(Edited on 16 Apr 2025.)

The BNY Mellon Global Short-Dated High Yield Bond Fund has a strong track record with top-quartile performances compared to its peer group over multiple time horizons1. Investors looking for a best-in-class fund within the high-yield space with an annualised dividend yield of 5% should read on below!

1. High-yield bonds are typically associated with higher risks. What are your thoughts on this characterisation?

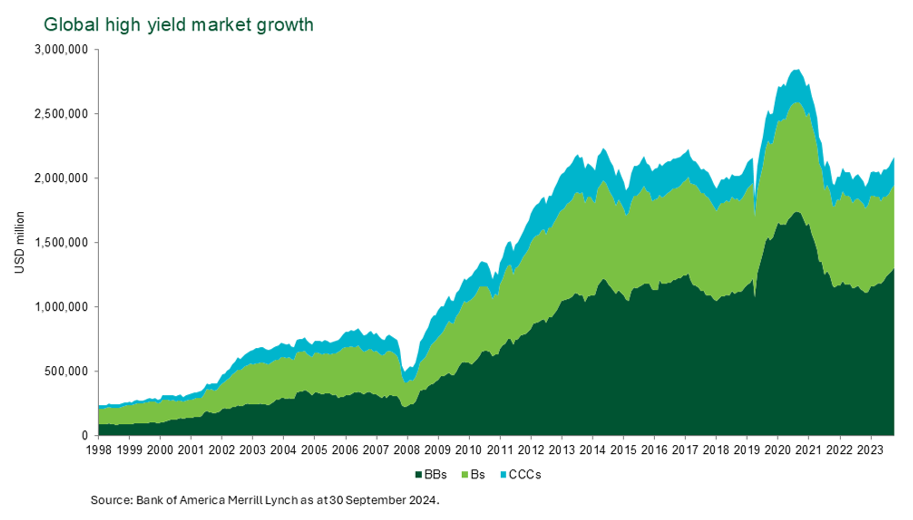

In our view, this association is completely out of date. Decades ago, high yield was associated with the term ‘junk bonds’ and that term stuck, but credit markets have changed dramatically. The credit quality of the global high yield market has been gradually improving over time while the credit quality of the investment grade market has deteriorated. For example, in Europe, 66% of the market was rated BB at the end of 2024, the best rating category for high yield, while in the US, over 50% of the market held this rating2. A decade ago, the average credit rating for both these markets was single B. Meanwhile, investment grade credit has gravitated towards the lowest BBB category.

Across a range of credit metrics – ratings, total debt/EBITDA (leverage), and EBITDA/Interest expense (interest coverage) – credit quality has markedly improved. This has translated into lower defaults and the expectation that defaults will remain low. The average rolling 12-month default rate for US high yield has been 3.4% over the past 25 years, and post-global financial crisis, it has been 2.5%. At the end of 2024, the default rate stood at just 1.5% for the US and 1.8% globally, both well below the long-term average. This reinforces our view that global high markets are significantly more resilient than in the past.

These underlying changes have significantly increased the appeal of the asset class to institutional investors. A decade ago, the high yield market was dominated by retail investors, which increased the volatility of the market. Today, a significant proportion of the investor base is institutional, many of which have dedicated long-term allocations to high yield, contributing to a more stable investment environment.

2. How does your short-dated high-yield strategy differ from a regular high-yield strategy?

Within our global short-dated high yield strategy we specifically aim to target issues which we believe will be repaid within a two-year time horizon. That provides a huge amount of discipline into what we do with a far greater focus on short-term cashflows than many other high yield strategies.

Ideally, the companies in which we invest are seeking to enhance their business in some way; this can take the form of selling an asset, buying a competitor, or undertaking capital investment such as building a factory or plant. This activity will lead to an increase in the amount of cash generated by the company, either via increased revenue streams or from the proceeds of a sale, which can be used by the company to repay its debt, or to refinance its debt on more attractive terms.

Once we have identified a potential target for investment, regular contact with management follows to ensure the plan is progressing as expected. We would normally identify four to five key stages over the two-year period which need to be met for us to be confident that we will be repaid on time. If it becomes clear that the plan is deviating from the expected timeline, we sell the issue. A sale in this situation is generally straightforward, as the original business plan is generally still in place, just delayed or not meeting our prudent timelines.

We also follow other simple rules to make our process even more robust. We avoid companies with a short track record or that are asset-light. We also don’t believe that CCC-rated issues offer a yield premium sufficient to compensate for higher default risk, so we generally avoid them. An exception to this is the subordinated debt of higher-rated issuers, where the default risk is that of the higher-rated BB or B-rated company.

Our focus on visible cashflows and the monitoring we undertake means we expect to avoid defaults under normal market conditions, allowing our clients to fully enjoy the yields available in the asset class. It has been over a decade since the strategy has faced a default within its holdings.

3. How does BNY Investments approach credit selection?

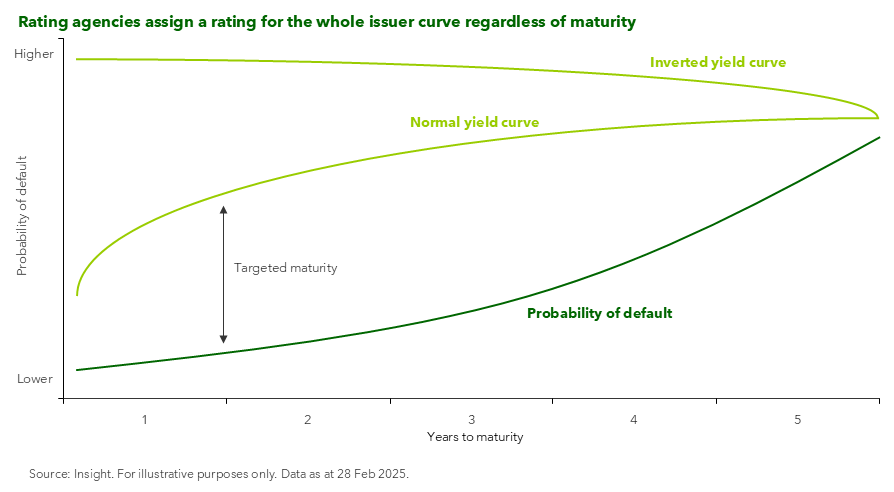

Like any labelling of a group of strategies, the detail is important. Some short-dated high yield strategies are constrained by maturity, others are constrained by currency, and some by index. Our constraint is focused entirely on the timing of the repayment of principal within two years. This imposes a discipline on analysts and portfolio managers to not only have a solid assessment of the credit today, but also a detailed financial model for how the business will perform over the two-year investment horizon.

Our analysts meet with the companies we invest in up to six times a year, checking progress versus the detailed assumptions made at the time of investing. If any deviation from the plan is highlighted, the investment thesis is reassessed, and the position sold if the repayment plan comes into doubt.

This strict investment and sell discipline reduces the margin for error. We cannot sit and wait for a turnaround in the story that may take us beyond the two-year horizon. We believe this discipline reduces portfolio risk and volatility.

The strategy’s global mandate gives us the flexibility to take advantage of opportunities in both major high yield markets. We believe being global and not following an index provides another important and relevant attraction; we do not have to own what we do not like.

4. The fund has a large allocation to Europe – why?

We invest globally, but Europe has a lot of attractions for high yield investors. The European Central Bank can be more confident about meeting its inflation target than the Fed, so we believe rate cuts are more certain in the eurozone than in the US. This should provide more of an anchor to bond markets, especially in shorter maturities. The fiscal backdrop is also much healthier, with most European economies running much smaller deficits than the US government.

There are many idiosyncratic opportunities as well, with countries such as Spain and Italy significantly benefiting from policies introduced during the pandemic when joint euro-government bonds were issued to modernise and derisk these economies. We’re now seeing plans being put forward in Germany which will allow a significant increase in spending for infrastructure and defence. We expect this to provide a rich target environment for our analyst teams to pinpoint investments that fit our requirements.

5. What are your favourite themes and sectors within the fund?

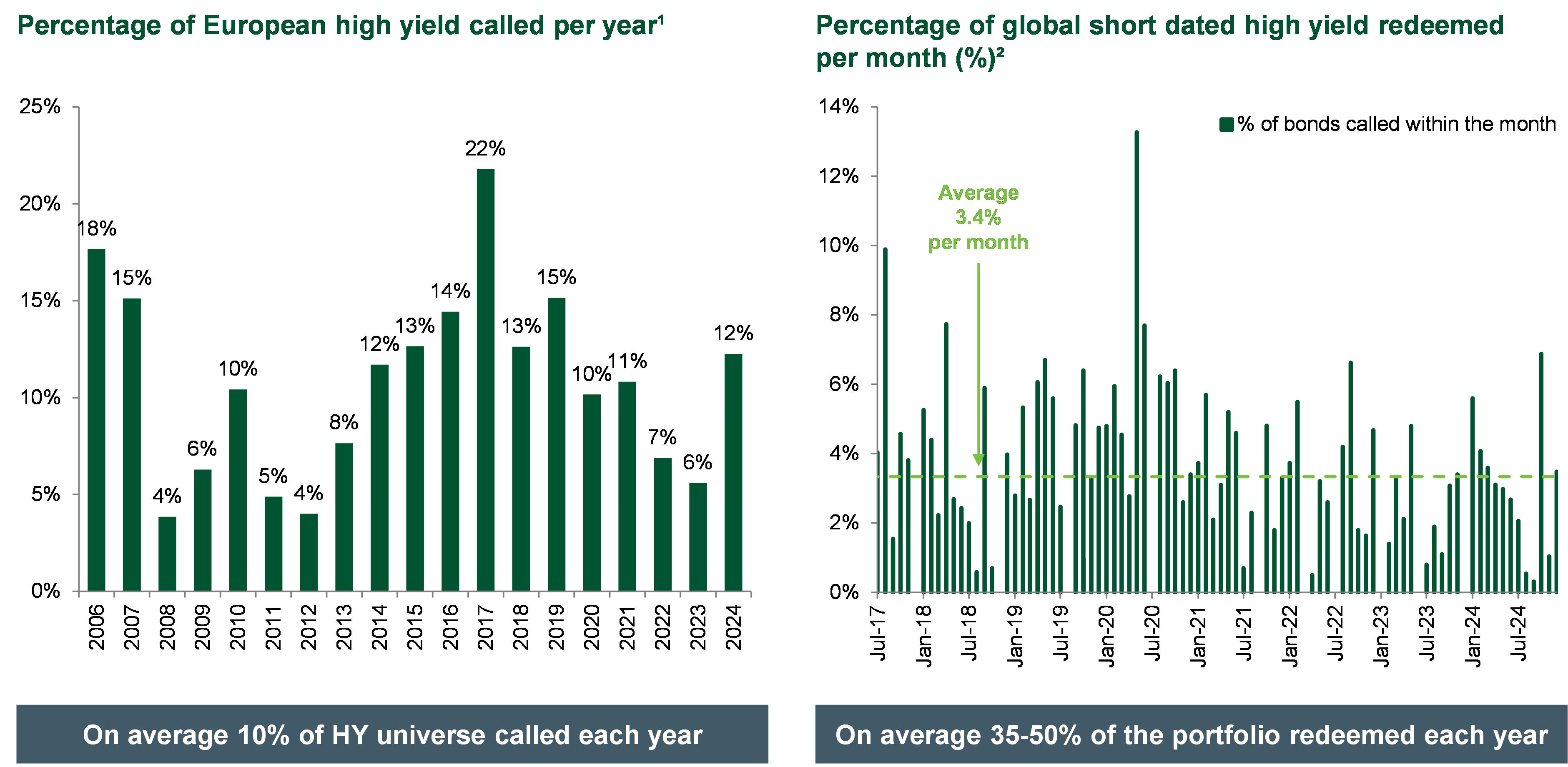

One theme we are seeking to take full advantage of is the level of refinancing activity taking place, which comes with a huge benefit to investors in the form of call premiums.

Many high yield bonds have structures which allow the issuer to redeem the issue at set future dates before the final maturity. This is very different to the investment grade market where bonds generally have a single maturity date. These redeemable dates are known as call dates, and generally an issuer has to pay a price above 100 to redeem or ‘call’ the bond early. The earlier the call, the higher the price the issuer needs to pay, declining over time to 100 at final maturity. For example, a bond may mature in 2028 at 100 but be callable in 2026 at 102. Once markets expect a bond to be called, the price of the bond tends to gravitate towards the call price and the investor makes a gain in excess of market returns.

As the management teams of high yield companies generally prioritise growth, it often makes sense for them to refinance and lock in funding for a future period as they reach key milestones in their growth plan. The premium they pay to call the debt early is a small price to pay in this process but can be a significant benefit to investors.

The short-dated nature of Insight’s high yield strategy, combined with an investment process focused on visible cashflows, means we believe we are well positioned to exploit call premiums. This has resulted in a solid track record of investing in bonds that are refinanced, with around 35% to 50% of the investments in the strategy being called each year since its inception.

Source: Insight Investment. Data as of end-December 2024.

6. What is the track record of this fund? How are fund distributions determined?

The fund has a strong track record, generating top-quartile performance relative to its peer group over three, five and seven years1. In US dollar terms to the end of January 2025, our fund has generated a three-year annualised return of 7.4% gross of fees, over the benchmark's 4.1%3. From inception, our annualised return is 5.2%3 to the same date, but that obviously included a period when yields were extremely low.

Fund distributions are determined with an eye on the underlying yield of the fund. We aim to ensure that distributions on income classes of the fund are sustainable over the medium term, so not all of the income generated is paid out.

7. In short, what are three reasons why investors should consider your fund?

We think the current environment is extremely positive for high yield investors. Central banks are easing which should support growth, and earnings are generally coming in higher than expectations. Issuers have returned to markets in 2024 to tap into elevated levels of demand and this is presenting abundant opportunities to add new names and lock in high coupon levels for at least two years.

To provide three key reasons to consider our specific fund:

- The power of compounding: One of the most powerful tools for investors is the concept of compound returns. This is where returns earned on investments increase the capital of the investor, resulting in the exponential growth of their investments over time. Unless market rates change significantly, we believe our fund is extremely well suited to compounding returns over time. Our strong track record of avoiding defaults means our investors have been able to gain the full benefit of the yields available in the asset class, and we expect this to continue in the future.

- Increased cashflow visibility guards against uncertainty: In a time of macro and geopolitical uncertainty it is critical to have a deep understanding of the underlying cash generation within the businesses in which you invest. We believe that understanding and therefore predicting cashflows is easier on a short-term, two-year, basis than over longer time horizons. This gives us confidence that our approach should prove resilient even amidst all of the uncertainty we are currently seeing.

- Reduced volatility: The short duration nature of our fund makes it less rate and spread-sensitive than many other high yield funds, with returns generally dependent on the performance of individual companies. This is especially important for those concerned about the potential for longer maturity yields to rise.

1Peer Group = Morningstar, Global High Yield Bond category, 3, 5, & 7 year period, as of 28 February 2025.

2Source: Bank of America, as at 31 December 2024.

3As at 28 February 2025. BNY Mellon Global Short-Dated High Yield Bond Fund, USD W Acc share class, gross of fees. Benchmark: Cash Benchmark SOFR(90-day compounded). Fund inception date: 30 November 2016.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.