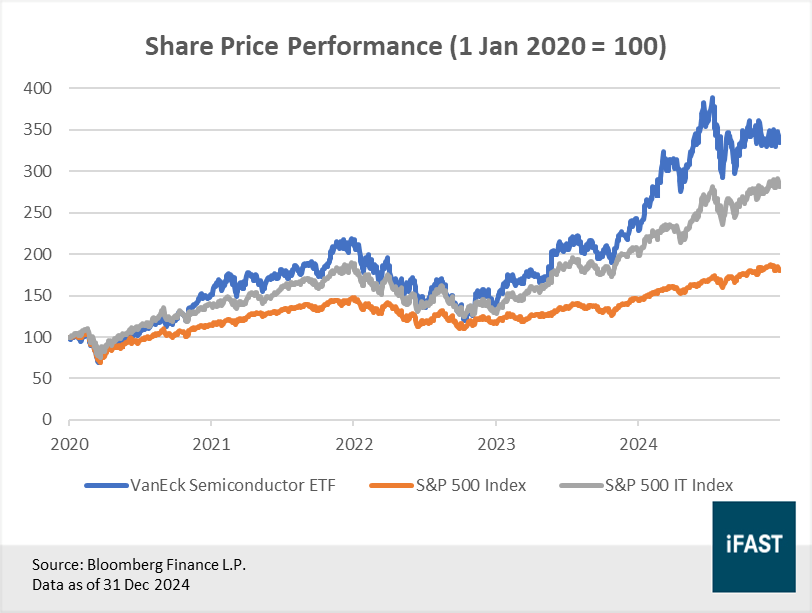

• Chip stocks have more than tripled in the past five years, outperforming both the S&P 500 Index and even the broader technology sector by a significant margin.

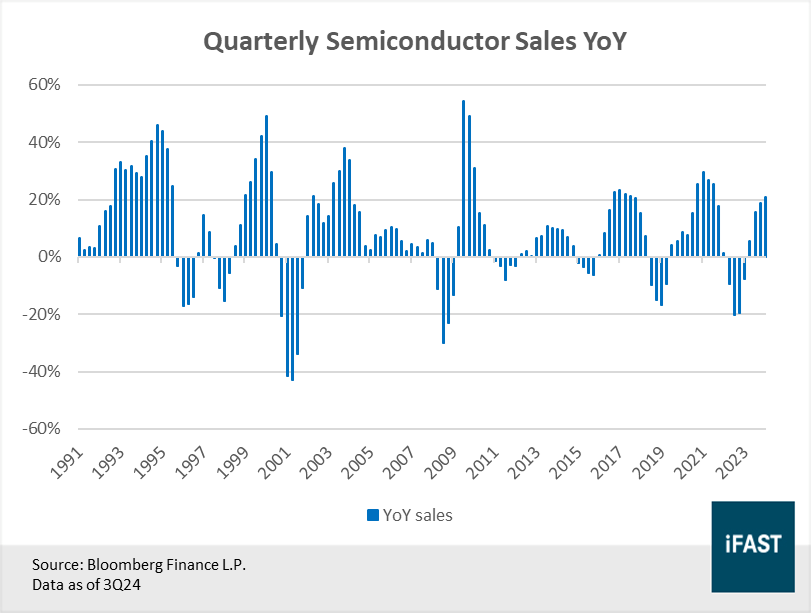

• The industry is currently in an upcycle, delivering robust double-digit sales growth over the past three quarters. Chip sales also reached an all-time high of USD 56.9 billion back in October 2024.

• Structural megatrends such as AI, and the continued digitalisation of the global economy are creating more demand for semiconductors, both in terms of the number of end use products and silicon content.

• With the industry’s long-term fundamentals well intact, investors should make full use of downcycles to build their positions.

• We project an upside potential of 27% for the VanEck Semiconductor ETF, which translates to a target price of USD 311 (as of 2 Jan 2025).

Chip stocks have more than tripled in the past five years

The past five years has been nothing short of spectacular for chip stocks.

From the beginning of 2020 up till today, share prices of chipmakers – measured by the VanEck Semiconductor ETF – have surged by 234% on aggregate. This means an investor who bought and held over this period would have more than tripled their initial investment within a span of five years.

In 2024 alone semiconductor stocks rose by 43%, solidifying the sector as one of the year's top performers. As a matter of fact, semiconductors have emerged as one of the top-performing sectors over the past five years, significantly outpacing both the S&P 500 Index and even the broader technology sector (Figure 1). This outstanding performance underscores investors’ confidence in the chipmaking sector, which continues to play a pivotal role in driving technological innovation and shaping global markets.

Figure 1: The VanEck Semiconductor ETF has risen 234% in the past five years

Beyond share prices, the fundamentals also reveal a strong outlook for the chip industry. Analysing the sales figures, we can clearly tell that the industry remains in an upcycle, delivering robust double-digit sales growth over the past three quarters (Figure 2). Earlier in October, chip sales also reached a record high of USD 56.9 billion. This stellar performance has undoubtedly contributed positively to share price movements across the sector.

Figure 2: Semiconductor sales saw three consecutive months of double-digit growth beginning in 1Q24

Despite their impressive performance, we believe that chips stocks can continue to deliver, and we reiterate our view that semiconductors will be one of the top performing sectors of this decade. Here’s why.

Higher silicon content, increasing applications and the AI megatrend driving chip demand

Semiconductors are the foundation of modern technology, and we expect chip demand to increase exponentially as the world continues its path of digital transformation. Aside from the growing number of semiconductor applications (such as AI, electric vehicles & smart devices), their rising silicon content is also another important factor contributing to the robust demand for semiconductors.

Take for instance in one of Micron’s recent earnings calls, the company shared that PC manufacturers are beginning to introduce new PCs equipped with AI capabilities. These AI-enabled PCs require additional DRAM content, with a minimum of 16GB for entry level PCs and 24GB and above for higher-end segments, compared to the current average of 12GB.

Similarly, AI-enabled smartphones continue to be a strong driver for mobile DRAM content growth. The two latest generations of Apple iPhones (15 & 16) feature Apple Intelligence and have significantly larger DRAM capacities compared to their predecessors. The iPhone 17 Pro, which is slated to be released in 2025 is rumoured to have 12GB of DRAM, 1.5 times more than the iPhone 16 (Table 1).

Table 1: AI-enabled devices require significantly higher DRAM capacity

|

Device |

Year Released |

RAM |

|

iPhone 17 Pro* |

2025 |

12GB |

|

iPhone 16 (all models) |

2024 |

8GB |

|

iPhone 15 Pro |

2023 |

|

|

iPhone 15 |

6GB |

|

|

iPhone 14 (all models) |

2022 |

|

|

iPhone 13 Pro |

2021 |

|

|

iPhone 13 |

4GB |

|

|

iPhone 12 Pro |

2020 |

6GB |

|

iPhone 12 |

4GB |

|

|

iPhone 11 (all models) |

2019 |

|

|

iPhone XS |

2018 |

|

|

iPhone X |

2017 |

3GB |

|

iPhone 8 Plus |

||

|

iPhone 7 |

2016 |

2GB |

|

iPhone 6s |

2015 |

|

|

iPhone 6 |

2014 |

1GB |

|

iPhone 5s |

2013 |

|

|

iPhone 5 |

2012 |

|

|

Prior generations to iPhone 5 |

Before 2021 |

< 512MB |

|

Source: Apple, iosref *All information related to iPhone 17 Pro are estimates Data as of Dec 2024 |

||

From a broader perspective, rising chip demand is likely to be bolstered by structural megatrends such as AI, which is arguably the biggest development the sector has seen since the arrival of smartphones in the late 2000s.

Recognising the vast potential of AI, big tech companies have ramped up spending, purchasing billions of dollars’ worth of AI chips. This surge has contributed immensely to the fortunes of companies like NVIDIA, which saw its data center revenue reach a record high of USD 30.8 billion in 3Q24, a 112% increase from a year ago.

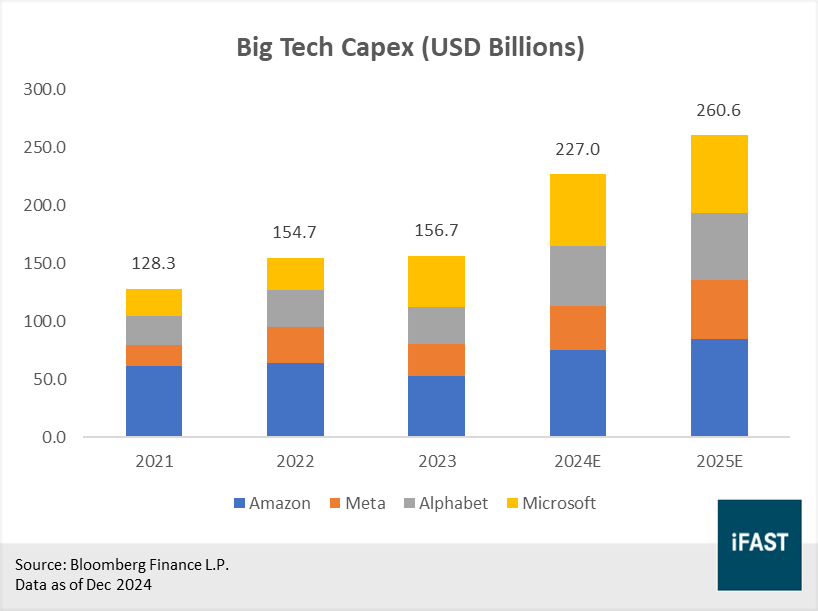

The good news? Global spending on AI does not appear to be slowing down. Big tech companies are still pouring massive amounts of money into AI. The combined capex of the four largest internet companies is expected to grow by 15% this year, even after rising more than 45% in 2024 (Figure 3).

Figure 3: Big tech companies are investing heavily in AI

That is not all. Besides buying directly from chipmakers, big tech companies such as the likes of Microsoft and Meta are also developing their own custom AI chips, which could be beneficial to foundry players like TSMC in the long run.

Just like the internet and smartphone revolutions in the past, we expect the AI revolution to create significant opportunities for chipmakers in the foreseeable future.

Generous government support adds to the positive outlook

In addition to these structural megatrends, semiconductor companies are also benefiting from significant support from the public sector. Governments worldwide are committing substantial funding and resources to bolster the industry, recognising its strategic importance in terms of economic growth and even national security.

In the US, Biden’s administration initiated the CHIPS and Science Act as part of a broader effort to bolster US competitiveness in semiconductor manufacturing, particularly in advanced semiconductors. The country aims to produce 20% of the world's most advanced chips by 2030. As of August 2024, the White House reported that USD 30 billion of the USD 39 billion in direct funding had already been disbursed and that it remains on track to allocate the remaining budget by the end of 2024.

Over in Asia, China has made the development of its domestic semiconductor capabilities one of its biggest national priorities, after enduring years of intensifying sanctions by the US. Support from the central government comes mainly from the China Integrated Circuit Industry Investment Fund (ICF), which has raised a combined total of over USD 40 billion in its first two phases. Phase three is expected to come with a hefty investment of USD 47.5 billion and will run from now till 2039.

Japan is also undergoing its own chip renaissance, marked by renewed investments from both the public and private sector. The government, in collaboration with major Japanese corporations have established Rapidus, a homegrown chipmaker with an ambitious goal of producing 2nm chips by 2027. Alongside other structural factors mentioned earlier, the extensive government support serves as another important catalyst for the semiconductor industry.

Why downcycles should be viewed as opportunities

What goes up must come down—a principle that holds true for the semiconductor cycle as well.

While the chip industry is currently basking in its moment of glory, seasoned investors will know that it is no stranger to cycles of ups and downs.

To recap, semiconductor cycles are essentially driven by fluctuating sales growth numbers, which stems from imbalances in supply and demand dynamics. There are a few factors, but for the most part, these imbalances can be explained by over-and under-estimations in production levels.

When times are good, chipmakers tend to overestimate demand, invest heavily in capacity, and produce more than what the market can absorb. Over time, the high level of production eventually becomes unsustainable as inventory starts to build, leading to an oversupply. When this happens, chipmakers slash prices and cut down on production as they work through excess inventory, causing sales growth to fall – even as demand remains relatively stable.

But just like how chipmakers tend to over-produce when times are good, they also have the tendency to under-produce when times are bad. Put simply, it is the excessive adjustments in production levels that lead to fluctuating sales growth numbers, a characteristic that defines the cyclical nature of the semiconductor industry.

There are, however, silver linings that investors should take note of.

Firstly, the semiconductor industry has evolved to become less cyclical and more structural. Recent down cycles have also shown milder declines in sales compared to the past, with growth during upcycles far outpacing these contractions.

Unlike the past where chips were found in only a handful of applications (e.g. PCs) and in relatively small amounts, semiconductors have practically become ubiquitous these days and are featured abundantly in numerous different applications (e.g. self-driving vehicles, data centers & Internet-of-Things devices). The diverse range of end use products helps to mitigate the impact of a downturn in any single segment, effectively making the industry less cyclical than before.

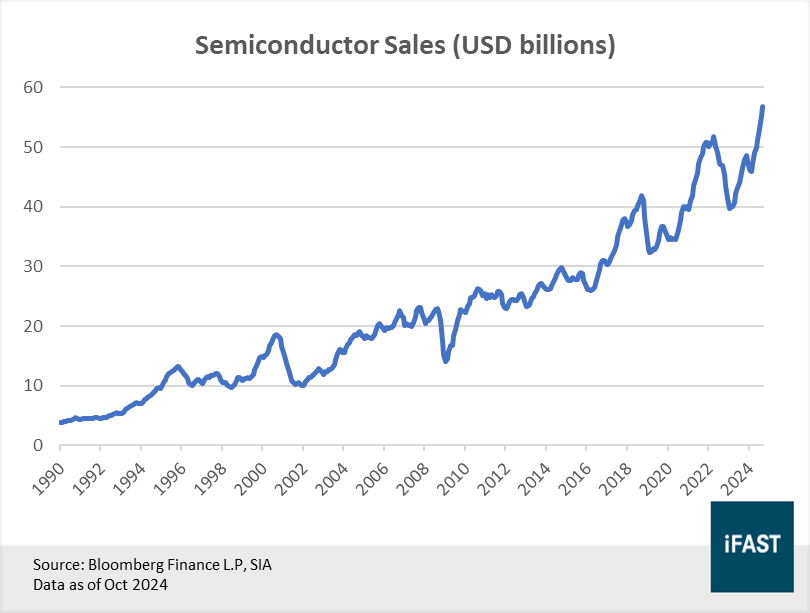

The second piece of good news is that down-cycles are unlikely to last forever. History has shown that after every single downturn, chip sales have continued to forge higher highs and lower lows (Figure 4), which again is most likely due to the structural tailwinds behind the industry. Ultimately, we are confident that the long-term growth story for semiconductors remains intact, and chips sales will only continue to trend higher as the years go by.

Investors should bear these things in mind when the next down cycle arrives.

Figure 4: Semiconductor sales have always bounced back to higher levels than before post-downturn

We believe chip stocks can continue to deliver

With such a promising long-term outlook, we believe that chip stocks can continue to deliver. While valuations have become more expensive this year following their impressive share price performance, they are still not overly expensive especially if we consider the level of earnings growth they can deliver – which is roughly 30% each year on average (Table 2).

Based on a fair PE multiple of 24X applied to 2026 estimated earnings, we project the upside potential of the chip sector to be approximately 27%, which translates to a target price of USD 311 for the VanEck Semiconductor ETF (NASDAQ:SMH).

Over time chip stocks could see more positive revisions to earnings estimates, which will serve to lower their valuations. This could also be accompanied by further multiple expansion, driven by improved market sentiment/investor confidence.

Table 2: Chip stocks possess strong earnings growth potential

|

MVSMHTR Index |

2023 |

2024E |

2025E |

2026E |

|

Earnings Per Share (EPS) |

238.66 |

317.00 |

418.00 |

527.00 |

|

Earnings Growth YoY |

-15.56% |

32.82% |

31.86% |

26.08% |

|

PE Ratio |

29.61 |

31.42 |

23.83 |

18.90 |

|

Upside Potential (based on a fair PE Ratio of 24X) |

- |

- |

- |

26.97% |

|

Source: Bloomberg Finance L.P., iFAST Compilations. Data as of 2 Jan 2024 |

||||

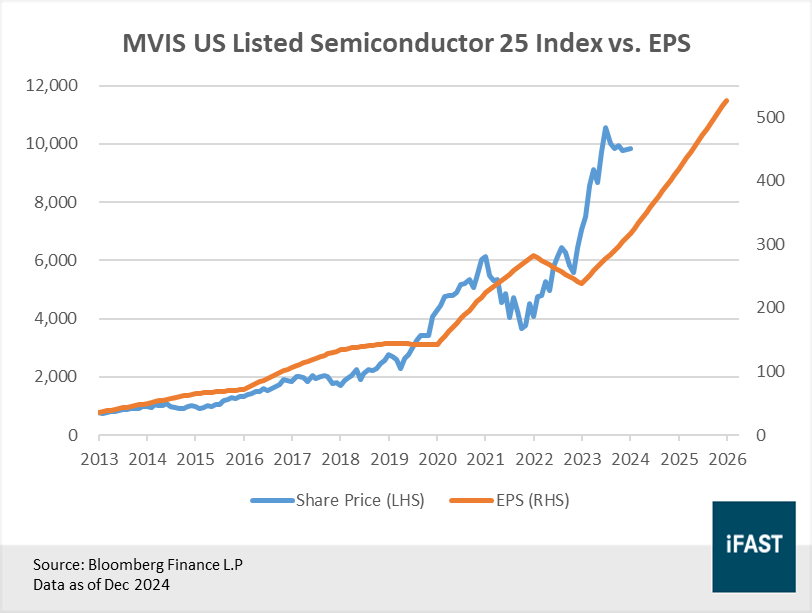

Figure 5: Share prices are predominantly driven by earnings in the long run

Investors concerned about valuations may choose to wait for a pullback to buy, though there is no guarantee that one will materialise. Instead, we recommend adopting a dollar-cost averaging strategy while keeping an eye out for sharp pullbacks to make lump-sum investments. This approach ensures that if the sector does indeed go on a run, investors are still able to benefit.

With growing demand, solid fundamentals and significant government backing, we believe that the chip sector is well positioned to thrive. We reiterate our view that semiconductors will be one of the top performing sectors over the next few years.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in the VanEck Semiconductor ETF.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.