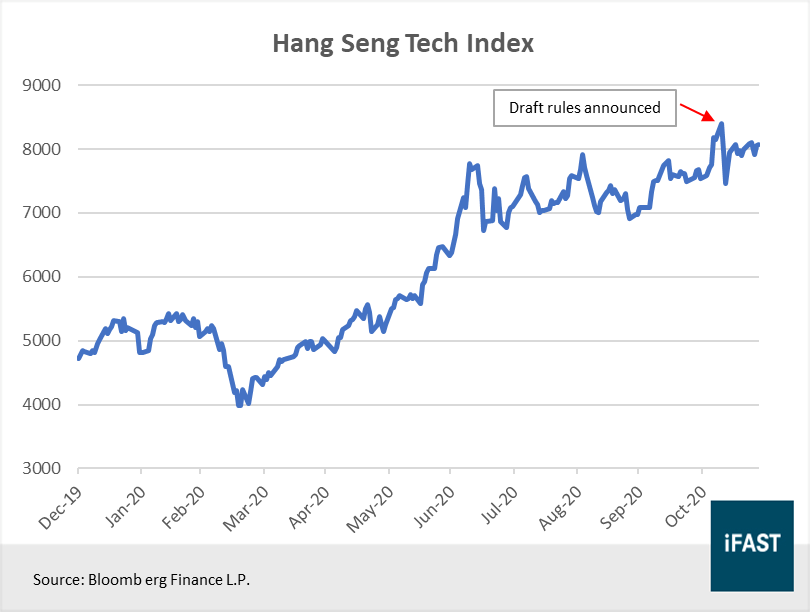

On 10 November 2020, China’s State Administration for Market Regulation announced a new set of draft rules aimed at controlling the growing influence Chinese Internet companies have over the country’s economy and society. This came right after China tightened rules on the consumer lending industry, a move that led to the suspension of Ant Group’s initial public offering (IPO).

The proposed rules cover a variety of issues ranging from the sharing of consumers’ data to the use of anticompetitive practices, such as forced exclusivity deals, and offering prices that are below cost to eliminate competitors.

The state regulator added that the main purpose of these rules is to safeguard consumers, and to promote healthy competition and the sustainable growth of China’s technology sector in the long run. It will be seeking public feedback on the draft rules until 30 November 2020.

Over the past few years, loose regulatory oversight has helped Chinese companies like Alibaba and Tencent grow into the behemoths they are today. Following the announcement of the draft rules, the share prices of Chinese tech giants plunged as investors fear that greater regulation could have an adverse impact on the future growth of these companies (Figure 1).

Figure 1: Shares prices of Chinese tech giants fell following the announcement of the draft rules

We believe that the recent sell-off is largely sentiment-driven, and we caution investors against making any knee-jerk reaction to the news. Instead, investors should remain focused on the industry’s long-term growth prospects.

Increased regulation unlikely to affect long-term growth story

On the whole, we believe that increased regulation should not significantly alter the long-term growth story of China’s technology sector, which is supported by real megatrends, such as the digitalisation of consumption, and a rapidly growing Internet population (Figure 2), which tech companies thrive on.

Figure 2: Tech companies benefit from the rapidly increasing internet population

First of all, we do not think that it is the government’s intention to freeze the growth of tech companies. Rather, because a number of tech companies have grown to become systemically important to the economy, with practically every Chinese citizen using their services on a daily basis, some form of regulation is necessary to keep them in check.

Moreover, the government has acknowledged that technology companies played a crucial role in stabilising the economy during the pandemic, allowing businesses and individuals to carry out their daily activities with as little disruption as possible. Through this, it is evident that the government recognises the value these tech companies have as the country undergoes a massive digital transformation.

Secondly, many of these tech giants, like Alibaba (NYSE:BABA) and Tencent (HKEX:700) for instance, are considered crown jewels of China’s modern economy. Without them, China’s digital landscape today would have been vastly different. If China wants to overtake the US to become the largest economy in the world, it cannot do so without the help of its technology companies.

Lastly, the majority of the successful tech companies in China today have benefitted from network effects (e.g. WeChat’s ecosystem) and superior product offerings rather than significant anti-competitive behavior, which is what the government is trying to deter. Because of this, we believe that consumers will likely continue to patronise their services.

In summary, we continue to hold a positive view on China’s technology sector. Even if the potential regulations were to be implemented, we believe that the negative impact on the long-term growth story of China’s technology sector should be minimal.

With technology companies at the forefront of China’s digital transformation, we expect to see strong earnings growth and better share price performance from them in the coming years. We continue to recommend the iShares Hang Seng Tech ETF (HKEX:3067) for investors who wish to gain exposure to China’s fast-growing technology companies.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.