Key Points

- We like and continue to recommend QNMSP 10Jul2028 Corp (SGD) for investors with a higher risk appetite. The bond is trading at an attractive yield of 3.80%, one of the higher-yielding short-term SGD bonds at the time of this publication.

- Q&M reported a 60% YoY decline in net income due to a one-off non-cash expense in loss from consolidation. However, core dental operations remain consistent, growing 3.5% YoY in 1H25.

- Q&M’s acquisition of Aoxin Q&M, its China arm, was largely credit neutral in our view. Despite reporting a net loss in 1H25 driven mainly by one-off non-cash items, we see the business to continue contributing modestly to the group’s operating cash flow.

- Q&M’s credit profile remains stable since our issuance article. Consistent operational cashflow and undrawn lines of credit mitigate near-term liquidity risk, although credit metrics are expected to initially worsen following the issuance of their recent bond.

Established in 1996, Q&M Dental Group (“Q&M”) is one of the largest private dental groups in Singapore, with additional presence in Malaysia and China. As of 30th June 2025, the Group operates 108 dental outlets, 5 medical outlets, a dental college, and a dental equipment distribution company in Singapore. Its Malaysia operations include 37 dental outlets and a distribution company, while in China it runs 7 dental polyclinics, a dental hospital, a training center, a distribution company, and a dental laboratory. Q&M also owns EM2AI, an artificial intelligence platform designed to support dental services. Q&M reports revenue in two main operating segments as described below.

· Core dental business comprising dentistry and distribution of dental supplies and equipment.

· Other businesses comprising sale and distribution of Covid-19 test kits and provision of laboratory testing, family medicine, aesthetic services and others.

Related article: Q&M Dental Group announces new 3Y SGD Senior Notes at an IPG of 4.35%. | FSMOne Singapore

Q&M Financial Highlights

We think that the 1H25 financials results reflect stable operating performance from Q&M. These results were largely not surprising for us, as we mentioned in our issuance coverage article that we expect the quality dental service of Q&M to remain largely sticky and resilient.

Core dental revenues held firm, sustaining consistent growth momentum.

As of 30th June 2025 (“1H325”), total revenues remained broadly stable, dipping slightly by 0.5% YoY to SGD 88.4m in 1H25 (1H24: SGD 88.8m). The decline was mainly attributable to non-core segments, due to the cessation of the Group’s medical laboratory business in September 2024 after the expiry of its clinical laboratory service license. Excluding this impact, core dental services revenue grew 3.5% YoY to SGD 87.2m in 1H25 (1H24: SGD 84.2m), driven by the consolidation of Aoxin (their Chinese arm), which transitioned from an equity-accounted associate to a subsidiary in 1H25.

When observing over a longer timeframe (Charts 1 & 2), we can see that Q&M’s total revenues remain largely stable and resilient, with Singapore and core dental services being largely the main drivers of long-term revenue. 2021 is noted to be a special year with a 50% YoY increase in revenues, largely due to the Covid-19 lab testing revenues witnessed (part of other revenue), which have since started winding down.Chart 1: Singapore remains largely the main driver of

revenue by geography.

Chart 2: Core dental services have always remained a key to Q&M’s topline. M&A serves as catalyst for growth (limited downside).

Adjusted earnings indicate resilient operational cashflows

Reported EBITDA fell 30.0% YoY to SGD 16.3m in 1H25 (1H24: SGD 23.3m), mainly due to a swing in net other gains/losses from a SGD 1.8m gain in 1H24 to a SGD 4.4m loss in 1H25; management attributed this to the non-cash loss on consolidation of Aoxin as subsidiaries, which we view as a largely one-off impact, with underlying operating performance remaining relatively stable. When adjusting for these one-off losses, adjusted EBITDA only fell by 4.4% YoY to SGD 20.1m (1H24: SGD 21.5m) from the drop in non-core revenues.

Similarly, 1H25 reported profit after tax declined 60.1% YoY to SGD 4.0m (1H24: SGD 8.3m), mainly due to the losses arising from the consolidation of the Aoxin, as well as a new SGD 1.1m expense from exchange differences related to Aoxin’s business in China. Excluding these largely one-off impacts, adjusted profit net of tax would have risen slightly by 1.6% YoY to SGD 8.4m (1H24: SGD 8.3m), reflecting a more stable underlying performance.

Bold M&A strategy to fuel expansion for core dental business

Q&M continues to expand its clinic network, operating 108 dental outlets in Singapore as of 1H25, up from 106 in FY24. Q&M has consistently turned to M&A as a key growth driver, expanding its network from 77 clinics in 2015 to 159 today. This growth aligns with management’s daring M&A-driven strategy to scale significantly in the coming years. Beyond Singapore, the group is actively pursuing regional opportunities, particularly in the Johor-Singapore Special Economic Zone, supported by the upcoming Rapid Transit System (“RTS”).

Management is also evaluating strategies to mitigate the potential outflow of patients to Johor, where cost advantages from currency exchange may become more attractive once the RTS is expected to commence operations in December 2026. Looking ahead, we anticipate Q&M’s core dental revenues to trend modestly higher, with M&A-led clinic expansion and the full-year contribution from Aoxin partly offset by some patient diversion from Singapore to Johor after the RTS launch.

Earnings are expected to stabilize and a successful M&A strategy can be a potential catalyst in the coming years

We expect that the coming years for Q&M will be marked with stable earnings growth, anchored by core dental business. We view the company’s M&A strategy as a catalyst for stronger earnings which should offset higher finance costs from their recent bond issuance. Although M&A-driven expansion may not always provide the most reliable earnings growth, we take additional comfort in Q&M’s case given the existence of profit guarantees on some acquisitions. These arrangements require vendors or subsidiary/associate shareholders to compensate Q&M for any shortfalls against the guaranteed profit levels, thereby offering some downside protection in the event of underperforming acquisitions. That said, investors should be mindful that Q&M may not always realize this profit guarantee income if the relevant guarantors lack the financial capacity to fulfill their obligations.

For their Chinese business, after Aoxin’s acquisition, we do not think it will be a drag on earnings but rather expect earnings contribution to mediate over the coming years with the newfound dormancy of their loss-making associate, resulting in weak but positive earnings.

Aoxin Q&M ("Aoxin") acquisition and effect on Q&M

On 30th April 2025, Q&M acquired an additional 17.2% stake in its Chinese arm, Aoxin, raising its total interest to 52.65%. This transaction resulted in Aoxin being reclassified from an associate to a subsidiary, thereby requiring full consolidation of their financial statements. Moving forward, Q&M will report its financials on a consolidated basis across Singapore, Malaysia, and China.

The reclassification triggered a one-off non-cash loss of SGD 4.4m to Q&M, recognized as “loss on consolidation of associate to subsidiary.” Despite the loss, the acquisition provided Q&M with a net cash inflow of SGD 9.9m, as Q&M now has access to Aoxin’s cash balance due to the consolidation.|

Aoxin Financials |

Units |

2022 |

2023 |

2024 |

1H 2024 |

1H 2025 |

|

Revenue |

SGDm |

25.0 |

31.7 |

32.9 |

14.9 |

15.5 |

|

Net profit |

SGDm |

(12.1) |

(8.5) |

(0.3) |

0.9 |

0.5 |

|

Net profit (adjusted)* |

SGDm |

(1.6) |

0.1 |

2.2 |

0.4 |

0.4 |

|

Cashflow from operations |

SGDm |

2.9 |

3.2 |

5.4 |

1.9 |

(0.0) |

|

Total debt |

SGDm |

0.3 |

0.2 |

0.1 |

0.1 |

0.0 |

|

Total cash |

SGDm |

7.1 |

9.2 |

12.5 |

12.5 |

12.0 |

|

Source: Company filings * Adjusted net income removes the losses / gains of share of results from associates and impairment losses on associates |

||||||

Historically, most of Aoxin’s negative results stemmed from non-cash items such as depreciation, impairment losses on associates, and share of results of associates. This explains why its net cash flow from operating activities has remained largely positive, despite reporting negative net income. 1H25 cashflow from operations dropped to negative due to large working capital changes.

Looking ahead, we expect Aoxin’s net profit to recover gradually, albeit from a weak base. The key driver is the reduced drag from Acumen Diagnostics, previously Aoxin’s main associate contributing impairment losses and weak share of results. Management disclosed that Acumen will be “dormant” since 1H25 following the expiry of its lab license and cessation of its government contract. We view this as supportive for Aoxin’s profitability outlook, as the absence of further impairment charges and negative associate contributions should help moderate earnings volatility. When adjusting for associate-related losses, Aoxin’s historical adjusted net income is largely positive, though still modest.

From a group perspective, Aoxin remains relatively small, contributing on average approximately 20% and 10% of Q&M’s revenue and net profit respectively over the last few years. As such, we see the impact of the consolidation as broadly neutral for the group. From a credit standpoint, the acquisition provides limited incremental risk: the initial uplift from Aoxin’s cash balance will be offset by its still-weak earnings contribution. Importantly, Aoxin carries little to no debt, which means its consolidation does not materially alter Q&M’s overall debt profile.

Credit highlights

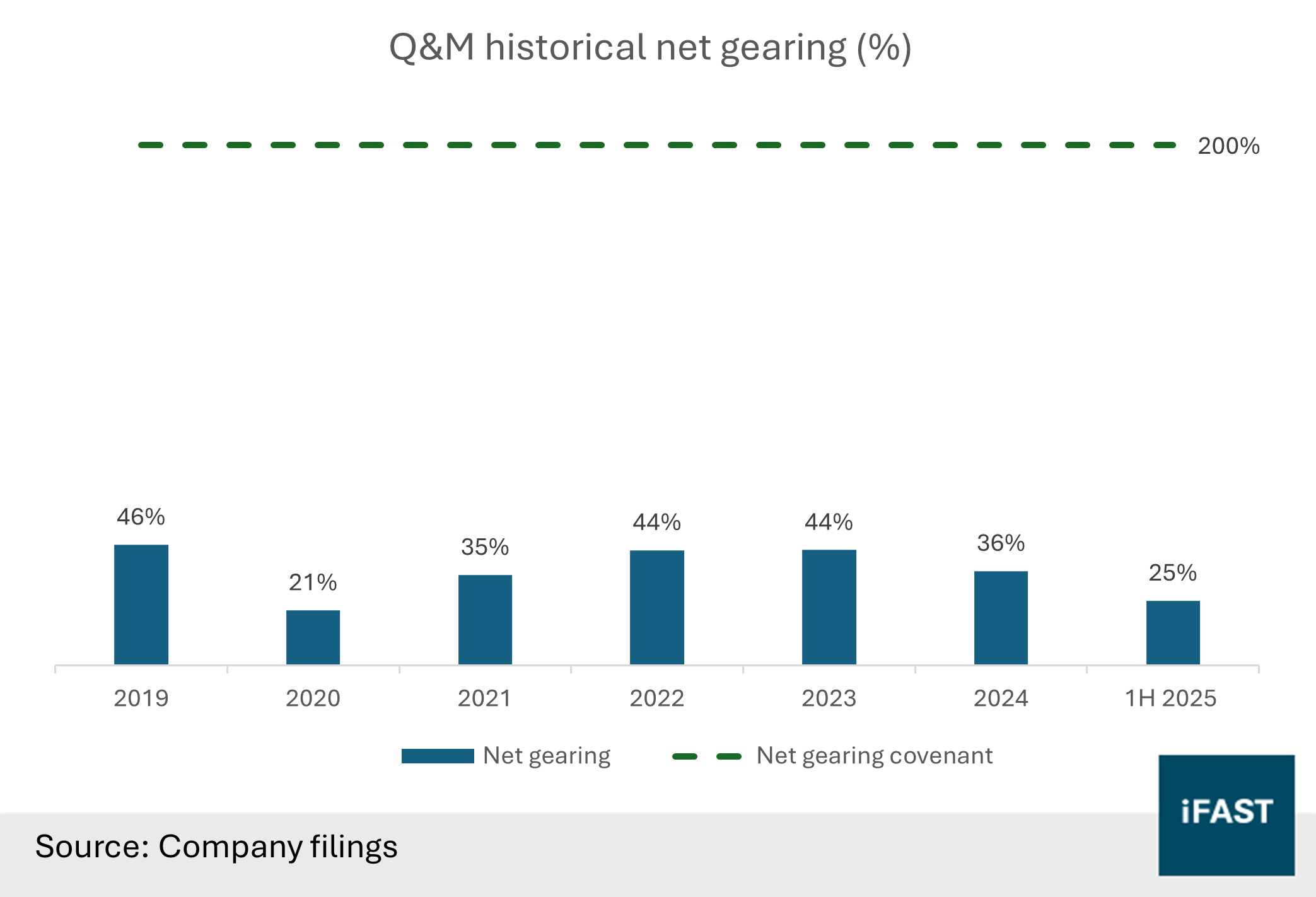

Q&M’s historical net gearing remains moderately leveraged, allowing for debt headroom post issuance.

Q&M’s credit profile remained broadly stable in 1H25, with total debt increasing by SGD 4.8m to SGD 78.5m in 1H25 (FY24: 73.7m). This increase was mainly due to the drawdown of a new SGD 5.0m term loan in 1H25 offset by slight debt principal repayments. As of 30th June 2025, Q&M has a short-term loan (payable in 1 year) balance of SGD 5.5m, approximately 7% of their total debt profile. The Group has also recently issued an outstanding SGD 130m 3-year SGD note which should raise total debt to SGD 208.5m post bond issuance.

1H25 net gearing (net debt / equity) improved to 25% (FY24: 36%), mostly due to the increase of non-controlling interests since the acquisition of Aoxin, increasing Q&M’s book equity. Historical net gearing shows a healthy buffer to the current 200% net gearing covenant that Q&M currently has (Chart 3). Adjusting for the recent debt issuance, net gearing ratio will be 128% assuming that all cash proceeds from the issuance are earmarked for M&A as per management and that book equity remains at 1H25 levels. This is still considerably lower than the 200% covenant set out by the bond, allowing for an additional debt headroom of USD 91.7m (after the debt issuance) before reaching breaching the covenant.

Interest coverage ratio remains adequate, providing a healthy buffer to existing bond covenants

Q&M’s interest coverage ratio remained largely stable, slightly decreasing from 7.1x in FY24 to 6.2x in 1HFY25 (trailing twelve months) due to the decrease in overall EBITDA due to the one-off negative effects of the consolidation with Aoxin. 1H25 finance costs fell 13.3% YoY to SGD 2.3m (1H24: SGD 2.7m) which we believe is largely attributable to lower SG benchmark rates, as some of Q&M’s existing bank borrowings are on floating rate terms.

After accounting for the recent debt issuance (including the resulting increase in interest expenses from coupon payments, assuming 1H25 EBITDA remains unchanged), Q&M’s interest coverage ratio (“ICR”) will fall to 3.1x. Lower ICR will be expected moving forward given the increase in interest expense. Nevertheless, an ICR of 3.1x still reflects a reasonable ability to cover interest obligations. Compared to the current ICR covenant of 1.75x, there is still buffer for the Group to bear greater finance cost, which also gives us some level of comfort (Chart 4).

Chart 4: Interest coverage ratio remains above covenant levels with healthy buffer

Healthy operating cashflows and liquidity

Historically, Q&M has generated stable operating cashflows, with 1H25 net cashflow from operations at SGD 15.0m (FY24: SGD 17.3m) and a steady upward trajectory since 2022 (excluding the one-off Covid-19 testing windfall in 2021). Liquidity has also strengthened, with cash balances rising to SGD 47.1m in 1H25 from SGD 34.3m in FY24, largely due to the consolidation of Aoxin’s cash position.

In addition, the group retains access to an undrawn SGD 20m money market loan facility (as of 31st December 2024), which can be deployed for operating activities or debt servicing. With only SGD 5.5m in short-term debt as of June 2025, we view Q&M as well positioned to comfortably meet near-term debt commitments through a combination of recurring operational cash generation, a strengthened cash buffer, and available credit lines.

Credit profile is expected to largely deteriorate following the issuance of their bond, but comfort can still be derived from their 1H25 results.

We expect Q&M’s credit profile and debt metrics to weaken following their recent debt issuance. While we anticipate an initial softening of their credit profile, Q&M’s historically robust debt metrics, resilient dental cashflows, decent cash balance, and access to undrawn credit lines provide a solid foundation for debt servicing. Looking ahead, we expect credit metrics to gradually improve as the company deleverages and realizes growth from its M&A strategy.

Key risks

We would like to inform potential investors of Q&M of 2 key risks:

Near-term debt maturity: Although exact debt maturity profile was not disclosed in the 1H25 financials, we estimate that there is still a large portion of debt that is due for repayment within 5 years. We think that financing needs are manageable considering 1) strong cash position that Q&M currently has (1H25: SGD 47.1m), 2) the expected stable operating cashflows moving forward from their strong core dental services.

M&A risk: As mentioned above, high capital expenditures from future clinic acquisitions are expected, which could result in higher CAPEX expenditure and a decrease in overall cash outflow. However, some comfort can still be gleamed by the fact that Q&M sets up profit guarantees with their associates / other investments, ensuring some level of cash realization from their investments.

Bond recommendation

|

Issuance |

Issuer |

Ask Price |

Years to Call |

Yield to Maturity |

|

Q&M Dental Group |

100.38 |

2.89 |

3.80% |

|

|

Thomson Medical Group |

105.55 |

2.78 |

3.39% |

|

|

Singapore Medical Group |

105.35 |

4.26 |

2.16% |

|

|

Hotel Properties Limited |

101.40 |

2.78 |

3.23% |

|

|

Vertex Venture Holdings Ltd |

102.80 |

2.94 |

2.30% |

|

|

City Developments Limited |

104.85 |

3.45 |

2.30% |

Before the recent debt issuance, we note that Q&M credit profile is rather stable, remaining rather unlevered, with healthy debt ratios (Chart 3 & 4). Looking ahead, we expect some credit profile deterioration following the recent SGD 130m bond issuance (as seen from the pro-forma levels), though this should be partially offset by potentially stronger operating cash flows from ongoing regional M&A expansion. We see room for gradual deleveraging as the core dental business continues to grow. Overall, Q&M’s credit profile remains stable in 1H25.

With an yield of maturity for QNMSP currently at 3.80%, we view the bond as rather attractively priced amongst SGD unrated peers of similar tenor. However, we think the higher yield is justified and reflects the higher risks stemming from heightened near-term maturity schedule after the debt issuance. There are only a few healthcare SGD bond issuers - Thomson medical and Singapore Medical Group – which does not offer meaningful comparison. That said, amongst the three comparable healthcare SGD issuances (Table 1), Q&M’s 2028 SGD bonds offer a higher yield which again reflects the risk from near-term maturity schedule.

In conclusion, we recommend this bond for investors who are seeking a higher yielding SGD option and are comfortable with the near-term maturity and the aggressive M&A expansion plan set out by management.

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) hold a position in TMGSP 5.500% 31May2028 Corp (SGD) and QNMSP 3.950% 10Jul2028 Corp (SGD). The analyst who produced this report holds a NIL position in the abovementioned securities.

Our podcast series, Yield Hunters, is available on Spotify, iTunes Podcasts and Google Podcasts. We share our thoughts on new bond issues and hold discussions on the fixed income space. Listen to our latest episode below and follow us!

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.

Please note that only certain bond(s) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to FSM's prevailing policies and procedures. Please read our full disclaimers in the website.