- Gold has risen more than 30%, presenting itself as one of the best performing asset classes year-to-date

- On our platform, there are numerous ways to gain exposure to the shiny metal, either via ETFs, or the list of actively managed gold equity funds on the platform

- Despite its safe haven status, gold is quite volatile and is not immune to boom and busts. For investors interested in having some gold exposure, we recommend you to keep the exposure to gold small and manageable

It’s no stranger why there has been an increase in investor interest in the shiny metal over the recent months. As the saying goes, there’s nothing like price that changes sentiment the way it does. Gold has seen quite a run on a year-to-date basis, returning an impressive 33% at its peak (US$2070/oz). As of 22 September 2020, the precious metal closed at a price of US$1906/oz . Falling real yields is arguably the biggest driver of gold prices in the current macro environment. Low nominal interest rates, and prospects of higher inflation in the future (due to higher deficit spending now) have attracted investors to precious metals as a source of hedge against uncertainty in growth prospects, and a potential debasement of fiat currencies across the globe.

Chart 1: Gold prices across major currencies are all at their all time highs

Physics students will be familiar with this concept: “For every action, there is an equal and opposite reaction”. The bigger the push, the bigger the pushback. Certainly, we’re not seeking to apply physics to investing, but you most likely get the drift. There are consequences for the recent monetary and fiscal policy actions enacted by governments globally, in response to the unprecedented economic slowdown. Especially in the US, of which we’ve seen one of the greatest rates of change, among its global peers, in terms of central bank and government balance sheet expansion. Rising precious metal prices across all major currencies, are most probably a feature of this opposite reaction.

Chart 2: There’s a strong relationship between lower real rates & higher gold prices

The biggest gold bulls on the street will likely tell you that the road to a post-COVID19 recovery will require governments to spend big while interest rates are kept low. As a consequence, real yields will likely remain depressed as economies attempt to get back on track to growth territory. The world will be flushed with liquidity. On the other end, there will be gold skeptics who will say that there’s no real way to value nor use gold on a daily basis, aside for decorative or cultural purposes. One could simply hedge against inflation by buying equities, as this rise in consumer prices will be captured in equity earnings. Both bulls and bears could be right. And yet we have no way of knowing until after the fact. However, if you belong in the bull camp, here’s some things that you might want to know before you start investing in gold.

Where is gold demand coming from?

Perhaps the first thing you want to know is who the main buyers of gold are. Gold has diverse uses. Most of the demand for gold comes from jewellery, of which the biggest markets are China and India. Gold still holds significant cultural value for these countries. About 50% of long-term demand comes from this segment, and rising wealth in these countries tend to bode well for demand for gold jewellery.

Investment demand by market participants is the second greatest source of gold purchases. While COVID-19 has dampened jewellery demand this year, gold prices have continued to climb. The fall in jewellery demand has been mostly offset by rising inflows into gold ETFs in the first half of 2020.

Another source of demand comes from central banks themselves. Central banks include gold as part of their reserves. Demand from this segment depends on reserve policies of central banks across the globe. Notably, China’s and Russia’s central banks have been net buyers of gold in recent years.

Lastly, there are also significant technological applications for gold. Gold is sought after for its stability in conducting electricity relative to other metals such as silver. About 10% of long term demand comes from producers of technological products.

Do you want to own physical gold, or merely gain exposure to gold?

There are various ways one can get exposure to precious metals. Most notably, investors will have to decide if they want to invest in physical or paper gold. Counterparty risk is the main difference separating the two. Physical gold (e.g. bullions & gold coins) investors do not encounter such risks. Rather, they will have to deal with storage costs which could add up to a substantial sum over several years or decades. On the other hand, paper gold instruments are probably the most popular option around today. Examples of such are your exchanged-listed gold ETFs.

Many of such ETFs (like NYSE:GLD) advertise to be physically backed. However, realistically it is likely that most mom-and-pop investors will not have a claim on the underlying. One would have to own a lot of shares (for GLD, a minimum of 100,000 shares is required) to be even eligible for physical delivery. Even so, taking on physical delivery will come with a new host of complications. Evidently, this is not realistic for most retail investors. But regardless, the benefits associated with investing via gold ETFs is difficult to argue. For one, gold ETFs have been able to track gold prices very closely at a very low cost. They are also highly liquid and easy to trade. Physically-backed gold ETFs enable retail investors to gain exposure to the asset class without the logistical problems and costs associated with storing gold.

Our ETF team has hand selected the SPDR Gold Minishares (NYSE: GLDM) as part of the 2020/2021 ETF Focus List. Unlike GLD, whose price is listed at 1/10th ounce of gold, GLDM is listed at a trading price of 1/100th ounce of gold, which allows for greater divisibility, and ease of access to investors. GLDM features similar tracking error as GLD, but with a lower expense ratio. The only downside is that GLDM has relatively lower liquidity than GLD. But with an average daily volume of 2.7m shares (for GLDM), retail investors should be able to attain a fairly good price when buying and selling. If you are seeking to buy and hold, GLDM could be a better choice given its lower fees.

Chart 3: GLD & GLDM have been great at tracking gold prices

(Related ETF: NYSE:GLDM, NYSE: GLD)

Investing in gold equities is not the same as investing in gold

Actively managed gold & precious metals unit trusts are another way to gain exposure to gold, but it is certainly not a pure-play. These funds often invest in companies that explore, mine and/or produce the commodity. Generally, the prices of gold equities will move in the same direction as gold over the long term. Higher volatility also tends to be a feature associated with investing gold mining companies, since there are more levers at play.

For instance, political, company, and country specific risks, and even oil prices (gold production is an energy intensive operation) could weigh on a company’s future profitability and detract from equity performance. Given different jurisdictions, every company likely has slightly different operations which entails different types of risks. Therefore, it may be important for you to consider an actively managed unit trust when thinking about investing in gold equities, as having a team to sieve out all these nuances for you could add significant value to your gold portfolio.

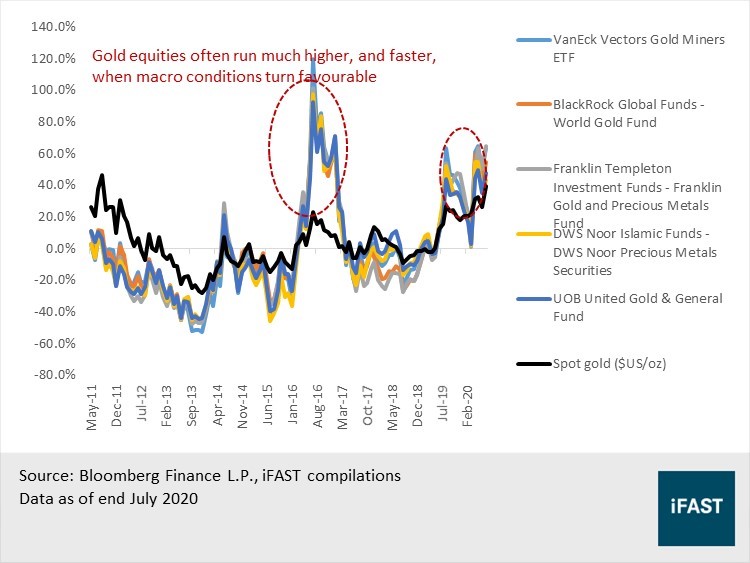

While gold equities are generally a riskier investment option, it is also more rewarding when they do show up to perform. High operational leverage employed by gold companies means that they would be extra sensitive to price changes in the underlying. Every dollar increase in gold would likely see a multiplier effect on their earnings or free cash flows, and thus their equity prices. When macro conditions turn favourable, we often see gold equity prices outperforming gold itself.

Chart 4: Rolling one-year returns of Gold Miners ETFs, Gold equity Funds, and Gold

(Related funds: NYSE:GDX, Blackrock World Gold Fund A2 USD, FTIF - Franklin Gold and Precious Metals A (acc) USD, DWS Noor Precious Metal Securities A USD, United Gold and General A Acc SGD, Schroder ISF Global Gold A Acc USD)

If you invest in gold, you might want to keep your exposure small or manageable

Adding gold to your portfolio could be one way to diversify your portfolios away from equity and fixed income. If you had some allocation towards gold this year, be it a gold ETF or a gold equity fund, your portfolio performance would have fared better than your peers who stuck with investing solely in equities and fixed income. A quick check on the performance of precious metals equity funds, or gold ETFs on a year-to-date basis should give you a good idea.

However, we believe gold as an asset class should not form a significant chunk of your portfolios. Often, the economic factors that drive gold prices tend to be less predictable, and less obvious than general equities. And despite its status as a ‘safe-haven’ asset, gold prices have historically shown to be fairly volatile. Gold is not immune to boom and busts. The sell-off yesterday (11 August) of more than -5% is a good timely reminder on that.

There have been periods when gold investors had to endure decades of underperformance. From the late 1970s to early 2000s (see Chart 1 above), if you had invested in gold back then, your investment would have been unprofitable for close to a good quarter of the 20th century. A massive opportunity cost, if one had concentrated his or her investments in gold or gold related instruments.

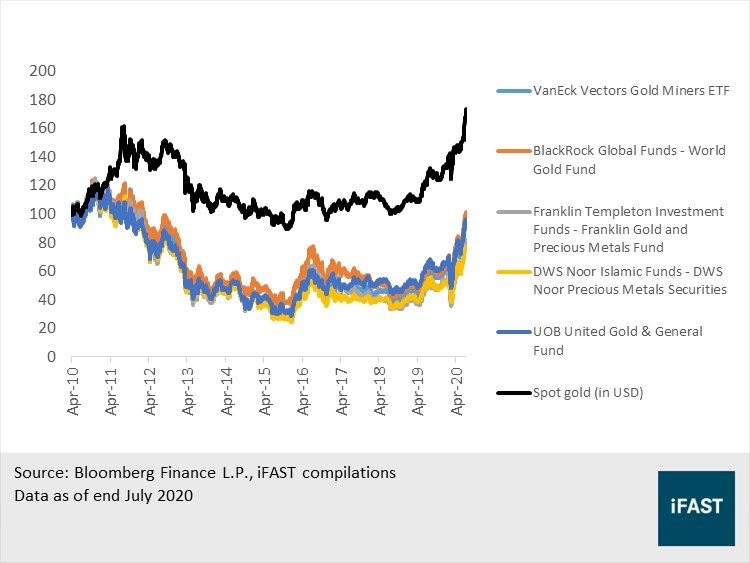

Another similar, and more recent case study could be observed from gold equities, which have only just begun to break even following the Great Financial Crisis. The chart below shows the indexed return of various gold equity funds (active & passive) versus the actual gold itself. The numbers are quite telling.

Chart 5: Gold equity funds are only beginning to break even since the GFC

For investors who are seeking to gain some exposure to gold or gold related investments, we recommend investors to keep any allocation small, as part of the supplementary portion within your overall portfolio. Often, we advise investors to apportion about 10% to 20% of their overall portfolios as supplementary. Investments within your supplementary portfolio are meant to serve as a complementary kicker to your core portfolio, whether in terms of adding higher-risk returns, or diversification. So within this supplementary allocation, you will have to think about how much should be allocated to each idea.

For example, if you do decide to have an equal allocation for four investment themes (with gold being one of them), your effective exposure towards gold at an overall portfolio level, will be either 5% or 2.5% at a 20% and 10% supplementary portfolio allocation respectively. If you are unsure about what to do, feel free to hit up with some of our friendly investment advisors who will be glad to help you on your way.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.