- The recent demise of the Luna/Terra stablecoin pair was only the latest chapter in what has already been a especially difficult 2022 for crypto assets.

- The Luna/Terra debacle has worrying parallels to historical financial crises in traditional financial markets, and we remain cautious amidst the crypto market's reluctance to learn from the mistakes of their predecessors.

- Because of this reluctance, what should have been a black swan event will likely occur again - and with no intrinsic value, there is no support when the panic selling ensues.

- Our stance remains clear: Cryptocurrencies remain a poor investment vehicle, and do not exhibit the quality and value characteristics we like in today's inflationary environment.

- After a difficult 2022 so far, quality and value opportunities with actual fundamentals and cash flows have emerged, and investors should consider buying the dip there instead.

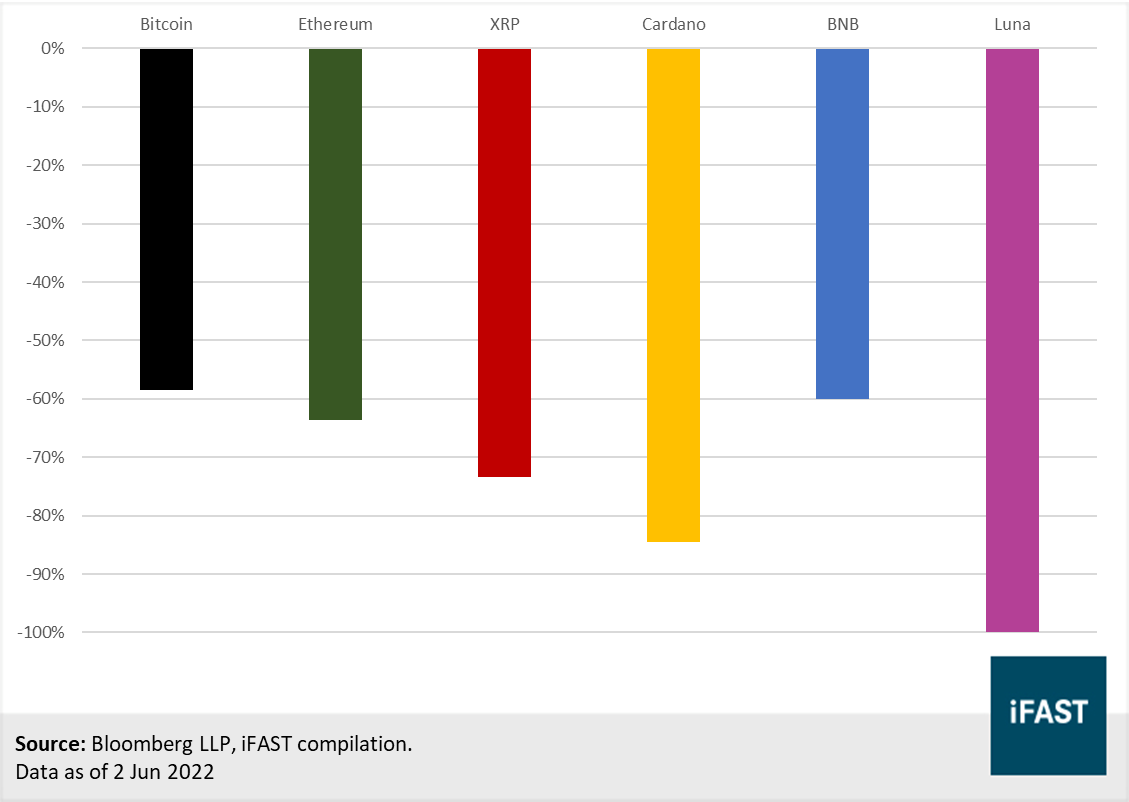

While 2022 has been a difficult year for most asset classes, few have been more troubled than cryptocurrency markets. After last year’s volatile swings, we have continued to warn investors about the industry’s limitations, and even cautioned averaging down or buying on dips given the absence of fundamental support. Since then, Bitcoin and Ethereum have seen large drawdowns, down almost 50% since most of their peaks in November 2021.

Figure 1: Since we issued our warnings, most major cryptocurrencies have been in the red

Figure 2: Not just red, but ugly to boot

The situation came to a head in May, with the demise of a pair of sister stablecoins – Terra & Luna. This debacle drove shockwaves through crypto markets, with many investors losing their life savings and observers drawing parallels to some of the worst financial crises seen in traditional markets. How did a “stable” asset go sour so fast?

Firstly, what are stablecoins and how do they work?

Stablecoins are cryptocurrencies that attempt to peg their market value to external sources of reference. Be it to currencies like the U.S. dollar or to the prices of commodities such as gold, one key aspect of stablecoins is to maintain price stability by ensuring sufficient reserve assets as collateral, or through algorithmic formulas to control supply.

To further understand the mechanics of stablecoins, let’s use an example of the already demised pair of cryptocurrencies mentioned earlier. Terra would always be exchangeable for $1 worth of Luna. If each Luna is worth $0.10, one Terra could be changed for 10 Luna. If Luna trades at $20, then one Terra could be change for 0.05 Luna. Through arbitrage and changes in supply, the goal is to ensure that Terra is always worth $1.

Stablecoins help to facilitate the use of cryptocurrencies as a medium of exchange by reducing the volatility, and hence, speculative nature of traditional coins.

Are stablecoins truly stable?

Unfortunately, the term “stablecoin” is very much a misnomer.

While collateralised stablecoins hold assets in reserve, they often lack accountability due to a lack of transparency. Most keep their cards close to their chest, and even amongst those that are audited, the validity of said audits often comes into question. While collateralised stablecoins are still generally considered a safer alternative to algorithmic stablecoins due to their collateralised nature, their faith-based nature means much of its “stability” hinges on the integrity and honesty of its founders. In the Wild West of the crypto world, this does seem relatively unwise.

So, what happened to Luna and Terra?

The algorithmic structure of these sister cryptocurrencies has meant that they were vulnerable to a death spiral, and death spiral it did.

The market lost faith in both Luna and Terra, possibly driven by the lack of confidence for the Anchor Protocol to maintain their 20% interest rates. Since both tokens have an algorithmic relationship, as Luna’s price went down, each Terra is now worth more and more Luna. With downward pressure on Luna’s price, investors lost faith in TerraUSD’s ability to hold the peg and sold off Terra, meaning the algorithm continued to increase Luna supply, exacerbating the downward pressure on Luna’s price. Eventually, this mechanism broke, and investors were left deeply in the red.

The supply of Luna has shot up from 343 million to 6.53 trillion, a magnitude of ~19000 times, and this dilution has resulted in the price of the coin cratering.

Should I buy the dip?

Here at iFAST, we remain firm in our stance that cryptocurrencies remain a poor investment vehicle – and investors should not attempt to average down and catch the falling knife.

Our rationale has not changed. Cryptocurrencies, unlike traditional investment assets like stocks and bonds, lack fundamentals and an end-use case, and are thus unlikely to be able to generate cash flows or earnings to return capital to investors. While some investors might draw parallels when investing in cryptocurrencies to investing in speculative early-stage companies, the key underlying difference is that companies are expected to generate cash flows in the (perhaps distant) future. These cash flows could then be returned to investors via share buybacks or dividends, which would help generate returns. As cryptocurrencies do not generate cash flows, barring someone buying it from you in the future at a higher price, one would struggle to see how investment returns are then generated (which is the very definition of the Greater Fool’s Theory).

So, what can we learn from this Luna/Terra debacle?

Although the novel concept of decentralisation in the financial world may be attractive and progressive to certain groups of investors, it is also important to understand the reality that regulations and laws are enacted for a reason. Unfortunately, crypto markets continue to willfully ignore the underlying reasons for these laws, either due to delusion or hubris.

It is relatively straightforward to draw parallels to bank runs - when trust and consumer sentiment rapidly weakens, leading to mass withdrawals and thus liquidity crunches in banks. The term “death spiral” has also been coined in traditional finance markets when used to describe the problematic structure of certain convertible bonds*, a relationship that is identical to that of Luna and Terra.

*Convertible bonds typically are exchangeable for a fixed number of shares, rather than a fixed dollar amount of shares, due to their vulnerability to death spirals. While traditional financial markets have learnt their lesson from this, cryptocurrency markets have turned a blind eye.

We also see similarities between the recent Terra/Luna incident to the Asian Financial Crisis in terms of currency pegs. Currency pegs are notoriously hard to maintain, and central banks historically have had to give up a significant amount of control over other monetary policy tools, such as interest rates or currency flows, in order to maintain these pegs. Despite that, history is littered with examples of failures – various Asian countries during the Asian Financial Crisis in 1997 and the UK pound peg in 1992 – highlighting the various challenges in doing so. Meanwhile, Luna/Terra sought to have their cake and eat it too – perhaps concerned by losing investor interest by either implementing lower interest rates on the Anchor Protocol or by limiting capital flows – resulting in a disastrous ending for all involved. Thus, investors should not be blindsided by this event or categorise it as a black-swan event.

On a larger, perhaps even systemic scale, alarm bells are chiming in the stablecoin market as well. Within the space, we see a proliferation of excessive leverage and self-perpetuating systems that are made to appear safer than they actually are – startling parallels to the mortgage-backed securities (MBS) that caused the Great Financial Crisis in 2008. Regulators worldwide have already taken note – and it remains uncertain if the current stablecoins remain nimble enough to survive the incoming regulatory tightening. Yet again, we advise caution – with no intrinsic value, there is no fundamental support for when the panic selling ensues.

How does this link to the traditional financial system?

While it is almost certain that digital currencies will be a thing in the foreseeable future, with central banks around the world being involved in testing and conceptualising their central bank digital currencies (CBDCs). Even Singapore has also embarked on our very own CBDC project, codenamed Project Ubin, since 2016. However, CBDCs and cryptocurrencies are two very different concepts.

CBDCs are not investments, but more of an alternative to traditional fiat currencies. However, there is no certainty that it has to be based on blockchain technology, given its limitations regarding transaction frequencies and cybersecurity issues. Moreover, we find the suggestion that these CBDCs will be based on any existing cryptocurrency network to be absurd. These currencies will almost definitely be centralised and controlled by a government – primarily for monetary policy, cybersecurity, and crime management purposes – and investing in the many tokens available today will not provide investment exposure to CBDCs in any meaningful way.

Our Stance: Avoid this 'Greater Fool Investment Strategy' Asset Class

We do acknowledge that the timing of our previous articles around this time last year was not perfect, with Bitcoin and Ethereum roaring to their all-time highs after we published our cautionary tales. But when it comes to taking a stance on cryptocurrencies, our answer is simple – avoid this 'Greater Fool Investment Strategy' asset class.

Related Reading: Crypto: Avoid this 'Greater Fool Investment Strategy' Asset Class

The space is rife with issues, ranging from smaller-scale issues like Ponzi schemes, scams, and insider trading to large systemic issues like excessive leverage, and self-perpetuating systems as we highlighted earlier in the article. History is rife with mistakes and financial disasters that the crypto industry should learn from, but are time and again willfully ignored. The launch of Luna 2.0 (the newly revamped version of the now-defunct Luna/Terra) and the launch of another stablecoin USDD (which works strikingly similarly to Terra/Luna, except it’s offering 30% p.a. instead – what could go wrong?) just days after the Terra/Luna debacle exemplifies the issues with the crypto industry.

Even the claims that Bitcoin is an inflation hedge have proven to be false – Bitcoin has behaved almost identical to a tech stock in 2022, and we know how these tech darlings have done in a rising rate environment. With the end-use case remaining unclear – Bitcoin has been touted as a variety of things, ranging from digital gold to the future of banking – the market clearly still sees Bitcoin as future tech, perhaps as an extension or proxy of blockchain technology.

Figure 3: Bitcoin moves like a more volatile tech stock…

Figure 4: … with their returns exhibiting a strong positive

correlation

With plenty of money circulating in the financial system in the last 2 years, cryptocurrencies have surged as investors search for investment alternatives. With monetary tightening and the tap drying up, so has irrational exuberance. Speculative investments have fallen out of favour, with cryptocurrencies featuring strongly amongst them.

Figure 5: The peaking of global money supply has preceded the peak of Bitcoin's market cap - which we do not believe is a coincidence

Yet again, we would like to reiterate: Do not attempt to average down and catch the falling knife. Markets have fallen throughout 2022, and opportunities have emerged – opportunities that have actual fundamentals and cash flows. In an inflationary environment, we like quality and value, and cryptocurrencies are anything but. The industry seems to have taken away no lessons from the Terra/Luna debacle, and until they do (or regulations step in), what should have been a black swan event will continue to happen – and investors should stay clear.

Related Reading: Here's Our Reply on Your Top-Voted Crypto Question

Related Video: Back to Terra Firma: What’s Next for the Crypto Space?

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.