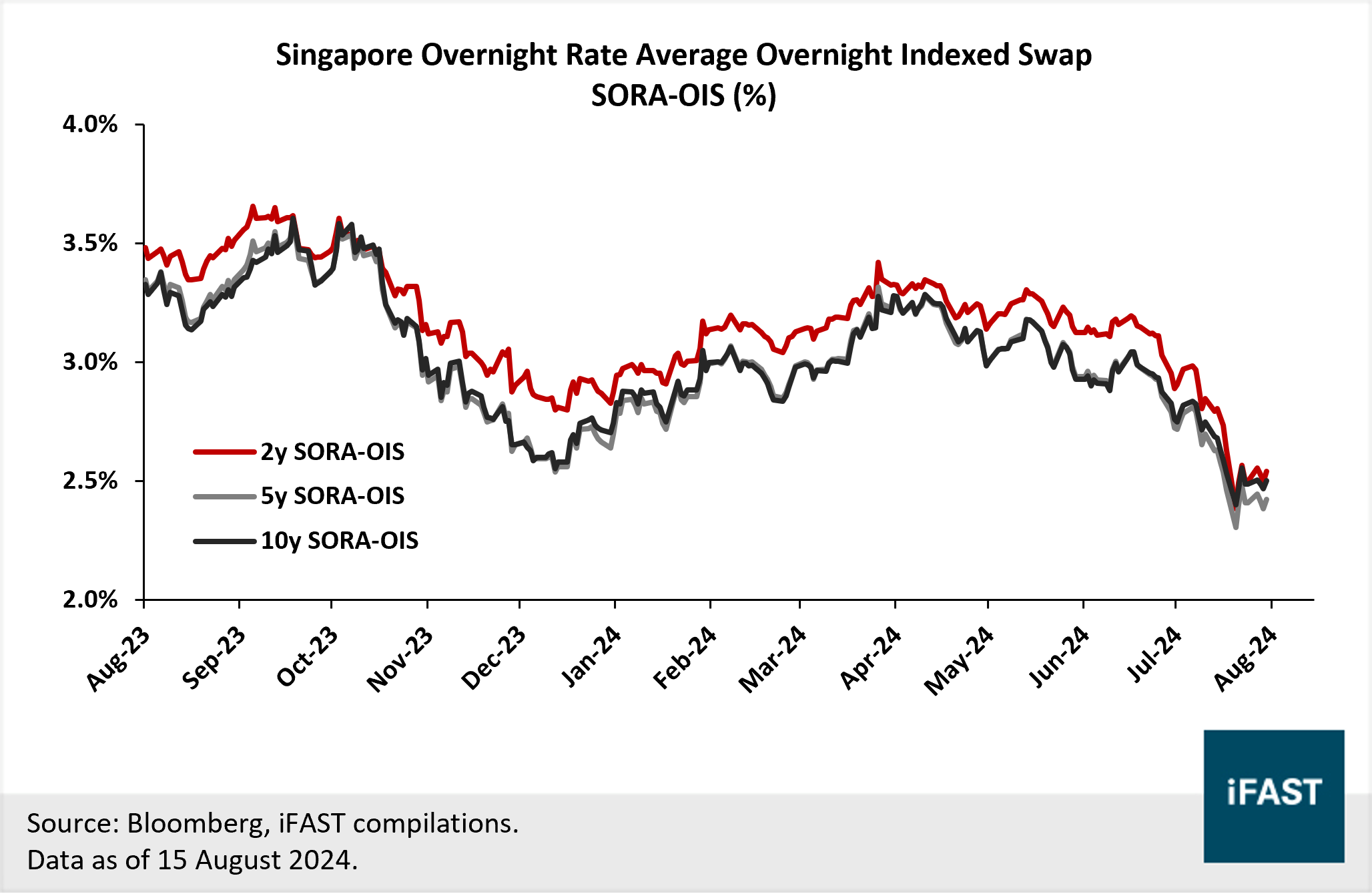

Singapore benchmark rates have started to decline

Chart 1: Singapore benchmark rates have fallen in recent months

Chart 2: Longer-tenor SG sovereign bond yields have closely mirrored the trajectory of benchmark rates

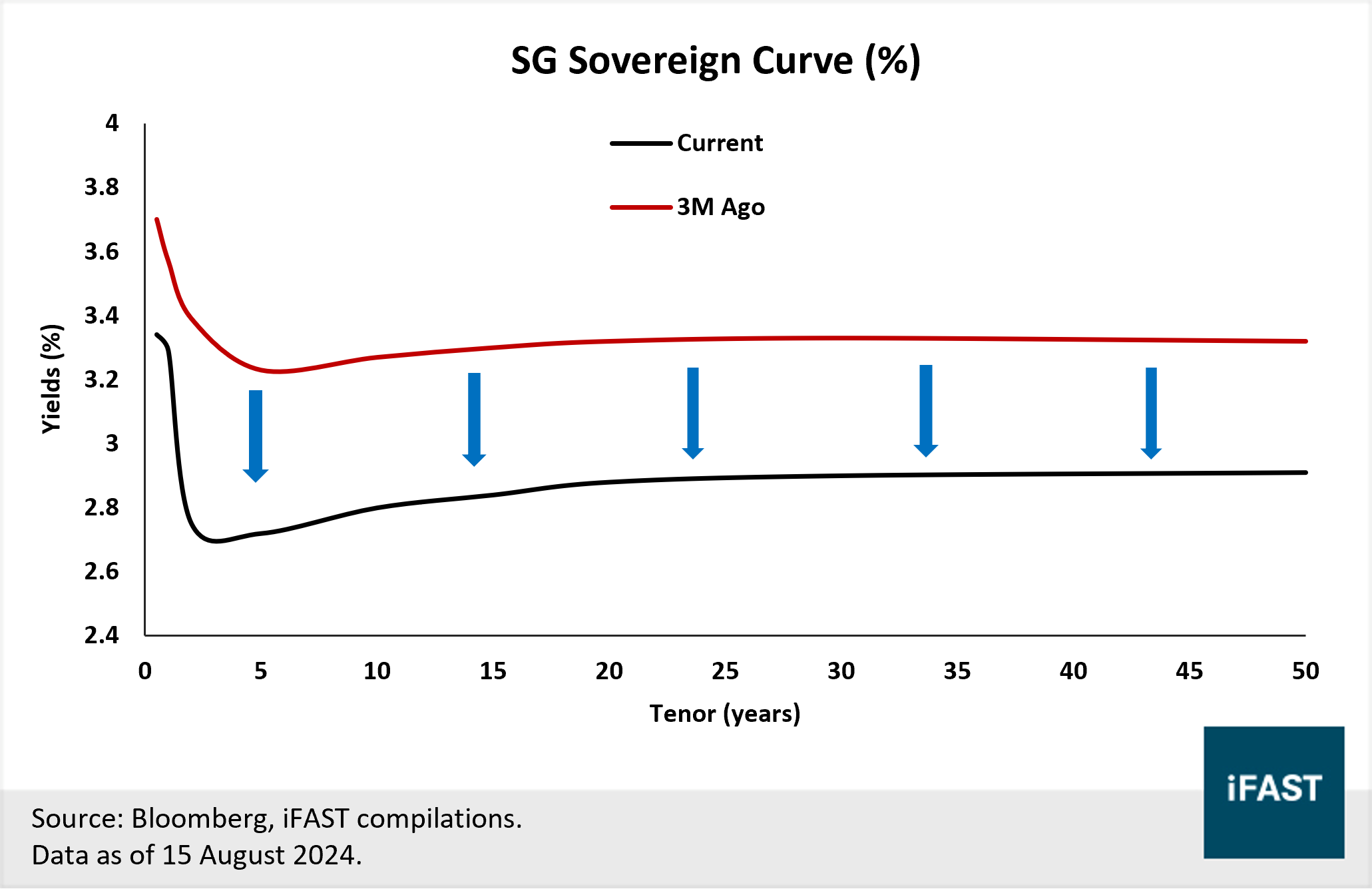

Chart 3: SG sovereign curve remains deeply inverted

Has this dimmed the appeal of SGD bonds?

Singapore T-bills shine amidst the equity market carnage

Treasures can be found across SGD corporate universe

- STRTR 3.750% 29Oct2025 Corp (SGD) and STRTR 4.100% 04May2026 Corp (SGD) offer close to 4.5% yield for under two years to maturity – one of the higher yielding short duration SGD bonds. Alternatively, GUOLSP 3.290% 26Oct2026 Corp (SGD) and GUOLSP 4.050% 04Jun2027 Corp (SGD) offer above 4% yield for two to three years to maturity.

- OUECT 3.950% 02Jun2026 Corp (SGD), one of the highest yielding investment-grade rated SGD REIT issuances.

- DB 5.000% 05Sep2026 Corp (SGD), an investment-grade rated bank bond boasting high coupons and near 4.2% yield to maturity (and 3.9% yield to call).

|

Issues |

Bond Issuer |

Ask Price |

Years to Maturity/ Next Call |

Yield to Maturity/ Next Call (% p.a.) |

|

The Straits Trading Company |

99.10 |

1.20 |

4.53 |

|

|

The Straits Trading Company |

99.45 |

1.71 |

4.44 |

|

|

OUE CT Treasury |

100.20 |

1.79 |

3.83 |

|

|

Deutsche Bank |

101.13 |

2.05/ 1.05 |

4.18/ 3.90 |

|

|

GLL IHT |

98.40 |

2.19 |

4.06 |

|

|

GLL IHT |

100.15 |

2.80 |

3.99 |

|

|

Sources: Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. Data as of 15 August 2024. |

||||

- GUOLSP 4.400% 27Jul2028 Corp (SGD) and STRTR 4.700% 24Jan2029 Corp (SGD)which offers around 4% – 4.5% yield for a similar tenor of 4 – 4.5 years.

- BNP 4.750% 15Feb2034 Corp (SGD) and CMZB 6.500% 24Apr2034 Corp (SGD) are IG rated bonds that offer around 4.3 – 5.2% yield and has a tenor of more than nine years but are callable in 4.4 more years. BNP Paribas’ 2034 bond is rated “BBB+” by S&P ratings while Commerzbank’s 2034 bond is rated “Baa3” by Moody’s ratings.

|

Issues |

Bond Issuer |

Ask Price |

Years to Maturity/ Next Call |

Yield to Maturity/ Next Call (% p.a.) |

|

GLL IHT |

101.40 |

3.95 |

4.01 |

|

|

The Straits Trading Company |

100.95 |

4.46 |

4.46 |

|

|

BNP Paribas SA |

102.4 |

9.50/ 4.50 |

4.29/ 4.15 |

|

|

Commerzbank AG |

106.75 |

9.69/ 4.44 |

5.21/ 4.79 |

|

|

Sources: Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. Data as of 15 August 2024. |

||||

- ASTLC 3.000% 18Mar2031 Corp (SGD) - Class A-1 - Retail and ASTLC 4.350% 19Jul2039 Corp (SGD) - Class A-1 - Retail. Both bonds have strong credit rating and offer one of the highest yields within the limited SGD retail bond space.

- We expect ASTLC 3.000% 18Mar2031 Corp (SGD) - Class A-1 - Retail to be redeemed early on its mandatory call date. In addition to the yield, investors will earn an additional 0.5% bonus redemption of the principal amount (owing to the “Sponsor Sharing” feature on Astrea VI).

|

Issues |

Bond Issuer |

Ask Price |

Years to Maturity/ Next Call |

Yield to Maturity/ Next Call (% p.a.) |

|

Astrea VI |

98.53 |

6.58/ 1.58 |

3.92/ 3.93 |

|

|

Astrea 8 |

102.42 |

14.92/ 4.92 |

4.13/ 3.81 |

|

|

Sources: Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. Data as of 15 August 2024. |

||||

- VRTVEN 3.300% 28Jul2028 Corp (SGD) which offers above 3.7% for a tenor of nearly four years. Vertex Ventures Holdings is a wholly-owned Temasek subsidiary and mainly invest in early-stage and growth-stage technology. The bond offers a yield pickup over the 2-year SGS (yield: 2.75%) and 5-year SGS (yield: 2.72%) as well as bonds of other Temasek owned/ linked issuers. Additionally, the slightly longer tenor allows investors to lock in higher yields for longer.

|

Issues |

Bond Issuer |

Ask Price |

Years to Maturity/ Next Call |

Yield to Maturity/ Next Call (% p.a.) |

|

Vertex Venture Holdings |

98.49 |

3.95 |

3.72 |

|

|

Sources: Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. Data as of 15 August 2024. |

||||

- OLAMSP 4.000% 24Feb2026 Corp (SGD), which is attractively priced with close to 1.5 years to maturity, and TMGSP 5.250% 13May2027 Corp (SGD), which offers close to 5% yield, with a longer tenor of close to three years. These names offer good compensation to investors for the additional credit risk (credit spread of around 150 - 220bps (z-spread)).

|

Issues |

Bond Issuer |

Ask Price |

Years to Maturity/ Next Call |

Yield to Maturity/ Next Call (% p.a.) |

|

Olam International |

99.00 |

1.52 |

4.69 |

|

|

Thomson Medical Group |

100.93 |

2.74 |

4.88 |

|

|

Sources: Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. Data as of 15 August 2024. |

||||

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.

Please note that only certain bond(s) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to Fundsupermart.com's prevailing policies and procedures. Please read our full disclaimers in the website.