Capital Group is one of the world’s oldest and largest investment managers, with USD 2.3 trillion in assets under management. Capital Group stands out not only because of its long-standing investment pedigree, but also due to its distinctive multi-manager structure, where each portfolio is managed by several portfolio managers who are each responsible for and accountable to their respective portfolio segments.

In the inaugural edition of our Q&A series with Capital Group, they have provided insights into the investment processes and the multi-portfolio manager structure of the New Perspective Fund (LUX). In this edition, we further explore the factors contributing to the fund's exceptional performance in 2023 and outline its strategic roadmaps for 2024. We are delighted to once again have Capital Group share their valuable insights on this flagship fund.

Related article: Q&A Series: A global equity fund taking advantage of our fast-changing world

1. The fund has exhibited a strong performance as of November 2023, outperforming the MSCI AC World Index. What factors contributed to this outperformance?

After a challenging 2022, Capital Group New Perspective Fund (LUX) (NPF) results have rebounded robustly in 2023. The improved showing reflects the cumulative changes portfolio managers have made over the past several years, with the portfolio now more balanced by geography, sector, and style. Nearly 50% of the portfolio, for example, is invested in companies based outside of the US. NPF outpaced global equity markets following a multi-year adjustment to become more diversified.

In 2023, equity markets were very narrowly focused and driven heavily by a small number of tech-related companies – the “Magnificent Seven” of Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla. NPF has a relatively low exposure to the “Magnificent 7”. Instead of hindering results, it has highlighted just how strong our research and stock selection capabilities have been. Excess returns vs. the MSCI AC World Index were driven almost entirely by company selection, with positive contributions from nine out of 11 sectors. The thousands of stocks we actively decided not to hold in the portfolio also contributed significantly to the positive excess returns. NPF focuses on global multinationals and the additive nature of this opportunity set is apparent in recent years, as it has enabled us to avoid the impact of heightened government regulations on domestically-focused Chinese companies and the sell-off in US regional banks following the banking crisis in that industry[1].

- Refers

to the collapse of Silicon Valley Bank, Signature Bank, and First Republic Bank

from March to May 2023.

2. Could you describe the fund's investment strategy, and do you anticipate any adjustments in this strategy in 2024?

NPF is based on one of Capital Group’s most well-known global equity strategies – the Capital Group New Perspective strategy. Originally offered only in the US, the strategy is now available to investors outside of the US via this Luxembourg-domiciled fund, which is managed by the same experienced investment team and follows the same approach. The New Perspective strategy recently celebrated its 50th year anniversary, which is a testament to the longevity of its investment approach.

When first launched in 1973, the New Perspective strategy was designed to thrive on long-term investment opportunities, arising from changing patterns of global trade and changing economic and political relationships. Our observation at that time was multinational companies were well-positioned to benefit from an increasingly complex global economy due to their flexibility, adaptability, and resilience. As a result, these companies should be able to provide strong and more consistent returns. Our founding beliefs remain the same today, even if the underlying companies in the portfolio have changed.

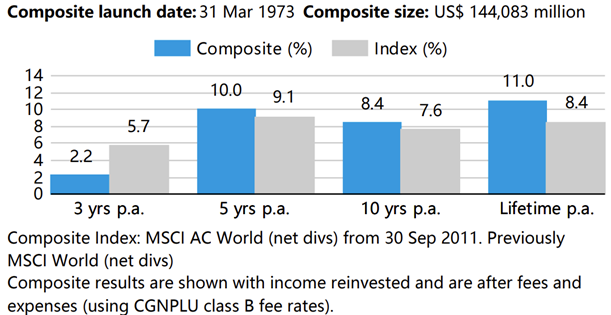

Our long-term focus on investing in multinational companies has resulted in superior outcomes for our clients over full market cycles. Over the last 50 years, the strategy has returned 11.0% per annum (p.a.) vs 8.4% p.a. for the index (Figure 1), while Capital Group New Perspective Fund (LUX) has returned 8.9% p.a. vs 8.7% p.a. for the index since its inception in Oct 2015 (Table 1).

Figure 1: Fund Performance v.s. Benchmark Performance

The investment results shown are for the Capital Group New Perspective Composite (defined as a single group of discretionary portfolios that collectively represent a particular investment strategy or objective). This is intended to illustrate our experience and capability in managing this strategy over the long term. Our Luxembourg fund has been a member of this composite since November 2015.

Table 1: Capital Group New Perspective Fund (LUX) results as at 30 November 2023 in USD terms,%

|

% |

3 years (p.a.) |

5 years (p.a.) |

Lifetime (annualised) |

|

NAV to NAV1 |

2.1 |

9.9 |

8.9 |

|

Net of sales charge2 |

0.3 |

8.7 |

8.2 |

|

MSCI ACWI3 |

5.7 |

9.1 |

8.7 |

Past results are not a guarantee

of future results.- Fund

results are shown at the share class level after fees and expenses and are

calculated as the increase or decrease in net asset value of the share class

over the relevant period.

- Includes the maximum

subscription charge of 5.25%. NAV to NAV results better reflect the pure

investment results.

- Index

is the MSCI ACWI (with net dividends reinvested).

3. The Fed proposes three rate cuts in 2024 during the FOMC meeting; however, core inflation still falls short of the 2% target. What does that mean for the equity market in 2024? Should investors re-enter the market soon or wait for more certainty on rate cuts?

We remain in an uncertain macroeconomic environment and it is impossible to say for sure when we could see a shift in US Federal Reserve (Fed) monetary policy. However, there are reasons to believe that we are close to a turning point in US interest rates, which presents a very attractive window of opportunity for investors to re-enter equity markets.

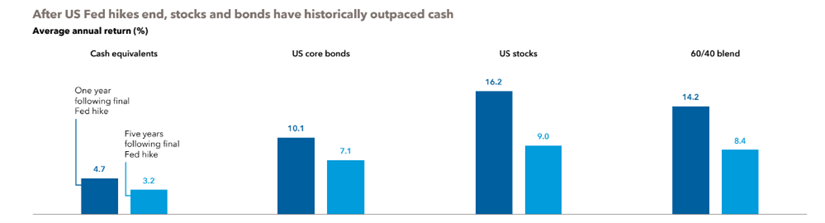

Following the last four periods when the Fed stopped raising interest rates, stocks, bonds and a blended hypothetical 60/40 portfolio (60% stocks, 40% bonds) sharply outpaced US 3-month Treasury bill returns in the first year after the last hike. Conversely, the 3-month Treasury yield, widely regarded as a proxy for cash-equivalent investments, rapidly declined an average of 2.5% in the 18 months after the last Fed hike (Figure 2). Given that no one has a crystal ball to say with 100% confidence when is the best time to re-enter equity markets, waiting could prove costly for investors. Consider a dollar cost average approach[1] to gain exposure over time.

Figure 2: Historical Asset Performance After Rate Hikes End

- Refers

to investing the same amount of money in the same security or fund at regular

intervals.

4. How will the New Perspective Fund navigate challenges in this prolonged high interest rate environment?

NPF is deliberately not positioned for a single outcome or ‘type’ of short-term market environment such as persistently high interest rates. The portfolio is designed to be well-balanced across sectors, geographies, styles and types of companies in order to be prepared for a range of outcomes. It has exposure to long-term secular growth opportunities and selected exposure to companies in more cyclical areas[1] that are backed by durable tailwinds. These are underpinned by a broad set of defensive businesses that could provide a stable foundation. The portfolio also invests in companies across a variety of industries that we believe possess strong pricing power in the context of inflation that is likely to persist beyond the ultra-low stable levels of the 2010s.

Our focus on a well-balanced portfolio and positioning for the long term rather than reacting to short-term market inflection points has delivered durable outcomes for our clients.

- Where

the underlying business generally follows the economic cycle of expansion and

recession.

5. Global equities have surged by over 15%, largely propelled by the success of the "Magnificent 7." New Perspective Fund's top 10 holdings also include tech giants like Microsoft, Tesla, Meta, and Alphabet. Do you believe that these stocks will continue to lead performance in 2024?

The extraordinary growth of the “Magnificent Seven” has certainly led the market in 2023 and resulted in a very narrow breadth of equity market leadership. NPF has relatively low exposure to these seven companies in aggregate. While the growth prospects for these seven firms may remain strong, our investment professionals are also unearthing many other companies with attractive fundamentals across a diverse set of geographies and sectors outside of US big tech.

We believe equity markets could see a greater breadth of leadership and become less one-dimensional going forward — not driven by a small set of stocks or themes such as ‘growth vs. value’, or ‘US vs. non-US’. We aim to build a deliberately well-balanced portfolio that is positioned to do well as equity market leadership broadens out.

6. Are there specific sectors / regions within your portfolio that you believe present compelling opportunities in 2024?

Health care is an area where we are seeing attractive opportunities from our bottom-up research. We believe we are in a golden era of health care innovation with companies developing new drugs and platform technologies to combat large and underserved markets such as obesity and cancer. This is particularly true in the pharmaceuticals/biotechnology space where we are focused on companies that have used technology to advance their drug research & development process. New Perspective is invested in a broad range of companies across the market capitalisation range and sub-sectors within health care, with a preference for companies with proven business models and strong pipelines.

Industrials is another area to which we have added quite meaningfully. In particular, smart industrials providing the ‘picks and shovels’ that will enable the energy transition as well as companies forming part of the solution to decarbonize the global economy could do well. Governments are making a big fiscal commitment to support infrastructure; in fact, the US government has committed almost US$1.5 trillion[1] by the end of this decade. Beneficiaries include heating and air conditioning companies focused on energy efficiency (buildings account for around 40%[2] of greenhouse gas emissions, and almost half of that is heating/aircon) as well as companies making more efficient plant machinery as demand for the electrical grid goes up.

- Data as

at 30 June 2023. Sources: White House.gov, McKinsey, US Department of

Transportation, Capital Group

- Source:

World Business Council for Sustainable Development, 31 Jan 2023

Disclaimer

All data as at 30 November 2023 and attributable to Capital Group, unless otherwise stated.

Investment involves risks. The value of your investment and income from it may rise as well as fall and cannot be guaranteed. This information has been provided solely for informational purposes and is not an offer, or solicitation of an offer, or a recommendation to buy or sell any security or instrument listed herein. This material is not intended to provide specific investment, legal, tax, financial or other advice. No consideration has been made to the specific investment objectives, financial situation or particular needs of any specific person. You should seek independent financial advice or consider carefully if the fund is suitable for you, and read the relevant Prospectus (available free of charge at capitalgroup.com) carefully before investing. This does not constitute an offer or solicitation for the purchase or sale of units in the fund. This material is issued by Capital Group Investment Management Pte. Ltd. which is regulated by the Monetary Authority of Singapore (“MAS”). This advertisement has not been reviewed by the MAS. © 2024 Capital Group. All rights reserved.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.