- The United States Oil Fund LP (NYSE:USO) previously tracks crude oil prices by investing exclusively in the front-month WTI crude oil futures contracts, which are rolled every month before expiration date. It has since announced sweeping changes to its investment strategy.

- The cost associated with rolling futures contracts in a contango market negatively affects the performance of USO.

- As the short-term demand for crude oil has been shattered by the COVID-19 outbreak, the futures markets has entered steep contango. This means that USO will have to pay a huge premium when it eventually rolls from June to the July contracts.

- There are also serious structural issues associated with USO, including a significant departure from its original investment objective, and a temporary suspension of new unit creation.

- Investors betting on an oil price rebound should steer clear of USO, and consider other alternatives like the United States 12 Month Oil Fund LP (NYSE:USL) and the Invesco DB Oil Fund (NYSE:DBO).

Last week, investors piled a record USD 1.6 billion into the United States Oil Fund LP (NYSE:USO), which is currently the largest and one of the most popular oil-related ETFs. If the record inflows to USO is any indication, scores of investors are rushing to position themselves for an eventual recovery in crude oil prices.

To be sure, there is nothing wrong in wanting to speculate on oil prices. In fact, oil is currently at dirt-cheap levels (Chart 1), and there are legitimate reasons to believe that oil prices may rise overtime.

Chart 1: Spot price for West Texas Intermediate crude oil at historical lows

Earlier this month, the OPEC pulled off a historic deal to cut global oil production by about 10%, putting an end to a devastating price war. Moreover, with a stabilisation in the global COVID-19 situation, countries around the world are also working on plans to gradually lift social distancing measures and reopen their economies, a move that could lead to a rebound in global oil demand.

Before you rush into buying USO, however, it is important to gain an understanding of how oil ETFs work.

The concept of “roll cost” in contango markets

While there exists physical commodity ETFs that actually own the underlying commodity, such as gold, most commodity ETFs do not invest in commodities directly. Instead, they produce exposure to the targeted commodity through the use of futures contracts. USO tracks crude oil price movements by investing in the West Texas Intermediate (WTI) crude oil futures contracts.

These futures contracts trade by month with expiration dates. On the day of expiry, investors have to either take physical delivery of the crude oil, or ‘roll’ their positions to the next month. USO invests exclusively in front-month contracts, referring to the contracts that are nearest to expiry, and it rolls its positions to the next month to avoid taking physical delivery. What this means is that, USO will sell its soon-to-expire contracts, and buy into contracts that expire the following month.

Most futures markets, including the crude oil futures market, are in contango, a situation where the price of contracts further out in time are more expensive than earlier contracts due to storage and insurance costs. As such, every month when USO rolls into the next-month contract before the front-month contract expires, it is buying the next-month contract at a higher price (Chart 2).

Chart 2: Prices of WTI crude oil futures contracts in contango

Other than incurring trading commissions and fees, the process of rolling positions from one contract to another, in and of itself, does not automatically result in a loss for investors, as USO’s total dollar exposure to futures contracts remains the same. However, if oil prices remain unchanged, futures prices will gradually decline to the spot price on expiration, and this means that USO will gradually decline over time in a contango oil market.

To illustrate simply, let us assume that USO currently holds January WTI crude oil contracts worth USD 50 (Table 1). Before they expire, USO sells these contracts and purchase the February contracts for USD 51. If spot oil prices remain unchanged at USD 50 when the February contracts expire, the prices of the February contracts will eventually decline towards USD 50. USO will then have to realise a 2.0% loss before rolling to the March contracts.

Similarly, if USO chooses to roll into the March contracts worth USD 52 instead of the February contracts, the prices of the March contracts will eventually decline towards USD 50 when they expire – that’s a cumulative 3.8% loss.

The realised loss by USO is also known as a “roll cost”. You can think of roll costs as the holder of a crude oil futures contract paying the storage costs, which accumulate over time.

Table 1: Illustration of roll cost in a contango market

|

January |

February |

March |

April |

May |

|

|

Futures Price (USD) |

50 |

51 |

52 |

53 |

54 |

|

Spot Price (USD) |

50 |

50 |

50 |

50 |

50 |

|

Roll Cost (%) |

0.0 |

2.0 |

3.8 |

5.7 |

7.4 |

Overtime, the cost associated with rolling futures contracts in a contango market negatively affects the performance of USO. A 2% roll cost every month adds up to a hefty 26.8% loss on an annualised basis. If oil prices simply stood still, contango ensures that USO will decline over time.

The current steep contango has made USO even more problematic

It is normal for the crude oil futures market to be in contango.

But times are far from normal.

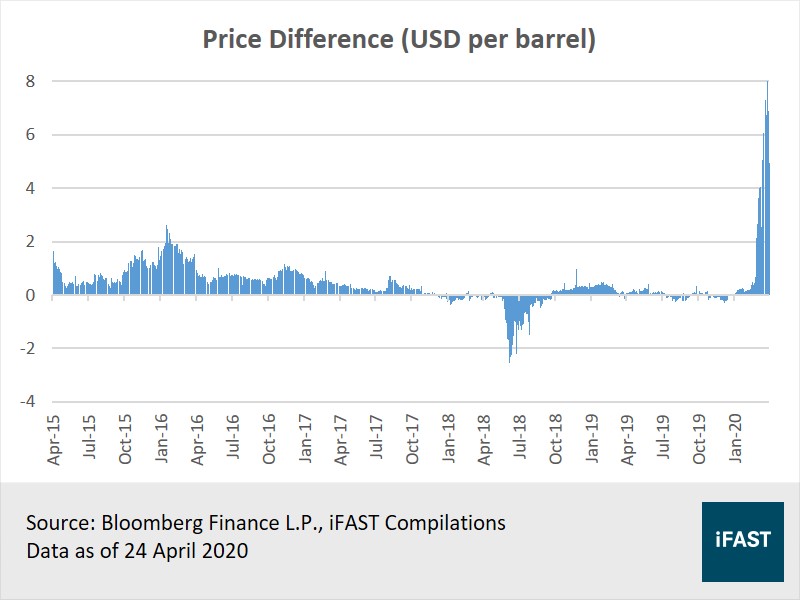

As the short-term demand for crude oil has been shattered by the COVID-19 outbreak, the futures markets has entered steep contango, with the price difference between the front-month and next-month contracts surging to record highs (Chart 3). At one point in time, WTI futures for May 2020 delivery fell to USD -37.63 per barrel. Yes, you saw that right. It fell to negative territory, meaning oil producers were effectively paying people to take the commodity off their hands.

Chart 3: Price difference between front-month and next-month contracts has surged to record highs

While the spread has narrowed over the past week, it remains high relative to historical standards. The front-month June contract is currently priced at USD 16.94, while the next-month July contract is priced at USD 21.22 (as of 24 April 2020). This means that USO will have to pay a huge premium when it eventually rolls from June to the July contracts.

As illustrated earlier, if spot oil prices remain unchanged, investors are guaranteed to lose money. A lot of it, especially if the steep contango in the oil futures market persists. If spot oil prices remain at its current level of USD 16.04 per barrel, the value of USO can still decline by as much as 30% over the next two months.

Also, don’t forget about USO’s total expense ratio of 0.72%.

USO’s troubles extend beyond steep contango

Besides the current steep contango in the oil futures market, there are serious structural issues associated with USO.

For years, USO has confined its holdings to just front-month contracts. Over the past few days, however, it has made several significant changes to its investment strategy, warning that the steps may result in “significant tracking deviations” to its benchmark.

On 16 April 2020, USO announced it intends to invest approximately 80% of its portfolio in front-month contracts, and 20% of its portfolio in next-month contracts. Just five days later, it abandoned the strategy, announcing that it will invest in futures contracts “in any month available or in varying percentages” and “without further disclosure”. USO can also now invest in non-crude oil futures investments.

With the recent tweak, USO now holds roughly 25% of its portfolio in the June contract, 50% in the July contract, 15% in the August contract, and 10% in September (Table 2). This is in contrast to its previous strategy of holding just front-month contracts, which is now June.

Table 2: Underlying holdings of the USO

|

Security |

Quantity |

Price |

Market Value |

|

WTI CRUDE FUTURE Jul20 |

76,436 |

21.22 |

$1,621,971,920 |

|

WTI CRUDE FUTURE Aug20 |

29,924 |

23.86 |

$713,986,640 |

|

X4 WTI CRUDE FUTURE JUN20 |

30,000 |

16.94 |

$508,200,000 |

|

WTI CRUDE FUTURE Sep20 |

13,939 |

25.71 |

$358,371,690 |

|

WTI CRUDE FUTURE Jun20 |

13,743 |

16.94 |

$232,806,420 |

|

X4 WTI CRUDE FUTURE JUL20 |

7,725 |

21.22 |

$163,924,500 |

|

Source: USCF Investments Data as of 24 April 2020 |

|||

This is a significant departure from USO’s original investment objective of reflecting the daily percentage changes in the spot price of crude oil. It is no longer a passive fund, but an actively managed fund that has the flexibility to invest in crude oil futures contracts in any month, as well as contracts for other petroleum-based fuels, and derivatives on those futures contracts.

Moreover, the record inflows to USO has created another massive problem for the fund – it has run out of registered shares. As a result, USO has temporarily suspended new unit creations. While USO has applied to the US Securities and Exchange Commission (SEC) for permission to register an additional four billion shares, it has not been cleared by the SEC.

Until then, USO will trade on the exchange like a closed-end fund, with investors competing with each other for a limited pool of USO units. Already, this has caused USO’s price to detach from its net asset value (NAV), with its share price currently at a 5.7% premium to its NAV. When the four billion shares are approved by the SEC, it is likely that USO’s share price will come down to be in line with its underlying holdings.

Forget about USO, buy these ETFs instead

Not all oil ETFs are created equal.

In light of the structural issues faced by USO, we believe it is no longer the best ETF to gain exposure to crude oil prices. Investors betting on an oil price rebound should steer clear of USO, and consider other alternatives like the United States 12 Month Oil Fund LP (NYSE:USL) and the Invesco DB Oil Fund (NYSE:DBO).

The United States 12 Month Oil Fund LP (NYSE:USL), offered by the same company as USO, adopts a different strategy compared to the USO. Instead of simply holding the front-month futures contracts, USL holds equal positions in each of the next 12 months’ futures contracts (Table 3). While USL is also subjected to roll costs, it only rolls 1/12 of its contracts every month. As such, USL is more diversified across a wider time period, minimising the roll costs associated with contango.

Table 3: Underlying holdings of the USL

|

Security |

Quantity |

Price |

Market Value |

|

WTI CRUDE FUTURE May21 |

728 |

31.17 |

$22,691,760.00 |

|

WTI CRUDE FUTURE Apr21 |

728 |

30.72 |

$22,364,160.00 |

|

WTI CRUDE FUTURE Mar21 |

728 |

30.26 |

$22,029,280.00 |

|

WTI CRUDE FUTURE Feb21 |

728 |

29.74 |

$21,650,720.00 |

|

WTI CRUDE FUTURE Jan21 |

728 |

29.13 |

$21,206,640.00 |

|

WTI CRUDE FUTURE Dec20 |

728 |

28.47 |

$20,726,160.00 |

|

WTI CRUDE FUTURE Nov20 |

728 |

27.67 |

$20,143,760.00 |

|

WTI CRUDE FUTURE Oct20 |

728 |

26.77 |

$19,488,560.00 |

|

WTI CRUDE FUTURE Sep20 |

728 |

25.71 |

$18,716,880.00 |

|

WTI CRUDE FUTURE Aug20 |

729 |

23.86 |

$17,393,940.00 |

|

WTI CRUDE FUTURE Jul20 |

728 |

21.22 |

$15,448,160.00 |

|

WTI CRUDE FUTURE Jun20 |

728 |

16.94 |

$12,332,320.00 |

|

Source: USCF Investments Data as of 24 April 2020 |

|||

The Invesco DB Oil Fund (NYSE:DBO) is also a viable alternative for investors betting on an oil price rebound. The structure of DBO is starkly different from both the USO and USL. Instead of rolling its futures contracts on a predetermined schedules, DBO utilises a rules-based approach that is intended to minimise roll costs in contango. As a result of this strategy, DBO currently owns only one type of contract, the February 2021 contract.

Table 4: Comparison between USO, USL, and DBO

|

USO |

USL |

DBO |

|

|

Assets (USD mil) |

3,600.0 |

234.2 |

385.8 |

|

Premium To NAV (%) |

5.74 |

0.68 |

1.52 |

|

Expense Ratio (%) |

0.72 |

0.79 |

0.78 |

|

90-Day Average Volume (mil) |

93.5 |

0.3 |

1.6 |

|

Source: Bloomberg Finance L.P. Data as of 24 April 2020 |

|||

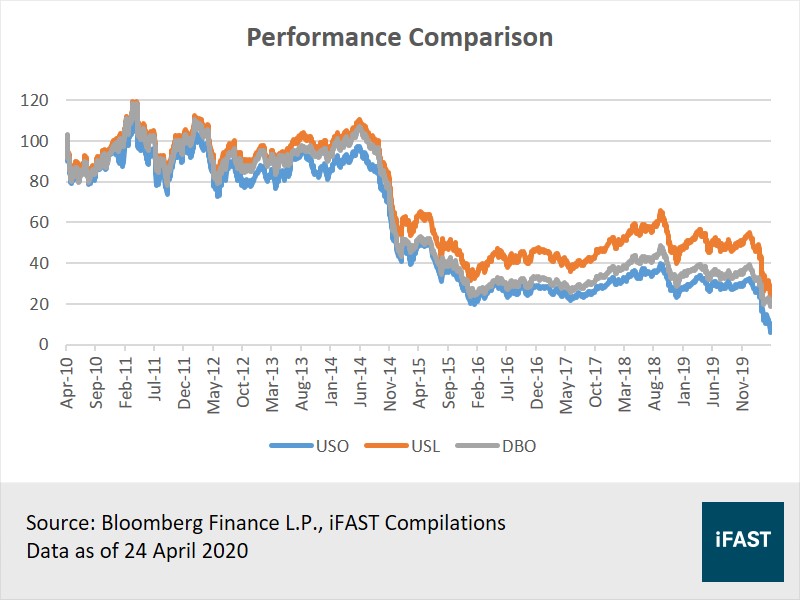

In terms of performance, both USL and DBO have also been outperforming the USO. On a year-to-date basis, the USL and DBO delivered returns of -55.0% and -50.0% respectively, much better than the -79.9% return delivered by the USO. While DBO has delivered better returns than USL in the short-term, the USL outshines the DBO if we assess their performances over a longer time period (Chart 4).

Both USL and DBO are viable alternatives to USO, but whichever you choose, don’t choose USO.

Chart 4: Performance comparison between USO, USL, and DBO

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report has a position in United States 12 Month Oil Fund LP.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.