(Note: FWD Group has since announced on 18 Sep [Mon] evening that the issuance will be cancelled. The Group has not said why the deal was cancelled.)

Important Events

FWD Group Holdings Limited (“FWD Group”) has announced a new 10Y USD fixed rate senior unsecured bond, at an initial price guidance (IPG) of T + 290bps. This translates to an approximate IPG of 7.232% (semi-annual coupon payments).

These bonds will be issued under FWD Group’s existing USD 5b Global Medium Term Note and Capital Securities Programme. The net proceeds from the Notes will be used for general corporate purposes, primarily for the refinancing of the USD 325m Senior Notes due 2024.

FWD Group recently received (on 24 Aug) its inaugural ratings of Baa2 (Positive) by Moody’s, and BBB+ (Stable) by Fitch. Its core life insurance operating entities’ insurer financial strength was also assigned a rating of A by Fitch, and A3 by Moody’s. This new issuance is expected to have issue ratings of Baa2 by Moody’s and BBB by Fitch.

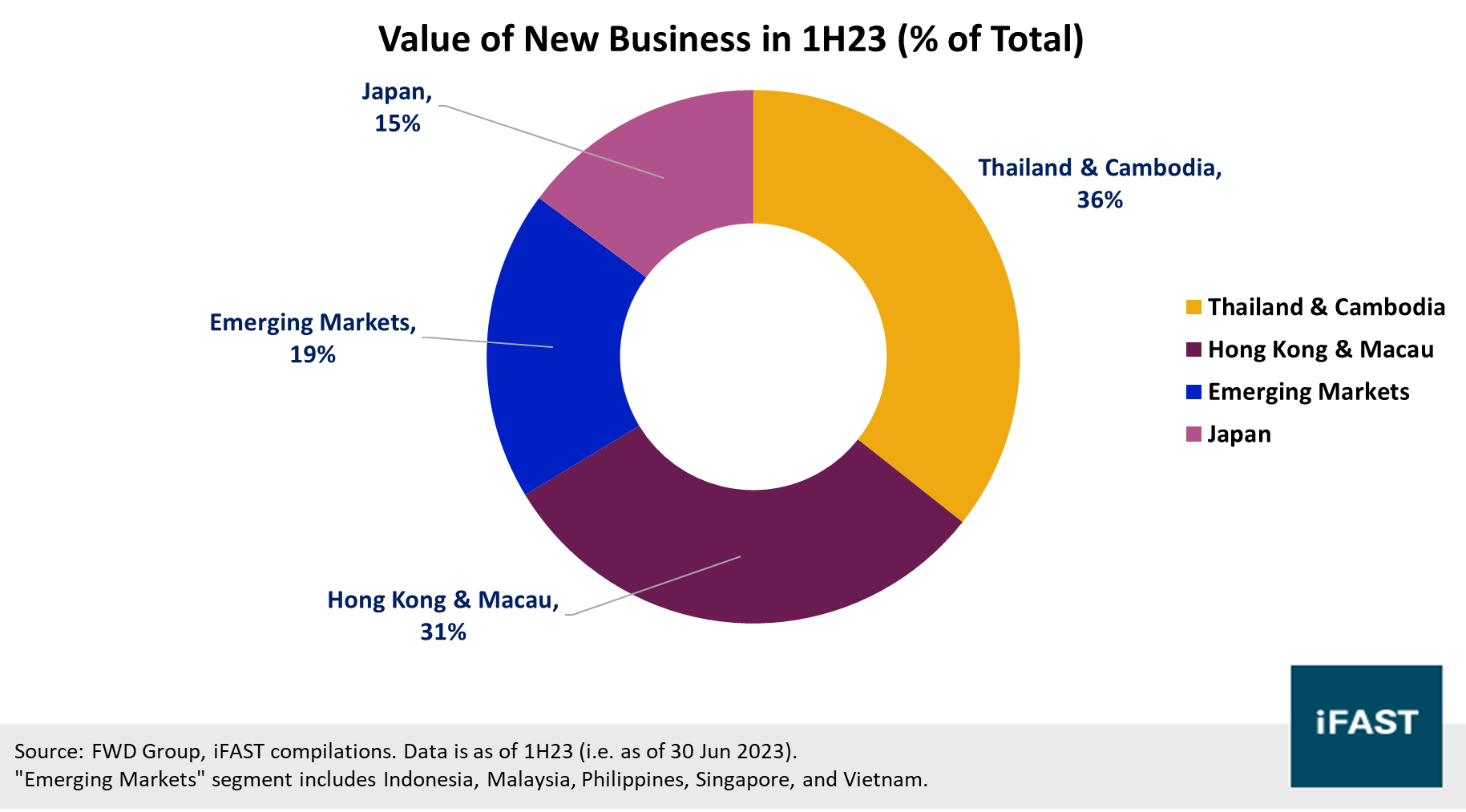

FWD Group is one of the largest insurers in Asia, with over 8m policyholders across 10 Asian markets as of 1H23 (i.e. as of 30 June 2023, as FWD Group’s financial year ends in Dec). It is well-diversified geographically across Asian markets, with a fairly equal distribution between the Thailand & Cambodia segment (36%), as well as the Hong Kong & Macau segment (31%) (Chart 1).

Chart 1: FWD Group is well-diversified across Asia

FWD Group’s recent financial results indicated strong organic growth in its core businesses. The Group made USD 845m of new business sales in 1H23 (up 19% YoY from USD 732m in 1H22), with the value of new business also climbing to USD 482m (up 22% YoY from USD 405m in 1H22). The strong jump in the value of new business was particularly driven by the Hong Kong segment following the reopening of borders with Mainland China, as well as the Thailand segment due to strong growth in the agency channel as well as bancassurance sales (Chart 2).

Chart 2: Thailand and Hong Kong were key drivers of new business in 1H23

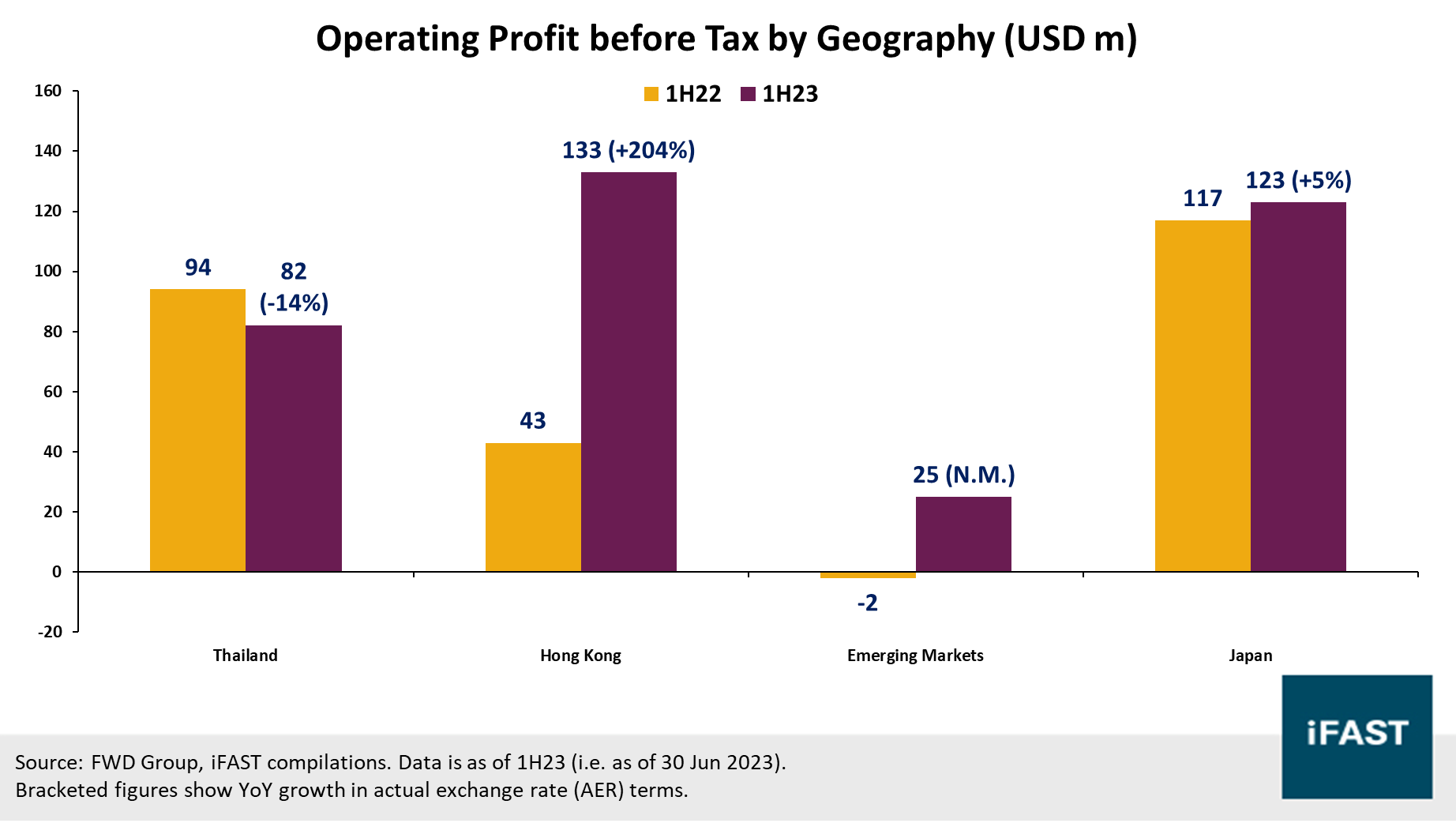

With this strong performance, FWD Group delivered USD 307m in operating profit before tax in 1H23, up 48% YoY in actual exchange rate terms from USD 208m in 1H22 (Chart 3). This was again mainly driven by a 204% YoY growth in the Hong Kong segment which was offset by a decline in Thailand operating profits as a result of higher claims expenses. Nonetheless, its two other segments remained fairly positive, including the Emerging Market segment which turned a positive profit in 1H23.

(Note: FWD Group reports figures in actual exchange rate [AER] and constant exchange rate [CER] terms. The former uses the actual exchange rates for the relevant periods, while the latter uses the average exchange rates for the relevant periods.)

Chart 3: Hong Kong in particular was a key driver of operating profit before tax

For FWD Group, pre-tax operating profit is mainly by the release of contractual service margin (CSM) – this contributed to USD 354m in operating profit in total (about 67% of pre-tax operating profit before corporate overheads). Because of the nature of CSM (i.e. released over time), this could provide greater stability to FWD Group’s profits each year.

(Note: CSM refers to the carrying amount of future profits / assets / liabilities that are yet to be earned. However, FWD Group will recognize these profits as it provides insurance contract services, and hence it will be released over time into the Group’s accounting profits.)

FWD Group’s capital and liquidity position remains sound. Its latest leverage ratio was reported at 34.3% of shareholders’ equity and 24.0% of comprehensive equity (1H23). In addition, its group-wide solvency ratio came in at 300% (an improvement from FY22’s 288%), indicating a sizeable buffer of its group-wide capital levels (USD 5,944m) over the prescribed capital requirement (USD 1,981m).

FWD Group’s investment portfolio continues to primarily comprise fixed income assets (83% of total, as of 1H23). Its fixed income assets primarily comprise a variety of bonds, including government and government agency bonds, as well as corporate bonds and structured securities. We note that a large majority of its corporate bond allocation (91%) and structured securities (99%) allocations are investment grade, mostly falling within A or BBB. These showcase a relatively prudent approach to investing and reflect the nature of FWD’s business as an insurer. On top of this, FWD Group has also done interest-rate sensitivity analyses on this solvency ratio of 300%, indicating that changes to equity prices and interest rates are unlikely to significantly reduce this ratio (Table 1).

Table 1: Interest rate sensitivity analysis conducted by FWD Group

| FWD Group (PCR basis) | 1H23 |

| Central Value | 300% |

| 10% Increase in Equity Prices | +2 pps |

| 10% Decrease in Equity Prices | -2 pps |

| 50bps Increase in Interest Rates | -1 pps |

| 50bps Decrease in Interest Rates | +1 pps |

| Source:

FWD Group, iFAST compilations. Data is as of 1H23 (i.e. as of 30 Jun

2023). PCR refers to prescribed capital requirements, which are levels below which the HKIA may intervene. |

|

We compare this new issuance with two of FWD Group’s existing bonds, maturing in Jul 2024 and Sep 2024 respectively (Table 2). Comparing this new issuance to the Jul 2024 bonds, this new issuance has a slightly lower indicative yield despite the longer maturity, though it is also ranked higher in seniority (senior unsecured versus subordinated). Comparing this new issuance to the Sep 2024 bonds, it does have a decent yield pick-up of +85bps, though investors should take note of the significant difference in maturities, which results in significantly higher duration risks for the former.

Table 2: Comparison between FWD bonds

| Bond Name | Maturity Date (Years to Maturity) |

Bond Rating by S&P / Fitch | Ask Price | Current Yield (%) |

Yield to Worst (%) |

| FWDGHD Sep2033 Corp (USD)* | 25 Sep 2033 (10.0) |

N.R./BBB | 100* | 7.232%* | 7.232%* |

| FWDGHD 5.750% 09Jul2024 Corp (USD) |

09 Jul 2024 (0.8) |

N.R./N.R. | 98.700 | 5.826% | 7.432% |

| FWDGHD 5.000% 24Sep2024 Corp (USD) |

24 Sep 2024 (1.0) |

N.R./BBB | 98.662 | 5.068% | 6.387% |

| Source: Bloomberg, Bondsupermart, iFAST

compilations. Data as of 18 Sep 2023. *Indicative figure as bond has not yet been issued. |

|||||

As a whole, we think FWD remains well-capitalised and poised for continued growth ahead. This new FWD issuance appears fairly priced and may be of interest to investors who wish to gain some yield pickup over the existing Sep 2024 bonds (both of which are senior unsecured). However, investors should remain mindful of the longer maturity and the accompanying duration risks of this new issuance.

Declaration: For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a position in FWDGRP 5.750% 09Jul2024 Corp (USD) and the analyst who produced this report holds a NIL position in the abovementioned securities.

Our podcast series, Yield Hunters, is available on Spotify, iTunes Podcasts and Google Podcasts. We share our thoughts on new bond issues and hold discussions on the fixed income space. Listen to our latest episode below and follow us!

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.

Please note that only certain bond(s) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to FSM's prevailing policies and procedures. Please read our full disclaimers in the website.