- Against the backdrop of structural challenges, such as the acceleration of e-commerce and work from home (WFH), investors should be selective when it comes to investing in S-REITs.

- It is time to take a look at hospitality REITs. We believe that the recovery of hospitality REITs will strengthen in 2H 2021, propelled by the roll-out of vaccines.

- As Singapore enters Phase 3 of re-opening, there are certain opportunities within retail REITs. The resilient suburban malls are likely to continue its recovery to pre-COVID levels, much faster as compared to downtown malls.

- The long-term outlook for office REITs remains uncertain as office demand remains dampened from the prevalence of WFH. However, a bright spot is the healthy demand from the rapidly expanding tech sector.

- Lastly, outperformance from the industrial and data centre REITs is likely to continue as the sub-segment is driven by favourable long-term trends, such as the acceleration of e-commerce and growth of cloud services.

There has been a performance divergence within the S-REITs sector year-to-date. The performance of hospitality and retail REITs have been hit the hardest, thanks to COVID-19, while the resilient industrial and data centre REITs have outperformed the broader sector.

Figure 1: Total return of S-REITs sub-segments

The divergence is not surprising. The COVID-19 pandemic has accelerated certain structural trends, such as the adoption of work from home (WFH) and e-commerce. These structural trends are tailwinds for industrial and data centre REITs, but are headwinds for retail and office REITs.

Against this structural backdrop and with share prices already recovered from their March lows, we think investors should be selective when it comes to investing in S-REITs.

Hospitality: A vaccine-led recovery

The COVID-19 vaccine is a key catalyst for the recovery of hospitality REITs. Thus far, there has been positive vaccine news, which has led to a jump in the share prices of hospitality stocks.

During the Phase 3 clinical trial, it was reported that the vaccine developed by Pfizer and BioNTech has an efficacy of 95% against COVID-19. The Health Sciences Authority (HSA) has approved the use of the Pfizer-BioNTech vaccine, and the first shipment has already arrived in Singapore. This enables all Singaporeans to get vaccinated by end-2021.

Elsewhere, vaccines are expected to be rolled out soon too. Billions of people can be expected to be vaccinated next year. According to data provided by Bloomberg, there are 7.38 billion doses of vaccine contracted for distribution around the world as of 4 December 2020.

Hence, we believe that the roll-out of vaccines around the world will strengthen the recovery of hospitality REITs in 2H 2021. Based on consensus estimates, hospitality REITs are offering a decent 2022 yield of 6-7% based on their current prices.

However, even if a vaccine were to be made available in 2021, we do not expect a full recovery to pre-COVID levels that soon, as time is needed to achieve mass vaccination. In the meantime, most hospitality REITs will be supported by the fixed rent from their master leases, which will continue to provide downside protection while we wait for a resumption in air travel.

We also note that the market may start to price in earnings beyond 2022. Looking further ahead, the long-term catalysts in Singapore’s tourism industry still remain intact. There are various tourism developments and initiatives in the pipeline, all of which will be able to support Singapore’s long-term growth in tourist arrivals.

Table 1: Major tourism developments in the pipeline

|

Name |

Description |

|

Rejuvenation of Orchard Road |

Revamping Orchard Road shopping belt via 4 sub-precincts with new retail concepts and attractions |

|

Expansion of Resort World Sentosa |

Multiple new attractions such as Minion Park and Super Nintendo World in Universal Studios Singapore |

|

Mandai Nature Precinct |

New developments include the Bird Park, Rainforest Park and a Nature Resort |

|

Sentosa Redevelopment |

Reshaping Sentosa and Pulau Brani into a premier leisure and tourism destination |

|

Jurong Lake District |

A new tourism development consisting of an attraction, retail, F&B, entertainment, hotel and open public spaces |

|

Source: OUE Commercial REIT, CDL Hospitality Trust, iFAST Compilations |

|

We

are positive on Ascott Residence Trust (SGX:HMN) for its large exposure to countries with a sizable domestic travel market, such

as Japan, Australia, China, and the US. As borders will take time to re-open,

domestic travel will recover at a much faster pace as compared to international

travel.

Figure 2: ART share price tracks its DPU

Table 2: ART DPU Growth

|

|

2019 |

2020E |

2021E |

2022E |

|

Distribution Yield (%) |

5.7 |

2.8 |

4.4 |

5.6 |

|

DPU Growth (%) |

6.3 |

-60.8 |

59.1 |

26.3 |

|

DPU (SGD) |

0.076 |

0.030 |

0.047 |

0.060 |

|

PB Ratio |

1.1 |

1.0* |

- |

- |

|

*Current PB Ratio Source: Bloomberg Finance L.P., iFAST Estimates Data as of 22 December 2020 |

||||

Retail: Suburban malls to stay resilient

The retail REIT is also another sub-sector to watch as Singapore enters into the long awaited Phase 3 re-opening on 28 December 2020.

We believe suburban malls are likely to continue their recovery to pre-COVID levels during Phase 3. Frasers Centrepoint Trust (SGX:J69U) – a predominantly suburban retail REIT – had experienced a sharp recovery post-circuit breaker. As of October 2020, total tenants’ sales were only down by -1.8% year-on-year.

It is also worthy to note that FCT’s tenant sales were above the industry average. According to the Department of Statistics, October retail sales in Singapore (excluding motor vehicles) fell by -11.2% year-on-year.

Figure 3: Frasers Centrepoint Trust is on a path to recovery

Suburban malls tend to focus on essential goods and services, and have a close proximity to densely-populated residential areas. Hence, this supports their ability to be more resilient against the acceleration of e-commerce, which has been posing structural challenges to physical stores.

Based on data obtained from the Department of Statistics, industries that focus on non-discretionary spending have indeed been more resilient despite the competition from e-commerce. As shown in Figure 4, the online sales proportion for supermarkets and hypermarkets in Singapore have remained relatively stable compared to other industries, even when the “circuit breaker” took effect from April to June 2020.

Figure 4: Online sales proportion for Singapore’s supermarkets and hypermarkets have remained relatively stable

As compared to suburban malls, we believe that downtown malls will take more time to recover. Downtown malls are more reliant on tourists and office workers. With continued restrictions on most short-term visitors to Singapore and many office workers yet to return to office, we expect rents in downtown malls to remain under pressure in the near term.

Looking into the longer term, downtown malls will continue to face headwinds such as the acceleration of e-commerce.

For instance, Capitaland Integrated Commercial Trust (SGX:C38U), the product of the merger between Capitaland Mall Trust and Capitaland Commercial Trust, has more downtown retail exposure. CICT will be taking on more risks from its tenants, resulting in the reduction its fixed rent component and increase in its turnover rent component, a negative for unitholders as distributable income will be more dependent on tenant sales, which are being threatened by the competition from e-commerce.

Hence, we are more positive on Frasers Centrepoint Trust for its exposure to suburban malls.

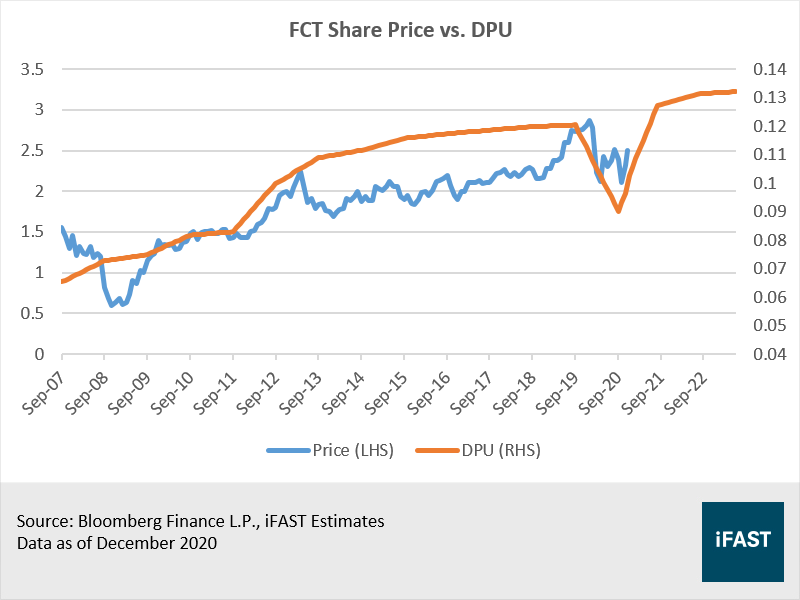

Figure 5: FCT share price tracks its DPU

Table 3: FCT DPU Growth

|

|

FY2020 |

FY2021E |

FY2022E |

FY2023E |

|

Distribution Yield (%) |

3.8 |

5.2 |

5.3 |

5.4 |

|

DPU Growth (%) |

-25.1 |

41.0 |

3.4 |

0.6 |

|

DPU (SGD) |

0.090 |

0.127 |

0.131 |

0.132 |

|

PB Ratio |

1.1 |

1.1* |

- |

- |

|

Financial Year ends in September *Current PB Ratio Source: Bloomberg Finance L.P., iFAST Estimates Data as of 22 December 2020 |

||||

Office: WFH is here to stay

It is undeniable that WFH is here to stay, given how it has brought about various benefits for both employees and employers. Even as Singapore enters into Phase 3 of re-opening, we think more companies will adopt a mix between WFH and work in office (WIO). Furthermore, as employees will not be in office as often as before, hot-desking may be getting more popular.

This will reduce the need for companies to expand their office spaces, and some may even consider downsizing. With the reduced demand for offices, occupancy rates and rental rates are likely to remain under pressure, thus affecting the income of office REITs in the longer term. We also expect more tenants asking for shorter and more flexible lease terms as they figure out their future office needs.

On a more positive note, office demand from the tech sector seems healthy. While tech companies have been the ones embracing the WFH model, they are still leasing office spaces. This could be attributed to the fact that the tech sector has continued to boom during the COVID-induced recession, resulting in its rapid expansion and the need for more workspaces.

For instance, Chinese tech giants like Alibaba, ByteDance and Tencent have announced that they will be setting up offices in Singapore. If such strong momentum persists, we think it might be able to mitigate the overall reduction in office demand.

As the long-term outlook for office remains uncertain, investors should be cautious on office REITs. Some office REITs have recorded weak rental reversions this year (e.g. Mapletree Commercial Trust: -1.6%). Rental reversions are likely to be weaker or even fall into the negative territory going forward as rental rates remain under pressure (Figure 6).

Figure 6: Rentals are on a downtrend

However, investors who wish to ride on office demand from the tech sector may consider Keppel Pacific Oak US REIT (KORE) (SGX:CMOU), which has a large exposure to the growing tech hubs in the US.

In 9M 2020, KORE reported a strong positive rental reversion of 14.1% largely due to the new and expansion leases from the tech hubs of Seattle and Denver. Against the backdrop of an uncertain economic environment, we expect to see single-digit positive rental reversions going forward. Moreover, US offices have built-in rental escalations, which provides opportunities for organic growth.

We have valued KORE at a target price of USD 0.79 (Upside: 12%, Yield: 9% as of 22 December 2020).

(Related article: Keppel Pacific Oak US REIT still has a role to play in a post-COVID future)

Industrial & Data Centre: Outperformance likely to continue

We believe industrial and data centre REITs are well-positioned to deliver resilient growth going forward. Their outperformance will be driven by favourable trends, such as the acceleration of e-commerce and growth of cloud services.

The acceleration of e-commerce will continue to drive the demand for warehouse spaces. Meanwhile, the prevalence of WFH has accelerated the shift towards cloud collaboration solutions. Coupled with the future adoption of 5G, the higher data traffic will lead to an increase in spending on data centres.

While recent rental rates have been under pressure due to the uncertain economic conditions, such strong demand should be able to support rental rates in the longer term.

Ascendas REIT (SGX:A17U) – the largest industrial REIT – is well-positioned to ride on the key trends of the post-COVID economy. It has a diversified portfolio consisting of assets such as data centres, suburban office properties and logistics properties.

Figure 7: Ascendas REIT boasts a diversified portfolio

We believe that growth will be driven by its expanding data centre portfolio which rides on the structural demand for cloud services. Moreover, its recent acquisition of US suburban office properties in the South of Market, San Francisco enables it to ride on the growing office demand from the burgeoning tech and life science sectors.

In terms of inorganic growth, its gearing ratio of 34.9% (as of 30 June 2020) leaves ample debt headroom of SGD 4.2 billion to supplement future growth. We believe that DPU-accretive acquisitions will be another key catalyst to its outperformance.

Figure 8: AREIT’s share price tracks its DPU

Table 4: AREIT DPU Growth

|

|

2019* |

2020E |

2021E |

2022E |

|

Distribution Yield (%) |

3.9 |

5.0 |

5.4 |

5.5 |

|

DPU Growth (%) |

-3.3 |

28.7 |

7.4 |

2.5 |

|

DPU (SGD) |

0.115 |

0.148 |

0.159 |

0.163 |

|

PB Ratio |

1.4 |

1.3** |

- |

- |

|

*9M ending Dec 2019 due to change in reporting period **Current PB Ratio Source: Bloomberg Finance L.P., iFAST Estimates Data as of 22 December 2020 |

||||

Conclusion

With the recovery in share prices (Figure 9), the valuations of S-REITs are looking less attractive as compared to the first two quarters of this year.

Figure 9: PB of the FTSE ST REIT Index

Therefore, with an uneven recovery within the S-REITs sector, investors should be selective when investing within this space (Table 5). Investors betting on a COVID recovery can consider hospitality and suburban retail REITs. Moreover, with long-term trends that will prevail in a post-COVID world, investors should also take a closer look at industrial and data centre REITs.

Table 5: S-REITs 2021 outlook

|

Sub-segment |

Outlook |

Stock Pick |

|

Hospitality |

|

Ascott Residence Trust (SGX:HMN) |

|

Retail |

|

Frasers Centrepoint Trust (SGX:J69U) |

|

Office |

|

Keppel Pacific Oak US REIT (SGX:CMOU) |

|

Industrial & Data Centres |

|

Ascendas REIT (SGX:A17U) |

|

Source: iFAST Compilations |

||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in Keppel Pacific Oak US REIT.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.