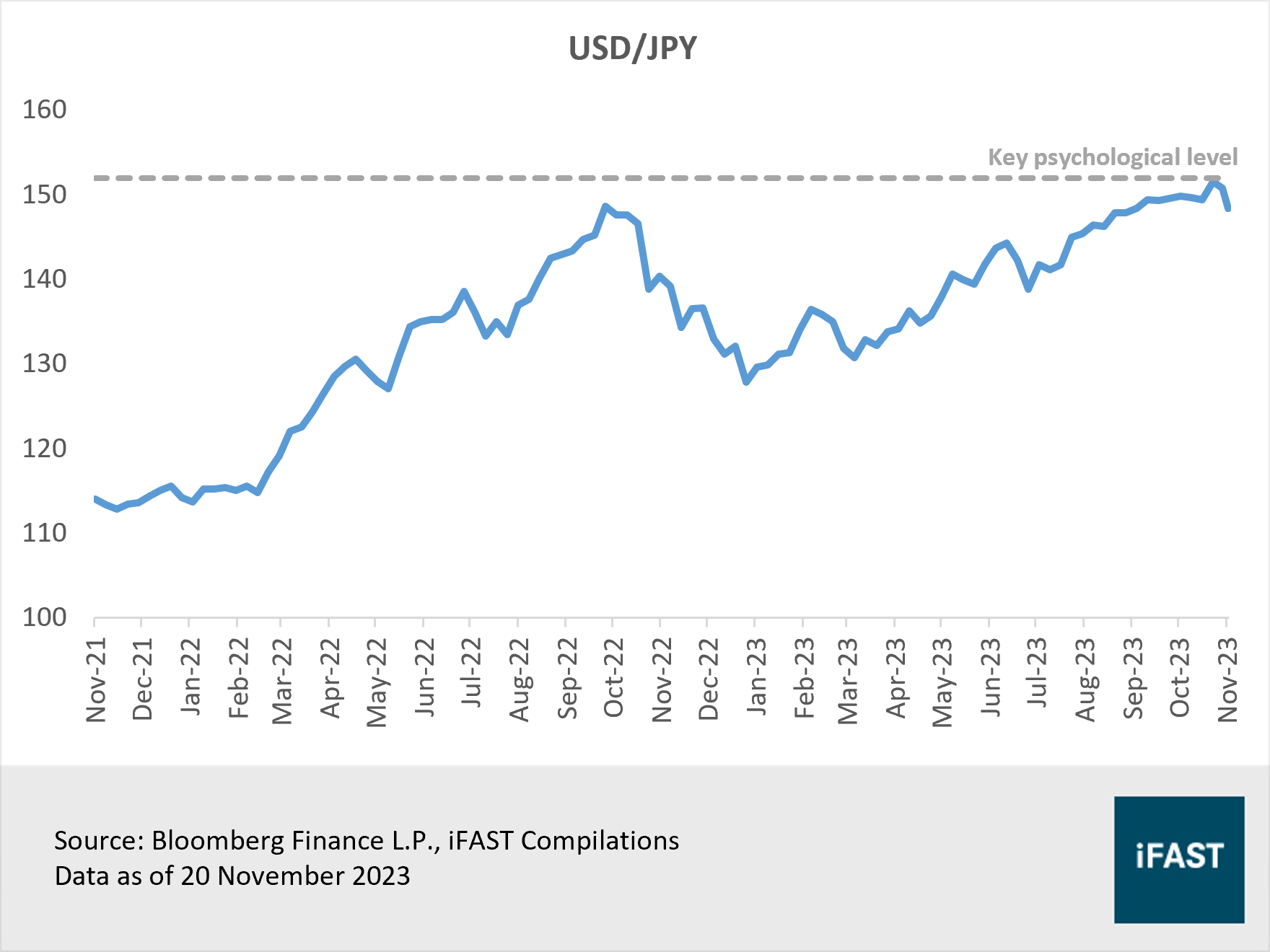

Moreover, the verbal warnings indicate the existence of an intervention zone for USD/JPY, with the key psychological level currently at 152. This implies that the JPY is unlikely to depreciate beyond 152 in the near term, as it will risk an intervention from Japanese authorities.

Figure 3: USD/JPY has stayed below 152

YCC is not sustainable as inflation stays elevated

While the downside risks for the JPY may be limited in the near term, the elephant in the room has been the divergent monetary policy between the BOJ and global central banks. The BOJ is the only major central bank that has refrained from raising interest rates in the current cycle.

It merely increased the target band for 10-year Japanese government bond (JGB) yield from 0.5% to 1.0% and later stipulated that the 1.0% is not a hard limit but a reference point. The central bank also moved away from its daily fixed-rate operations, the primary tool for capping yields using an unlimited purchase of government debt.

The yield curve control (YCC), designed to fight deflation by artificially keeping policy rates and JGB yields at very low levels, is becoming increasingly unsustainable. Today, inflation in Japan is getting stickier. The BOJ’s preferred measures of inflation, core CPI (excluding fresh food prices) and core-core CPI (excluding fresh food and energy prices), both exceeded consensus estimates in September, remaining elevated at 2.8% and 4.2% respectively. In addition, Tokyo CPI (core and core-core), a leading indicator for Japan’s overall inflation, saw an uptick in October due to an acceleration in services prices.

Figure 4: Inflation is getting stickier

Service prices tend to reflect domestic wage trends. Major companies agreed to average pay hikes of 3.58% this year, marking the highest increase in three decades. Wage growth is anticipated to accelerate further. Japan’s largest labour organisation Rengo plans to request a total pay hike of over 5% during the spring 2024 negotiations. At the same time, the largest industrial union, UA Zensen, is aiming for a 6% wage increase. With strengthening wage growth, we believe Japan is set for a new dawn, with the country likely to get out of its 25-year battle with deflation – the very reason why the YCC was initially implemented.

Higher JGB yields to drive JPY strength as other central banks pause rate hikes

Furthermore, in the recent policy meeting that ended on 31 October 2023, the BOJ significantly raised its price forecasts to project that inflation will well exceed its 2% target this year and the next. That said, it kept its initial forecast of inflation dropping back below 2% in 2025. On a positive note, we reckon central bank officials will be paying close attention to the wage negotiations in 2024, where robust data would strengthen the BOJ’s confidence that inflationary pressures are sustainable in the longer term.

It is also worth highlighting that after the policy meeting, the BOJ signalled a gradual move towards ending the YCC. BOJ Governor Ueda acknowledged for the first time that the probability of achieving the long-term inflation target is rising gradually.

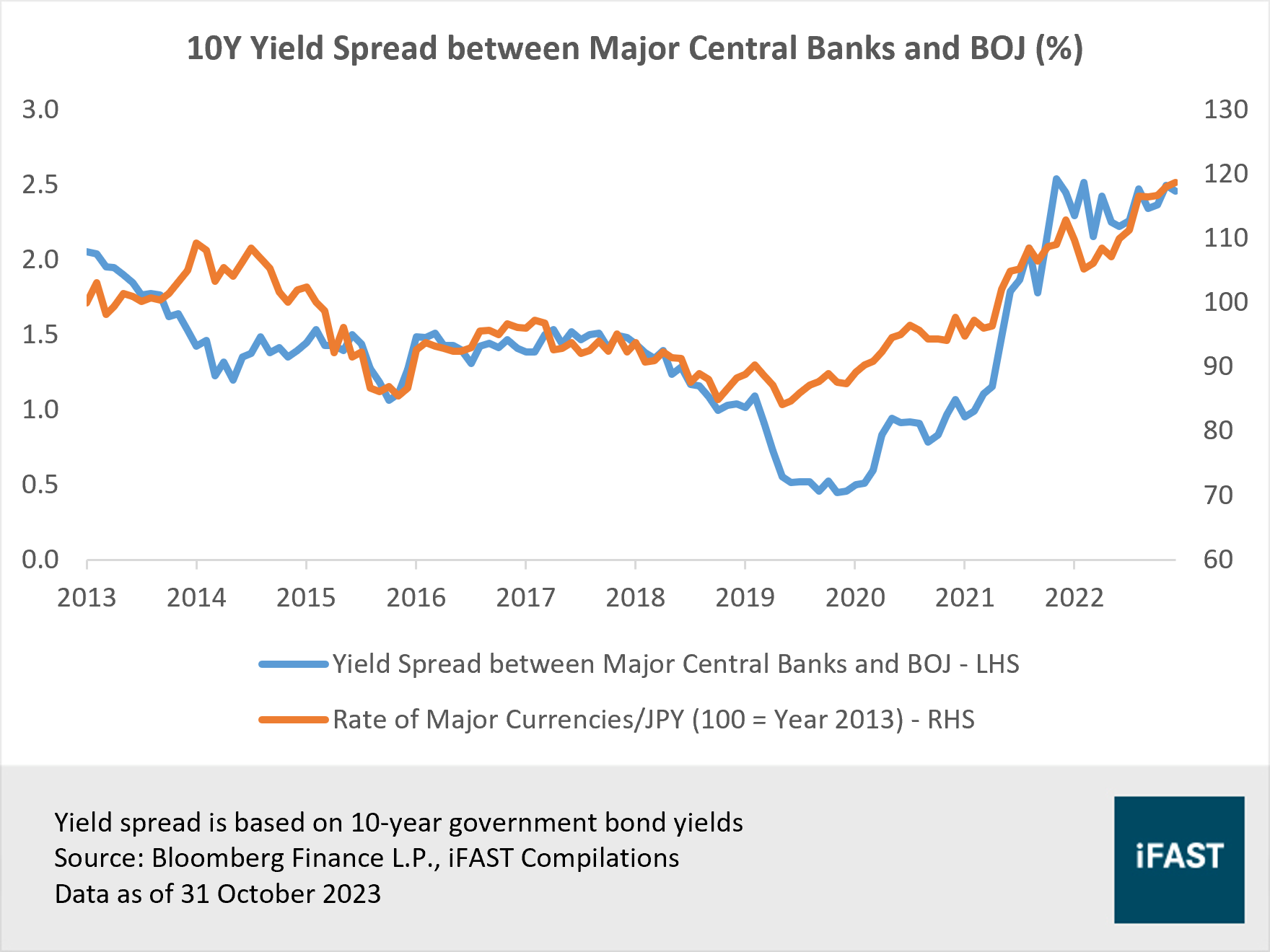

In our view, the BOJ is aiming for an orderly exit from its ultra-easy monetary stance, especially when considering the country’s high debt levels. This suggests the possibility of additional policy tweaks during future policy meetings in 2024 to pave the way for the potential abandonment of the YCC. As such, we see more room for JGB yields to adjust upwards. As many other central banks have opted to halt interest rate increases, this divergence is poised to narrow the yield differential between the BOJ and foreign central banks, resulting in an appreciation of the JPY (Figure 5).

Figure 5: The spread between major central banks and BOJ has widen

In particular, we anticipate a steadier JPY outperformance against major currencies like those in Latin America, the euro (EUR), and the British pound sterling (GBP). For example, the easing inflationary pressures in Mexico may prompt the Bank of Mexico to consider a gradual reduction in its key interest rates. Meanwhile, sluggish growth in Europe limits the capacity of the European Central Bank and the Bank of England to sustain interest rate hikes. Beyond that, we are also expecting a solid outperformance against the Chinese yuan (CNY) in view of the domestic headwinds in China that may require more monetary easing.

Yen is at its weakness level in over 50 years

Our optimism for strong JPY outperformance is also underpinned by the fact that JPY weakness has hit an extreme level. The Japan real effective exchange rate (REER) is at an all-time low since data inception in 1970. REER represents the value of a currency against a weighted average of its peers adjusted by consumer prices.

Figure 6: The JPY is at its cheapest level since 1970

We believe yen bulls eagerly awaiting a turnaround would not be left disappointed again in 2024. This time is likely to be different. In the near term, the downside to JPY is likely to be restricted by repeated verbal warnings by Japanese officials, even without direct FX intervention. Besides, what will truly be a game changer is the narrowing of yield differentials driven by additional policy tweaks (and a potential shift) in 2024 in response to a new era of sustained inflation, while other central banks pause or end their rate hikes. Our conviction is further underpinned by the BOJ’s message that the probability of achieving the long-term inflation target is rising.

We believe that an appreciation in the JPY is unlikely to hurt Japanese equities as it would enhance their attractiveness to foreign investors. Furthermore, we note that extreme weakness in the currency as witnessed today can be undesirable when it amplifies macro headwinds like trade deficits and import costs, which could in turn weigh on Japanese corporates. We also hold the view that the investment case for Japan is well-supported by corporate governance reforms and Japan’s resurgence as a semiconductor powerhouse.

Therefore, we remain optimistic on the outlook of Japanese equities and prefer an unhedged share class to maintain exposure to the JPY. Our recommended products to gain access to Japan’s equity market are the Eastspring Investments - Japan Dynamic AS SGD and the iShares MSCI Japan ETF (NYSE:EWJ). In particular, the Eastspring Investments - Japan Dynamic AS SGD is well-positioned to benefit from higher JGB yields due to its value-oriented strategy.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.