- Asia ex-Japan and Emerging Market equities delivered solid gains in 1H25, as capital rotated out of the US for diversification. South Korea led the rally as the new presidency boosting investor optimism.

- Moving forward, heavyweights China and India are expected to continue benefiting from domestic policy support. China's growth narrative has become increasingly attractive, with structural risks receding.

- Taiwan and South Korea are expected to sustain growth, driven by strong AI chip demand. TSMC is expected to serve as Taiwan’s key bargaining chip in tariff negotiations, while South Korea’s stimulus is likely to take effect and improve economic conditions.

- As the US remains shaped by policy uncertainty and rising stagflation risks, we believe the appeal of Asia ex-Japan and EM equities will persist, underpinned by structural growth drivers and supportive macro catalysts.

- We have upgraded AxJ’s star rating from 2.5 “Neutral” to 3.0 “Attractive”, with a projected 21.8% upside by FY2027. EM also presents an upside potential of 18.1%.

Performance of Major Asian and EM Markets in 1H25

Asia-ex-Japan (AxJ) and Emerging Market (EM) equities returned to the spotlight in the first half of the year, as the appeal of US equities waned following the implementation of Trump’s tariff policies and a downgrade in US credit ratings. Capital rotated out of the US, while AxJ and EM markets saw increased investor positioning, supported by structural growth themes and favourable macro catalysts.

South Korea emerged as the top performer, driven by renewed investor confidence following the inauguration of President Lee Jae-myung. His leadership brought greater political stability and raised expectations for economic stimulus and corporate reform. Sentiment was further boosted by robust demand for AI technologies, lifting major index constituents such as SK Hynix and Samsung Electronics.

Chinese equities rallied early in the year, spurred by excitement over DeepSeek’s AI breakthroughs, which triggered a re-rating of China’s tech sector. Although gains were later tempered by steep tariffs, pro-growth government policies supporting the private sector helped sustain momentum, with Chinese equities rising 9.3% during the period.

Taiwan and India posted more modest gains. Taiwan’s equity market rose 2.1%, constrained by tariff concerns affecting chip demand and the sharp appreciation of the Taiwan dollar, which introduced financial volatility. India’s market remained flat, weighed down by foreign fund outflows, earnings downgrades, and weakness in the Indian rupee.

Overall, with most key individual markets ending in positive territory, AxJ and EM equities delivered solid gains of 6.8% and 7.5%, respectively. EM equities slightly outperformed, supported by attractive valuations in Latin America and the region’s relatively lower tariff exposure announced by President Trump in April (Figure 1, all returns in SGD terms, unless stated otherwise).

Figure 1: South Korea led the performance in 1H25

China and India benefited from stronger domestic growth tailwinds

China’s economy grew by 5.3% year-on-year in the first half of 2025, showcasing resilience amid persistent tariff headwinds. In response to external pressures, the government has pivoted toward a domestically driven growth model. This shift has been supported by stronger policy backing for the private sector, highlighted by measures such as the Private Economy Promotion Law. Positive signs of this transition are evident in the steady retail sales momentum, hovering around 5% in recent months, and a gradual pickup in Chinas’ domestic investment activity.

Moving forward, we expect supportive policy tailwinds to remain a key driver of growth, with a particular emphasis on the technology sector. The ongoing “Guo Bu” trade-in programme, with another CNY138 billion set to be launched in subsidies for goods in 2H25, will boost e-commerce platforms through increased sales volumes. At the same time, declining costs of AI model deployment and rising demand for AI infrastructure are contributing to stronger earnings among major internet companies. With improving market sentiment and sustained policy support, technology firms are well-positioned to sustain robust earnings growth.

We believe structural risks in China are gradually receding in this pro-growth environment. Reflecting our more constructive outlook, we upgraded China’s investment rating in June from 2.5 stars “Neutral” to 3.0 stars “Attractive”.

Related article: Upgrade China to 3.0 Stars 'Attractive' Rating Amid Private Sector Resurgence

Moving on to India, another major market within Asia and EM, it is also experiencing stronger policy-driven growth. Easing inflation provides room for further repo rate cuts, while continued policy support, such as income tax relief for middle-income households, is expected to boost consumption and credit growth.

With private consumption as its main growth engine and limited export dependence, India is better positioned than many regional peers to weather the impact of Trump-era tariff policies. Meanwhile, escalating trade tensions have catalysed India’s “Make in India” drive, leading to a wave of manufacturing relocation. Major global firms like Apple and Shein have expanded their operations in India, underscoring the country’s growing role in the global supply chain.

However, near-term risks persist. Geopolitical tensions, particularly military conflicts with Pakistan, will likely weigh on investment sentiment and consumer confidence. Persistent fiscal and current account deficits also continue to pressure the rupee, posing headwinds for foreign investor returns.

Nonetheless, the relatively weak equity momentum in 1H25 has enhanced risk-adjusted return prospects, creating more attractive entry points for the Indian equity market.

Related article: Indian equities set for a comeback

AI advancements remain a long-term growth driver for Taiwan and South Korea

While the risk of higher tariffs on semiconductors remains elevated, Taiwan’s economy is expected to remain relatively resilient in 2H25. TSMC’s dominance in advanced chips production (7nm and below), makes Taiwan critical to US’s AI ambition, giving it strong bargaining power in trade negotiations with the US. TSMC’s investment plan in wafer fabrication plants in Arizona may also serve as a strategic condition for securing tariff reductions or exemptions.

Beyond tariff concerns, digitalisation and the AI revolution continue to underpin Taiwan’s long-term economic and equity market growth. With AI chip demand outpacing supply and robust orders from major chip designers like Nvidia and Intel, TSMC has raised its 2025 revenue growth forecast from the mid-20% range to 30% in USD terms. The company's planned mass production of 2nm chips in 2H25 is also expected to be a major growth catalyst.

As TSMC remains the cornerstone of the TWSE Index and Taiwan’s strong technology ecosystem supported by key players like Hon Hai and MediaTek, we believe the recent share price consolidation presents an attractive entry point for long-term growth opportunities.

Related article: Taiwan Stock Market 2H25 Outlook: Can Taiwanese Stocks Break Through Tariff & FX Barriers?

Robust semiconductor demand is also set to benefit South Korea, another major chipmaking hub, with strong export momentum supported by surging demand for high-bandwidth memory (HBM) chips. US tariff risks and rising legacy memory chip output from China, South Korea remains well-positioned given SK Hynix’s clear leadership in the HBM segment. The company plans to increase its capital expenditure by 30% to KRW 29 trillion this year to meet surging demand from major chip designers. We also expect Samsung, another KOSPI heavyweight, to ramp up production capacity following internal R&D restructuring.

On the domestic front, we expect the positive economic impact to materialise in 2H25, supported by the recently approved KRW 31.8 trillion stimulus package aimed at reviving weak consumption and easing inflation, which allows room for further rate cuts. Corporate reform efforts, such as revisions to the Commercial Act, are also regaining attention to address the “Korean Discount” and improve market valuations. These developments should build on the sentiment-driven optimism seen in 1H25.

We view South Korea as a "New Asian Tiger," underpinned by its leadership in memory chips, favourable policy momentum, and rising fiscal stimulus. These factors collectively set the stage for stronger and more sustainable economic growth in the periods ahead.

Related article: Tariffs turn into opportunity: Potential upside for the South Korean market near 60%

Asia and EM present attractive investment opportunities

Looking ahead, tariffs will remain a key headwind for Asian and EM economies, particularly for China, which continues to face an elevated baseline tariff rate of 30%, and South Korea, which recently received tariff warning letters from President Trump. However, we believe these economies are increasingly well-positioned to cushion the impact through policy support and structural reforms.

Importantly, the long-term structural growth drivers of these major economies remain intact. China has adopted a more pro-growth policy stance while rapidly advancing in technological innovation. India is addressing its fiscal deficits and repositioning itself within global supply chains. Meanwhile, surging global demand for semiconductors continues to drive growth in Taiwan and South Korea, whose technological edge in chip manufacturing remains difficult to replicate in the near term.

While both Asia ex-Japan and Emerging Markets share similar heavyweight markets, Asian economies are better positioned to navigate current headwinds, supported by proactive policy measures and deepening regional integration. Trade momentum between ASEAN and China has remained robust, and we anticipate a further acceleration in intra-regional trade flows should global negotiations fail to reach consensus by 1 August.

In contrast, Latin America faces greater challenges due to its heavy trade reliance on the US. In the latest round of tariff actions, the US raised import duties on Brazil and Mexico to 50% and 30% respectively, posing a significant risk to the growth momentum.

From a valuation perspective, both markets remain attractive. Asia is trading at 13.6x forward P/E, above its long-term average of 12.9x, while EM stands at 12.9x, above its 12.7x historical average. Much of the tariff-related negative sentiment appears to be priced in, with recent negotiation progress suggesting more optimistic outcomes, particularly for markets like India and Taiwan, which may benefit from potential tariff reductions. However, EM could face further downside, dragged by steeper US tariffs on Latin American countries.

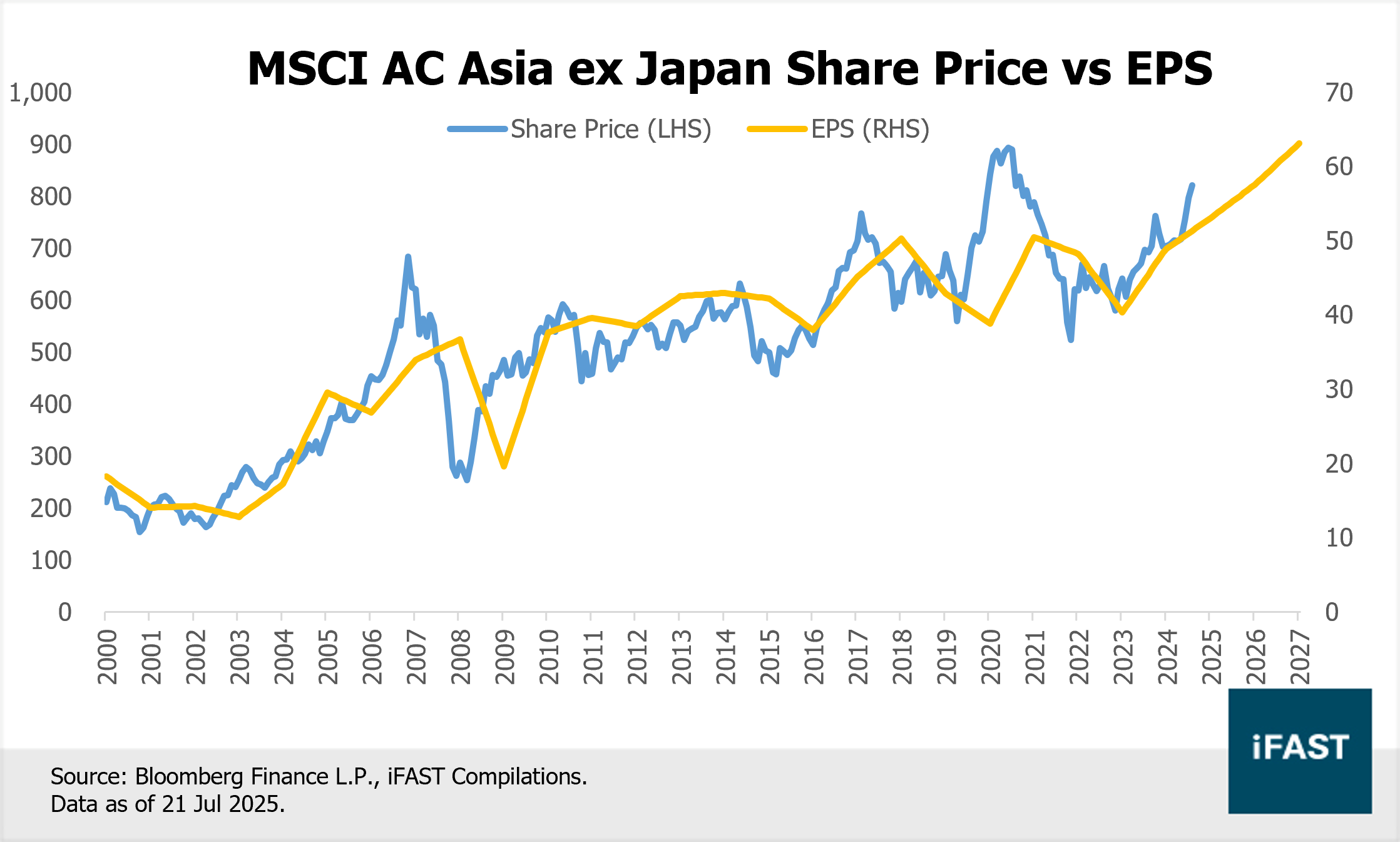

Applying a 13.5X fair PE ratio to the MSCI AC Asia ex-Japan Index and a 12.5X fair PE ratio to the MSCI Emerging Market Index, we estimate 21.8% upside for Asia and 18.1% upside for EM as of FY2027 (Tables 2 & 3). As a result, we upgrade Asia ex Japan’s rating from 2.5 stars “Neutral” to 3.0 stars “Attractive”, reflecting both attractive valuation upside and fundamental improvements, while maintaining our “Attractive” rating for EM.

As the US continues to be shaped by policy uncertainties and elevated risks of stagflation, capital is likely to continue rotating out of the US in search of diversification. Asia and EM are now supported by a more durable growth narrative and a range of macro catalysts. Investors may consider gaining exposure through regional funds and ETFs or through country-specific strategies. Ultimately, we believe 2025 is shaping up to be a year for Asia and EM to shine (Table 1).

Table 1: Recommended Products

Table 2: AxJ presents 21.8% upside as of FY2027

|

MSCI AC Asia ex Japan Index (MXASJ) |

2024 |

2025E |

2026E |

2027E |

|

PE Ratio (X) |

16.8 |

14.9 |

12.8 |

11.1 |

|

Earnings Per Share |

48.9 |

55.0 |

64.2 |

74.0 |

|

Earnings Growth |

18.7% |

12.4% |

16.7% |

15.2% |

|

Target Price (based on 13.5X fair PE ratio) |

1000 |

|||

|

Upside Potential |

21.8% |

|||

|

Source: iFAST Estimates. |

||||

Figure 2: Price vs EPS for the MSCI AC Asia ex Japan Index

Table 3: EM presents 18.1% upside as of FY2027

|

MSCI Emerging Market Index (MXEF) |

2024 |

2025E |

2026E |

2027E |

|

PE ratio (X) |

15.8 |

14.4 |

12.5 |

10.6 |

|

Earnings Per Share |

79.3 |

86.9 |

100.6 |

118.1 |

|

Earnings Growth |

11.7% |

9.6% |

15.8% |

17.4% |

|

Target Price (Based on 12.5X Fair PE ratio) |

1480 |

|||

|

Upside Potential |

18.1% |

|||

|

Source: iFAST Estimates. |

||||

Figure 3: Price vs EPS for the MSCI Emerging Market Index

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in iShares Core MSCI China ETF (HKEX.2801).

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.