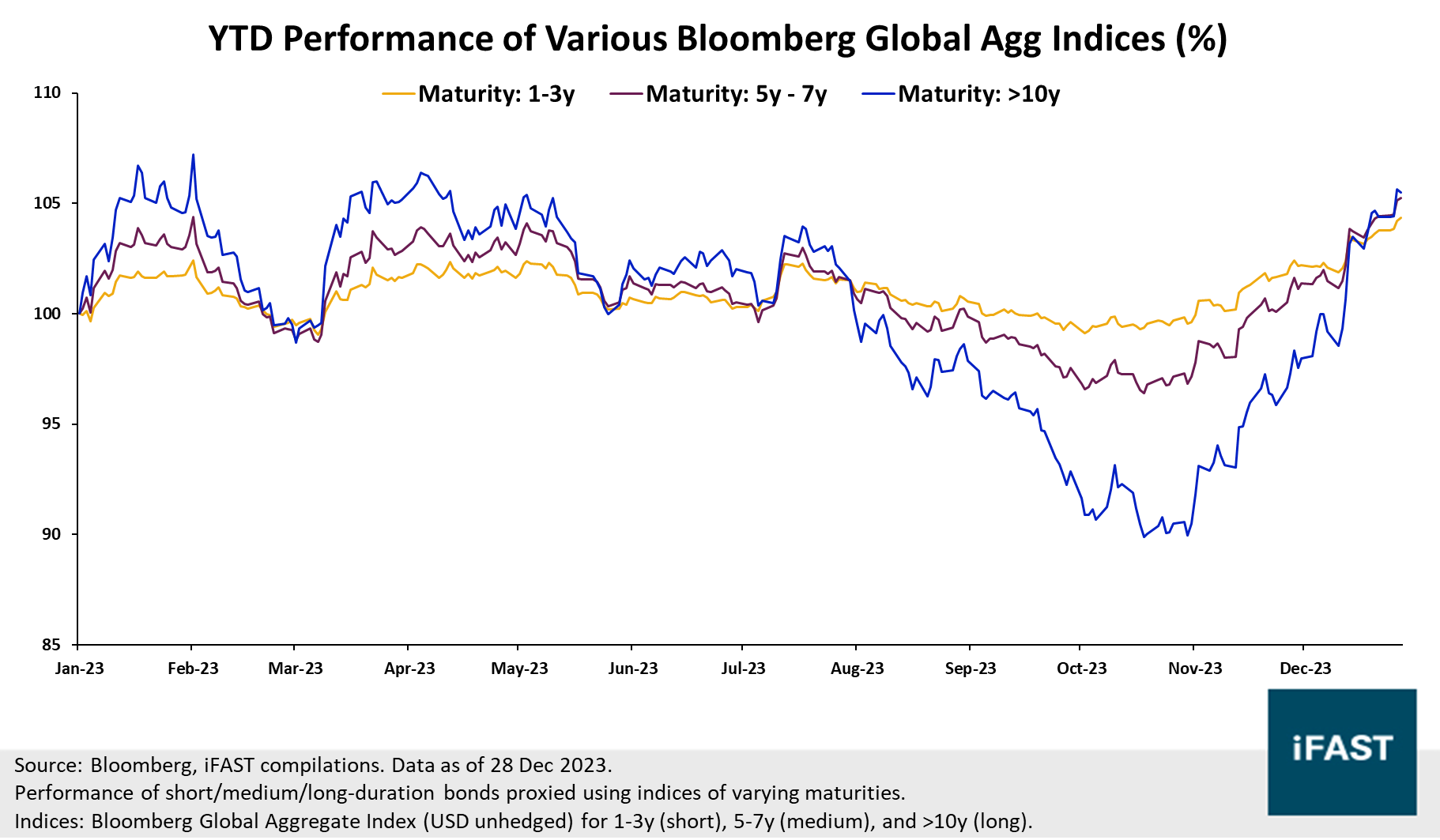

In our previous year’s Market Outlook article, we expressed a preference for short-duration over long-duration due to short-end yields looking attractive relative to longer-end yields. In the year-to-date (YTD), short-maturity bonds have generally delivered a positive performance, though they have fallen very slightly behind longer-maturity bonds following a sharp rally in the latter (Chart 1).

In this article, we do a quick recap of 2023, and provide our thoughts on what to expect for inflation and yields in 2024. We also reiterate our preference for short-duration over long-duration bonds.

Chart 1: Short-maturity bonds have generally fallen behind longer-maturity bonds in performance this year

A quick recap of 2023

2023 was a year of surprises on multiple fronts. In the US, economic growth has largely turned out better than expected, the labour market has also been remarkably resilient, and inflation has also come down significantly (Chart 2). These have led to growing calls for a ‘soft landing’ in 2024, and for some to even declare the battle against inflation already won.

Policy rate expectations have also fluctuated wildly. In the past six months, market pricing for end-2024 policy rates has gone from about 3.8% to a high of 4.8% in late-Oct, before falling back to 3.8% today (Chart 3). The increasingly dovish tone adopted by the Fed in recent months has also resulted in both short-end and long-end yields retracing downwards significantly over the past few months.

Chart 2: Key macro data points in the US

Chart 3: Implied end-2024 policy rates have fluctuated significantly over the past 6 months

Reasons to remain positive on Short Duration Bonds

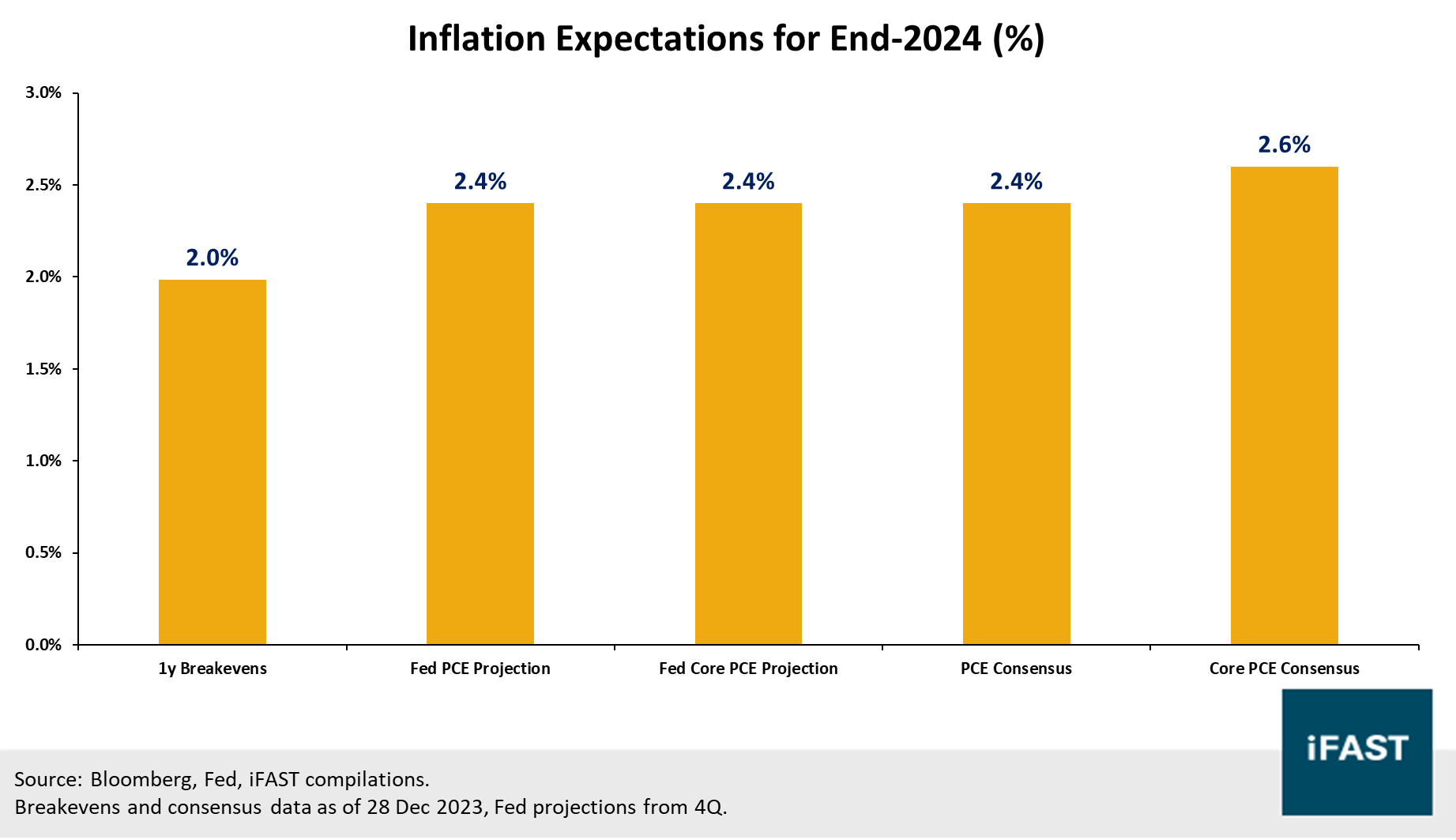

We expect inflation in the US to remain persistently elevated. In contrast, multiple metrics of inflation expectations generally point towards a belief that inflation will continue to ease in 2024 to about or below 2.5% (Chart 4) - we think these are too low and overoptimistic. While the recent decline in inflation readings has certainly been encouraging, we still expect inflation to remain firmly above the Fed target of 2%, with a heightened risk of rebounding from existing levels (e.g. 3.1% CPI reading in Nov), due to a mix of shorter-term factors like energy uncertainty as well as longer-term factors like deglobalisation.

Consequently, our base case is for the Fed to hold rates steady in 2024, contrary to market pricing today (Chart 5). If inflation continues to remain stubborn and surprise to the upside, policymakers may opt to remain hawkish for longer than markets may be expecting, which could ultimately lead to a repricing of yields higher again in 2024. Considering that longer-duration products are generally more sensitive to changes in yields, we continue to discourage the addition of excessive duration exposure at this point.

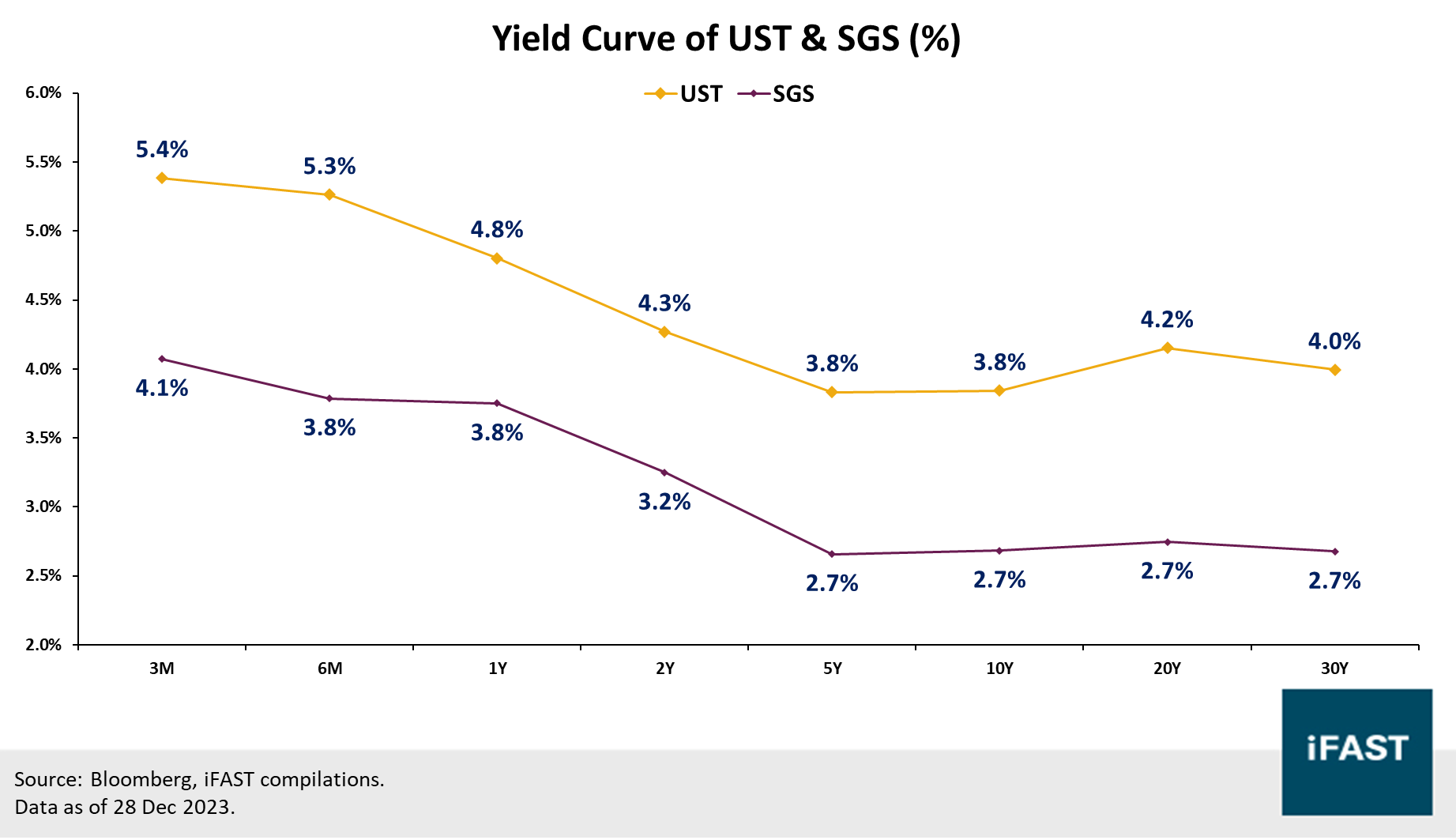

The good news for investors is that short-end yields are expected to remain anchored at attractive levels for some time. Short-end yields (of 2y USTs and SGSes) are now at about 4.3% (UST) and 3.3% (SGS), compared to several years ago when they were much closer to zero (Chart 6). We think that our forecast of higher-for-longer rates in 2024 should result in even greater anchoring of these short-end policy-sensitive yields.

Chart 4: Inflation expectations generally point towards inflation coming down by end-2024

Chart 5: Markets are pricing in 6 rate cuts by end-2024

Chart 6: Short-end yields look much more attractive today relative to several years ago

When should you add duration?

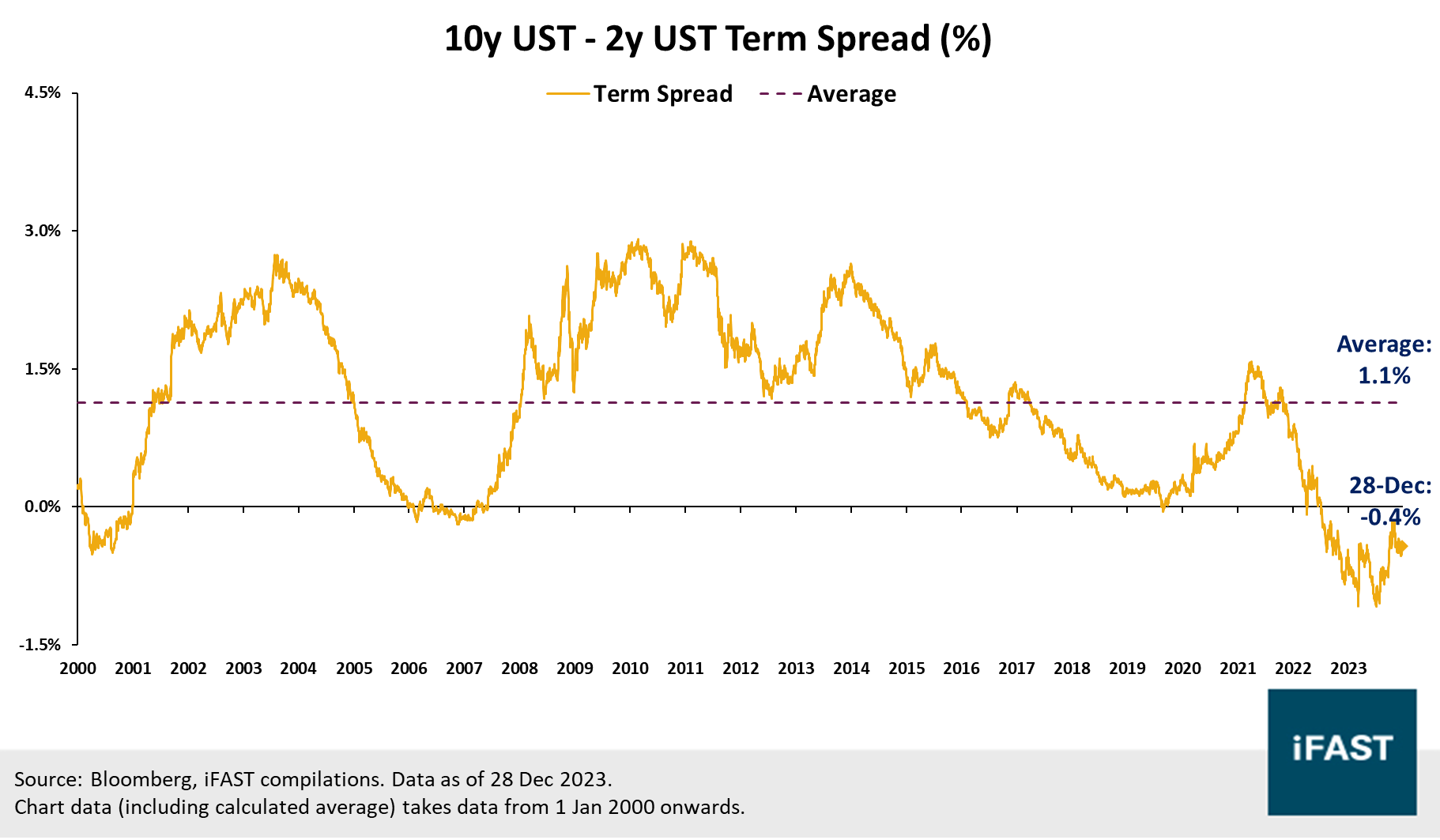

We would ideally need to see a dis-inversion of the yield curve before we turn more positive on duration. Currently, investors are essentially getting paid less (lower yields) despite taking on higher duration and maturity risks (for most tenors) (Chart 7). For instance, the term spread for USTs (10y – 2y) currently sits at -0.4% with this inverted curve, much lower than the historical average of +1.1% (Chart 8). Coupled with our view that shorter-end yields should remain anchored, we see room for longer-end yields to increase in 2024 before investors consider adding duration.

Our forecast of a growth rebound next year (including within the US) should also help to put upward pressure on nominal yields. For instance, a persistently robust labour market would directly result in wage inflationary pressures, particularly in terms of services inflation. In addition, a growth rebound would mean that the Fed would have less incentive to stimulate the economy through rate cuts, especially with inflation still hovering above the 2% target. Overall, we see room for long-end yields to rise in 2024 if the US economy remains resilient.

Chart 7: UST and SGS yield curves remain deeply inverted

Chart 8: Current term spread is significantly below historical average of 1.1%

Recommendations

To summarise, we expect both inflation and rates to remain elevated for some time, more than what markets may be pricing in or expecting themselves. We also think that longer-end yields may reverse higher in 2024, and prefer to wait for at least a curve dis-inversion before adding duration.

For a short-duration exposure to fixed income, our primary fund recommendations are the Nikko AM Shenton Short Term Bond Fund and the United SGD Fund. Both funds have a similar objective of preserving capital while achieving outperformance over a cash-based benchmark, through investing in global investment-grade bonds. These funds have relatively attractive portfolio yields (Nikko AM: 5.48% / United SGD: 4.82%); more importantly, they also generally keep their duration exposure fairly limited (Nikko AM: 0.96y / United SGD: 1.12y). For a deeper look into both funds, please check out our recent article below.

Alternatively, investors may also consider a cash-like portfolio, which could potentially offer an even shorter-duration exposure to fixed income. On this front, we first recommend our various Auto-Sweep facilities as a low-risk and high-liquidity (same-day usage of monies for investments) option. Alternatively, investors can also customise their very own cash-like portfolio using the available funds on our platform – we provide some ‘model’ portfolios for SGD (Table 1) and USD (Table 2) as a starting point below.

Related article: Cash Management: Attractive yields on your idle cash

Table 1: Model SGD cash management portfolios

| Risk Profile | SGD Auto-Sweep | Conservative | Moderate | Aggressive |

| Constituents | 35% Fullerton SGD Cash Fund

25% LionGlobal SGD Enhanced Liquidity Fund

25% United SGD Money Market Fund

15% Cash |

80% Fullerton SGD Cash Fund

20% United SGD Fund |

50% Fullerton SGD Cash Fund

25% United SGD Fund

25% LionGlobal Short Duration Bond Fund |

25% Fullerton SGD Cash Fund

25% United SGD Fund

25% LionGlobal Short Duration Bond Fund

25% Fidelity Enhanced Reserve Fund |

| 3-year Annualised Return | 1.6% | 1.4% | 0.9% | 0.2% |

| 3-year Annualised Volatility | 0.1% | 0.3% | 0.6% | 1.2% |

| Return / Volatility | 15.5 | 9.6 | 6.1 | 2.9 |

| Max Drawdown (past 3 years) | N/A | -0.9% | -3.0% | -5.6% |

| Net Yield* | 3.242% (as of 26 Dec) | 3.94% | 4.29% | 4.75% |

| Duration (years) | 0.1 | 0.3 | 0.8 | 0.9 |

| Platform Risk Rating | 0.3 | 0.4 | 1.0 | 1.8 |

| Time required to use funds | Immediate for investments T+1 for redemptions |

Fullerton: T+1 United: T+4 |

Fullerton: T+1 United: T+4 LionGlobal: T+3 |

Fullerton: T+1 United: T+4 LionGlobal: T+4 Fidelity: T+3 |

| Source:

iFAST compilations. Data as of latest available factsheets / data from

fundhouses. *Inclusive of fund-level fees (e.g. expense ratio), but excludes platform fee. **Fullerton only provides an average maturity for their fund which we use for our duration calculation (will slightly overestimate duration). |

||||

Table 2: Model USD cash management portfolios

| Risk Profile | USD Auto-Sweep** | Conservative | Moderate | Aggressive |

| Constituents | 90% iFAST USD Enhanced Liquidity Fund

10% Cash |

80% Nikko AM Shenton Short Term Bond

Fund

20% Fidelity Enhanced Reserve Fund |

50% Nikko AM Shenton Short Term Bond

Fund

25% Fidelity Enhanced Reserve Fund

25% Maybank Enhanced Income Fund |

25% Nikko AM Shenton Short Term Bond

25% Fidelity Enhanced Reserve Fund

25% Maybank Enhanced Income Fund

25% LionGlobal Short Duration Bond Fund |

| 3-year Annualised Return | N/A (Portfolio launched on 3rd July 2023) | 0.7% | 0.6% | 0.4% |

| 3-year Annualised Volatility | N/A (Portfolio launched on 3rd July 2023) | 1.1% | 1.3% | 1.4% |

| Return / Volatility | - | 1.1 | 0.8 | 0.5 |

| Max Drawdown (past 3 years) | N/A | -8.0% | -7.9% | -7.7% |

| Net Yield* | 4.775% (as of 26 Dec) | 5.21% | 5.26% | 5.30% |

| Duration (years) | 0.4 | 0.9 | 0.9 | 1.1 |

| Platform Risk Rating | 2.7 | 2.2 | 2.3 | 2.8 |

| Time required to use funds | Immediate for investments T+0 for redemptions |

Nikko: T+2 Fidelity: T+3 |

Nikko: T+2 Fidelity: T+3 Maybank: T+4 |

Nikko: T+2 Fidelity: T+3 Maybank: T+4 LionGlobal: T+4 |

| Source:

iFAST compilations. Data as of latest available factsheets / data from

fundhouses. *Inclusive of fund-level fees (e.g. expense ratio), but excludes platform fee. **USD Auto-Sweep was only recently incepted and does not have 3 years of historical data. |

||||

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the securities mentioned in this article.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.