- China equities have surged over 10% YTD, as DeepSeek’s breakthrough AI model has reignited investor confidence in the tech sector. H-shares have outperformed A-shares due to their more attractive valuations.

- Economic challenges, such as deflationary pressures, persist, but the property sector is showing signs of moderation in sales and price declines. While the policies implemented last September were effective, the sector will require time to fully recover.

- Corporate profits have shown signs of recovery in the tech-centric sector, while additional consumption stimulus would likely benefit consumer discretionary first. The DeepSeek-driven rally may also spur tech giant collaboration, driving innovation and earnings growth.

- While China’s stock market has been largely lifted by sentiment, we believe it is heading in the right direction. We await more stimulus from the “Two Sessions” and greater support for the private sector, which could drive continued market growth.

- The share price of the MSCI China Index has surpassed our FY2026 target of HKD72.0, so we remain cautious about a near-term pullback. However, China is positioning itself in the right direction to be the dark horse market of the year.

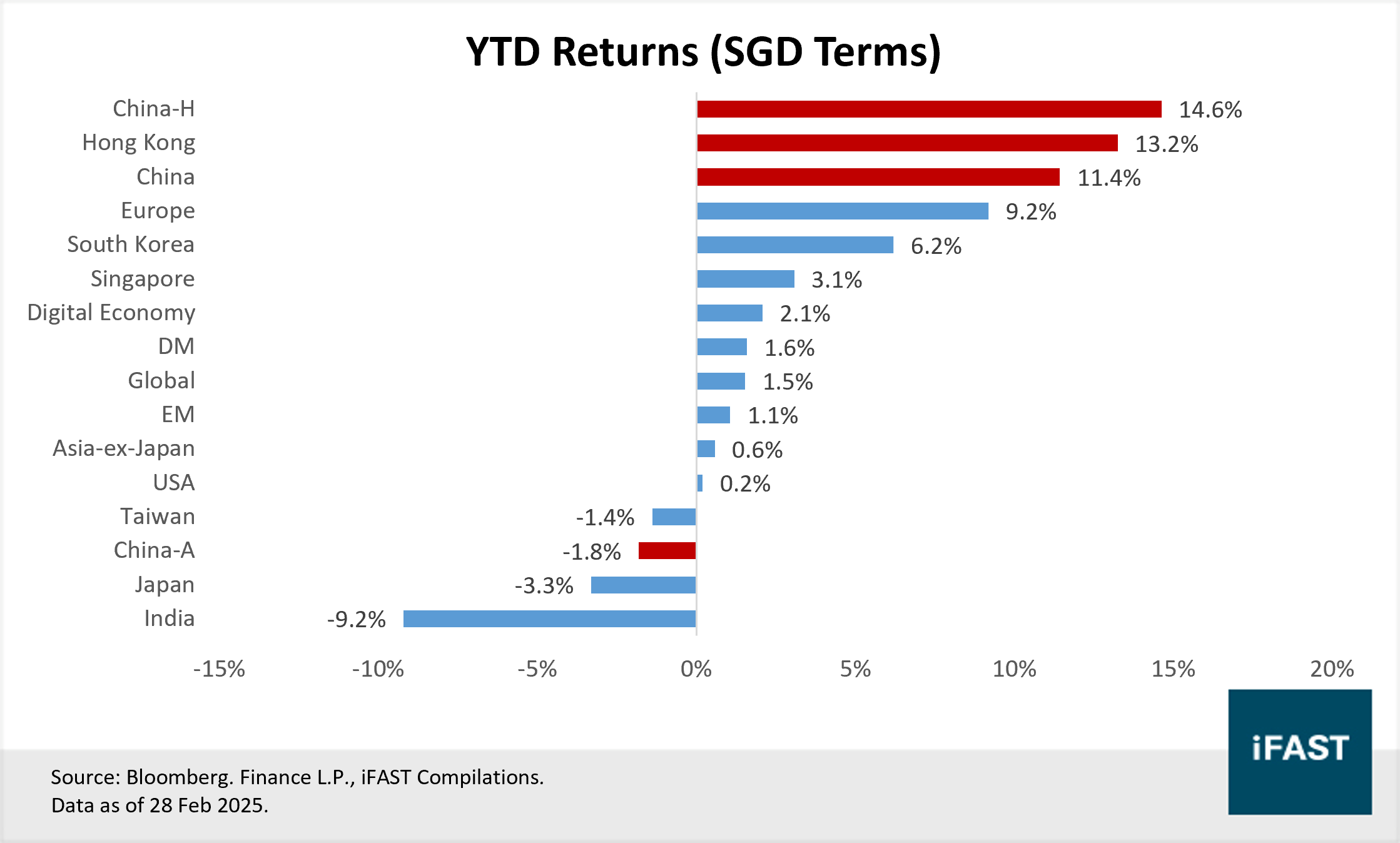

Chinese equities have shown exceptional momentum in 2025 year-to-date, driven by DeepSeek’s breakthrough AI model, which has reignited investor confidence in the country’s technology sector. As of 28 February 2025, China H-shares, Hong Kong equities, and the MSCI China Index—which represents broad China exposure—all posted returns exceeding 10%, making China the top-performing market within our coverage (Figure 1).

Figure 1: Chinese equities have been the best-performing market within our coverage

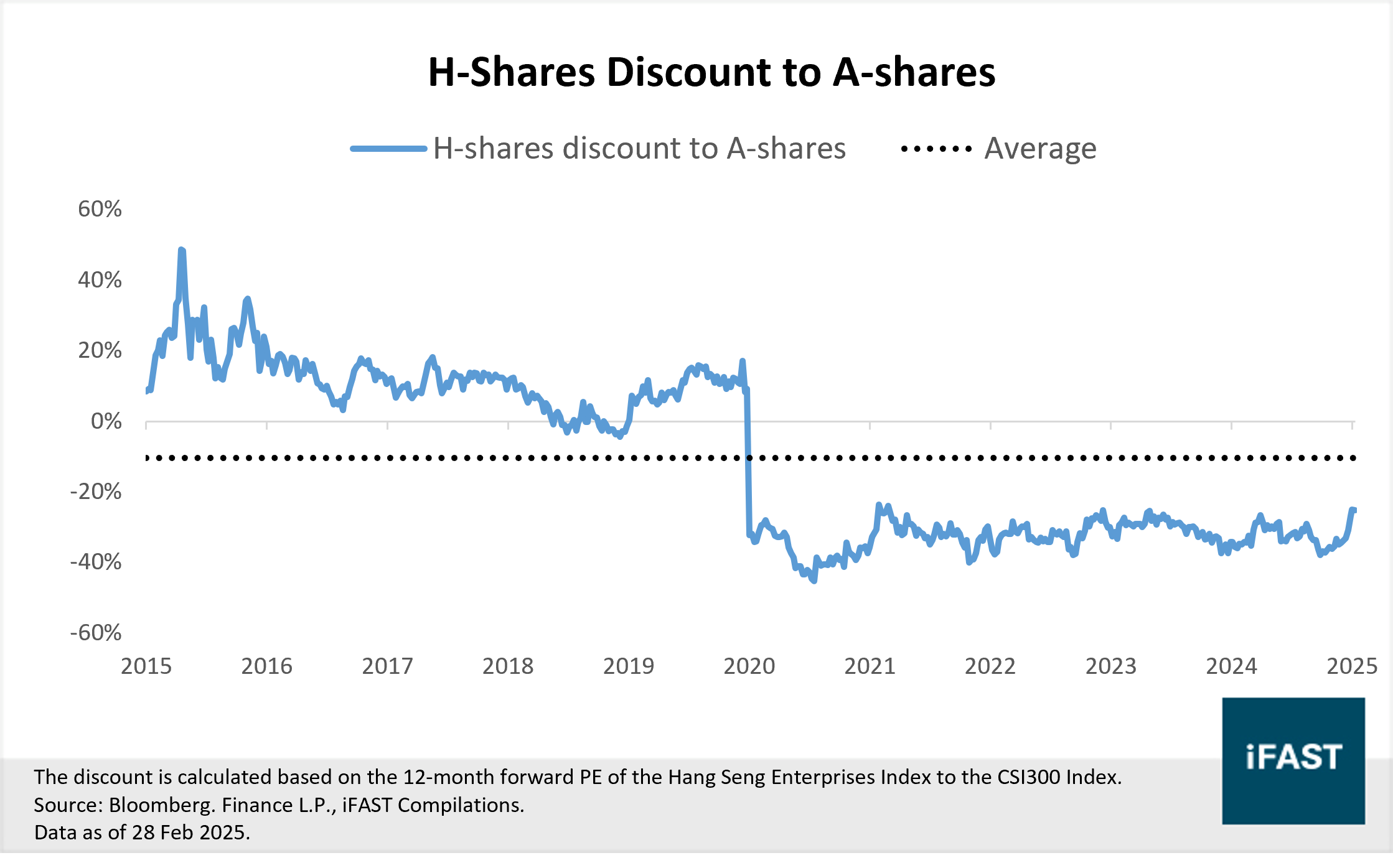

China H-shares Rallied On Valuation Discount

China H-shares have surged on a record buying spree, while A-shares have remained subdued, as investors seize on a wide valuation gap between the two markets. Since 2020, H-shares have consistently traded at a discount to A-shares, and as of the start of the year, their valuation was 33.3% lower than A-shares (Figure 2). The discrepancy has fuelled a wave of Southbound flows, with mainland investors funnelling HKD 152.8 billion into Hong Kong stocks in February - the highest monthly level since 2024.

Figure 2: Hong Kong stocks traded at more attractive valuations

The rally has not been driven by domestic investors alone, global capital is also playing a key role. Concerns over stretched valuations, weaker-than-expected corporate earnings, and the risk of reciprocal tariffs with the US have prompted foreign institutional investors to offload their Indian equity positions. With Chinese stocks trading at roughly half the valuation of their Indian counterparts, the reallocation of capital has become increasingly attractive, fuelling strong gains in Chinese markets through January and February 2025.

Riding the wave of AI enthusiasm, chipmakers Semiconductor Manufacturing International Corporation (SMIC) and Hua Hong Semiconductor emerged as standout performers among the most traded stocks in February, delivering impressive returns of 66.3% and 56.3%, respectively (Table 1). They are well-positioned to benefit from tightening US semiconductor export controls and the AI-driven surge fuelled by DeepSeek, as Chinese technology firms increasingly turn to domestic chip suppliers. Further adding to their appeal, both companies’ Hong Kong-listed shares trade at a significant discount to their A-share counterparts, presenting a compelling valuation gap with strong potential for capital appreciation.

Other notable gainers include Ubtech Robotics and Alibaba, both of which have delivered over 50% returns year to date. Ubtech’s stock gained traction, particularly after humanoid robots danced at this year’s Spring Festival Gala, showcasing the potential tasks these robots can perform. Meanwhile, Alibaba’s shares surged significantly, driven by stronger-than-expected net income of CNY 48.95 billion for the quarter ended 31 December 2024. Additionally, the company announced a collaboration with Apple to introduce AI-powered features in China, further reinforcing its AI-driven growth narrative.

Table 1: Top 10 Most Traded Southbound Stocks in February 2025, Ranked by Performance

| Ticker | Securities | Performance YTD (in SGD Terms) |

| 981 HK Equity | SMIC | 66.3% |

| 2013 HK Equity | Ubtech Robotics | 62.2% |

| 1347 HK Equity | Hua Hong Semi | 56.3% |

| 9988 HK Equity | Baba-W | 52.7% |

| 1810 HK Equity | Xiaomi-W | 48.3% |

| 1024 HK Equity | Kuaishou-W | 20.7% |

| 700 HK Equity | Tencent | 13.2% |

| 2800 HK Equity | Tracker Fund | 12.8% |

| 3690 HK Equity | Meituan-W | 5.4% |

| 941 HK Equity | China Mobile | 1.7% |

| Source: Bloomberg

Finance L.P., HK Exchange, iFAST Compilations. Performance data as of 28 Feb 2025. |

||

Persistent Economic Headwinds, but Signs of Progress Emerging

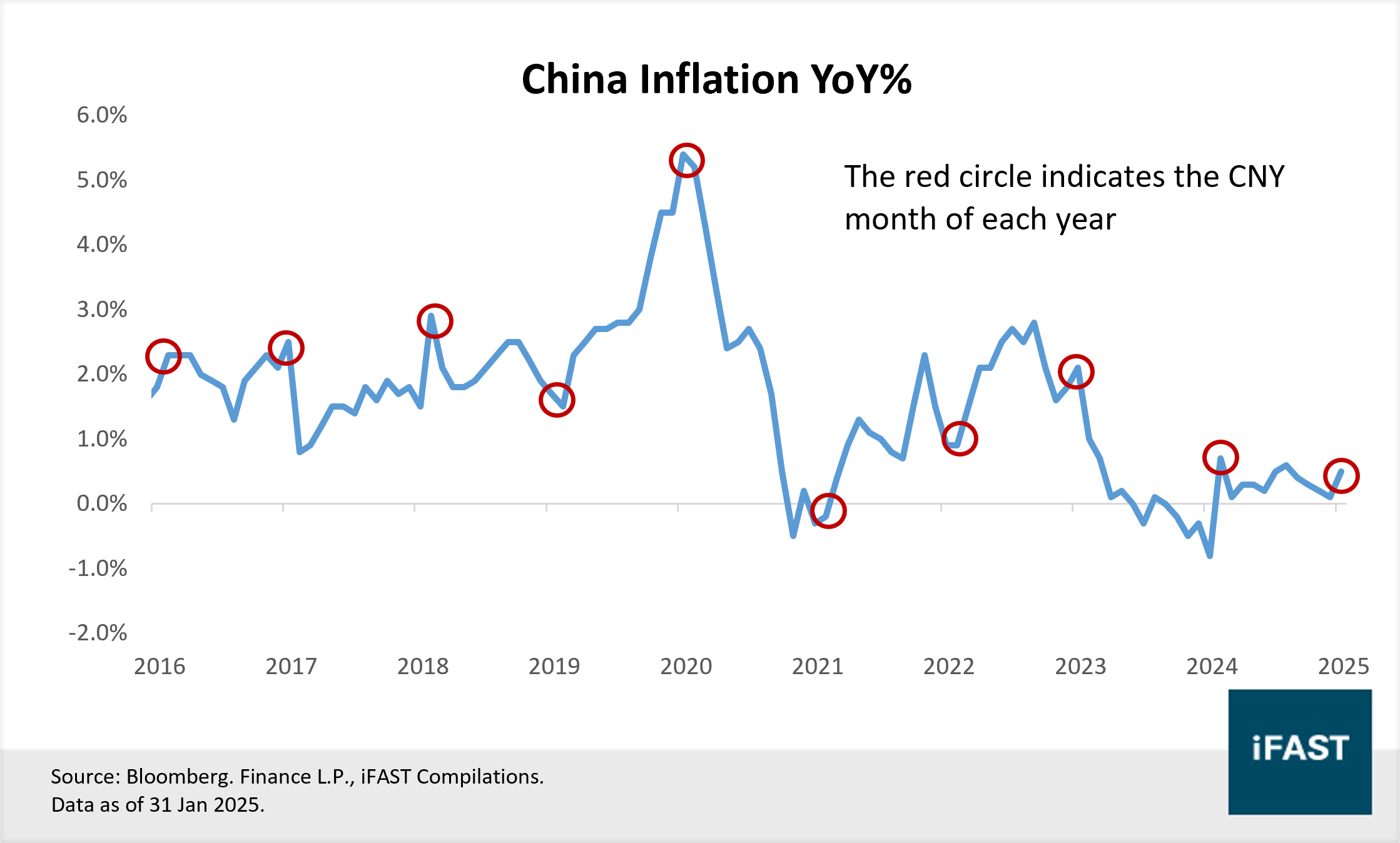

While improving sentiment has propelled Chinese equities higher, the broader economy continues to grapple with some challenges. Deflationary pressures remain a concern, with consumer prices edging up just 0.5% year-on-year in January - an increase largely attributed to seasonal demand during the Chinese New Year. This follows an anaemic 0.1% rise in December, underscoring weak underlying consumption. Historical patterns suggest that inflation typically spikes during the holiday season before tapering off in the subsequent months (Figure 3).

Figure 3: Inflation readings typically rise during the Chinese New Year period

In a bid to stimulate demand, Beijing has expanded its trade-in program to cover a wider range of home appliances this year. Consumers purchasing mobile phones, tablets, and smartwatches priced under CNY6,000 are now eligible for a 15% subsidy. We believe these discounts could encourage spending across a wider range of goods. However, based on last year’s track record, they appear less effective in reversing the broader deflationary trend. Ultimately, the program’s impact will depend on consumer confidence - a factor that remains fragile amid a weak employment outlook.

Although speculation arose in December 2024 about a possible CNY 500 monthly pay raise for public sector workers, no official confirmation has been given. Even if true, the measure is hard to have a significant effect. The public sector represents only a fraction of the workforce, and many civil servants endured multiple rounds of pay cuts in 2024 - leaving a modest wage increase unlikely to offset past reductions. With consumer spending still weak and confidence subdued, policy responses so far appear insufficient to reverse the broader consumption weakness.

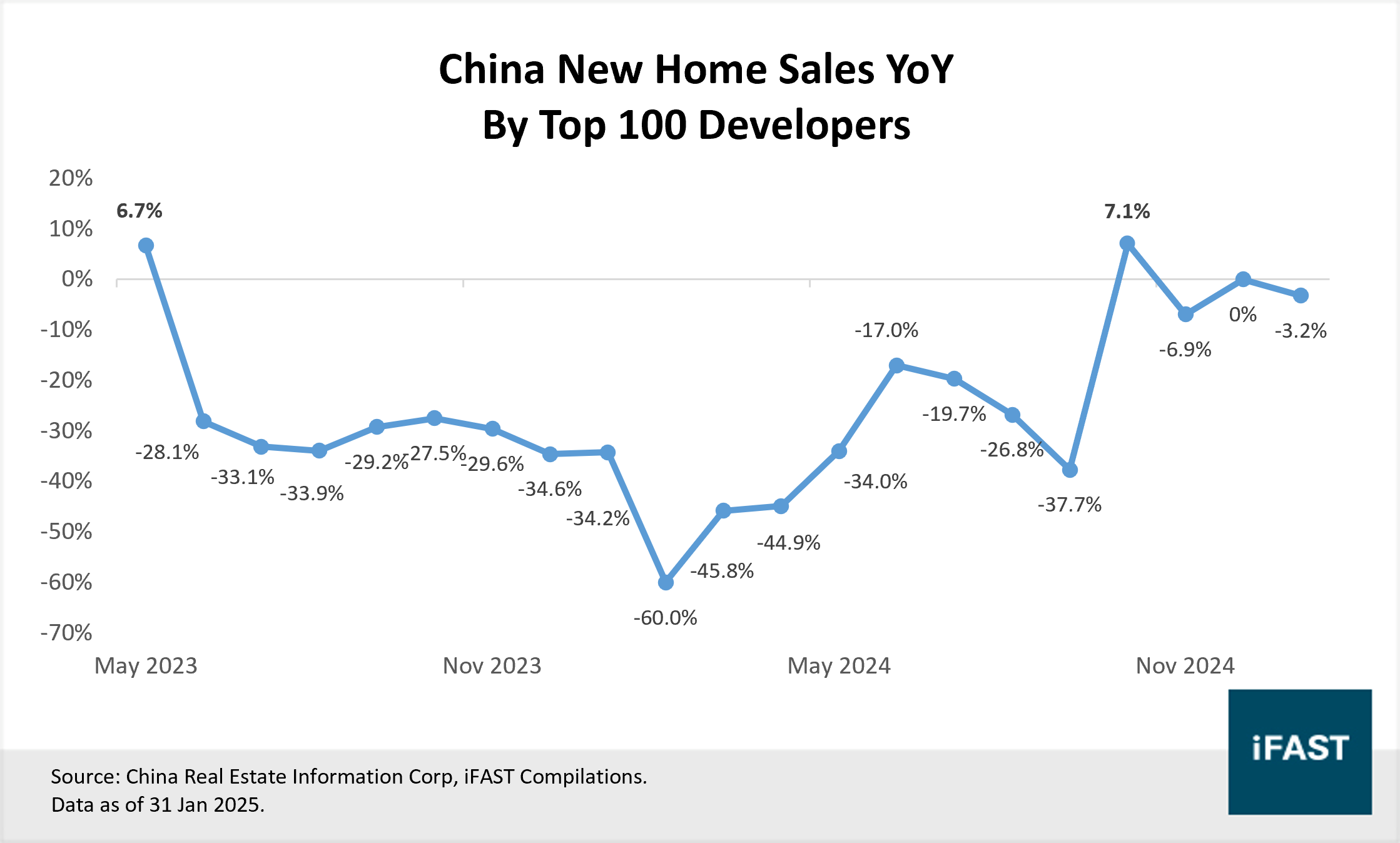

Unlike sluggish consumption, China’s property sector has shown signs of improvement following last year’s sweeping stimulus measures. New home sales by the country’s top 100 developers turned positive for the first time last October, rising 7.1% year-on-year - the first gain since May 2023. While sales have since resumed their decline, the pace has slowed to single digits (Figure 4). Sentiment towards the sector has generally improved. In January, new home prices across 70 cities fell by 5.0% year-on-year, the smallest decline since last July. Meanwhile, top-tier cities saw a 6.0% year-on-year increase in new home prices, according to the China Index Academy.

Figure 4: The decline in China's new home sales has slowed since last October

The narrowing sales declines and price stabilisation in major cities reinforce our view that the property market is trending towards stabilisation. While progress is evident, the property crisis will still take time to resolve. The prolonged property slump has strained liquidity for major developers, with the government recently stepping in to support Vanke amid liquidity pressures. In 2025, the sector will remain a drag on China’s economic growth.

Early Signs of Corporate Profit Recovery Emerging in Tech-centric Sectors

Latest corporate earnings are showing signs of improvement and could provide the next leg of support for China’s stock market rally. While EPS estimates for MSCI China stocks are still well below 2021 levels, they have been revised up by 2.3% YTD. Companies in the index have also begun reversing their streak of negative sales and EPS surprises for 4Q24 (Figure 5). Technology-centric companies from the information technology, consumer discretionary and communication sectors are generally seeing improvement in their fundamentals (Table 2).

Figure 5: China stocks are showing signs of earnings recovery

Table 2: Tech-centric sectors have generally delivered positive earnings surprises

|

Securities |

Actual EPS |

Consensus Estimates |

Surprise |

Sector |

|

Hithink Royalflush Informa |

2.18 |

0.83 |

162.7% |

Financials |

|

Lenovo Group Ltd |

0.05 |

0.03 |

86.2% |

Information Technology |

|

Tal Education Group |

0.06 |

0.04 |

53.8% |

Consumer Discretionary |

|

Baidu Inc |

19.18 |

14.13 |

35.8% |

Communication Services |

|

Netease Inc |

15.09 |

12.56 |

20.1% |

Communication Services |

|

Alibaba Group Holding Ltd |

21.39 |

19.12 |

11.9% |

Consumer Discretionary |

|

Bilibili Inc |

1.07 |

0.97 |

10.1% |

Communication Services |

|

Autohome Inc |

3.99 |

3.67 |

8.6% |

Communication Services |

|

Vipshop Holdings Ltd |

5.70 |

5.26 |

8.4% |

Consumer Discretionary |

|

Trip.Com Group Ltd |

4.35 |

4.20 |

3.6% |

Consumer Discretionary |

|

ACM Research Shanghai |

0.90 |

0.88 |

2.3% |

Information Technology |

|

Yum China Holdings Inc |

0.30 |

0.31 |

-3.5% |

Consumer Discretionary |

|

New Oriental Education & Tec |

0.22 |

0.26 |

-13.7% |

Consumer Discretionary |

|

ZTE Corp |

0.11 |

0.41 |

-73.4% |

Information Technology |

|

Beigene Ltd |

-0.11 |

-0.42 |

-73.7% |

Health Care |

|

Hua Hong Semiconductor Ltd |

-0.02 |

0.02 |

-188.2% |

Information Technology |

|

Beijing Oriental Yuhong |

-0.48 |

-0.16 |

-197.8% |

Materials |

|

Source: Bloomberg. Finance L.P., iFAST Compilations.

|

||||

Stronger performance in consumer discretionary and communication, which largely depend on consumer spending, points to a gradually warming economic environment in China. Once further policy measures supporting consumption come into play, the consumer discretionary sector - including companies like Alibaba, Meituan, and JD.com - stands to be among the first to benefit, strengthening their growth trajectory. Meanwhile, China’s AI sector is gaining traction, with DeepSeek’s emergence reinforcing the country’s technological capabilities. The AI boom has spurred high-profile collaborations, such as Apple partnering with Alibaba and Baidu to develop AI-driven features for the iPhone in China. These alliances are expected to drive innovation and generate new revenue streams for the country’s technology firms in the coming quarters and years.

For investors seeking earnings growth to support expanding valuations, we believe technology-centric sectors are beginning to provide that foundation. However, when looking beyond these sectors to the broader economy, a full valuation recovery may take time. Sectors tied to China’s struggling property market—such as materials and industrials—continue to lag, posing a challenge to overall market rebound.

China is progressing in the right direction

China’s stock market continues to surge amid growing optimism that "China is back." While sentiment has been a key driver of recent gains and the recovery remains uneven across sectors, both economic fundamentals and corporate earnings have started to show signs of progress. Overall, we believe China is moving in the right direction.

In our outlook article published in December, we highlighted China as a potential dark horse market this year, with that view hinging on two critical factors. The first is the need for additional near-term stimulus to support the ongoing real estate recovery and revive consumer spending. The durability of the current rally will be put to the test during the upcoming “Two Sessions” in early March. If policymakers could present a clear and credible roadmap for stimulating demand and reflating the economy, market sentiment could strengthen further, supported by improving fundamentals.

Beyond short-term stimulus, China’s shifting stance toward the private sector is another crucial factor that could position it as this year’s dark horse market. On 17 February 2025, President Xi held a symposium with high-profile entrepreneurs, notably featuring Alibaba founder Jack Ma, who had remained out of the spotlight since the regulatory crackdown in 2020. His reappearance sent a clear message: the Chinese government recognises the vital role of private enterprises in driving technological advancements and economic growth amid domestic economic weaknesses and rising geopolitical tensions —and is prepared to support them.

Related article: Chinese equities could be 2025’s dark horse, but here’s what needs to happen

The recent signs of government support are encouraging. If concrete policies—such as enhanced funding access, regulatory easing, and stronger legal protections for private businesses—materialise in the coming weeks and months, they could further strengthen investor sentiment and drive earnings recovery. This could set the stage for a turnaround in China’s private sector in 2025 – a basis for us to turn more positive on China.

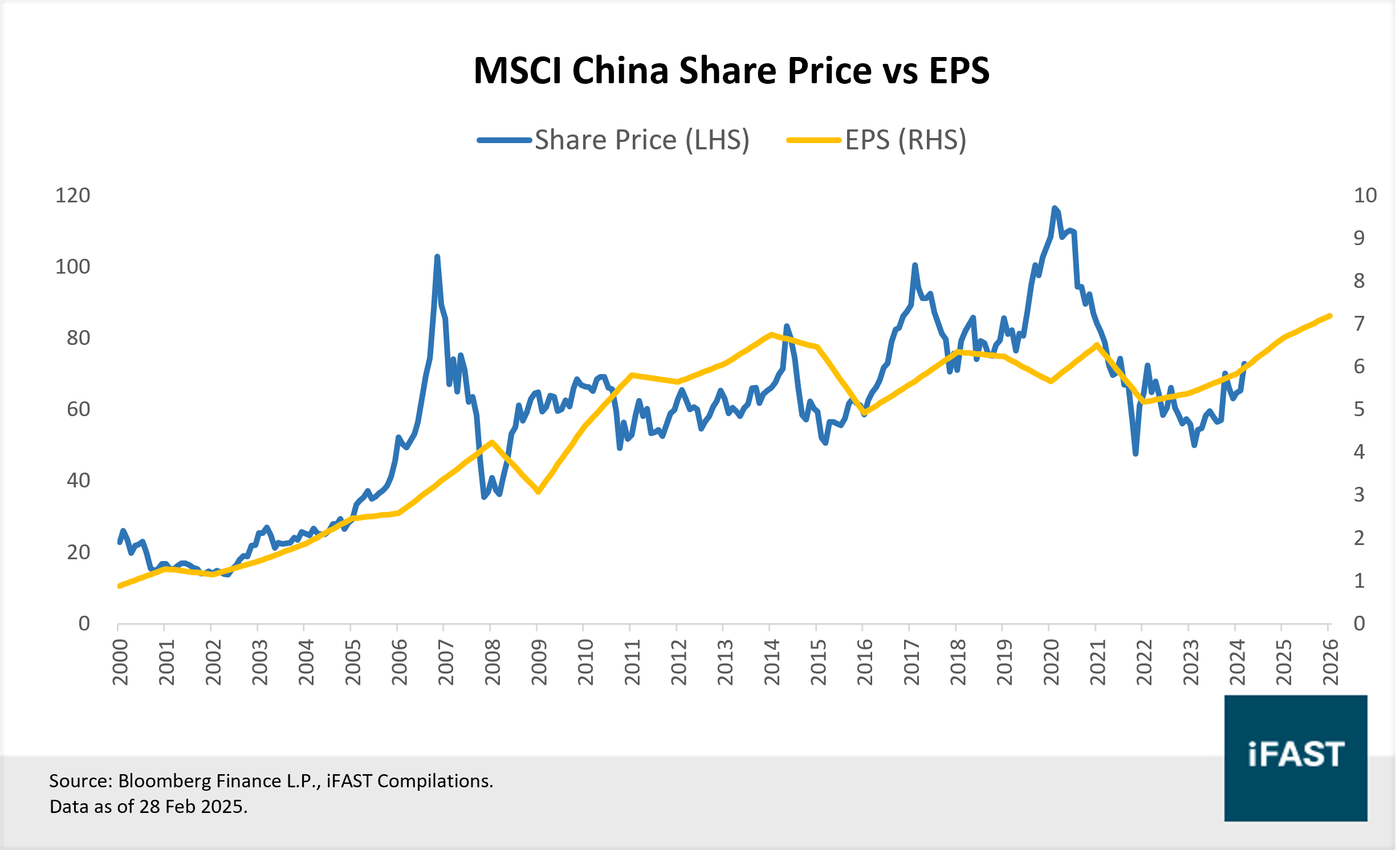

China’s rapid stock price surge over the past two months has pushed the MSCI China Index beyond our FY2026 target of HKD 72.0 (Table 3). Given the sharp rally within a short period, a near-term pullback is likely, and investors should exercise caution before adding significant additions to their positions at this moment. However, China’s strong start to the year suggests its potential as this year’s dark horse. For investors seeking a tactical bet, we recommend Fidelity China Focus A-SGD, iShares Core MSCI China ETF (HKEX: 2801), or iShares MSCI China ETF (NASDAQ: MCHI).

Table 3: MSCI China’s earnings projections till FY2026

|

2023 |

2024E |

2025E |

2026E |

|

|

PE Ratio |

15.1 |

12.5 |

10.9 |

10.1 |

|

Earnings Growth |

5.22% |

20.7% |

14.3% |

7.8% |

|

EPS |

4.84 |

5.84 |

6.68 |

7.20 |

|

Projected Fair Price (Based on fair PE ratio of 10X) |

|

72.0 |

||

|

Upside |

|

|

|

-1.2% |

|

Source: Bloomberg Finance L.P., iFAST

Compilations |

||||

Figure 6: MSCI China Index vs. EPS

Declaration:

For specific disclosure, at the time of publication of this report, the analyst who produced this report holds positions in iShares Core MSCI China ETF (HKEX: 2801).

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.