- Amidst the broad and rapid depreciation of the JPY, there is growing anticipation that Japan could take action to stabilise the yen and potentially reverse its downward trajectory.

- Moving forward, the cessation of negative interest rates and the strengthening of the Japanese economy may gradually restore the JPY's safe-haven appeal.

- In our view, the BOJ is likely to raise interest rates again this year. Moreover, the removal of a reference to its monthly government bond purchases should pave way for quantitative tightening.

- With historic lows in yen valuation and the abovementioned factors acting as drivers, we believe the yen is poised for a turnaround.

- Investors should consider an unhedged exposure when investing in Japan.

As the resilient US economy pushed back expectations of Fed rate cuts, the dollar surged, exerting pressure on many other currencies. Notably, the Japanese yen (JPY) bore the brunt of this trend. The yen sell-off continued as the Bank of Japan (BOJ) kept rates unchanged at a range of 0% to 0.1% in its recently concluded April policy meeting, following the cessation of its negative interest rate policy just one month prior. Consequently, the yen has plummeted to fresh lows against the dollar since 1990.

Following this extended decline, we believe that the yen has now become too cheap to ignore. We maintain an optimistic outlook on the currency, seeing that it is poised to break out of its long slump.

Yen intervention is becoming increasingly likely

The yen weakness extends beyond its decline against the dollar, encompassing major currencies like the euro and the Australian dollar as well. Recently, the euro-yen exchange rate reached its highest level since 2008, while the yen softened to a decade low versus the Australian dollar.

In light of the broad-based and rapid depreciation of the JPY, Japanese authorities have issued repeated verbal warnings to stem further declines. Japanese finance minister Shunichi Suzuki expressed strong concerns about how a falling yen pushes up import costs. While a weaker yen can boost exports, it also has the adverse effect of increasing the cost of living for households, potentially offsetting the benefits of wage gains.

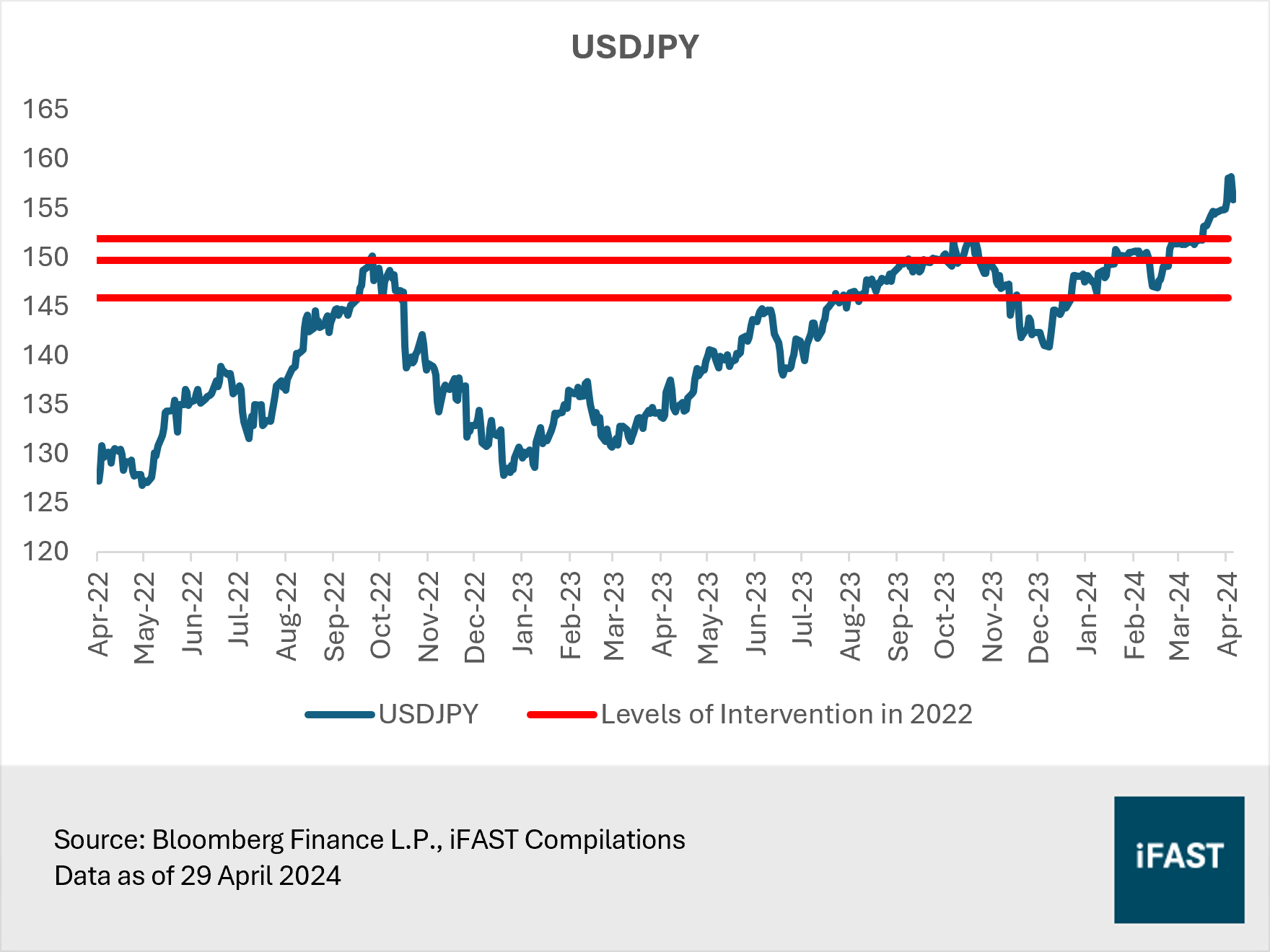

Despite verbal warnings, the JPY continues to depreciate, prompting Japan to consider taking action to stabilise the currency and potentially reversing its downward trajectory. Authorities are likely to take decisive action akin to their last interventions in September and October 2022. At that time, the yen had weakened to an intraday high of nearly 152 versus the dollar (Table 1).

Table 1: Yen intervention in 2022

|

Date |

Intervention Amount |

Yen’s low |

Yen’s high |

|

22-Sep-22 |

JPY 2.8 trillion |

145.90 |

140.36 |

|

21-Oct-22 |

JPY 5.6 trillion |

151.95 |

146.23 |

|

24-Oct-22 |

JPY 730 billion |

149.71 |

145.56 |

|

Based on dollar-yen exchange rate Source: Ministry of Finance, Bloomberg Finance L.P. Data as of 2022 |

|||

Today, the dollar-yen exchange rate dipped to as low as 160, surpassing previous intervention levels (Figure 1). Since the beginning of the year, the JPY has depreciated at a staggering annualised rate of 40%. One-way currency movements like this can be considered as excessive, and unlikely to be welcomed by Japan. Masato Kanda, the country’s top currency official, emphasised that the recent weakening of the yen is driven by speculation and is not aligned with fundamentals.

Figure 1: The yen has weakened pass previous levels of interventions

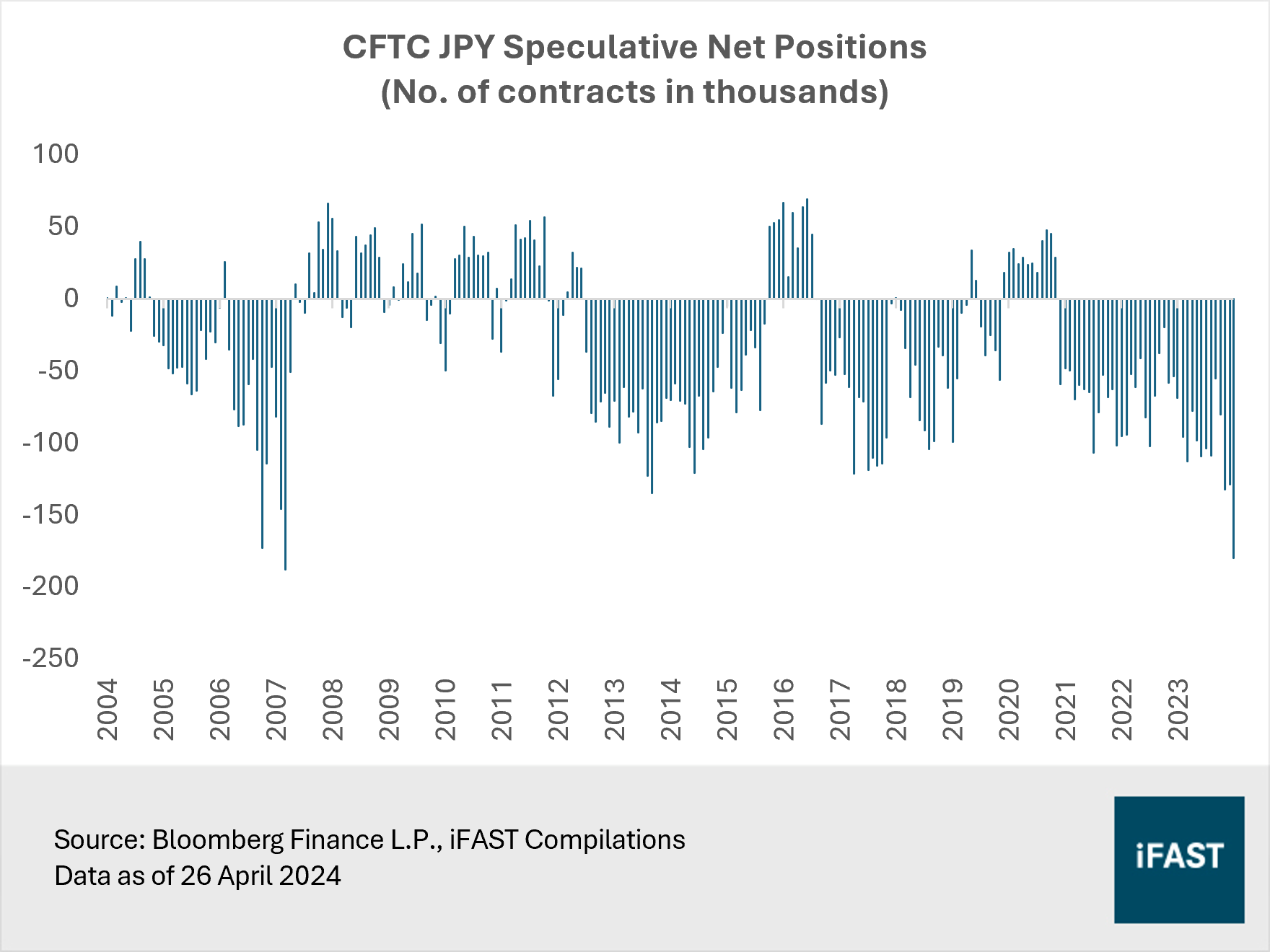

As Japan increasingly considers intervention, traders may begin to cover their short positions on the JPY as the risk-reward become less favourable. Data from the Commodity Futures Trading Commission (CFTC) showed that speculative short exposure on the JPY has reached near-record levels, making it the most shorted currency among the G10 currencies (Figure 2). Consequently, should Japanese authorities intervene, the yen is likely to rebound and stage a near-term rally.

Figure 2: Yen shorts are near record levels

Heighted geopolitical tensions could drive safe haven flows

Moreover, geopolitical uncertainty could bolster the JPY, which is traditionally considered a safe-haven currency due to its strong liquidity and stable political environment.

Recent events, such as Israel's retaliatory strike on Iran following weeks of escalating tensions between the two countries in the Middle East, highlight the growing geopolitical turmoil on a global scale. Increasing polarisation and conflicts between nations contribute to a climate of unpredictability, which could prompt investors to seek shelter in safe-haven currencies.

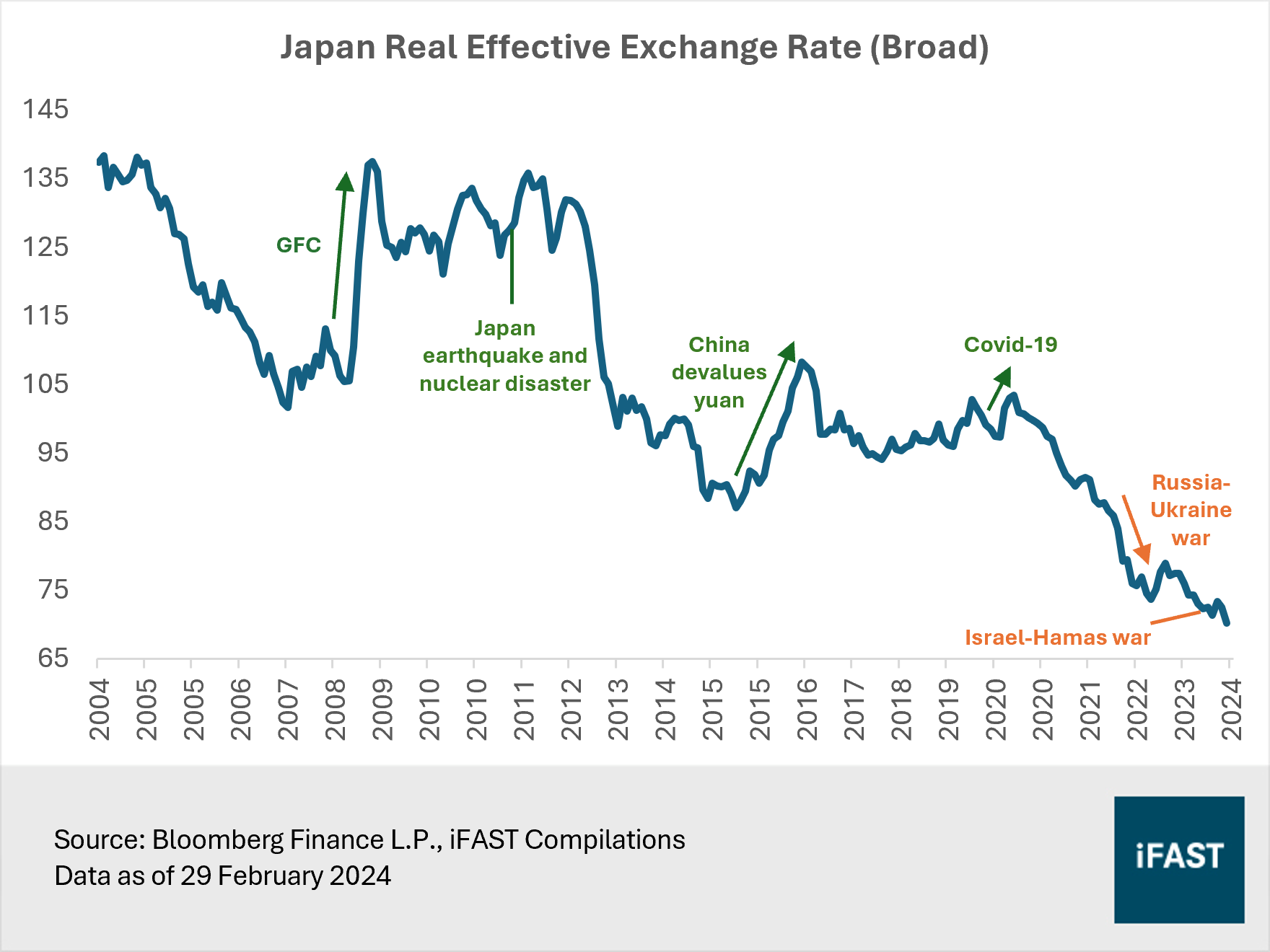

Since 2008, the JPY has appreciated in effective terms in the aftermath of various shocks such as the global financial crisis and the Covid-19 pandemic (Figure 3). However, its traditional haven status has faced challenges in recent years. The BOJ’s ultra-easy monetary policy, combined with other central banks hiking rates to combat inflation, alongside a trade deficit from high energy prices, have impacted the yen’s allure.

Figure 3: The JPY is a traditional safe-haven currency

Moving forward, the end of the negative interest rate policy and the strengthening of the Japanese economy could gradually restore the JPY’s safe-haven appeal. As discussed in previous articles, we believe the removal of negative interest rates during the March policy meeting signals growing stability and confidence in the Japanese economy, marking a departure from the era of the “Lost Decades”.

(Related article: Reasons to buy Japan and the yen after BOJ’s first hike in 17 years)

Economic conditions in Japan are showing signs of improvement and normalisation. Core CPI, which excludes volatile fresh food prices, has consistently stayed at or above the 2% target for 24 consecutive months. In response, wages have seen robust increases, with major corporations agreeing to pay hikes of 5.28% during this spring’s shunto wage negotiations – the largest increase in 33 years.

Officials are hopeful that this positive trend will lead to a virtuous cycle of rising wages and prices, stimulating consumption. February’s solid retail sales has provided some encouragement, with a year-on-year growth of 4.6% surpassing market expectations of 3% growth, and extending a healthy 24-month streak of expansion.

Higher JGB yields expected to strengthen the yen

Looking beyond near-term factors, fundamentally, higher rates should eventually strengthen the JPY. While the BOJ kept its benchmark policy rate unchanged during the April policy meeting, it continues to adopt a data-dependent approach. Governor Kazuo Ueda stated that the central bank will raise interest rates again if the longer-term rate of inflation accelerates.

The BOJ issued fresh estimates projecting inflation to remain at or above its 2% target through fiscal year 2026, signalling its readiness to hike rates. We think that positive trends for wages and prices could spur inflation expectations, potentially translating to bigger price increases and increasing the likelihood of the BOJ raising interest rates again this year.

Higher import costs could also contribute a hike. While Ueda has ruled out directly targeting yen moves in guiding policy, he mentioned that a weakening currency could push up trend inflation by boosting import prices.

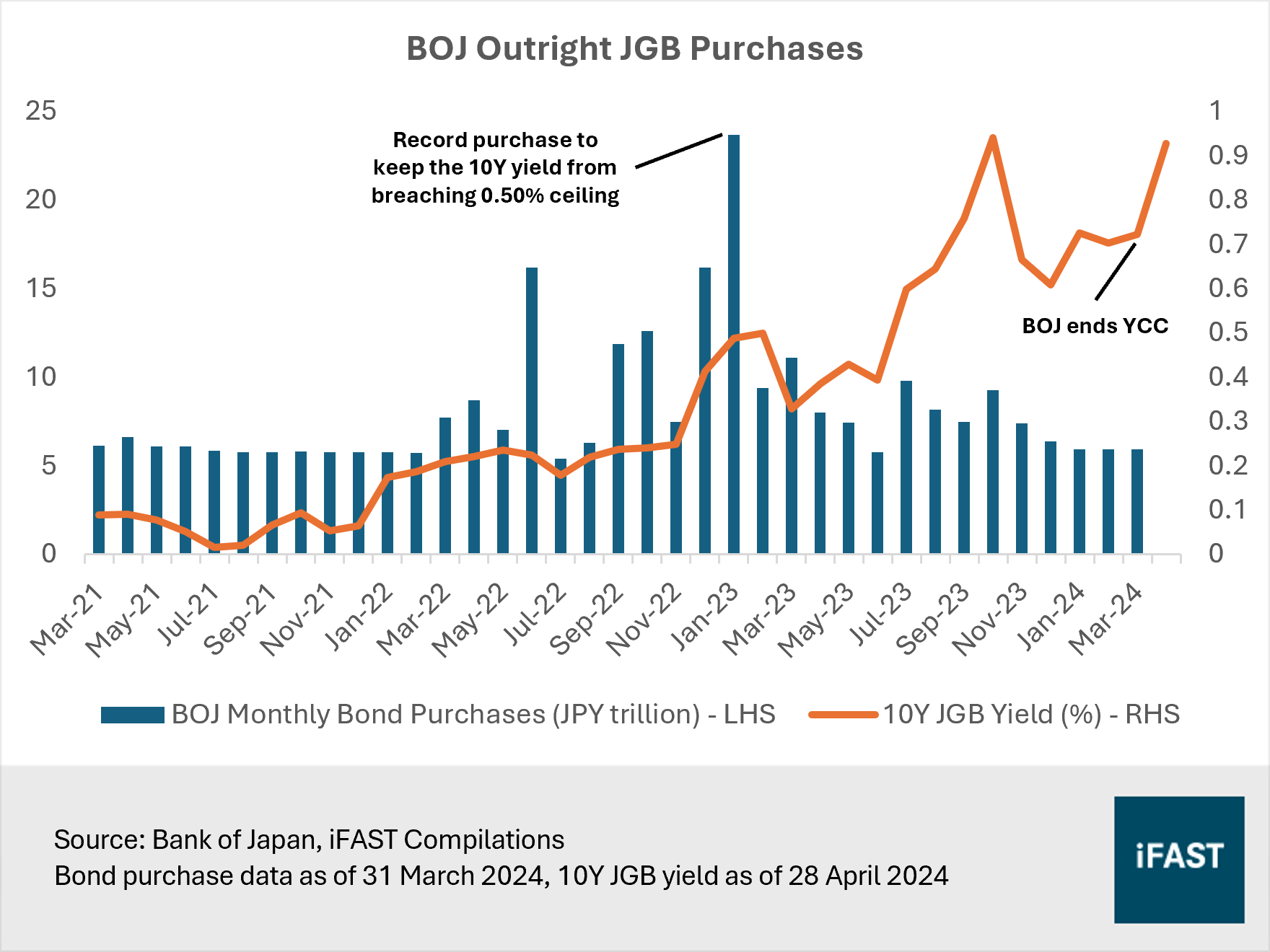

The BOJ has also removed a reference to the amount of government bonds it has roughly committed to buying each month. In March 2024, Japanese government bonds (JGBs) purchases totalled JPY 5.93 trillion (Figure 4). We think the removal of the reference paves way for the central bank to reduce its purchases of JGBs, which is a form of quantitative tightening. The impending shift will allow market forces to influence long-term interest rate and bond yields. This, coupled with further rate hikes, we anticipate more room for JGB yields to adjust upwards. Currently, the 10-year JGB yield stands at a five-month high of 0.9%.

Figure 4: JGB yields likely to rise as the BOJ cuts bond purchases

The policy divergence is poised to narrow the yield and rate differentials between the BOJ and foreign central banks, potentially resulting in an appreciation of the JPY. Major central banks like the Fed and the European Central Bank have ended their historic monetary tightening cycles, while the Swiss National Bank became the first G10 central bank to cut rates. Besides, the rate-cutting cycle in emerging economies like Brazil, which have hiked rates earlier than DM central banks, has continued steadily.

We maintain our optimistic view on the yen

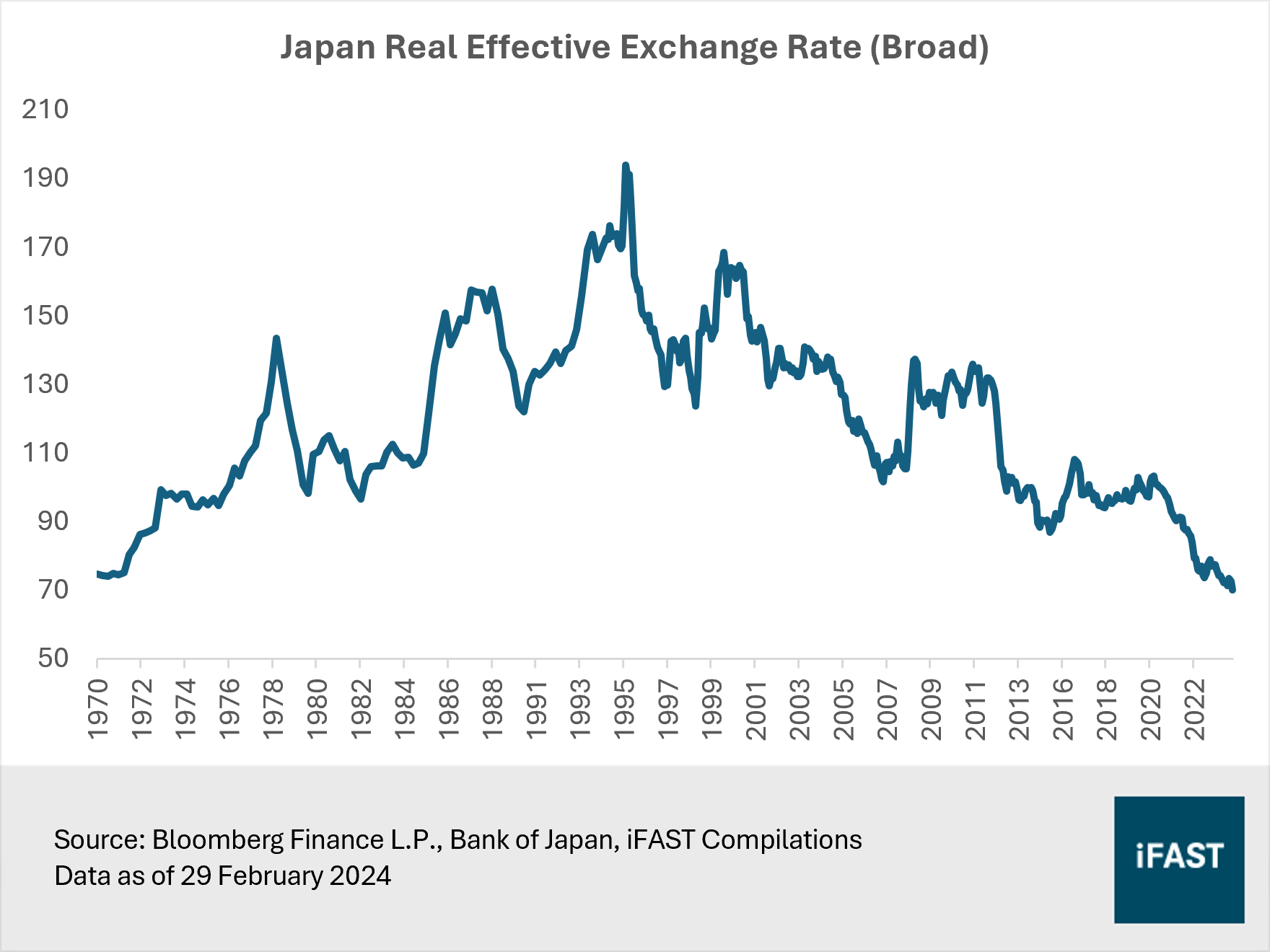

Our optimism for a stronger yen is also underpinned by the fact that the currency’s weakness has hit an extreme level. The Japan real effective exchange rate (REER), which measures the value of the yen against its peer average adjusted by consumer prices, remains at an all-time low since data inception in 1970 (Figure 5).

Figure 5: The JPY is still at its cheapest level since 1970

In our view, the historic lows in yen valuation signal an opportunity for a turnaround. Through a strategic combination of currency intervention, interest rate hikes coupled with quantitative tightening, and a gradual restoration in the yen’s safe-haven appeal, we believe the currency’s fortunes will reverse over time. As investor confidence renews, the JPY could even potentially emerge as one of the top-performing major currencies by the end of this year.

To be clear, we anticipate the appreciation of the yen against the dollar to be gradual, given our expectations of no Fed rate cuts this year. On the other hand, Japanese policymakers are unlikely to deliver rapid rate hikes, as they are mindful of the potential adverse effects on the economy.

(Related article: As we predicted, interest rate cuts are looking less likely. Here’s why)

Overall, investors can consider adopting an unhedged exposure when investing in Japan. In our view, Japan’s growth narrative is underpinned by structural factors, presenting an attractive long-term investment opportunity. Furthermore, we are confident that a strengthening of the JPY will still reach a comfortable level for exporters, supporting the equity market. At the same time, a stronger yen serves to mitigate macro headwinds, like surging import costs.

Our recommended products are the Eastspring Investments - Japan Dynamic AS SGD and the iShares MSCI Japan ETF (NYSE:EWJ). For investors who prefer to receive distributions, they may consider the Nikko AM Japan Dividend Equity JPY or Nikko AM Japan Dividend Equity SGD.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.