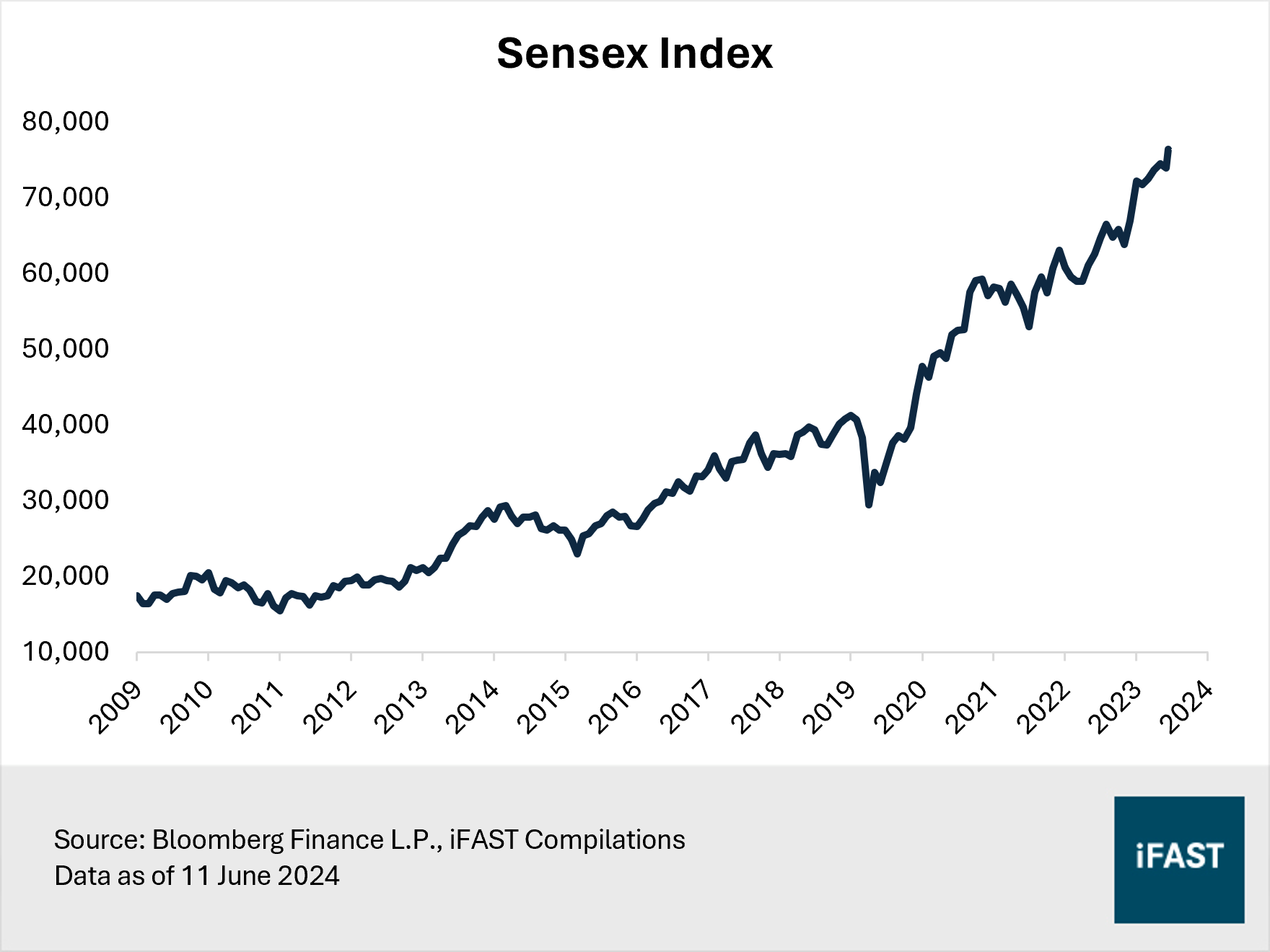

- Volatility has been high in India’s Sensex Index. It tumbled 6% on June 4, the day of the election results. But since then, the index has recovered and is trading at a fresh all-time high.

- Modi continues as India’s prime minister for a third term, but his party lost its majority in parliament, forcing reliance on allies to form a government for the first time in a decade.

- Politics aside, we believe investors should not overlook India's persistent issues. Notably, youth unemployment is among the highest in emerging Asia. Also, its twin deficits pose a significant threat to long-term economic stability and growth.

- The surprise election results may increase volatility in Indian equities in the near term. Additionally, elevated valuations risk a market correction if economic and earnings growth fall short of expectations.

- Based on our fair PE ratio of 19X, we project a 2026 target price of nearly 77,600 for the Sensex Index, which translates to an upside potential of only 1% based on the closing price on 11 June 2024.

Volatility has been running high in India’s Sensex Index. It tumbled by 6% on 4 June, the day of the nation’s election results. This represented the worst trading session in four years as Modi’s ruling party secured a narrower-than-expected victory, despite exit polls predicting a landslide win.

That said, days later, the index recovered after a key ally of the political alliance led by Modi’s party affirmed support for the formation of the next government. Consequently, the Sensex is now trading at a fresh all-time high (Figure 1).

Figure 1: Sensex fell after reaching an all-time high

No party wins majority

On 9 June, Narendra Modi was sworn in as India’s prime minister for the third term. However, his party lost its majority in parliament, forcing him to rely on allies to form a government for the first time since he came to power a decade ago. A coalition government may delay reforms and decision-making, which many see as crucial in driving long-term economic growth.

It is worth noting that a single-party government led by Modi has produced significant reforms in the past decade, like demonetisation and the implementation of the goods and services tax.

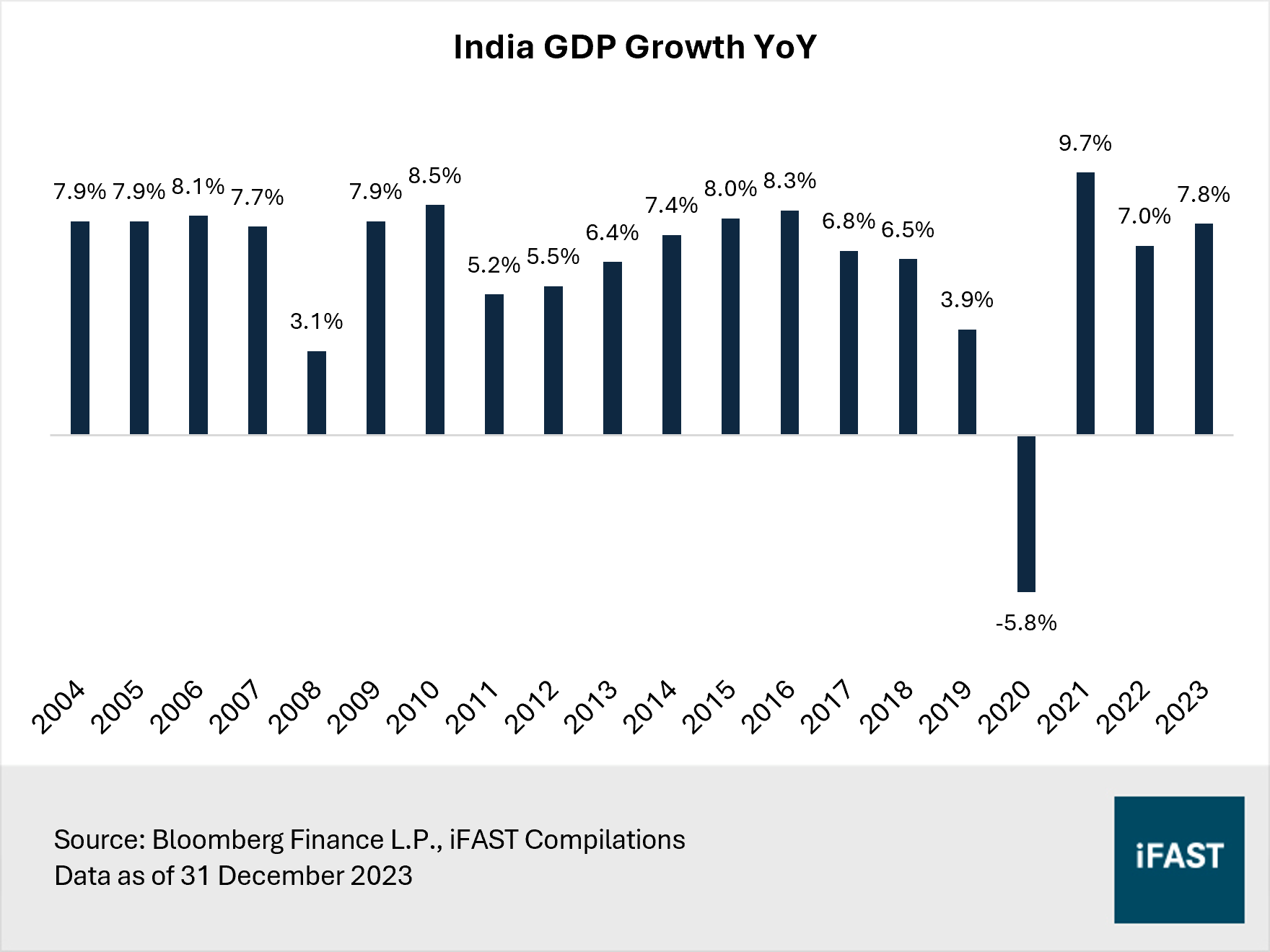

Modi had also pledged ambitious economic growth targets, including making India a developed country by 2047. Economists estimate that India would need to deliver growth of 8 to 9% per annum for the next 20 years in order to meet this goal. This is a tall order, given that the country has never consistently achieved such levels of growth (Figure 2). Meanwhile, China was one of the few countries to have attained an average of 10% a year for about three decades after it initiated economic reforms in the late 1970s.

Figure 2: India GDP in the last two decades

On a more positive note, coalition governments are not new to India. The nation has seen several coalition governments, especially between 1992 and 2014. Coalition governments typically act as a built-in system of checks and balances. Also, the policy direction of Modi will likely get carried forward despite the narrow victory. India’s business-friendly policy should continue to benefit industries such as manufacturing and banking.

The ‘China plus one’ story also remains intact, with India increasingly viewed as a prime destination for diversifying supply chains away from China. The Indian government has been actively courting multinationals to establish operations in the country, rolling out a series of measures such as corporate tax cuts and incentives under the “Make In India” campaign.

High youth unemployment

Opportunities aside, we believe investors should not overlook the persistent issues facing India.

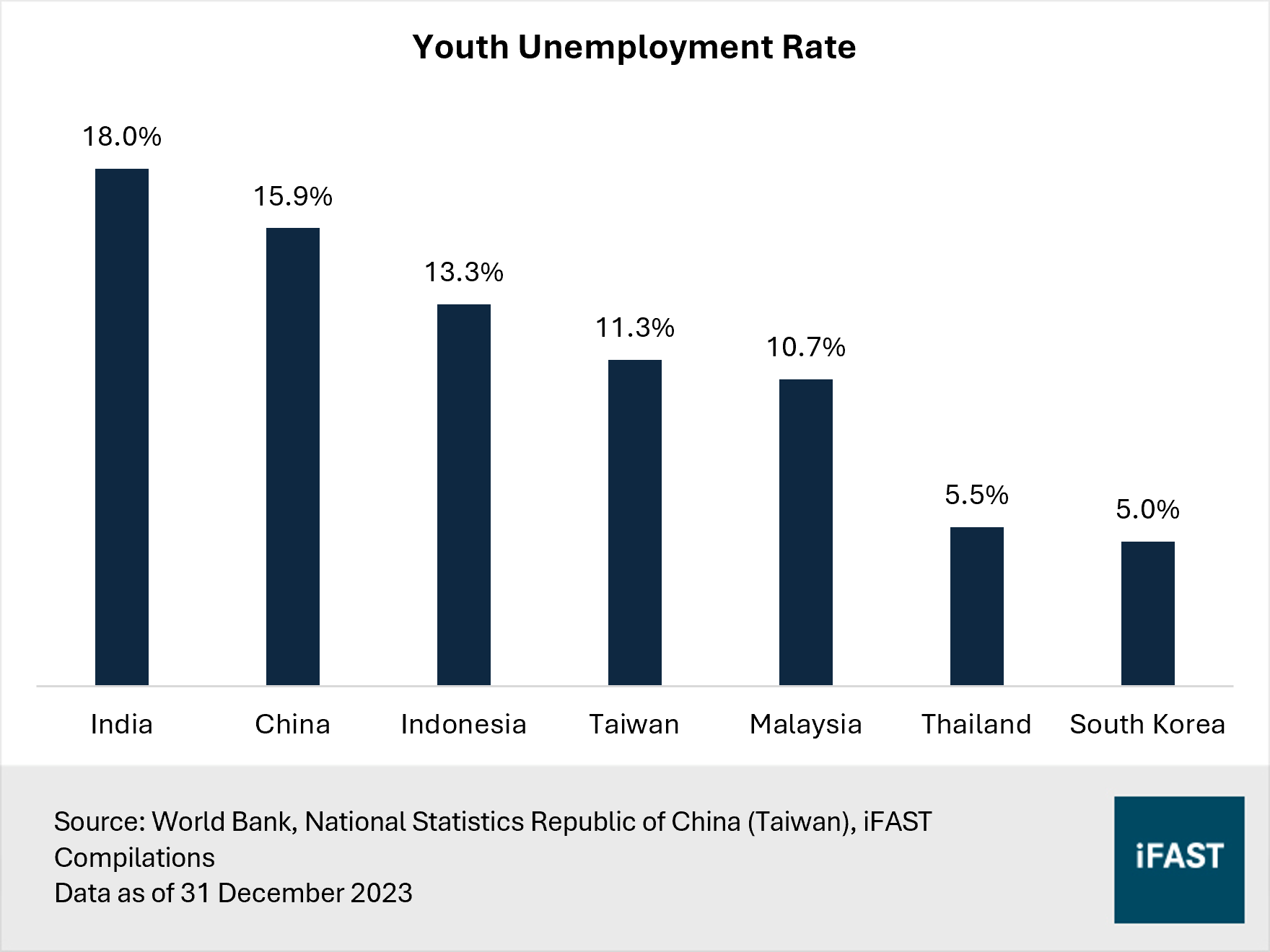

Notably, the country’s youth unemployment – the share of the labour force ages 15 to 24 without work but available for and seeking employment – is one of the most acute in emerging Asia. According to World Bank estimates, youth unemployment in India is worse than in China and ASEAN nations like Indonesia and Malaysia (Figure 3).

Figure 3: Youth unemployment is acute in India

Meanwhile, the Centre for Monitoring Indian Economy (CMIE), a private research company, estimates that the jobless rate of those aged 20 to 24 was 44.5% in the October-December quarter of 2023.

Employment emerged as a key election campaign issue, with opposition parties criticising the government for failing to deliver enough jobs, especially for young people. Poor schooling and high drop-out rates mean young people are not being adequately equipped to take on the jobs needed to sustain India’s high growth.

This is especially important as India seeks to join the global semiconductor supply chain, covering aspects like chip packaging and design. A common factor among top nations excelling in the semiconductor industry – like South Korea, Singapore, the US, Taiwan, and Japan – is an exceptional education system as well as a highly skilled and productive workforce. India, on the other hand, has a large labour pool but is still far from equipping its people with the necessary skills.

Twin deficits to continue

India is also burdened by a twin deficit (i.e. fiscal deficit and current account deficit) which poses a substantial threat to long-term economic stability and growth.

India’s fiscal deficit stood at 5.63% for fiscal 2023/24. According to Moody’s, the smaller mandate for Modi raises the risk of more populist spending to consolidate political support. This would likely lead to a sustained high fiscal deficit and negatively impact economic stability via increasing cost of borrowing.

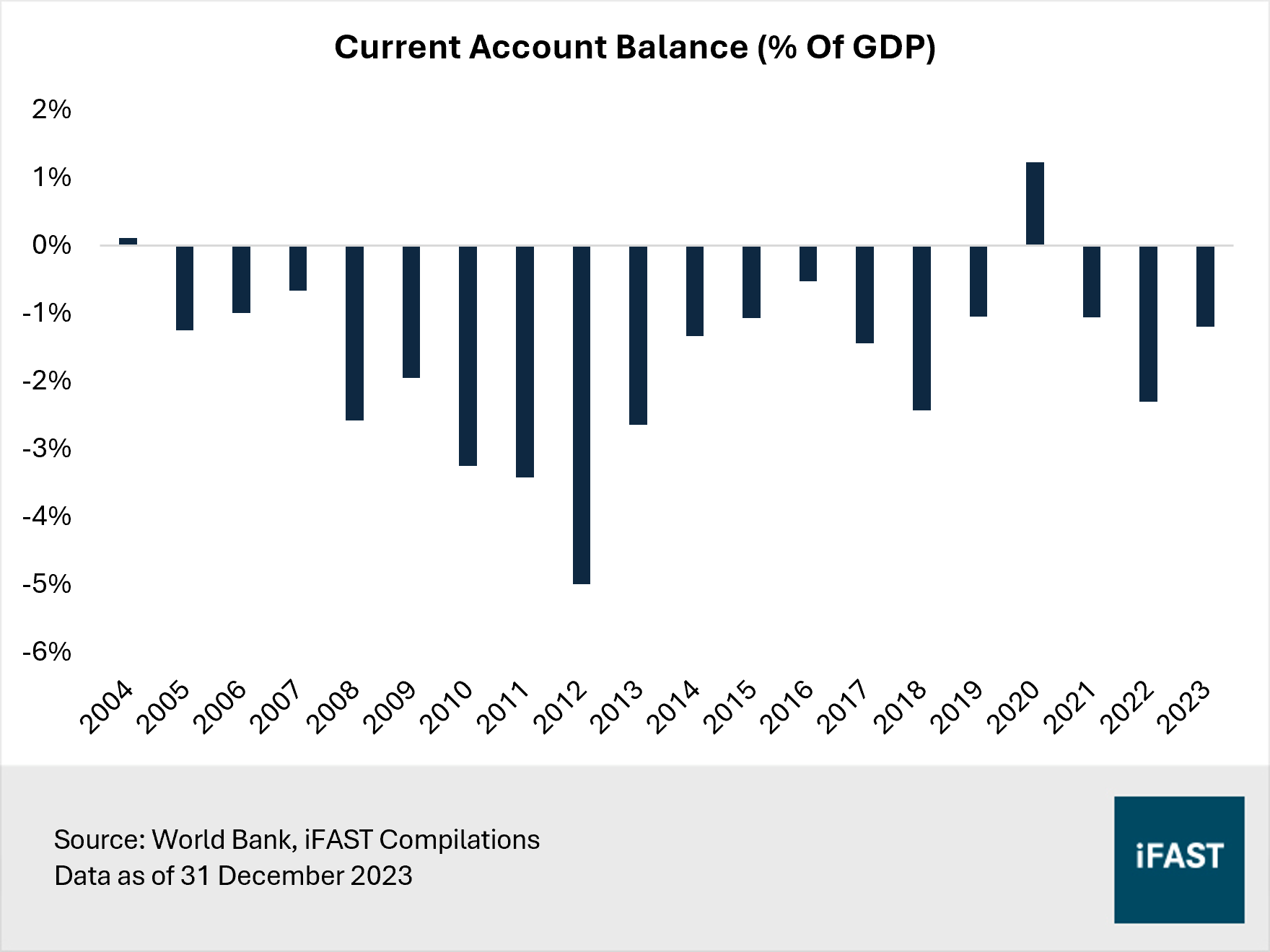

Meanwhile, India has a chronic current account deficit largely due to its high import dependency for energy and gold (Figure 4). As the world’s third-biggest consumer of oil, India is particularly vulnerable to higher crude prices.

Figure 4: India’s current account has persistently been in deficit

We anticipate energy prices to remain higher-for-longer due to escalating tensions in the Middle East which threaten global oil supply. Additionally, in June, OPEC+ agreed to extend most of its oil output cuts into 2025, further constraining supply in the market. Consequently, India’s current account deficit is likely to widen moving forward.

A widening deficit, in turn, creates a spiral effect that weakens the Indian rupee. In the last decade, the Indian rupee has depreciated at an average rate of 4% annually against the US dollar. The weakening of the Indian rupee would further intensify pressure on the current account deficit as it raises the cost of imports. Managing this currency fluctuation presents an additional challenge in balancing the current account, potentially impacting long-term economic growth.

Overall, coupled with the high youth unemployment rate mentioned earlier, these issues underscore the importance for comprehensive reforms in India in order to fully capitalise on the country's potential as an economic powerhouse that can come close to China. Following the recent election results, we will be looking towards the Indian government's ability to enact such positive changes.

We see little upside potential for Indian equities

Following the surprise election results, we expect to see increased volatility in Indian equities in the near term. While India’s business-friendly policy is expected to continue, the focus remains on India’s priority and whether the country’s structural challenges like high youth unemployment rate and twin deficits would be addressed. It remains uncertain whether Modi’s ambitious economic growth targets can be achieved. India’s potential role in the global semiconductor supply chain is also in question given the country’s lack of a highly skilled and productive workforce.

Besides, we believe that the upside potential of Indian equities is currently constrained by elevated valuations. They present risk of a market correction if future economic and earnings growth fail to meet expectations.

Based on our fair PE ratio of 19X, we project a 2026 target price of nearly 77,600 for the Sensex Index (Table 1). This translates to an upside potential of only 1% based on the closing price on 11 June 2024. As such, we maintain our Star Rating for Indian equities at 2.0 Stars “Not Attractive”.

Nevertheless, investors who still wish to seek exposure to Indian equities can adopt a dollar-costing average strategy via a regular savings plan. Our recommended products for India are the iFAST-DWS India Equity A SGD and RAMS Investment Unit Trust - India Equities Portfolio II A USD. For passive instruments, we recommend the iShares MSCI India UCITS ETF USD Acc (LSE.NDIA).

Table 1: Earnings growth for Indian equities

|

|

2023 |

2024E |

2025E |

2026E |

|

PE Ratio (X) |

25.7 |

22.6 |

19.7 |

18.7 |

|

EPS |

2,808.0 |

3,386.4 |

3,877.4 |

4,082.9 |

|

Growth |

11.4% |

20.6% |

14.5% |

5.3% |

|

Target Price (based on 19X fair PE ratio) |

77,576 |

|||

|

Potential Upside (%) |

1% |

|||

|

Source: Bloomberg Finance L.P., iFAST Estimates Data as of 11 June 2024 |

||||

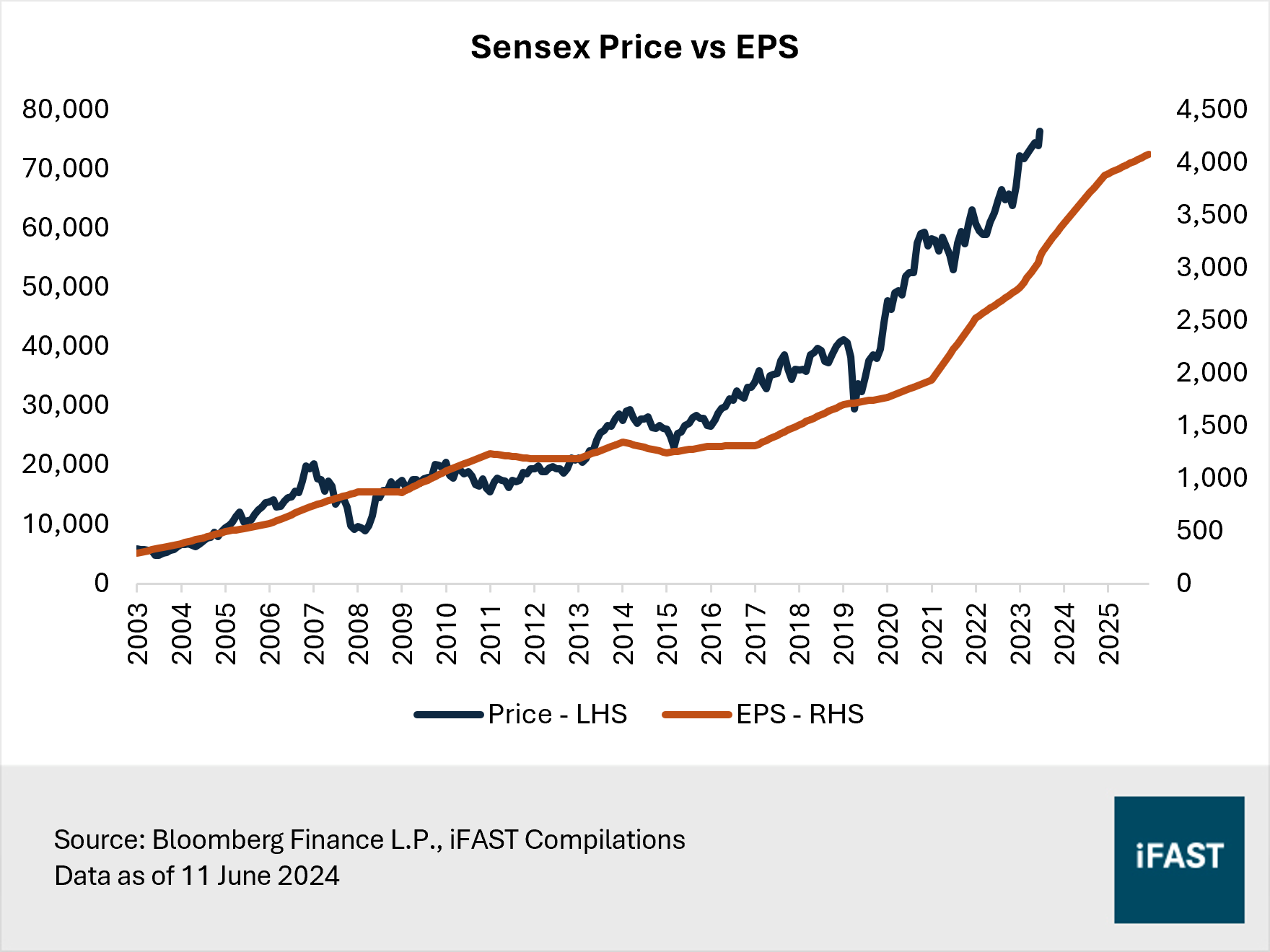

Figure 5: Indian equities have risen over the years on the back of strong earnings growth

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.