-

NextEra Energy is not your typical utility company. It is one of the largest electric power and energy infrastructure companies in North America and a leader in the renewable energy industry.

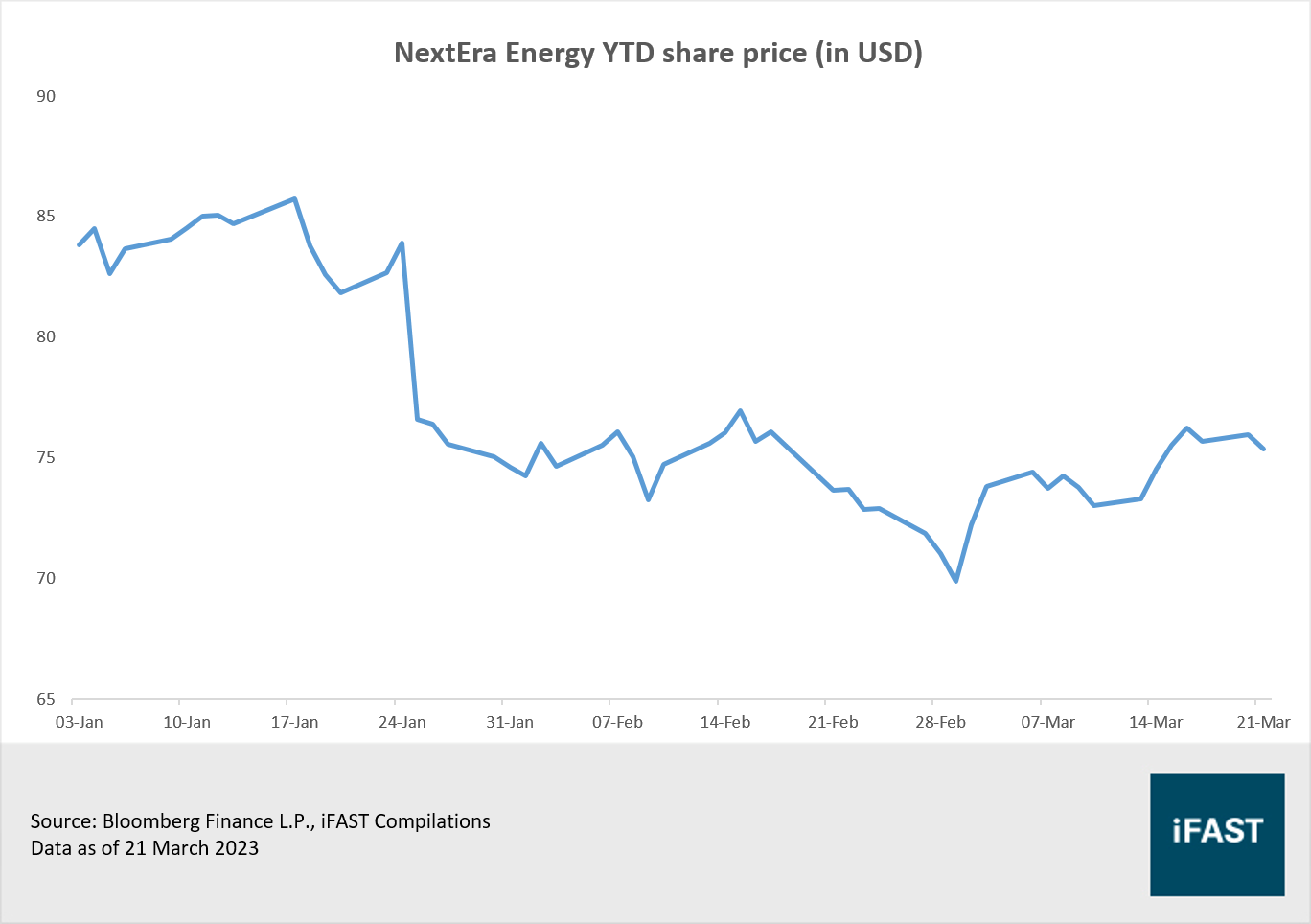

The company has been sold down on news that Florida Power & Light's (FPL) CEO was retiring after 11 years, and that the company is seeking dismissal of a Federal Election Commission complaint alleging the utility violated state and federal campaign law.

The regulatory framework under US and Florida law includes timely cost recovery mechanisms that enable FPL to generate predictable and stable cash flows in spite of inflationary pressures, ensuring earnings resilience.

A big factor driving NextEra Energy forward is the accelerating demand for renewable energy, with the company riding on the back of massive policy support after the passing of the Infrastructure Investment and Jobs Act and the US Inflation Reduction Act.

We have a 2025 target price of USD 94 for NextEra Energy, which translates to an upside potential of 25% based on the last closing price of USD 75.36 on 21 March 2023. Investors can also expect to receive a dividend yield of 2.5% (before withholding tax).

NextEra Energy (NYSE:NEE) is not your typical utility company. It was founded in 1925 as Florida Light and Power, and was purely a traditional fossil fuel powered utility back then. The company had later gone on to expand within the renewables space, and is today the world’s largest producer of wind and solar energy.

In late January, NextEra Energy was sold down on news that Florida Power & Light's CEO, Eric Silagy, was retiring after 11 years, and that the company is seeking dismissal of a Federal Election Commission complaint alleging the utility violated state and federal campaign law. The sharp sell-down on 25 January 2023 resulted in NextEra Energy losing about USD 14.5 billion of its market capitalisation.

We think that the sell-off was overdone, as we do not expect that the allegations of federal campaign finance law violations to be material, given that the contributions referenced in the complaint is less than USD 1.3 million. With the company’s share price yet to meaningfully recover, investors are presented with a good opportunity to pick up the stock.

Figure 1: Share price of NextEra Energy year-to-date

Company Overview

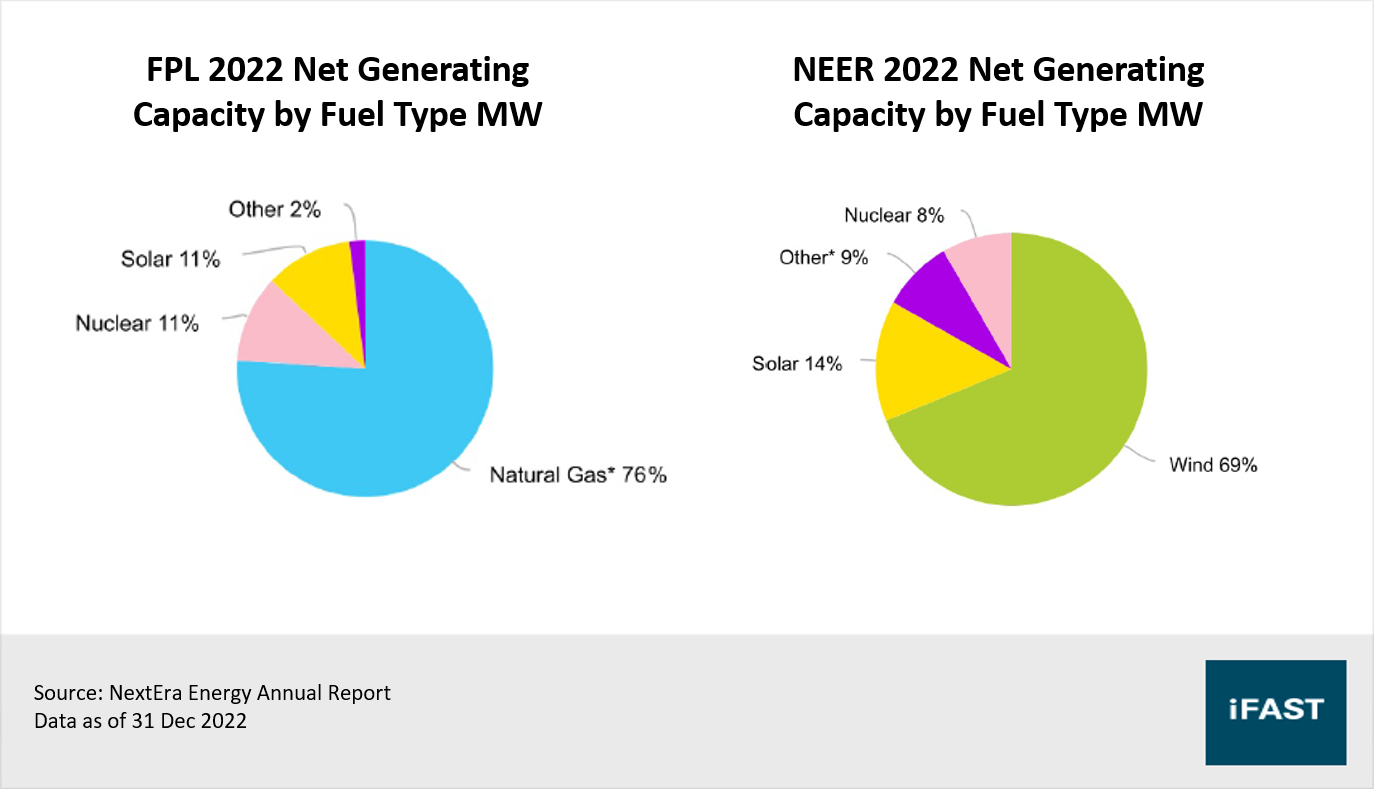

NextEra Energy is one of the largest electric power and energy infrastructure companies in North America and a leader in the renewable energy industry. The company has a split structure as a traditional gas-reliant regulated utility, and a deregulated wholesale provider focused on renewables.

Its two principal businesses, Florida Power

& Light (FPL) and NextEra Energy Resources (NEER) made it a unique player

within the utilities space (Table 1). FPL is the largest electric utility in the state

of Florida, and one of the largest electric utilities in the US. Its large,

mainly residential service territory benefits from economic expansion that

leads to organic sales growth. NEER on the other hand, together

with its affiliates, is the world’s largest generator of wind and solar energy

as well as a world leader in battery storage, with a 20% market share of the US

renewables market.

Table 1: Description of NextEra Energy two principal business

|

Business/Operation |

Description |

|

Florida Power & Light (FPL)

|

|

|

NextEra Energy Resources (NEER)

|

|

|

Source: NextEra Energy 2022 Annual Report Data as of 31 Dec 2022 |

|

Figure 2: FPL and NEER fuel sources for its generation facilities

Looking at NextEra Energy’s FY2022 financial results, the company’s revenue was USD 20.96 billion, which is a 22.8% increase from USD 17.7 billion of revenue in 2021. The company also reported a net income of USD 5.74 billion compared to USD 5.02 billion which is 14.4% year-over year (yoy) increase.

Table 2: Financial highlights of NextEra Energy based on its latest performance

|

In millions of USD except per share |

4Q22 |

4Q21 |

Change |

FY22 |

FY21 |

Change |

|

Revenue

|

6,164 |

5,046 |

22.2% |

20,956 |

17,069 |

22.8% |

|

Net Income

|

1,011 |

814 |

24.2% |

5,742 |

5,021 |

14.4% |

|

Earnings per share

|

0.51 |

0.41 |

24.4% |

2.90 |

2.55 |

13.7% |

|

Source: NextEra Energy, iFAST Compilations. Data as of 31 Dec 2022 |

||||||

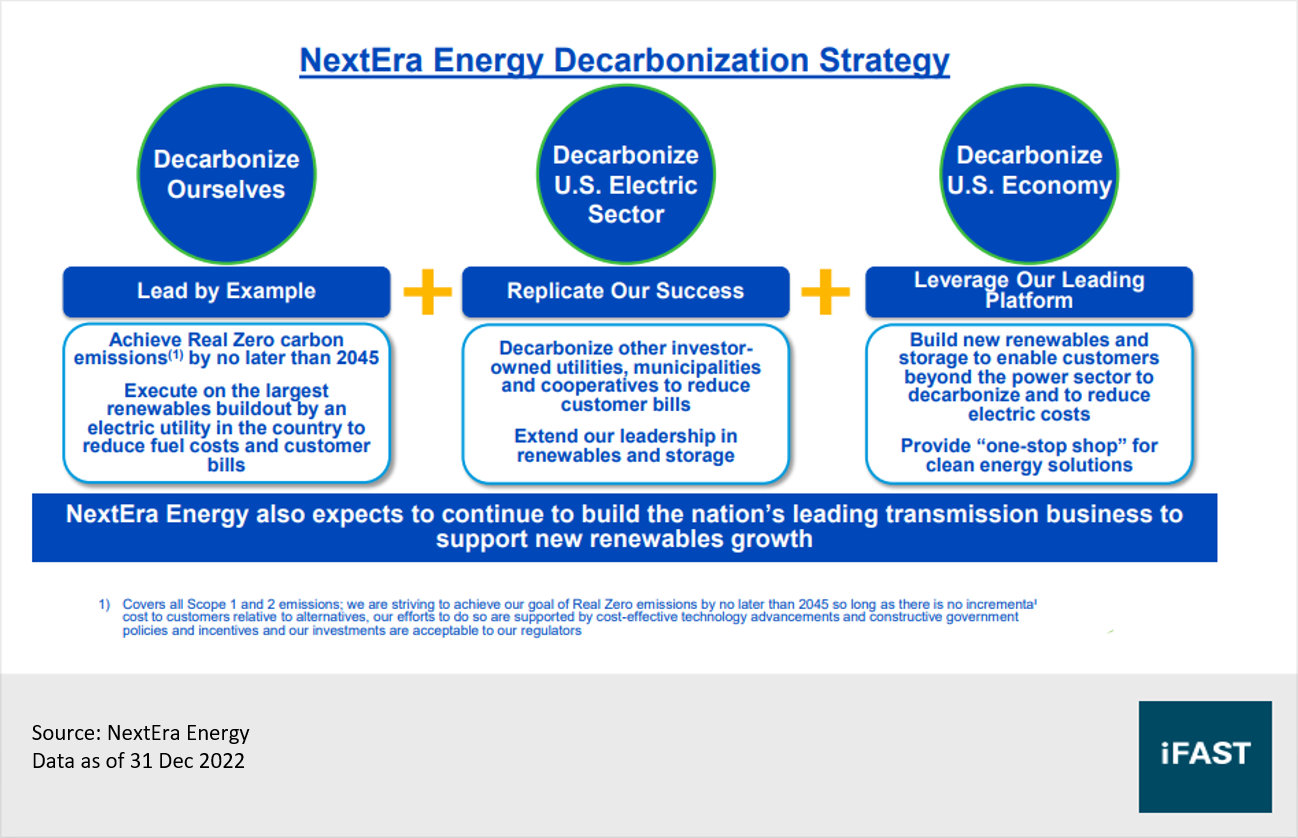

As the first mover in the US utility scale renewable energy development, NextEra Energy continues to enjoy scale advantages over rivals. It even targets to double its solar and wind business from 24 gigawatts (GW) capacity in 2021 to 46-53GW capacity in 2025. Under its “Real Zero” plan, NextEra Energy aims to cut its carbon emissions from 2005 levels by 70% by 2025, 82% by 2030, 87% by 2035 and 94% by 2040 before hitting zero emissions in 2045, without the use of carbon offsets (Figure 3).

Figure 3: Strategy to extend leadership in the US clean energy transition

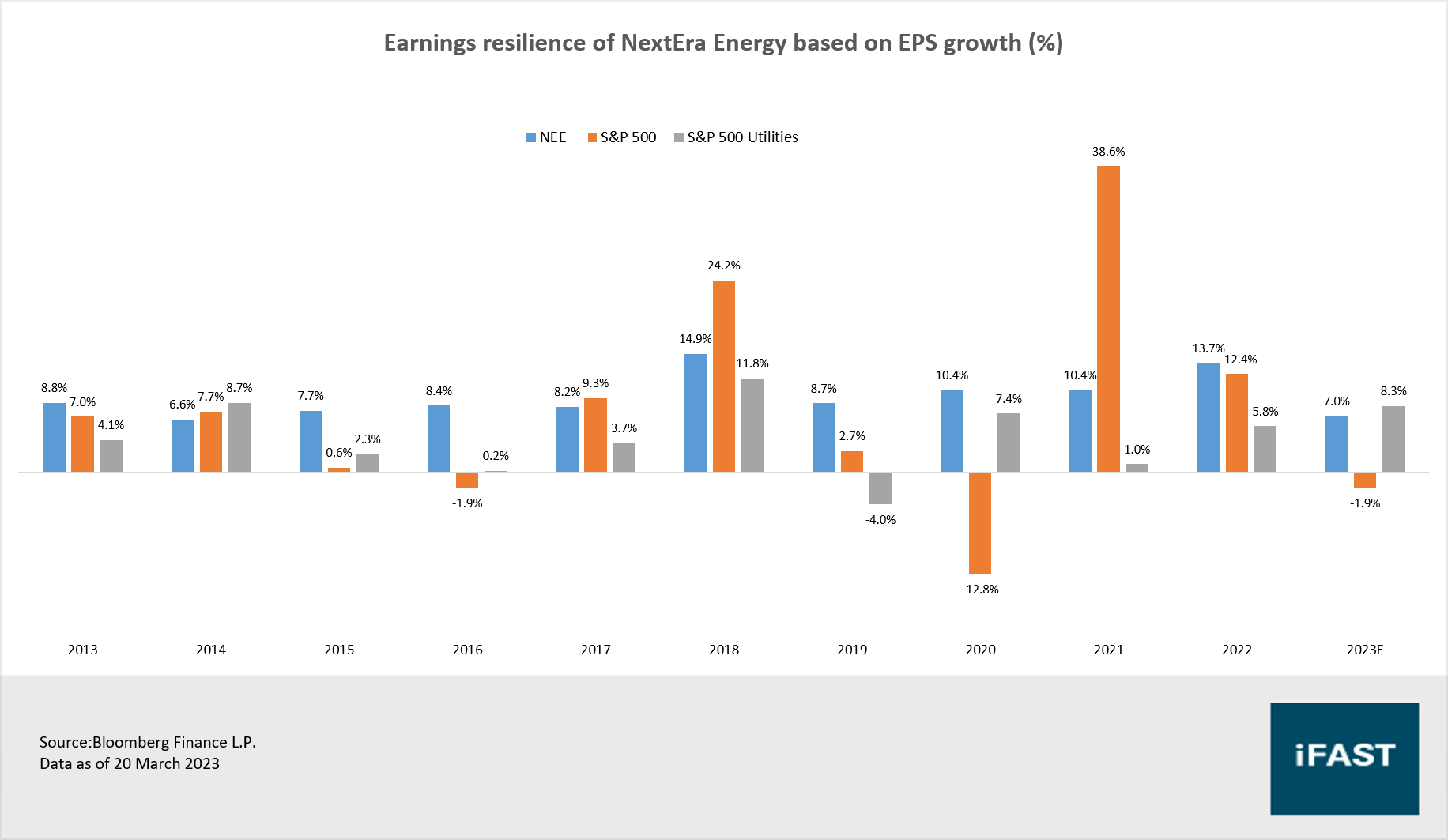

Steady utility business ensures that its earnings and margins remain resilient

NextEra Energy has a resilient business model owing to the fact that they provide an essential, non-discretionary service, which benefits from inelastic demand. Their services continue to be used through periods of economic downturns, enabling them to produce steady cash flows.

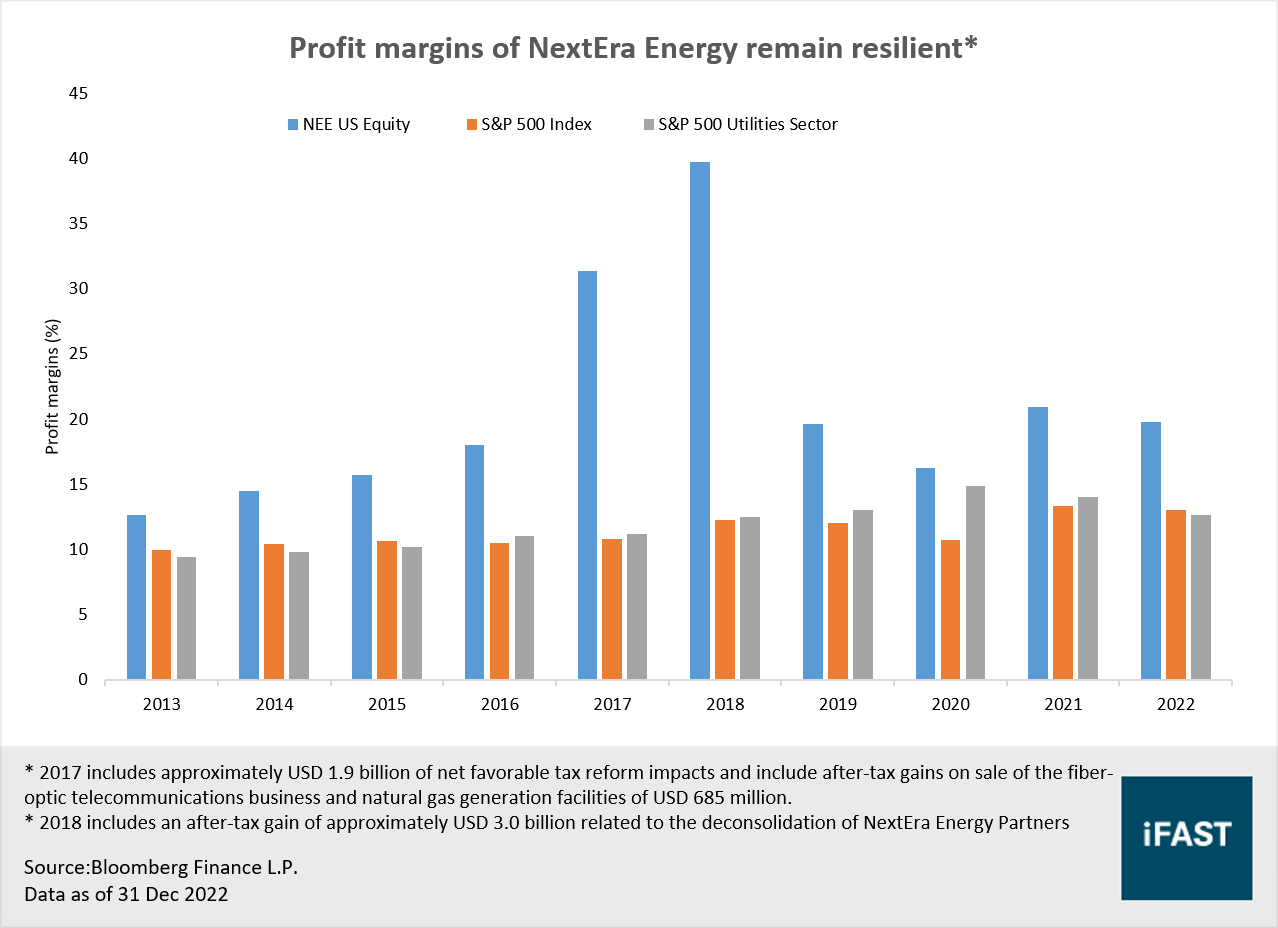

Moreover, in an inflationary environment that we are currently in right now, revenue streams from NextEra Energy can increase along with the general increase in prices, ensuring that its earnings and profit margins are better protected from inflation and are likely to stay resilient ahead (Figure 4 and Figure 5).

Figure 4: NextEra Energy earnings growth has been very resilient over the years

Figure 5: NextEra Energy profit margins have remain resilient and have outpaced the S&P 500

This is because the regulatory framework under US and Florida law includes timely cost recovery mechanisms. FPL operates within these regulated frameworks which enables them to earn an allowed rate of return on money spent maintaining or improving their asset base (or in other words earn a reasonable rate of return for providing this service). For instance, FPL's authorised regulatory ROE is 10.60%, with a range of 9.70% to 11.70%.

Beyond this, FPL's service to its electric retail customers is provided primarily under franchise agreements negotiated with municipalities or counties. During the term of a franchise agreement, which is typically 30 years, the municipality or county agrees not to form its own utility, and FPL has the right to offer electric service to residents. As of 31 December 2022, FPL held 225 franchise agreements with various municipalities and counties in Florida with varying expiration dates through 2052. These franchise agreements cover the vast majority of FPL's retail customer base in Florida.

As such, because of such characteristics mentioned above, the earnings growth of NextEra Energy would likely outpace the S&P 500 moving ahead, especially in the current weakening economic environment. Not to mention, we think that current earnings estimates for the S&P 500, with a slight earnings decline are being overly optimistic given the mounting economic risks.

NextEra Energy is riding on the back of massive policy support

Moreover, there is massive policy support for infrastructure or utility companies such as NextEra Energy. In the US for instance, there is an urgent need to replace and upgrade ageing infrastructure. According to the 2021 report by the American Society of Civil Engineers, much of the local infrastructure in the US has a rating of C to D, meaning it is in urgent need of being replaced or upgraded in the next few decades.

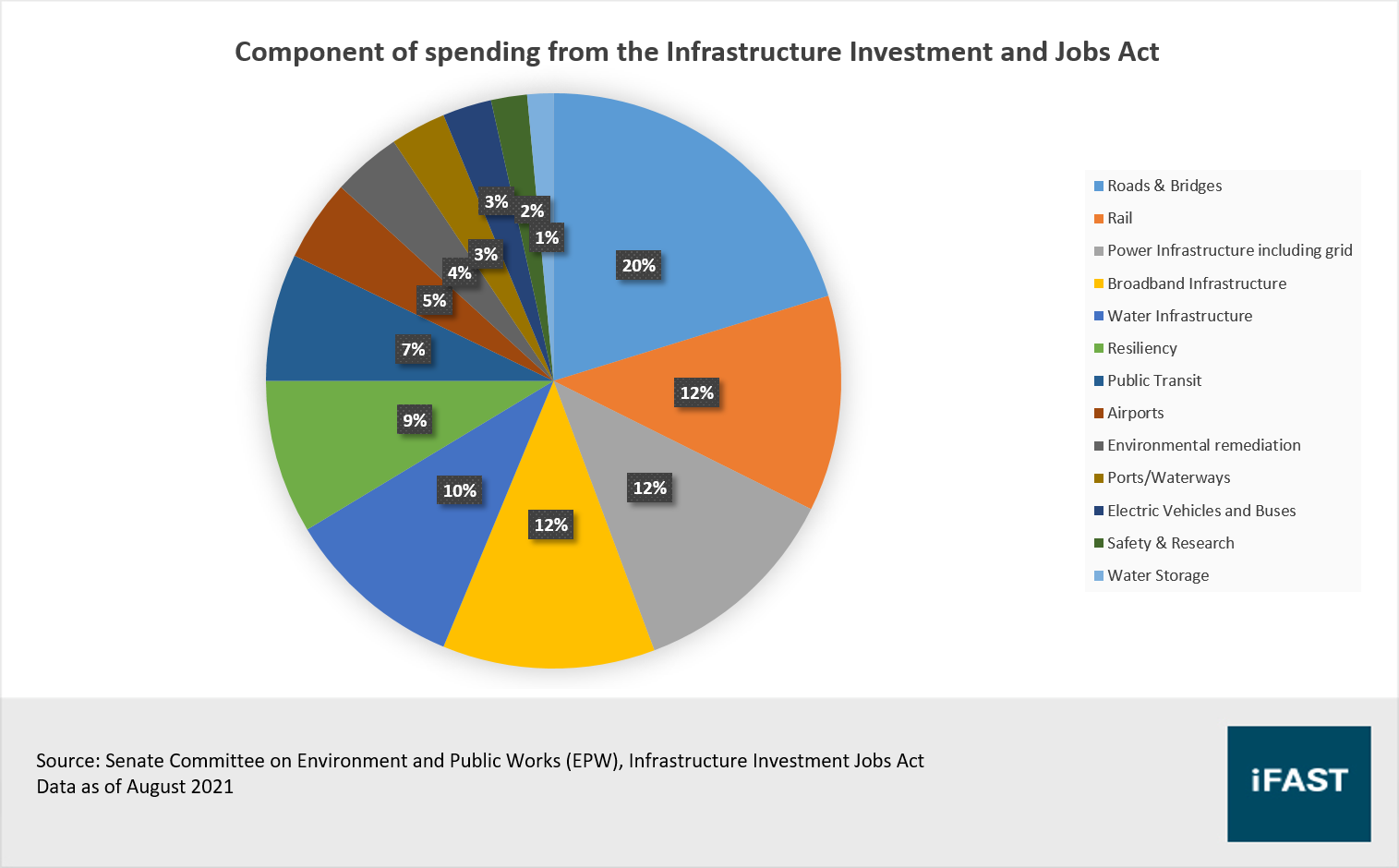

On 5 November 2021, Congress passed a bipartisan infrastructure bill known as the Infrastructure Investment and Jobs Act (IIJA) to modernise the country’s infrastructure and to create jobs. Funding from the IIJA is expansive in its reach, addressing energy and power infrastructure, access to broadband internet, water infrastructure, and more. The Act totals USD 1.2 trillion over the next decade, USD 550 billion of which would be for new federal spending that will be allocated over the next five 5 years (Figure 6).

Figure 6: Allocation of the USD 550 billion of new federal spending

Not to mention, Russia’s invasion of Ukraine caused turmoil within the global energy markets last year, driving oil and gas prices sharply higher. That forced many economies to reconsider their energy supplies and push ahead with longer term plans towards energy sustainability.

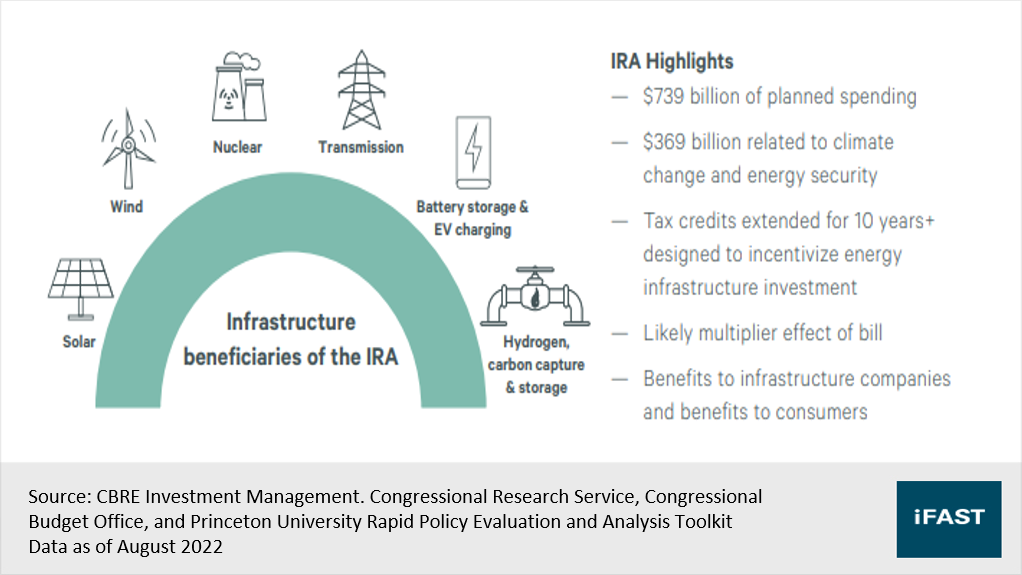

On August 2022, the US Inflation Reduction Act (IRA) was signed into law, and is one of the most significant climate legislation in US history. It commits more than USD 739 billion in planned spending and USD 369 billion to subsidies and tax credit over a decade to encourage decarbonisation and cleaner energy, including measures to support the development of hydrogen as a fuel source (Figure 7).

Figure 7: Infrastructure is at the heart of the Inflation Reduction Act

These measures incentivise the domestic supply chain within US and will support further investment and drive growth in renewable utilities. Moreover, the long-term extension of production tax credits and investment tax credits for wind and solar and the expansion of tax credits for other renewable technologies (e.g., clean hydrogen) will provide material long-term future funding streams.

Table 3: NextEra Energy is a clear beneficiary of the Inflation Reduction Act (IRA)

|

Impact of the IRA on NextEra Energy |

|

|

IRA Provisions |

Potential Growth opportunities |

|

|

|

Source: NextEra Energy, iFAST Compilations. Data as of Sep 2022 |

|

NextEra Energy is in an excellent position to benefit from money pouring into clean energy investments. The company estimates that solar production tax credits are also expected to save customers roughly USD 400 million over the term of its current rate agreement.

Key investment risks

Political risk: Regulated electric utilities are subject to federal and state regulation, including determinations of allowed revenues. Any adverse change in the Florida regulatory environment for instance could have a negative impact on FPL and its future earnings.

Interest rate risk: Infrastructure companies such as NextEra Energy often have high levels of capital expenditure, and thus debt levels. This exposes the companies to interest rate volatility or refinancing risk. Nonetheless, NextEra Energy is also less leveraged relative to its peers, with a debt-to-equity ratio of 1.14, compared to Duke Energy with 1.34, Xcel Energy with 1.49, and American Electric Power Company with 1.39.

Well-positioned for a long runway of growth

NextEra Energy has a unique proposition and a wide economic moat given its status as one of the largest utility and renewable companies in America. Its defensive utility and high growth renewable segment means that investors can benefit from having the best of both worlds. Despite trading at a premium relative to its peers (other utilities companies), we note that this is well warranted due to the company’s much higher than average EBITDA and profit margins (Table 4), and its strong renewables footprint.

Table 4: Comparison against its peers

|

|

Market Cap (USD millions) |

Forward PE (X) |

Profit Margin (%) |

EBITDA Margin (%) |

|

NextEra Energy |

146,598 |

23.79 |

19.79% |

42.67% |

|

Duke Energy |

72,549 |

16.71 |

8.86% |

43.76% |

|

Xcel Energy Inc |

35,328 |

19.04 |

11.34% |

32.28% |

|

CMS Energy Corporation |

17,222 |

19.04 |

9.74% |

28.20% |

|

American Electric Power Company |

45,659 |

16.79 |

11.75% |

36.27% |

|

Constellation Energy |

25,689 |

20.11 |

-0.65% |

11.95% |

|

WEC Energy Group Inc |

28,030 |

19.30 |

14.68% |

31.12% |

|

Consolidated Edison Inc |

32,412 |

18.74 |

10.59% |

29.95% |

|

Average |

50,436 |

19.19 |

10.76% |

32.45% |

|

*Profit Margin and EBITDA Margin are based on trailing 12 months Source: Bloomberg Finance L.P., iFAST Compilations. Data as of 9 March 2023 |

||||

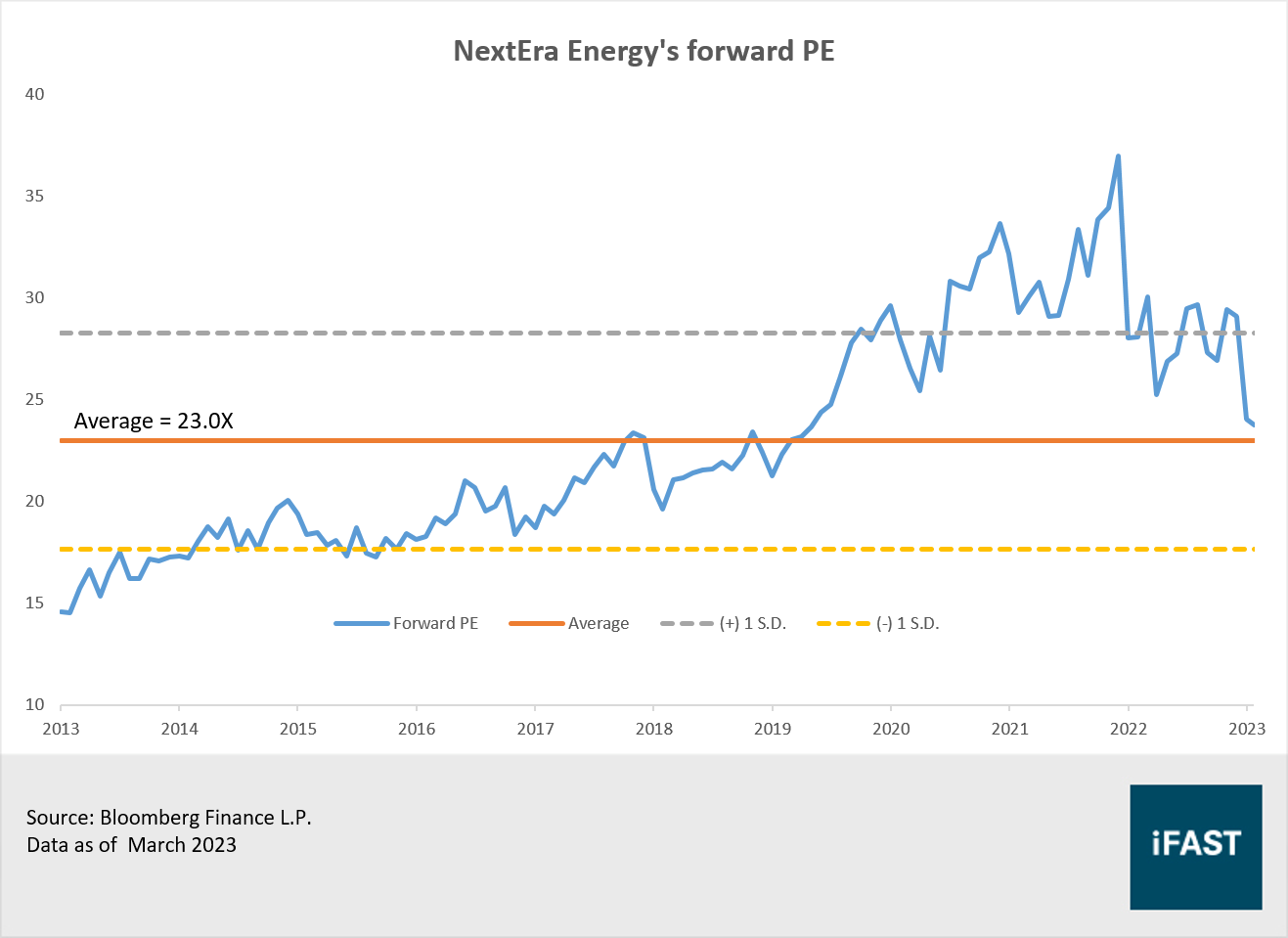

We assign a fair PE multiple of 25X to NextEra Energy, and while this is above the 10-year historical forward PE of 23.0X, we note that this is reasonable given the company has traded at higher multiples over the recent year (5-year historical forward PE is 27.0X). Not to mention, as the shift towards renewables accelerates, NextEra Energy is especially well-positioned to capitalise on this. Our 2025 target price for NextEra Energy is USD 94, and this translates to an upside potential of about 25% based on the last closing price of USD 75.36 on 21 March 2023.

Figure 8: NextEra Energy historical forward PE over the past 10 years

Table 5: EPS growth over the years

|

NextEra Energy |

FY22A |

FY23E |

FY24E |

FY25E |

|

PE Ratio (X) |

28.8 |

24.3 |

22.2 |

20.1 |

|

Earnings Growth |

13.7% |

7.0% |

9.5% |

10.0% |

|

EPS (in USD) |

2.90 |

3.10 |

3.40 |

3.74 |

|

Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 March 2023 |

||||

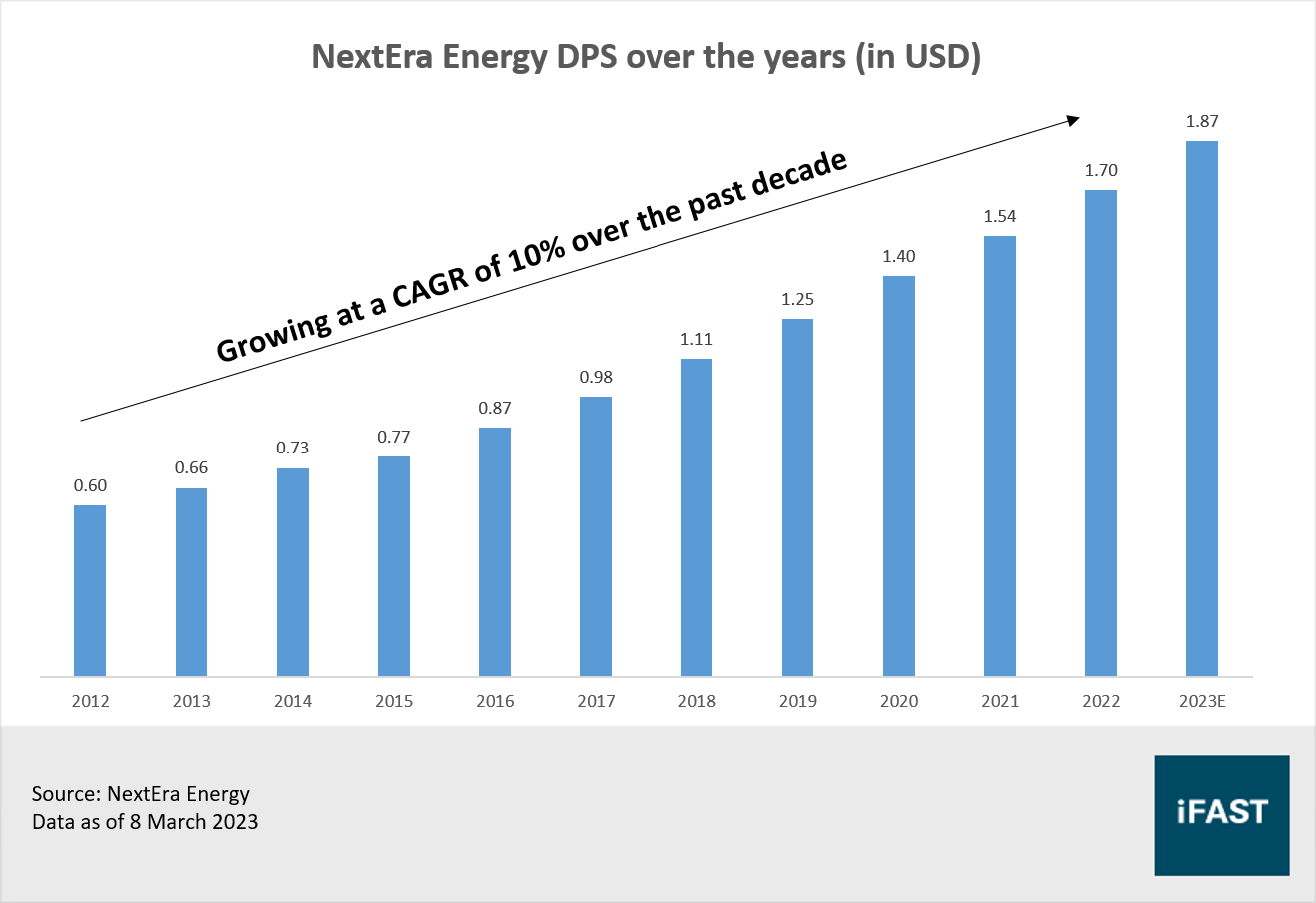

While NextEra Energy's dividend is not really considered high, its dividend growth is consistent as the company has increased its dividends per share (DPS) over the past two-and-a-half decades. For instance, its DPS has grown at a compound growth rate (CAGR) of 10% over the past decade (Figure 8). Investors can expect to receive a DPS of USD 1.87 for 2023, translating to a dividend yield of 2.5% (before withholding tax)

Figure 9: NextEra Energy DPS have been growing at a CAGR of 10% over the past decade

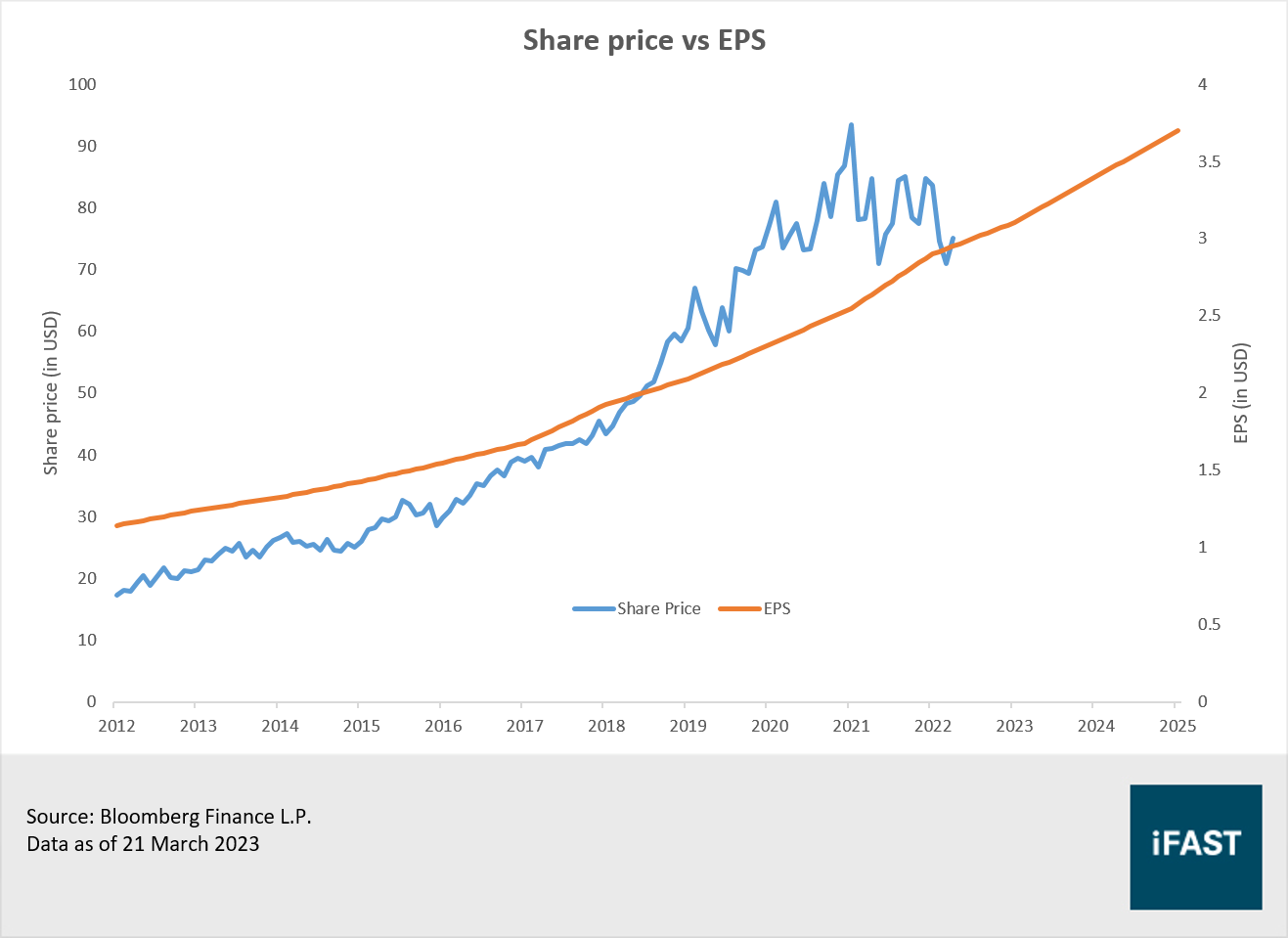

Figure 10: In the long run, share prices are driven by earnings

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report holds a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.