This is a translated and edited version of a Chinese article published earlier on fundsupermart.com.hk on 28 Jun 19.

China Evergrande Group (“Evergrande”) is a name many investors are familiar with. As the leading property developer in China, Evergrande naturally has larger funding needs. The group has launched a number of giant USD bond sales in the past, earning itself the “king of debt” title. In this article, we will explore which Evergrande bonds are worth investing in.

Highlights:

- Contracted sales growth has slowed, but still on track to achieve annual contracted sales target.

- Slight increase in leverage, but credit risk remains at relatively low level.

- Short-term bonds looking very attractive.

Key credit considerations

Slowdown in 2019 sales

Evergrande’s contracted sales grew 10.1% YoY to RMB 551.43 billion in 2018. In terms of attributable contracted sales, the group’s operating scale ranks first in China’s property sector.

Full-year revenue grew 49.9% YoY to RMB 466.2 billion in 2018. Supported by low land cost, net profit grew 106.4% to RMB 72.21 billion, which is the highest in the property sector.

Evergrande’s core profitability is also growing stronger each year, with its growth rate surpassing the industry’s average. In 2016, 2017, and 2018, Evergrande’s net profit margins were 8.3%, 11.9%, and 14.3% respectively.

However, China’s property market entered a new period of adjustment from the start of 2H18. The housing market cooldown even led to China Vanke’s unveiling a new slogan, “to survive”. At the current juncture, the housing market is still facing tough times, and a decline in sales for large developers seems likely. Evergrande was not spared from the sector headwinds.

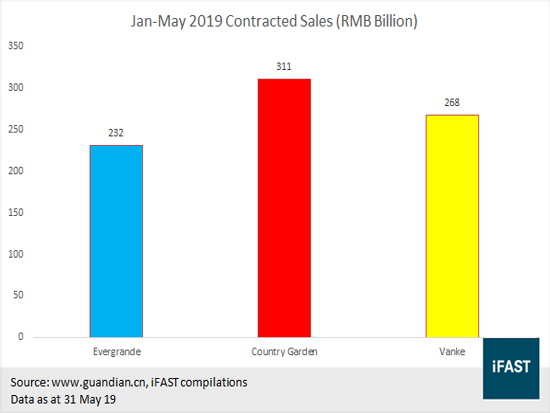

Figure 1:

As can be seen from Figure 1, Evergrande’s overall performance in the first five months of 2019 was disappointing. Cumulative contracted sales declined 8.9% YoY to RMB 231.5 billion over the period, falling behind Country Garden and China Vanke. Based on the group’s contracted sales target of RMB 600 billion set at the beginning of the year, Evergrande achieved 38.6% of its target through May.

China’s housing market recovered briefly in early March, but the short resurgence faded entering April. In addition, there has been a lack of positive developments in the industry, as the Chinese government is still maintaining tight policy controls on the property market. However, based on past data, contracted sales are expected to rebound in the second half of the year as Chinese developers usually focus their efforts on driving second-half sales. Therefore, we believe there is still a chance for Evergrande to achieve its annual contracted sales target.

Rebound in leverage

After indicating their concerns over the group’s elevated indebtedness a few years ago, management has begun to deleverage actively starting in 2017. For instance, Evergrande redeemed approximately RMB 110 billion worth of perpetual notes in 1H17, which reduced its net debt-to-equity ratio from 432.2% in 2016 to 240.4% in 1H17.

Evergrande’s deleveraging efforts achieved notable results. With no offshore USD bonds issued in 1H18, the group’s net debt-to-equity ratio improved further to 158.0%.

However, when the property market took a turn for the worse in 2H18, the group became increasingly strapped for cash, and had to start issuing offshore USD bonds again in October 2018. As shown in Figure 2, we note that Evergrande’s major credit metrics deteriorated in 2H18, with its interest coverage most notably declining by 52.2%.

Figure 2:

| Credit Metrics | 2H18 | 1H18 |

|---|---|---|

| Current Ratio | 1.36x | 1.48x |

| Quick Ratio | 0.14x | 0.19x |

| Interest Coverage | 1.44x | 3.01x |

| Net Debt-to-Equity Ratio | 1.76x | 1.58x |

| Source: Company, iFAST estimates | ||

Good access to capital markets

Despite the decline in Evergrande’s credit metrics, the group has faced little difficulty in raising capital. Take for instance the debt market, based on the information we gathered, Evergrande has issued a total of USD 6.2 billion of offshore bonds and RMB 31.0 billion of onshore bonds this year (see Figure 3). The group’s issuance volume is far higher than other industry peers, living up to its reputation as the king of debt.

Moreover, new bonds issued by Evergrande are usually well received by the market, with almost all the new issues recording oversubscriptions of multiple times. Therefore, considering the reputation and size of Evergrande, we believe that it is relatively easy for the group to tap capital markets for funding. As the group has the ability to pay off its existing debt by issuing new bonds and borrowing from banks, the likelihood of it running into a credit shock is low.

Figure 3:

| Offshore USD Bonds | Onshore RMB Bonds | |||||

|---|---|---|---|---|---|---|

| Date | Issue Size | Coupon Rate | Date | Issue Size | Coupon Rate1 | |

| 23-Jan-19 | 1.1 bil | 7.00% | 21-May-19 | 20.0 bil | 6.40% | |

| 23-Jan-19 | 0.875 bil | 6.25% | 24-May-19 | 11.0 bil2 | Pending | |

| 23-Jan-19 | 1.025 bil | 8.25% | ||||

| 08-Apr-19 | 1.25 bil | 9.50% | ||||

| 08-Apr-19 | 0.45 bil | 10.00% | ||||

| 08-Apr-19 | 0.3 bil | 10.50% | ||||

| 15-Apr-19 | 0.2 bil | 9.50% | ||||

| 15-Apr-19 | 0.4 bil | 10.00% | ||||

| 15-Apr-19 | 0.4 bil | 10.50% | ||||

| 21-May-19 | 0.2 bil | 8.90% | ||||

| Total | 6.2 bil | 31.0 bil | ||||

| Source: Bloomberg, Company, Shanghai Stock Exchange, Shenzen Stock Exchange; data as at 26 Jun 19. Notes: 1) Weighted average coupon rate; 2) Issuance application has been accepted, but the notes are not issued yet. |

||||||

Which bonds are worth considering?

Below is a selected list of bonds issued by Evergrande that are available on the iFAST platforms.

Figure 4:

| Bonds | Remaining Years to Maturity | Net YTM |

|---|---|---|

| EVERRE 7.000% 23MAR2020 CORP (USD) | 0.74 | 5.0% |

| EVERRE 6.250% 28JUN2021 CORP (USD) | 2.00 | 7.9% |

| EVERRE 8.250% 23MAR2022 CORP (USD) | 2.74 | 9.4% |

| EVERRE 9.500% 11APR2022 CORP (USD) | 2.79 | 9.5% |

| EVERRE 10.000% 11APR2023 CORP (USD) | 3.79 | 10.6% |

| EVERRE 7.500% 28JUN2023 CORP (USD) | 4.00 | 10.5% |

| EVERRE 9.500% 29MAR2024 CORP (USD) | 4.76 | 10.8% |

| EVERRE 10.500% 11APR2024 CORP (USD) | 4.80 | 11.0% |

| EVERRE 8.750% 28JUN2025 CORP (USD) | 6.01 | 11.2% |

| Source: iFAST; data as at 25 Jun 19 | ||

With a total of nine Evergrande bonds available on the platform, how should investors go about picking the right ones to invest in? We think there are two major aspects to consider.

Firstly, investor should consider the investment period. Generally, the longer the investment period, the greater the uncertainty in an issuer’s credit and operating conditions, and hence the potential risk is higher. Bonds with shorter maturities are consequently a better choice for most ordinary investors. We think investors can consider the notes that have remaining maturity less than three years, which are the first four bonds listed above.

Secondly, investors should consider whether the yield to maturity is reasonable. For example, although the 2021 bond has an investment period that is 1.3 years longer as compared to the 2020 bond, the former is able to provide a yield pick-up of almost three percentage points (“ppt”). Therefore, we think that the bond maturing in 2020 is less attractive.

On the other hand, the increase in yields relative to their longer tenor for bonds maturing after April 2023, are lower. For example, the bond maturing in April 2023 has a 1-year longer investment period as compared to the bond maturing in April 2022, but it can only offer incremental yield of around one ppt.

We note that the Evergrande curve is inverted between the April 2023 and June 2023 maturities—the EVERRE 7.5% ‘23s have a marginally lower yield (-0.1 ppt) despite their two-month longer maturity. All in all, our view is that the Evergrande bonds maturing in June 2021, March 2022, and April 2022 have relatively reasonable yields and stronger investment appeal.

It is worth mentioning that the EVERRE 8.25% ‘22s are available on Bond Express, where accredited investors can purchase the notes in sizes from as little as USD5,000.

Conclusion

Macroeconomic and sector factors have undoubtedly weighed on Evergrande’s growth, leading to a deterioration in its credit profile. However, as a company that is too big to fail, Evergrande’s condition is fairly stable and its bonds are still worthy of investors’ consideration.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) has a principal position in EVERRE 8.250% 23Mar2022 Corp (USD) and EVERRE 7.500% 28Jun2023 Corp (USD). The analyst(s) who produced this report holds a NIL position in the abovementioned securities.