BYD announced its first quarterly results for the year. Table 1 summarizes the key financial data performance.

Table 1: BYD's First Quarterly Results 2025

|

2025 Q1 (In RMB) |

Beat / Miss Consensus |

YoY Growth |

|

|

Revenue |

170.36B |

Miss |

36.3% |

|

EPS |

3.12 |

Beat |

98.7% |

|

Gross Margin |

20.07% |

Beat |

- |

|

Net Profit |

9.16B |

Beat |

100.4% |

|

Vehicle sold |

1,000,804 |

Miss |

59.8% |

|

Source: BYD, Bloomberg and iFAST Compilation Data as of 31 March 2025 |

|||

BYD's revenue and vehicle sales volume in the first quarter were slightly lower than expected due to the sluggish global consumer sentiment. Nevertheless, BYD maintained a 20% gross margin and more than doubled its net profit year-on-year thanks to the expansion and maturity of its EV production scale. We will analyze why BYD is still in a high growth phase.

1. Stable Gross Margin

BYD's approach to business expansion coincides with Tesla's. Both companies have been engaged in different vertical integration over the past 20 years to stabilize the supply chain and provide greater bargaining power. In March 2020, BYD spun off its four automotive core technology businesses into a separate company called “Verdi” and started to supply other new energy vehicle suppliers.

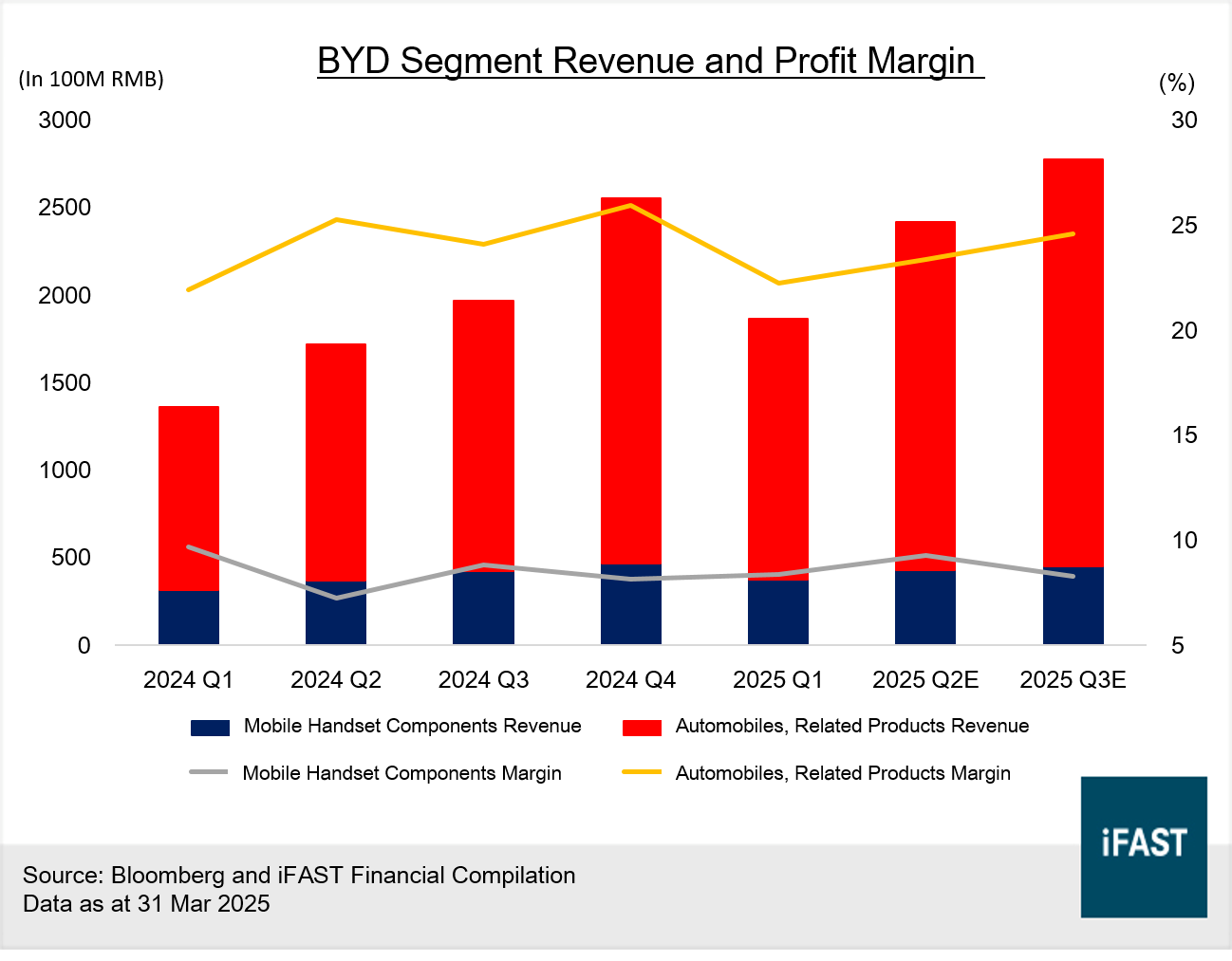

Currently, 80% of BYD's revenue comes from its automobile and related products business, and its gross profit margins, though declining this quarter, still managed to stay above 20%, which is the highest among other Chinese EV companies. In addition, BYD's acquisition of eAssurance, because car insurance is a necessity, BYD can use its own insurance company for bundled sales, and even through its car database to calculate the number of miles driven, the incidence of accidents, and other data, thus reducing the risk of the insurance company, optimizing costs, and increasing the gross profit margin of the business.

BYD announced its first quarterly results in mid-April, and Table 1 summarizes the key financial data performance.

Chart 1: BYD Segment Revenue and Profit Margin

The vertically integrated business has shielded BYD from China's price wars. Over the past year, BYD has taken the lead in drastically reducing the retail price of its vehicles to capture a share of the Chinese market, and other Chinese EV companies have been forced to follow suit. Since BYD develops and assembles most of its auto parts and batteries in-house, it has more control over costs. On the other hand, other automakers generally outsource parts and batteries to provide materials for vehicle manufacturing, making it difficult to adjust costs in a price-cutting war, and so they can only lose gross margins in exchange for orders.

Chart 2: Gross profit margins of major EV companies in China

The market has been comparing BYD to Tesla, and in terms of gross margins, BYD has led Tesla in gross margins since Q2 2023. In terms of overall business, Tesla has invested more profitably in new businesses and autonomous driving developments over the past two years, including the Optimus humanoid robot and Robotaxi. These businesses have not yet brought profitability to Tesla, and therefore have been a drag on the company's overall gross profit performance over the past two years.

Chart 3: Tesla and BYD Gross Profit Margins

2. BYD's “GOD'S EYE” Enjoys Economies of Scale

BYD mentioned in its February press conference that the “ GOD'S EYE ” will be applied to different car models in three levels, with the doorway below 100,000 RMB. The company's sales guidance for 2025 is expected to exceed 5 million vehicles, and the proportion of intelligent driving models will be increased from less than 5% to 80%, making autonomous driving more popular. With the rapid development of AI on the mainland, automotive companies are among the first to utilize AI. BYD cited the use of AI to train its smart-driving systems as a way to reduce costs significantly, allowing it to sell its latest smart-driving models at reduced prices while maintaining profits. BYD also announced that it will implement Deepseek into its existing “Xuanji Architecture” system, and that the “ GOD'S EYE ” system will be standardized on BYD's cars priced above RMB100,000. In the long run, we believe that mature intelligent driving technology will be the watershed for hundreds of electric vehicle companies in China. BYD's own user base is already ahead of other competing car brands, and the popularization of the “ GOD'S EYE ” system will enable the company to obtain free autonomous driving data from its users, which will in the future serve as a resource for the research and development of higher-level autonomous driving systems, thus increasing the overall gross profit margin.

However, at present, the computing chips used in the three levels of “ GOD'S EYE” still rely on NVIDIA's Orin-X and Orin-N, and the supply of the chips may be affected by the trade tariffs between China and the U.S. or the restrictions on the export of chips. BYD is actively developing its own chips to replace its reliance on NVIDIA, and under optimistic scenarios, the chips will be in mass production by 2026, which is expected to increase the overall gross profit of automobiles.

3. Overseas growth has become a bright spot

Apart from winning in the mainland market, BYD's overseas target is in full swing. In the first 4 months, BYD's overseas sales steadily accounted for 20% of the total EV sales, with a cumulative total of over 200,000 units. This year, the management has mentioned that the overseas sales target is 800,000 units, and the market is optimistic that the target will be achieved after the release of the first-quarter results.

BYD has been realizing its “going overseas” blueprint since its early years, and one of the blueprints is to build factories locally. Currently, BYD has nine overseas factories, including the Brazilian, Thai, Uzbek and Indian factories, which have already commenced production. With these four factories operating at full capacity, the annual production capacity will exceed 600,000 units. Southeast Asia and Europe are the main regions that BYD wants to capture. In addition to saving time and cost for transportation, BYD has also localized the configuration of its plants in different regions through the feedback from local employees. For example, taking into account the fact that road surfaces in Thailand are usually more prone to dents and damages, BYD has enhanced the shock absorption function of its Thai models.

In addition, BYD has set up a specialized ocean-going fleet, and has already invested in four roll-on/roll-off transport vessels. A ship can transport 9,200 cars at a time, four a round trip, you can transport 36,800. In total, BYD has ordered eight such vessels, and with the delivery of the vessels, the capacity will continue to increase.

To maximize profitability and future growth, BYD acquired Hedin Electric Mobility, a subsidiary of its German distributor Hedin, which distributes automobiles and parts in the German market, to strengthen its pricing and supply capabilities in the European market, another vertical merger and acquisition, which we expect will help BYD on its way to the sea in the future.

Chart 4: BYD's Overseas Sales Share

Chart 5: BYD's Overseas and Local Sales YoY Growth

4. Advanced Supercharging Technology

With BYD aiming to charge faster than fuel, the popularity of high-voltage platforms could accelerate significantly as BYD's newly announced Super e platform, with its 1,000V all-area high-voltage architecture and up to 1,000kW of charging power, intensifies the competition for charging speed and efficiency. With most competitors still using 400V architectures, there is an urgent need to upgrade to 800V architectures to remain competitive, especially in the mid-to-high end EV segment.

Currently, electric vehicles based on the 800V platform from Krypton, Xiaopeng and Ideal Auto have a range of 400 kilometers on a 10-minute charge, which is still longer than BYD's five-minute charge, so BYD's improved charging configuration may encourage more fuel owners to switch to a new vehicle, which is expected to increase its competitiveness.

Investment Insight

Overall, BYD has risen to the top of the electric vehicle industry over the past 20 years, and its vertically integrated development model has enabled the company to build a strong moat and maintain its gross profit margin at over 20%. As an outstanding automobile manufacturer, BYD has not only designed a wide range of models to meet the needs of different consumers, but also rapidly popularized its intelligent driving technology in its affordable cars. Therefore, based on the above development trend and analysis, we believe BYD's future potential is very attractive.

Based on a Fair PE of 26x, BYD's share price has a potential upside of 57.0% by the end of 2027.

Table 2: BYD's EPS and Potential Upside

|

BYD(1211.HK) |

2024 |

2025E |

2026E |

2027E |

|

EPS |

4.61 |

6.16 |

7.42 |

8.50 |

|

Earnings Growth |

34.1% |

33.6% |

20.5% |

14.5% |

|

PE (x) |

30.5x |

22.8x |

19.0x |

16.6x |

|

Target Price (based on fair PE of 26x) |

221 |

|||

|

Potential Upside |

57.0% |

|||

|

Source: BYD, Bloomberg and iFAST Compilation Data as of 11 June 2025 |

||||

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.