• TSMC delivered another record-breaking year in 2022, with revenue rising by 33% and earnings by nearly 60%. However, 4Q22 results showed that demand has been falling quicker than expected.

• Expect negative earnings growth in 2023 due to the ongoing semiconductor down-cycle and higher expenses associated with overseas fab expansion and the ramp up of N3.

• Long-term outlook of the chip sector remains bright, driven by (i) an increase in the number of semiconductor applications, and (ii) the increase in silicon content within them.

• TSMC’s technology leadership and strong balance sheet should not only help it to navigate this downturn with ease, but also enable the company to emerge stronger than before.

• Based on a revised fair PE ratio of 22X and 2025 EPS estimates, our target price for TSMC is USD 143. This represents an upside potential of approximately 55%.

TSMC has delivered another record-breaking year yet again

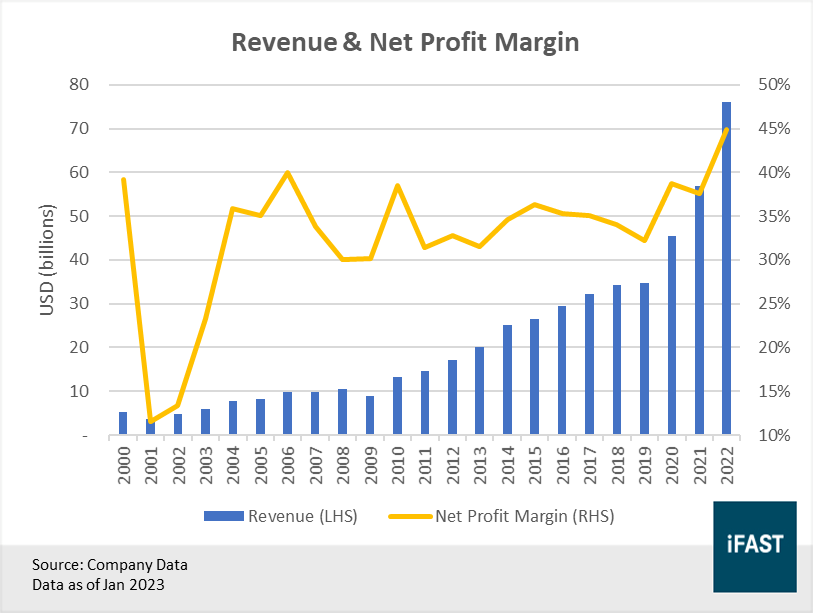

Taiwan’s chip darling has had another year for the books. TSMC (NYSE:TSM), the world’s largest chipmaker, grew its revenue to a new record high of USD 75.9 billion in 2022, eclipsing the previous year’s record of USD 56.8 billion. This equates to a year-on-year increase of more than 33%, one of the best growth rates achieved in the company’s illustrious history. Earnings were not too shabby either, rising by 59% year-on-year backed by strong net profit margins (Figure 1).

Figure 1: TSMC grew its revenue by more than 33% in 2022, surpassing the previous record high

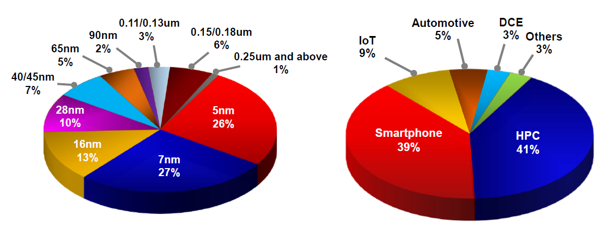

As usual, the bulk of TSMC’s revenue (53%) is derived from advanced technologies, which the company defines as 7nm and below. This should not come as a surprise because Taiwan as a whole is estimated to produce over 60% of the world’s semiconductors, including more than 90% of the most cutting-edge chips. Of the various nodes, 7nm contributed 27% of wafer revenue, while 5nm made up 26%. In terms of platforms, Smartphone and High Performance Computing (HPC) combined to make up more than 80% of TSMC’s wafer revenue (Figure 2).

Figure 2: Breakdown of TSMC’s revenue by process node and platform

Source: Company Data

Data as of Jan 2023

Throughout 2022, all six platforms achieved positive growth, led by Automotive which grew by a staggering 74%. Nearly three years after automakers first complained about having to cut production due to a shortage of chips, the supply of auto chips still remains constrained even to this day. Bank of America estimates that the market for automotive chips is still 10% undersupplied today compared to 20% last year. High demand and low supply have led to higher prices, which explains the sizeable revenue growth for this platform.

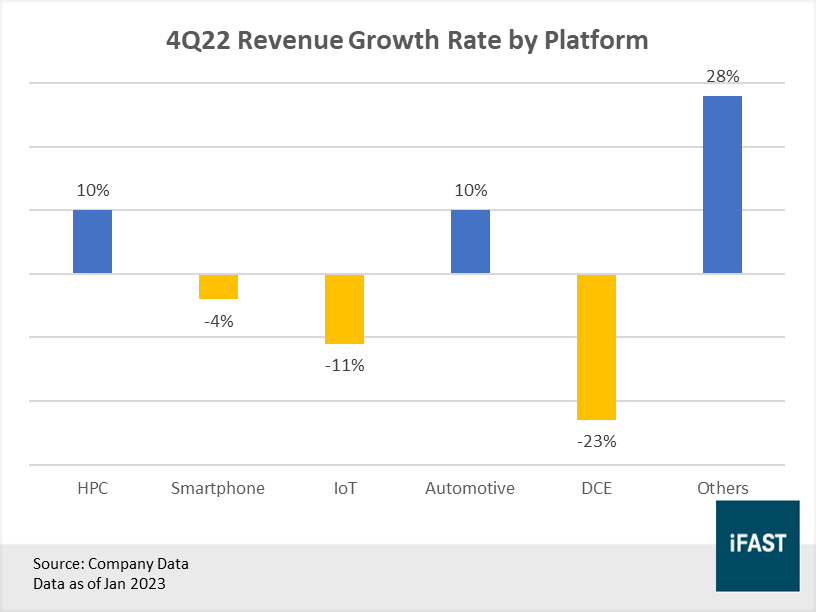

Revenue from HPC rose 59% last year, powered by heavy demand from enterprise-driven end market segments, such as data centres. Meanwhile, Smartphone and Internet-of-Things (IoT) revenue grew 28% and 47% respectively. While the full-year numbers certainly look fantastic, a closer look at the fourth quarter numbers paint an entirely different picture (Figure 3) – one that shows demand is softening quickly, particularly in consumer-related platforms, such as Smartphone, IoT, and Digital Consumer Electronics (DCE).

Figure 3: Revenue for Smartphone, IoT, and DCE platforms have fallen in the fourth quarter

Lower revenue and higher expenses to weigh on TSMC’s earnings

As early as January last year, we have cautioned investors on multiple occasions that the strong post-pandemic recovery experienced by chipmakers is not sustainable, and it was just a matter of time before a downturn takes place.

That officially arrived in the fourth quarter of 2022.

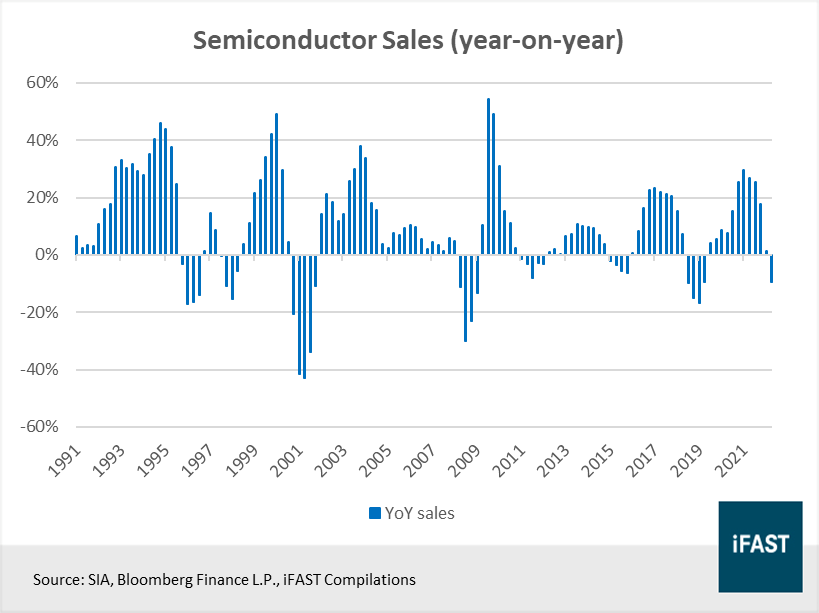

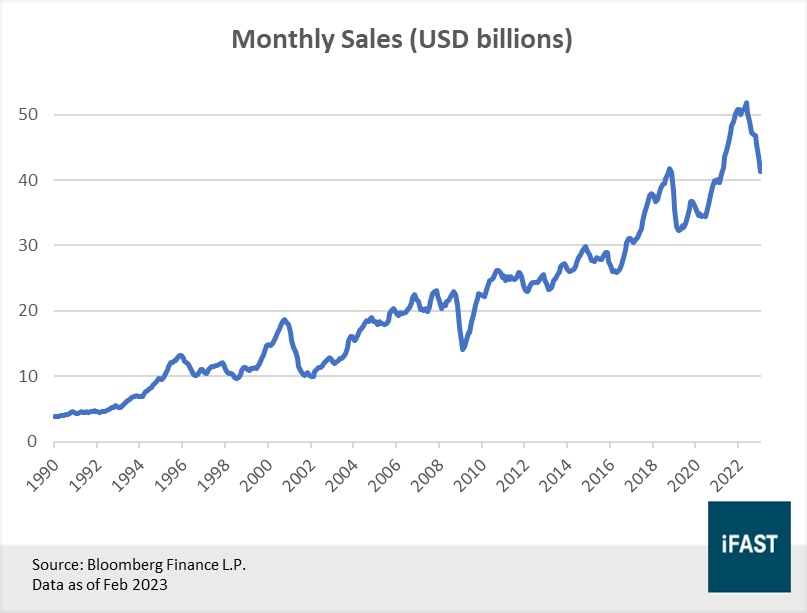

For the first time since late 2019, semiconductor sales growth has fallen back into negative territory, coming in at -9.4% year-on-year in the final quarter of 2022 (Figure 4). While the drop in sales is significant, things will likely worsen over the coming quarters as the down-cycle plays out.

Figure 4: Semiconductor sales fell by nearly -10% in the final quarter of 2022

The sharp fall in sales comes as high inflation and rising interest rates are starting to take a toll on consumers and businesses alike, forcing them to tighten their belts. Furthermore, as most economies are now more or less fully reopened, consumer spending has also shifted away from goods (e.g. consumer electronics) and towards services such as travel and leisure, thus lowering the demand for semiconductors.

In the latest earnings call, the management of TSMC noted that they continue to observe softness in the consumer end-market segment, while enterprise-driven end-market segments (e.g. data centres), which were initially more resilient, have softened as well. Capacity utilisation rates have also fallen to much lower levels than previously anticipated, particularly for N7 and N6.

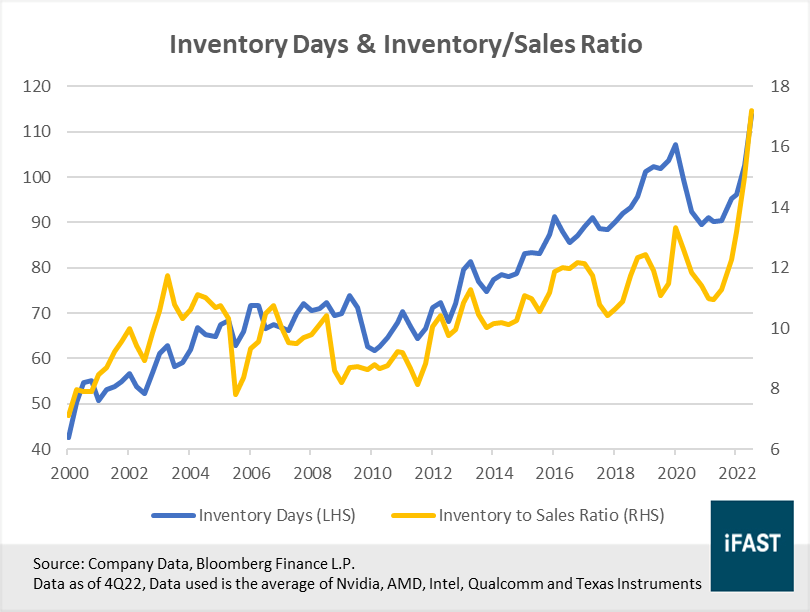

Inventory channels are bloated, likely because customers double-ordered during the shortage. Taking a quick look at the numbers for the top five chipmakers in the US, we can see that both inventory days (the average number of days it takes to sell off inventory) and the inventory-to-sales ratio are rising. Both measures indicate that turnover is slowing (Figure 5).

Figure 5: Inventories are rising among semiconductor companies

Looking forward, with the pandemic boom now behind us and a global recession looming, demand for semiconductors will likely weaken further as customers continue to adjust their inventories. According to the guidance set out by TSMC’s management, 1Q23 revenue is expected to be about -15% lower than the previous quarter.

Aside from the lacklustre revenue guidance, operating margins are also expected to see a significant drop from the current level of 52% to 42% in 1Q23 due to lower capacity utilisation rates and higher expenses associated with overseas fab expansion. Right now, TSMC is in the process of constructing two mega fabs in Arizona, US. When completed, they will produce chips using 4nm and 3nm process technologies. Both fabs are expected to be up and running by 2026.

Even with generous government subsidies, such as the CHIPS Act, TSMC estimates that its total investment in Arizona could be as much as USD 40 billion, which is roughly equivalent to four to five times the cost of a similar fab in Taiwan. The reasons for this huge cost gap is largely due to the higher cost of construction, such as labour, permits, raw materials, and more. After completion, TSMC will also have to hire more expensive skilled labour (relative to Taiwan) to operate the fab, which adds to its total expenses.

All in all, given the higher initial and ongoing costs associated with the overseas expansion and the ramp up of 3nm production, TSMC should see lower margins and weaker earnings growth for the time being.

Down-cycles are temporary, long-term outlook remains bright

As we have mentioned countless times before, semiconductors are the bedrock of all modern technology. While the current downturn might last a few more quarters as supply and demand readjust, we firmly believe that semiconductor sales will recover to higher levels than before, driven by (i) an increase in the number of applications, and (ii) the increase in silicon content in them.

Figure 6: Semiconductor sales have always bounced back to higher levels than before post downturn

Technology leadership and healthy balance sheet adds to resilience

Even though TSMC is not immune to the down-cycle, it is probably in the best position to recover from it. Here are a few reasons why.

First of all, due to its dedication to continuously improve its technology offerings, TSMC has effectively cemented its status as the number one go-to foundry for customers looking to get their hands on leading-edge chips. It is little wonder that both the US and China covet its unmatched ability to make advanced chips.

In the fourth quarter of last year, TSMC’s 3nm node entered volume production. N3 is another full node stride from N5, and it is currently the most advanced node TSMC offers. It promises up to 70% logic density gain, up to 15% speed improvement at the same power, and up to 30% power reduction at the same speed as compared to N5.

Even in current conditions where global economic growth is slowing, there has been considerable interest in N3 and the management expects its capacity to be fully utilised this year. Across TSMC’s diverse client base, it is rumored that Apple (TSMC’s largest customer) has snapped up all the available supply of N3, which will presumably be used to manufacture chips that will go into Apple’s new line of products, such as the iPhone 15 Pro. Aside from Apple, other clients, such as Nvidia and AMD, are also expected to adopt N3 soon. TSMC expects to see a meaningful contribution from N3 starting from the second half of the year, and the pickup in N3 demand to drive an earnings rebound in 2024.

Next, TSMC has one of the healthiest balance sheets across the entire sector with a net cash position, which raises the odds that it will make it through this downturn with ease (Table 1).

Table 1: TSMC has one of the healthiest balance sheets among its peers

|

Company |

Next Debt to Equity Ratio |

|

TSMC |

-22.6% |

|

Samsung |

-29.6% |

|

Intel |

7.9% |

|

UMC |

-37.3% |

|

SMIC |

4.8% |

|

Global Foundries |

-8.3% |

|

Source: Bloomberg Finance L.P. Data as of 4 Apr 2023 |

|

Lastly, unlike other chipmakers, such as Intel and Micron, which have announced mass layoffs and salary cuts, TSMC did the exact opposite, announcing plans to recruit more than 6,000 new engineers (equivalent to approximately 10% of its current headcount) this year as part of its long-term expansion plan. This goes to show the level of confidence the company has with regards to its future prospects.

Key investment risk

Geopolitical risks: Sandwiched between the US and China, geopolitical risk is by far the greatest risk TSMC faces. The fact that both countries are fighting hard over semiconductor technology only serves to make matters worse. Right now, the US prohibits the sale of advanced semiconductors to China, if they are made with the help of US technology – this includes chips produced by TSMC.

While the chances of an armed conflict between China and Taiwan are low at this point, it is no longer a remote possibility. China may also retaliate by imposing a blockade on Taiwan, which would be detrimental to its economy and TSMC.

Related Article: Downgrade Taiwan to 3.5 Stars: Macroeconomic headwinds mount but valuations still appealing

55% upside potential even in a recession

As for valuations, we have lowered the fair PE multiple for TSMC from 24X to 22X in order to factor in the greater geopolitical risk. Next, we have also made some downward adjustments to earnings estimates to account for the down-cycle in the chip industry. Even though earnings growth will likely be negative this year due to the weakening outlook, we would like to remind investors that times like these will not last forever. Earnings growth will definitely pick up once the down-cycle is over.

Trading at just 14.2X 2025 estimated EPS versus our fair PE multiple of 22X, TSMC’s shares has an upside potential of approximately 55%. This implies a target price of USD 143.

Table 2: Earnings growth expected to recover in 2024

|

TSMC |

2022 |

2023E |

2024E |

2025E |

|

Earnings Per ADR (USD) |

6.60 |

5.28 |

5.91 |

6.50 |

|

Earnings Growth YoY |

61.0% |

-20.0% |

12.0% |

10.0% |

|

PE Ratio (X) |

11.29 |

17.46 |

15.59 |

14.17 |

|

Upside Potential (based on fair PE Ratio of 22.0X) |

- |

- |

- |

55.27% |

|

Source: Bloomberg Finance L.P., iFAST Compilations Data as of 4 Apr 2023 |

||||

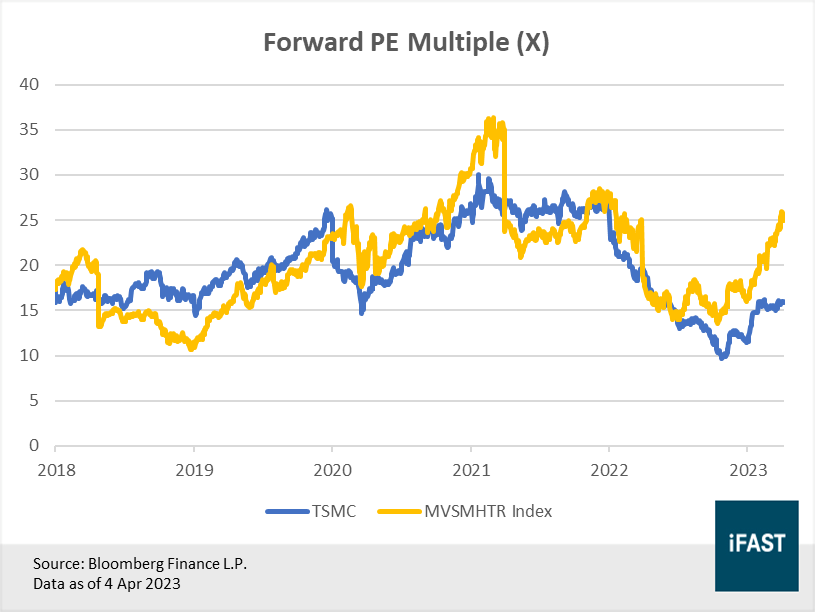

When compared to the broader US semiconductor index, we can also clearly see that TSMC is trading at a significant discount, making it one of the more attractive semiconductor stocks on a relative basis. (Figure 7).

Figure 7: TSMC is relatively undervalued vs the rest of the semiconductor industry

Although there is a good chance that share prices may fall further in the future, current valuations already provide investors with a decent margin of safety. Even if valuations do fall further, it’s an opportunity to pick up more shares at a discount, which also means the potential upside is greater.

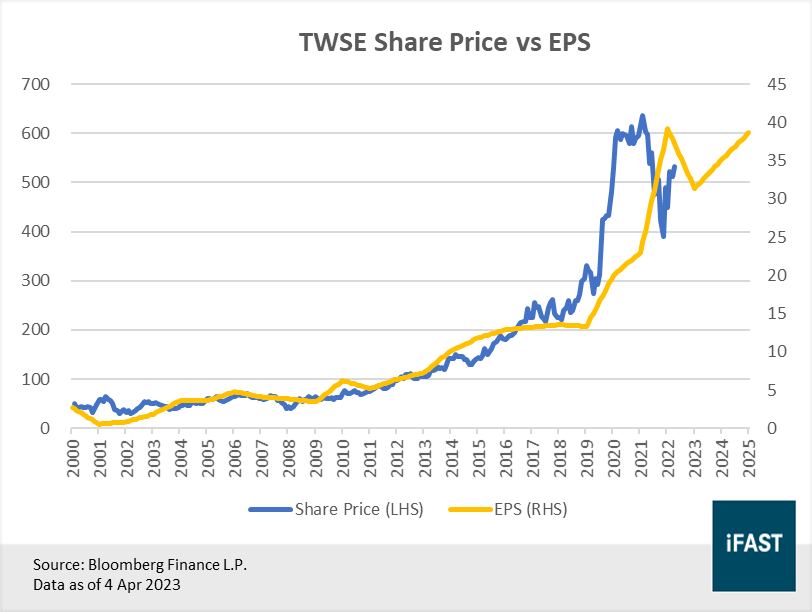

Most importantly, the long-term growth story that underpins the semiconductor industry will only become stronger as the world becomes increasingly tech-driven. And right at the top of sits TSMC, the most important chipmaker in the world.

Figure 8: In the long run, share prices are ultimately driven by earnings.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.