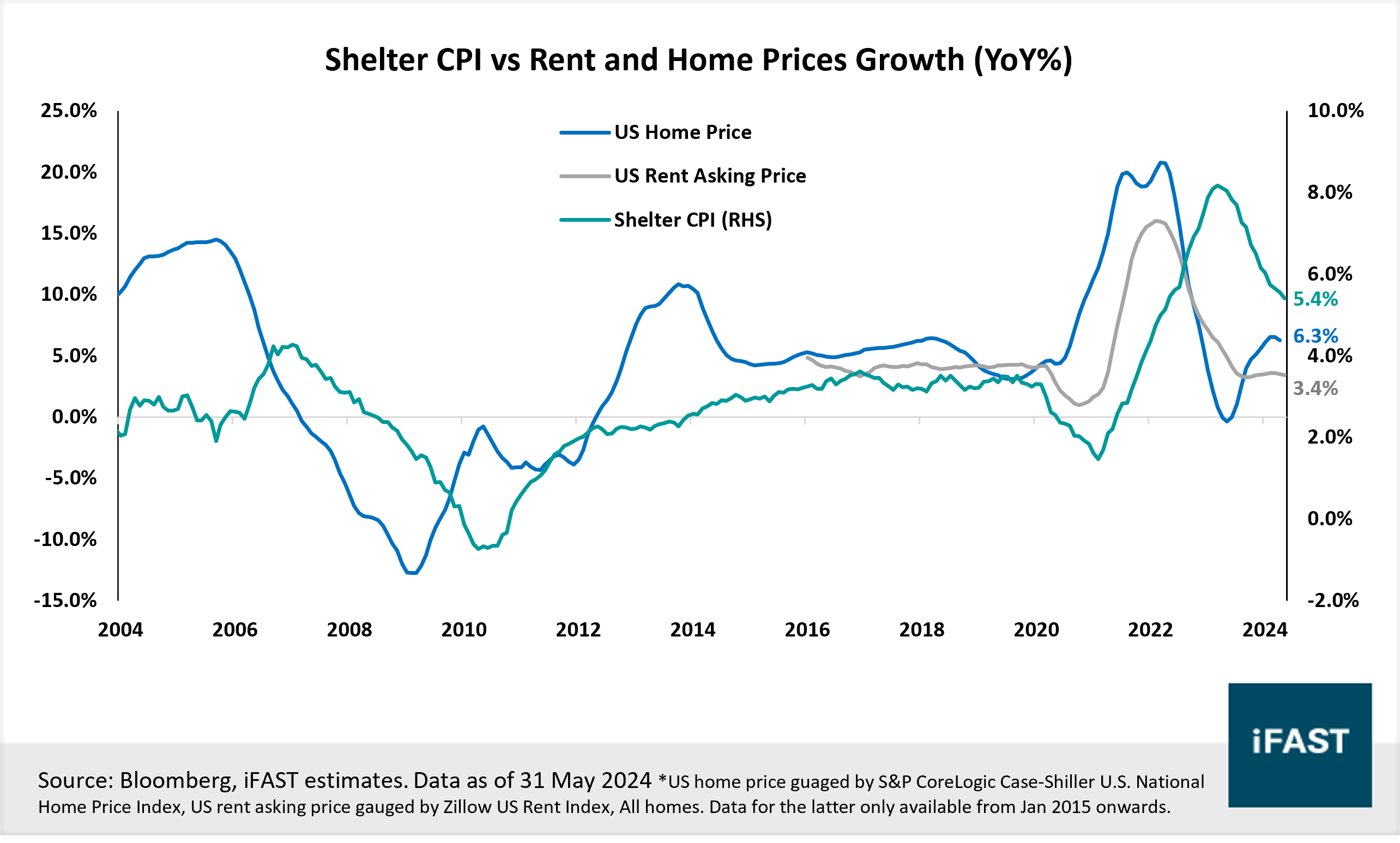

- We maintain our view of no Fed rate cuts in 2024 as shelter inflation stays sticky while the US economy remains resilient, supported by consumer spending.

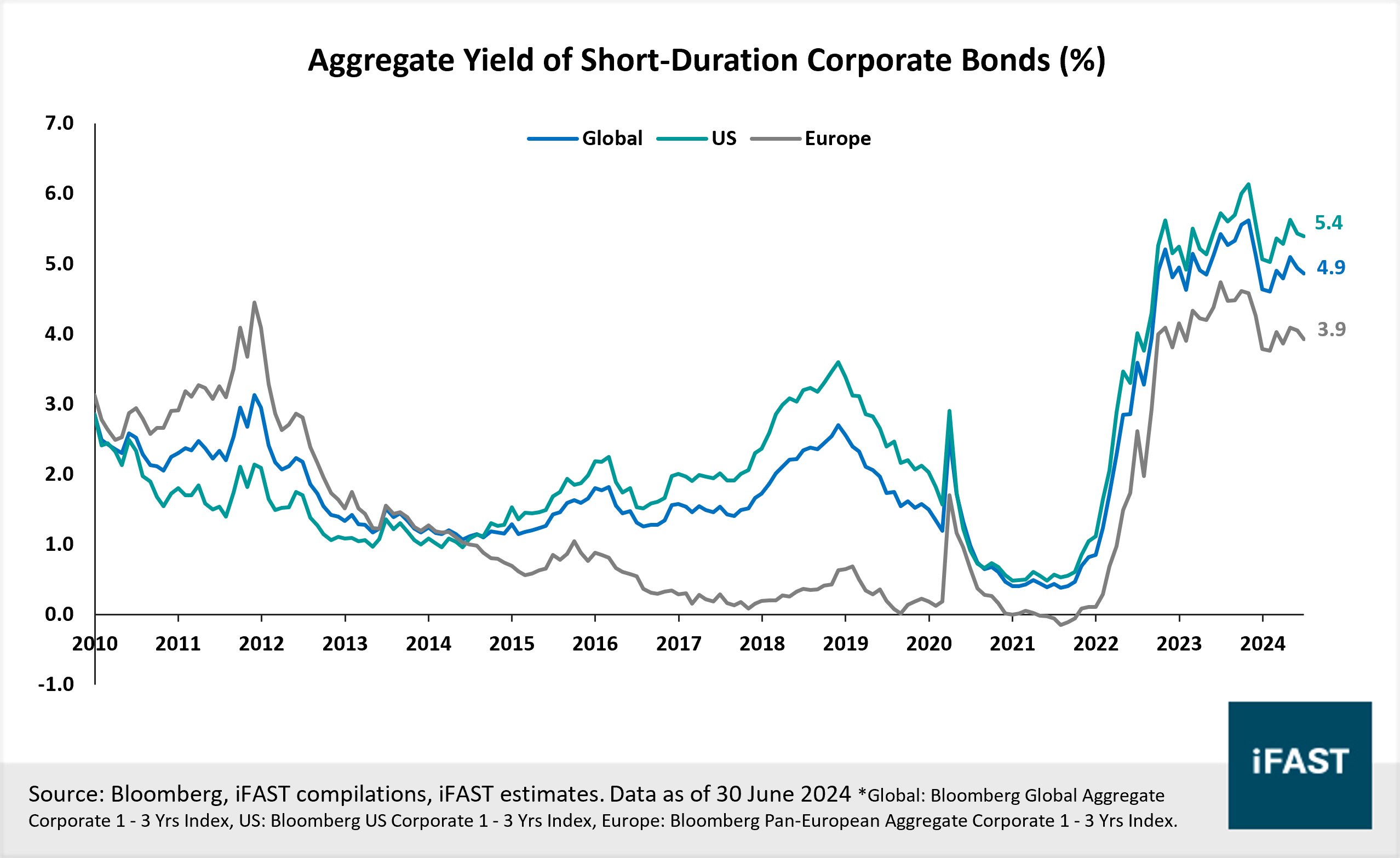

- Anchored by the above view, we continue to favour short duration bonds as yields remain attractive. We also see poorer risk-reward from longer duration bonds currently.

- We are sticking to stronger quality bonds as high rates are likely to exert increasing pressure on high-yield issuers, which are trading at tight valuations.

Chart 1: Bond markets have rebounded in late-2023, with most markets seeing positive returns in 1H24

1. No Fed rate cuts in 2024

Chart 2: Growth in home and rent price remains resilient, suggesting that shelter inflation may take longer to subside

Chart 3: US inflation has eased but remains elevated. Core PCE remains firmly above policymaker’s 2% target.

2. Sticking with short duration bonds

Chart 4: Short duration corporate bond yields have risen significantly and remain high relative to history

Chart 5: Rate cut expectations have been greatly tempered over the past six months

3. Climb the quality ladder

Chart 6: HY debt might face a maturity wall as soon as 2025

Chart 7: A global default cycle is underway

Looking for individual bond picks?

Table 1: Recommended SGD corporates

|

Issues |

Ask Price |

Years to Maturity/ call |

Yield to Maturity/ call |

|

98.40 |

1.63 |

5.04% |

|

|

100.58 |

2.84 |

5.03% |

|

|

99.62 |

0.56 |

4.76% |

|

|

100.10 |

0.64 |

4.92% |

|

|

99.45 |

1.82 |

4.42% |

|

|

99.10 |

1.31 |

4.47% |

|

|

99.90 |

1.90 |

4.00% |

|

|

99.97 |

0.68 |

4.03% |

|

|

100.55 |

2.16/ 1.16 |

4.95%/ 4.50% |

|

|

Sources:

Bondsupermart, Bloomberg Finance L.P., iFAST Compilations. |

|||

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a position in OLAMSP 4.000% 24Feb2026 Corp (SGD), ESRCAY 5.100% 26Feb2025 Corp (SGD), STRTR 4.100% 04May2026 Corp (SGD), STRTR 3.750% 29Oct2025 Corp (SGD), OUECT 3.950% 02Jun2026 Corp (SGD) and the analyst who produced this report holds a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.