- Our projection of 4% economic growth for Singapore in 2024 was proven accurate, driven by a robust rebound in industrial production, particularly in electronics. This strong growth was also reflected in the STI Index, which delivered a total return of 23.5% in 2024.

- The manufacturing sector is expected to maintain its recovery in 2025, driven by the electronics upcycle. Local equipment manufacturers are poised for higher output and earnings. Additionally, we believe trade restrictions will have a less significant impact on Singapore compared to other Asian economies.

- Singapore’s banks are likely to sustain modest growth in 2025, with wealth management continuing to drive expansion. While net interest income growth may be limited, excess capital ensures banks’ continued commitment to shareholder returns.

- Despite the attractive valuations, we remain cautious on Singapore REITs due to persistently high interest rates and an uncertain path to rate cuts. Investors should prioritise fundamentals when selecting the sector’s potential winners.

- We maintain our 4.0 star "Very Attractive" rating for the Singapore equity market, projecting a 23.6% upside for the STI Index by 2026.

In late 2023, we projected Singapore’s GDP growth for 2024 to reach 4%, which was notably more optimistic than the Ministry of Trade and Industry’s 1 to 3% forecast. Our prediction was spot on, with the actual GDP growth for 2024 coming in at 4%. This outstanding growth reinforces our upbeat outlook in Singapore’s economic resilience, driven by a strong manufacturing recovery and a robust financial sector.

Related article: Singapore’s GDP to soar by 4% in 2024, here’s how to capitalise on this

Singapore experienced broad-based growth across both goods production and services in 2024. Growth momentum was particularly strong in the second half of the year, driven by a significant rebound in industrial production, with accelerated output growth in electronics (Figure 1). In November 2024, electronics recorded a 26.2% year-on-year (YoY) growth, fuelled primarily by surges in semiconductors (28.8%) and computer peripherals and data storage (23.6%).

Figure 1: Industrial production rebounded strongly in 2H24

Alongside the robust GDP growth in 2024, the STI Index also delivered an impressive total return of 23.5% for the year. Leading the performance was Yangzijiang Shipbuilding from the industrial sector, with a remarkable total return of 101.5% in SGD terms (Table 1), driven by strong order book growth and revenue visibility. Additionally, Singapore's top three banks - DBS, OCBC, and UOB - posted double-digit returns, supported by healthy net interest income and positive growth surprises in the wealth management segment. These businesses demonstrated resilience against a complex macroeconomic backdrop, propelling the STI Index to its highest annual return since 2017.

Table 1: Top Performers of the STI Index in 2024

|

|

Security |

Total Returns in 2024 (in SGD terms) |

Sectors |

|

1 |

Yangzijiang Shipbuilding |

101.5% |

Industrials |

|

2 |

DBS Group Holdings Ltd |

53.2% |

Financials |

|

3 |

Hongkong Land Holdings |

37.5% |

Real Estate |

|

4 |

Oversea-Chinese Banking |

37.4% |

Financials |

|

5 |

United Overseas Bank Ltd |

35.2% |

Financials |

|

6 |

Singapore Exchange Ltd |

35.0% |

Financials |

|

7 |

SATS Ltd |

33.5% |

Industrials |

|

8 |

Singapore Telecommunication |

32.8% |

Communication Services |

|

9 |

Singapore Tech Engineering |

24.3% |

Industrials |

|

10 |

Sembcorp Industries Ltd |

6.3% |

Utilities |

|

Source: Bloomberg. Finance L.P., iFAST Compilations. Data as of 31 Dec 2024. |

|||

Monetary Policy Outlook in 2025

Since November 2024, Singapore’s headline and core inflation have both fallen below 2%, primarily due to a moderation in food and service inflation. Meanwhile, as global conditions eased gradually and the trade-weighted Singapore dollar strengthened, the prices of imported manufactured goods continued to decline broadly.

Figure 2: Singapore’s core inflation have dipped below 2% since November 2024

Given the progress in taming inflation, the Monetary Authority of Singapore (MAS) has signalled a slight slowdown in the appreciation of the Singapore dollar in 2025. This will be achieved by slightly reducing the slope of the Singapore dollar nominal effective exchange rate (S$NEER) policy band, while keeping the band’s width and center level unchanged. These modest adjustments are in line with our inflation outlook. Domestically, the resilient labour market is expected to support ongoing wage growth, while strong economic performance in the third and fourth quarters of 2024 has led MAS to adopt a more cautious approach, avoiding aggressive easing to prevent the economy from overheating.

Externally, persistent inflation in the U.S., with core PCE at 2.8% in November, has led the Federal Reserve to signal slower rate cuts in 2025. Additionally, as a trade-reliant economy, Singapore remains vulnerable to imported inflation. Uncertainties surrounding potential tariffs by Trump could either weaken the global growth outlook or exacerbate inflationary pressures, requiring MAS to react differently. Geopolitical tensions could also drive up oil prices and production costs, hindering progress in global disinflation. Given these risks, we expect MAS to maintain a cautious stance, staying vigilant to risks to both inflation and economic growth.

A snapshot of the sectoral outlook for 2025

Manufacturing to Drive Growth, Fuelled by the Electronics Upcycle

The manufacturing sector is poised to sustain robust economic growth in 2025, with the electronics cluster expected to continue its expansion. This growth will be driven by strong demand for AI data centres and servers, alongside the increasing adoption of high-performance chips in consumer devices. Singapore's strategic position in the downstream semiconductor value chain positions it well to capitalise on the ongoing semiconductor upcycle.

In 2024, significant earnings growth was observed among upstream integrated circuit design companies like Nvidia and AMD, as well as midstream foundry players such as TSMC and Samsung Electronics. We believe this growth is cascading down the value chain, benefiting local companies involved in packaging, testing, and equipment manufacturing by helping them digest inventory and driving higher output and earnings growth.

Some local semiconductor equipment manufacturers have already begun to experience earnings recovery in 2024. Frencken Group reported a 6.7% year-on-year increase in revenue for 9M24. In 3Q24, its semiconductor segment led the growth with a robust 23.0% YoY increase, driven by steady sales to European customers and a sustained recovery in the Asian market. Similarly, Grand Venture Technology saw its 9M24 revenue surge by 35.8% YoY, with semiconductor segment revenue rising by an impressive 50.8% YoY. While AEM Holdings and UMS Holdings faced prolonged inventory digestion and slower recovery from key customers in 2024, we remain optimistic about order momentum in 2025 and the overall growth of the industry.

With sustained strong demand for semiconductors, Singapore is likely to maintain solid electronics-led export growth in 2025. While acknowledging that foreign direct export rules restricting sales of chipmaking equipment to China could have some negative impact on exports, the effect is expected to be limited. Semiconductor exports to China account for only about 5.3% of Singapore’s total exports for the first eleven months of 2024. Additionally, since Singapore primarily focuses on mid-to-lower-end semiconductor components, which are less affected by the new policy, the impact will be further mitigated.

The potential return of Trump to the political stage and his trade policies may increase trade uncertainties. However, Singapore is less likely to be significantly affected compared to other Asian economies. Based on 2023 trade data, Singapore ran a small bilateral trade deficit with the US and accounted for just 2.1% of US total exports. This makes it unlikely to face direct tariffs, unlike countries such as Canada, Mexico, or China, which are top exporters to the US. Moreover, Singapore continues to benefit from supply chain diversification efforts outside of China. This “China+1” trend is expected to persist even if Trump returns to office, providing an ongoing tailwind for Singapore’s industrial production and trade performance.

Banks’ Earnings to Stay Resilient, Though Upside May Be Constrained

Shares of Singapore banks had a record-breaking year in 2024, supported by resilient earnings, solid asset quality, and strong capital returns to shareholders. Looking ahead to 2025, DBS, OCBC, and UOB are expected to achieve moderate income growth, driven by robust momentum in wealth management fees.

As of the end of 2024, the number of single-family offices in Singapore had increased by 43% year-on-year to 2,000, according to Deputy Chairman Chee Hong Tat. He emphasised that the MAS would further support the industry's growth, solidifying Singapore’s position as a key hub for financial services and wealth management. With firm government support, Singapore’s appeal to ultra-high-net-worth individuals is expected to remain strong, underpinned by its political and economic stability and pro-business environment, particularly amid escalating geopolitical tensions between major powers.

We anticipate stable net interest income for the three banks in 2025, as they continue to manage deposit costs, increase investments in fixed-rate assets, and extend portfolio durations to mitigate margin compression. Additionally, the US Federal Reserve’s indications of slower rate cuts, with structurally higher interest rates compared to pre-2022 levels, are expected to help stabilise banks’ net interest income. While slower rate cuts serve as a tailwind, growth in this segment is likely to be limited due to a broad downtrend in interest rates and the subdued pace of loan growth, which has yet to offset narrower margins.

While limited growth in net interest income may temper capital appreciation potential, resilient earnings and significant excess capital above regulatory requirements strengthen the case for another year of robust shareholder returns from Singapore banks. With dividend yields surpassing 5% and the potential for additional share buybacks, these banks remain highly appealing to income-focused investors.

Related article: SG banks’ share prices hit record high: How to position for the next move

Still Maintain a Cautious Outlook on S-REITs

Singapore REITs (S-REITs) ended 2024 in red, with the FTSE ST All-Share REIT Index posting a total return of -5.4% in SGD terms, inclusive of distributions. Persistent inflation and elevated interest rates shaped our cautious view of the sector in 2024, and many S-REITs with weaker balance sheets continued to trade at significant discounts to their book values. Given the resurgence of inflationary pressures and potential trade disruptions from Trump’s policies, we maintain a cautious outlook for the sector in 2025, recommending a selective approach.

Besides valuations, investors should focus on the fundamentals of S-REITs to identify potential winners. Key considerations include capital management, balance sheet discipline - crucial for a debt-reliant sector - and income-generating metrics such as occupancy rates and rental reversions. Based on our stress test, CapitaLand Ascendas REIT (CLAR) (SGX:A17U) has demonstrated greater resilience relative to its peers in the sector.

Related article: A full rebound for Singapore REITs may be premature despite first Fed rate cut

STI’s Valuation Remains Attractive

In 2025, we expect Singapore’s economy to remain robust, driven by a continued rebound in the manufacturing sector, particularly fuelled by the electronics upcycle. Singapore banks are also projected to achieve moderate income growth while continuing to offer attractive shareholder returns. Despite the appealing valuations of S-REITs, we maintain a cautious outlook and advise investors to be selective, focusing on high-quality S-REITs given the ongoing challenges posed by elevated interest rates.

Beyond the strong economic conditions that could bolster investor sentiment, the MAS’s efforts to enhance the liquidity of the local stock market may contribute to potential price-to-earnings (PE) multiple expansion. MAS established a review group in August 2024 to evaluate a combination of demand-side, supply-side, and ecosystem-level measures. We believe this initiative could lead to a comprehensive plan that positions Singapore’s stock market on a stronger footing for long-term growth.

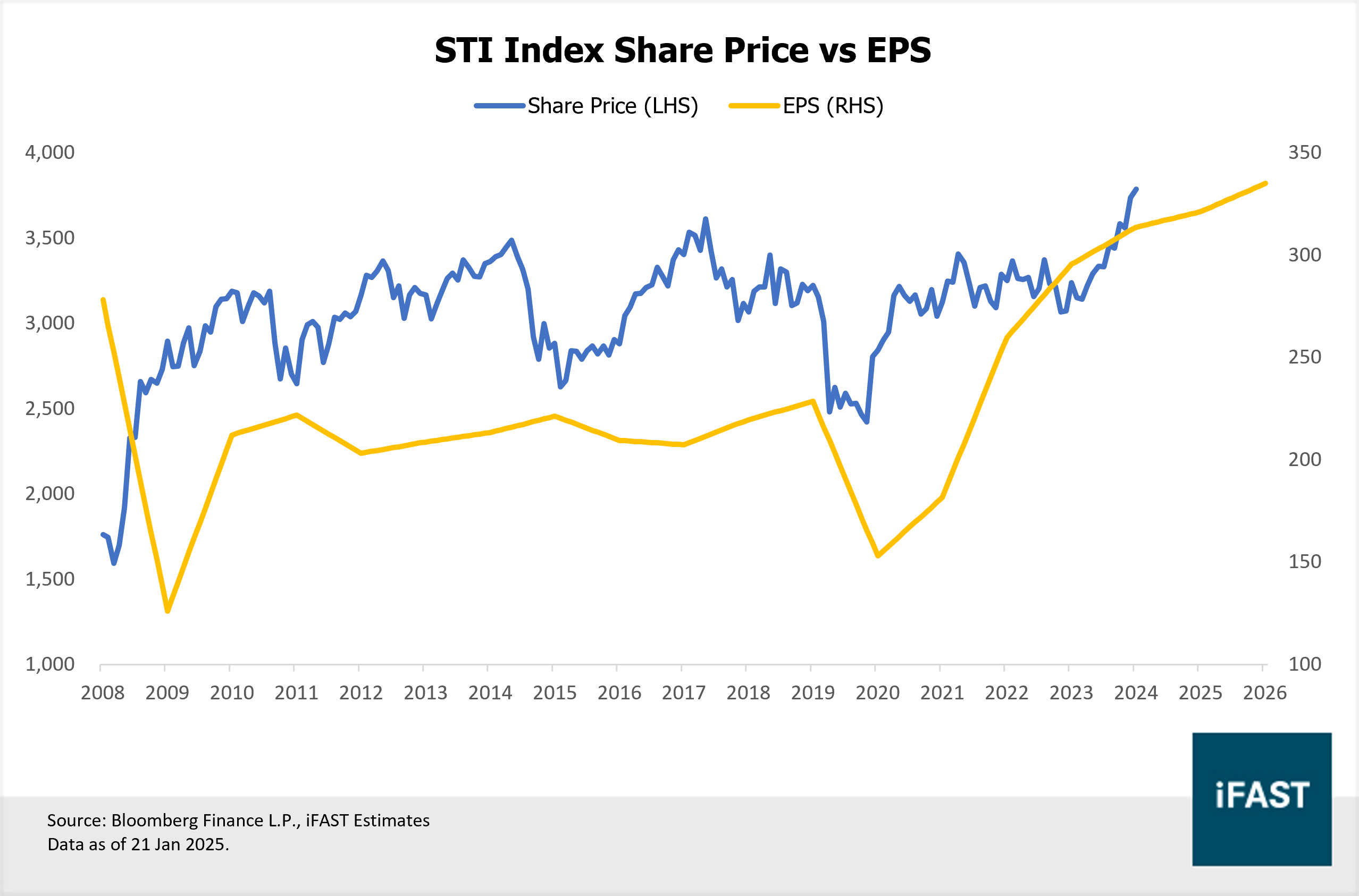

Despite the stellar performance of the STI Index in 2024, its valuations remain attractive. As of 31 December 2024, the index's PE ratio stood at 13.6X, below its 10-year average of 15.3X (Figure 3). Using our fair PE multiple of 14.0X, we derive a target price of 4,690 for the STI by the end of 2026, representing an upside potential of 23.6%. We maintain our current 4.0-star "Very Attractive" rating.

We recommend that investors remain invested in Singapore’s growth story, with the Nikko AM Singapore Dividend Equity SGD Fund and the Nikko AM Singapore STI ETF (SGX: G3B) as attractive investment options.

Figure 3: The STI index’s valuation remains below its 10-year average

Table 2: The STI index’s valuation table

|

|

2023 |

2024E |

2025E |

2026E |

|

PE Ratio (X) |

12.9 |

12.1 |

11.8 |

11.3 |

|

Earnings Growth (YoY %) |

13.8% |

6.1% |

2.4% |

4.3% |

|

Projected Earnings Per Share (EPS) |

295.6 |

313.7 |

321.3 |

335.1 |

|

Target Price (Based on 14X fair PE Ratio) |

- |

- |

- |

4,690 |

|

Potential Upside (%) |

- |

- |

- |

23.6% |

|

Dividend Yield (%) |

4.53% |

4.92% |

5.01% |

5.41% |

|

Source: Bloomberg Finance L.P., iFAST Estimates |

||||

Figure 4: STI Price vs EPS

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.