• A narrow rally led by big tech stocks does not necessarily mean trouble as these companies have strong moats, pricing power and a global business model.

• We continue to prefer big tech companies over their smaller and less profitable peers, due to their stronger balance sheets, ability to refinance and treasure trove of cash.

• Recovery in the advertising space is uneven, and big tech companies once again demonstrated their resilience and rebounded faster.

• Within the cloud space, market leaders continue to dominate while smaller players are left vying for a smaller piece of the pie.

• We maintain a 2.5 Stars “Neutral” rating for Digital Economy. Investors can expect an upside potential of about 23.3% by the end of 2025 for the Invesco NASDAQ Internet ETF (NASDAQ: PNQI).

Narrow rally does not necessarily mean trouble

After the strong rally this year, the seven largest stocks (Apple, Microsoft, Amazon, Nvidia, Alphabet, Tesla, Meta) now form up about 28% of the total value of the S&P 500 Index, up from roughly 20% at the start of the 2023. With these select few companies forming up a large part of the index, investors are getting increasingly worried whether such performance extremes could result in trouble, especially when they look back at history and compare to past technology bubbles.

However, the case for the big tech companies of today is extremely different, and the outlook for these companies continues to remain strong, supported by their strong moats, pricing power and global business models, which can be seen from their recent quarterly earnings.

Furthermore, the strong gains this year is also a result of the relatively larger selloff in big tech stocks in 2022. Therefore, even with the narrow rally, it does not necessarily serve as an impediment for further gains.

Related article - Picking the winners within the technology sector as challenges lie ahead

Preference for big tech over smaller and unprofitable companies

Within the technology sector, we continue to prefer big tech names over smaller, unprofitable companies, due to their stronger balance sheets and revenue streams. At today’s interest rate levels, smaller companies may find it difficult to borrow money or repay their debt, impeding their ability for further research and development (R&D), or their ability to expand.

While interest rates may not increase much more from today’s levels, or at the pace in the past year, they are likely to remain higher for longer, as there are structural forces at play which are causing inflation to remain elevated. Moreover, a resilient labour market adds to the worries that inflation may remain entrenched, which makes rate cuts unlikely in the near term. Under such conditions, big tech companies will be more resilient as they are able to tide through the higher for longer interest rate environment much better than their smaller and less profitable peers.

Related article – How long will it take for inflation to hit 2%? Hint: much longer than you think

The small tech companies’ relatively lower stability compared to larger companies also means that their credit rating is likely to be worse off, meaning higher borrowing costs to take into account their higher insolvency risk, further diminishing their standing in the competition as their cost of capital increase. As for the unprofitable companies, they face an even more difficult problem as their growth rates decelerates with slowing consumer and corporate spending, making their sustenance an issue.

Meanwhile, big tech companies do not face the same problem as they have a treasure trove of cash (Figure 1). In fact, these companies are so flush with cash that they are capable of paying off their debt instantly. Even though it may seem that Amazon has a lot of total debt, its earnings before interest and taxes (EBIT) can cover its interest expense nine times over, thus making its debt unthreatening. As the technology sector continues to consolidate, smaller and unprofitable companies would either go down under, or get acquired by the larger companies.

Figure 1: Big tech companies have tons of cash reserves

Adding to the fact that these big tech companies already have strong moats and pricing power, these factors mentioned above would further hinder the ability of smaller companies to disrupt the industry. Furthermore, while these big tech companies are listed and mainly operate in the US, they have a global business model, making them more resilient even if a specific country or region is experiencing slowing growth (Figure 2).

Figure 2: Revenues among big tech companies extend beyond US

Lastly, the products and services offered by these big tech companies are deeply entrenched in our everyday lives, ranging from consumers to corporates. It would be difficult to imagine how the world operates without Google, Microsoft Office or Amazon Web Services. Meanwhile on the social media front, humans are deeply connected to one another on services like Instagram and continue to communicate on WhatsApp, making Meta a stronghold in today’s world. In fact, it would be better off to imagine these big tech companies as utilities that are almost irreplaceable in today’s world.

Advertising revenue recovery is stronger among big tech companies

Ever since the most recent quarter, technology companies have witnessed a resurgence in advertising revenue. However, as all things are, not all of these technology companies are built the same, as witnessed from the stronger growth seen among the larger names (Figure 3).

Figure 3: Ad revenue is recovering slower among smaller tech companies

While many investors attribute Google and Meta as market leaders within the advertising industry who are unlikely to see further growth from their already large market share, they continue to defy the odds of naysayers and performed remarkably well. Compared to Snap or Pinterest which come off from a relatively smaller user base and lower revenues, one would expect that these companies may experience faster growth as they attempt to grab market share from the existing players within the advertising space. However, in reality, they are experiencing slower growth compared to the larger companies in the industry, which is worrying as these smaller players may face the risk of becoming outright obsolete as they lose market share and fall further behind.

Meanwhile, Meta and Amazon have guided for double digit growth on a year-on-year (YoY) basis for the upcoming quarter, while Snap has guided for -4% YoY growth and Pinterest has guided for +6% YoY growth. This indicates that market leaders are further extending their lead over the smaller players, and over a longer time frame, with an increasing number of businesses adapting to digital transformation and artificial intelligence (AI), ad spending will likely also witness an uptick.

Cloud services market dominated by a select few

The cloud market is becoming increasingly competitive as more players attempt to enter the space given the positive double digit growth outlook in the next few years. However, there are clear signs that the space is dominated by a select few players, which also happens to be the big tech companies.

According to data provided by Synergy Research Group, cloud spending grew by 18% in 2Q23 on a YoY basis and up 3% from 1Q23 on a quarter-on-quarter basis, making this the third consecutive quarter of growth. Although the current economic climate has dampened cloud spending growth slightly, the market continues to expand at a healthy rate, and is set to continue growing in the years to come.

Analysing the trend of the major players within the cloud provider market, big tech companies like Microsoft and Google continue to take market share from the smaller players and grow steadily, while Amazon maintained its long-standing market share band of 32-34% as the top player. On aggregate, the top three companies account for the large majority at around 65% of the worldwide market (Figure 4).

Figure 4: Market leaders in cloud continue to dominate the majority of the pie

This leaves the tier two and smaller cloud providers (eg. Oracle, Snowflake, MongoDB, VMware) vying for a smaller piece of the pie, which is getting increasingly competitive, fragmented and unprofitable as the smaller companies need to compete on price or superior technology, which itself requires spending through R&D. Meanwhile, the sluggish local growth in China and decoupling from the rest of the world has resulted in Alibaba losing market share.

Over the longer-term horizon, we believe that sheer size, outreach, moat and pricing power would allow the big tech companies to extend their lead over the smaller players as they face intensifying competition even as the size of the cloud market continues to expand.

Gain exposure to big tech companies via PNQI

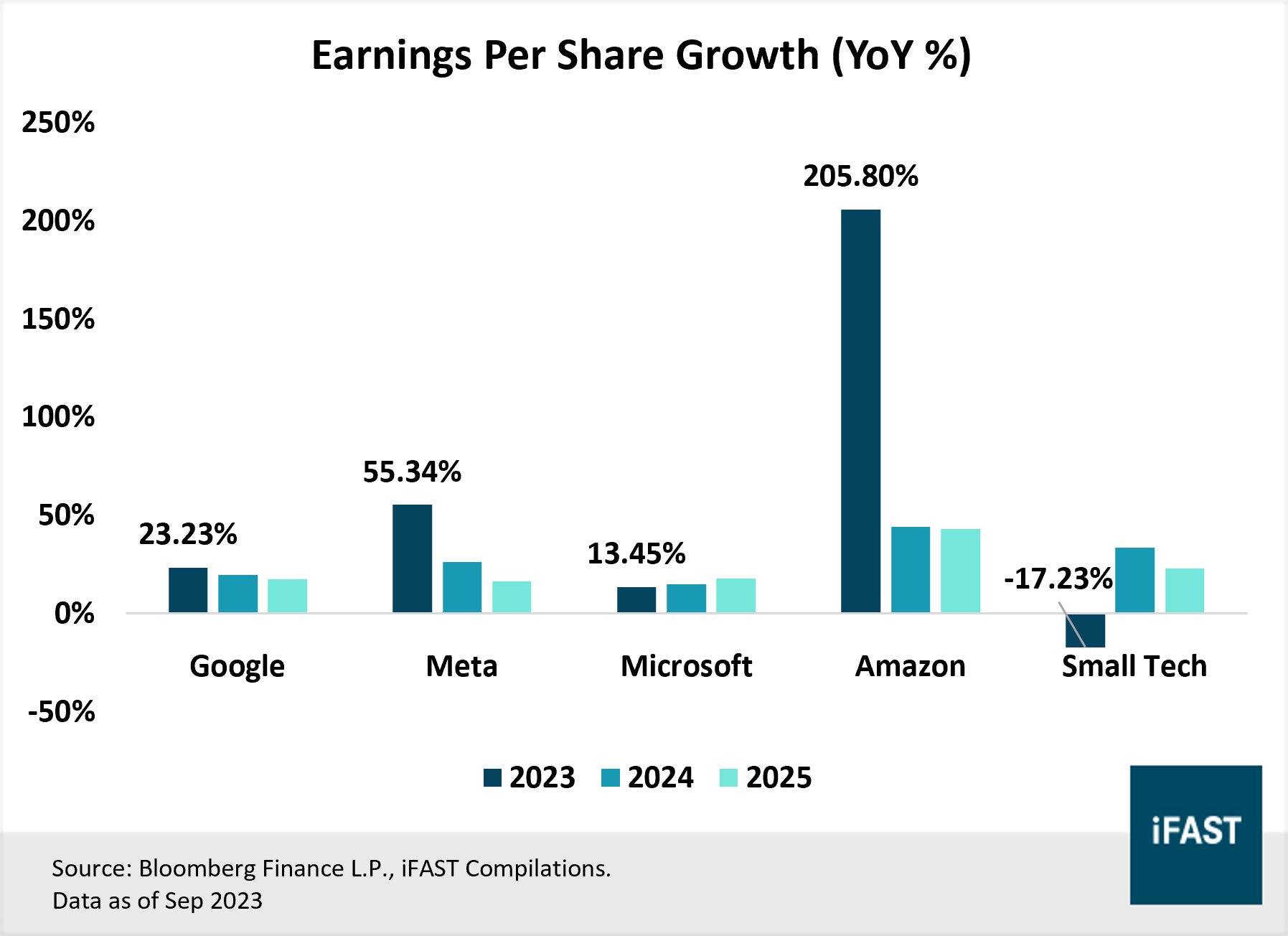

Taking a look at their consensus estimates, we observe that the earnings growth for the big tech companies exceeds that of the smaller companies, signifying that the recovery within the technology sector is uneven (Figure 5). As for Amazon, coming off a huge decline in earnings last year, there is a surge in earnings growth this year.

Furthermore, as mentioned earlier, we believe that higher-for-longer rates would negatively affect the smaller companies much more than the big tech companies due to the higher cost of capital and the lack of sufficient cash reserves. Where it stands, the consensus earnings estimate for these smaller and unprofitable tech companies may be overly optimistic and could be revised downwards, making them even more unattractive as compared to the big tech companies.

Figure 5: Earnings growth for big tech is stronger than smaller counterparts

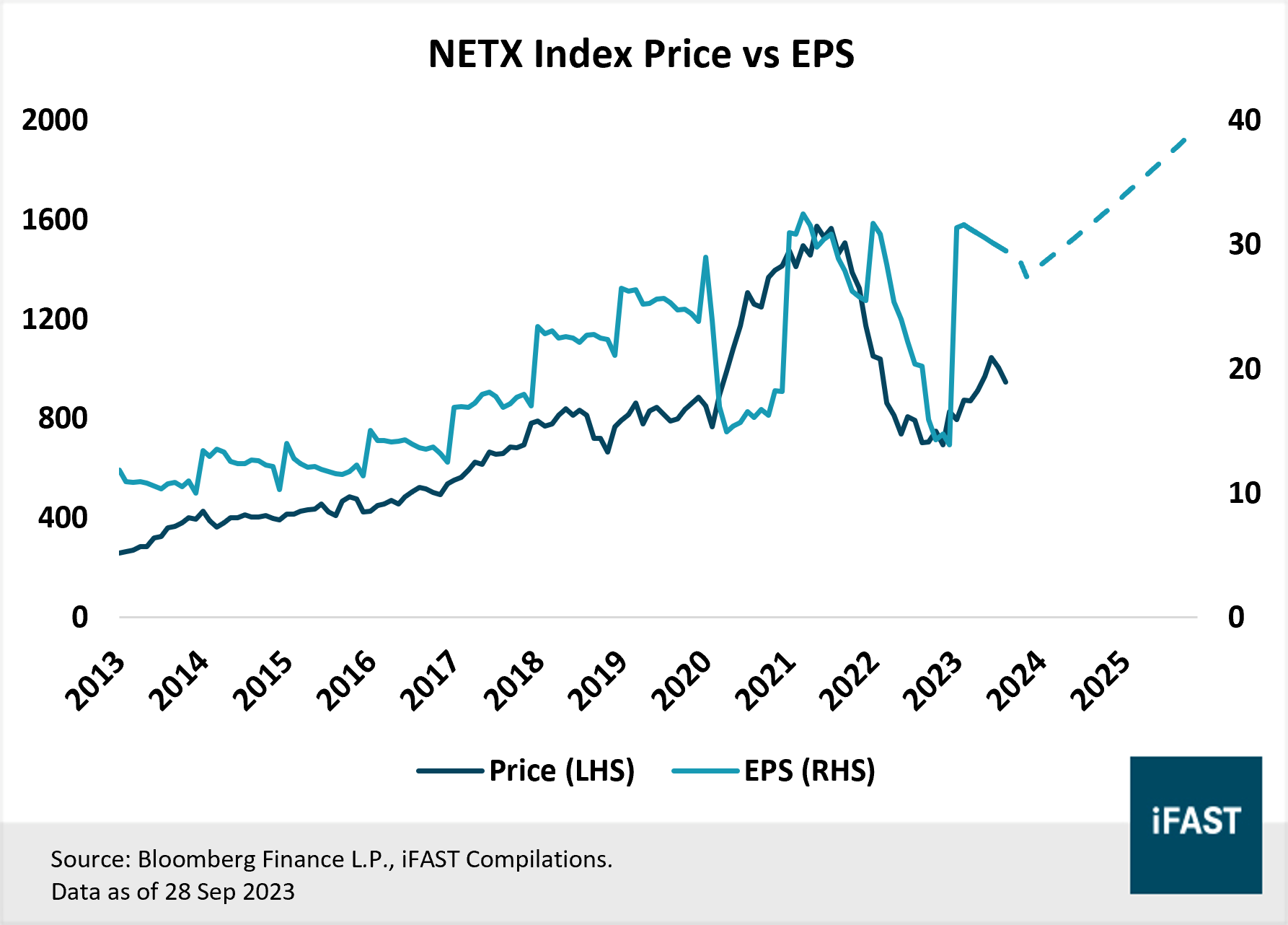

Looking ahead, while we are still positive on big tech, the technology sector as a whole still trades at an elevated PE multiple vs its historical 5-year average PE ratio despite the recent pullback in share price (Figure 6). Therefore, we choose to maintain our 2.5 Stars “Neutral” rating for the Digital Economy. Based on our fair PE multiple of 30X, we arrive at a target price of USD 38 for the Invesco NASDAQ Internet ETF (NASDAQ: PNQI), representing an upside potential of 23.3% (Table 1) by the end of 2025.

[Note: PNQI completed a 5 for 1 stock split on 17 July 2023]

Figure 6: Technology stocks still trades above its historical valuation despite the recent pullback

As the world gets increasingly digitalised, and with the adoption of artificial intelligence, the technology sector would be increasingly important as consumers and corporate incorporate these products and services into our everyday lives. What sets the big tech companies apart from the rest would be their strong moat and pricing power, which would propel their earnings growth ahead of the pack. Lastly, due to their global business models, these big tech companies deserve an allocation in any equity portfolio.

Apart from ETFs, investors who are keen to invest in technology sector via an active approach can also consider the Fidelity Global Technology A-ACC-USD Fund.

Table 1: Projections for NETX Index

|

Nasdaq CTA Internet Index |

2022 |

2023E |

2024E |

2025E |

|

PE Ratio (X) |

44.9 |

34.7 |

28.9 |

24.3 |

|

Projected Earnings Growth (YoY %) |

-20.8% |

29.4% |

20.1% |

18.8% |

|

Projected Earnings Per Share (EPS) |

21.2 |

27.4 |

32.9 |

39.1 |

|

Target Fair Price (Based on a fair PE ratio of 30X) |

- |

- |

- |

38 |

|

Potential Upside (%) |

- |

- |

- |

23.3% |

|

Source: Bloomberg Finance L.P., iFAST Estimates |

||||

Figure 7: NETX Index Price vs EPS

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.