• While the US has managed to avoid a recession thus far, we expect growth to be modest in the months ahead.

• Even though conventional wisdom suggests that growth stocks tend to perform poorly as economic growth slows, businesses with quality attributes such as competitive advantages, strong pricing power, and robust balance sheets can still do well in a downturn.

• For 2023/24, we have chosen the Fidelity American Growth A-USD fund as one of our recommended funds for US equities.

• This fund seeks to deliver long-term capital growth by investing in companies which are benefitting from secular growth trends. Within an overall growth context, the portfolio managers are also valuation sensitive and aim to find the best risk/reward to implement the growth theme.

• The Fidelity American Growth fund has displayed its ability to deliver consistent outperformance over its peers while also being relatively more resilient during down markets.

Growth stocks can still thrive in a slowing growth environment

The US economy continues to defy all expectations of a recession.

According to the latest figures published by the Bureau of Economic Analysis, the US economy grew at a rate of 2.1% in 2Q23, following the first quarter’s expansion of 2.0%. The increase in the second quarter was largely driven by strong consumer spending and business investment. July saw consumer spending rising further to 0.8% month-on-month, ahead of the median consensus forecast of a 0.7% gain. Adjusted for inflation, consumer spending rose 0.6% in July – the largest gain since January - not too shabby for an economy that is supposed to enter a recession.

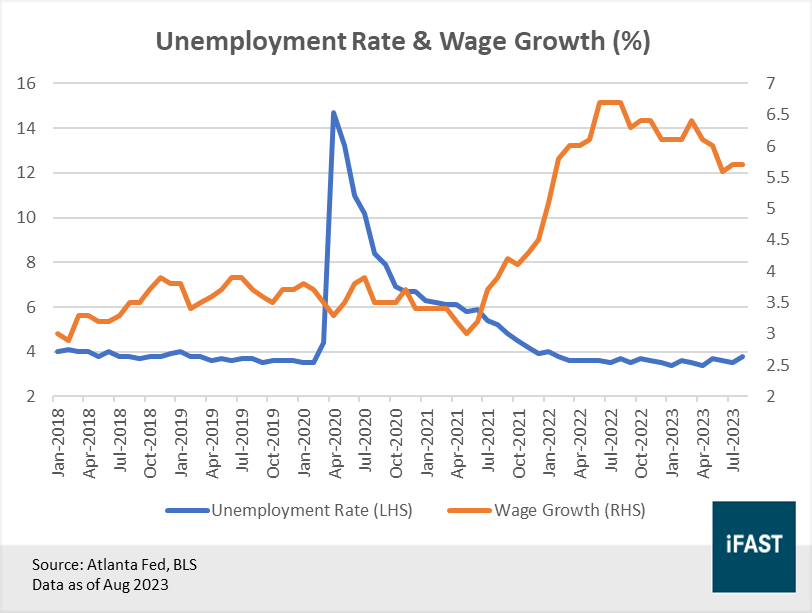

The strength of the US consumer is underpinned by a robust labour market, which has been red hot despite the Fed’s best efforts to cool it down. While the labour market has shown some signs of loosening lately - with a jump in the unemployment rate and slowing wage growth - it remains tight relative to pre-pandemic levels (Figure 1).

Figure 1: Consumer spending in the US likely to be supported by tight labour markets.

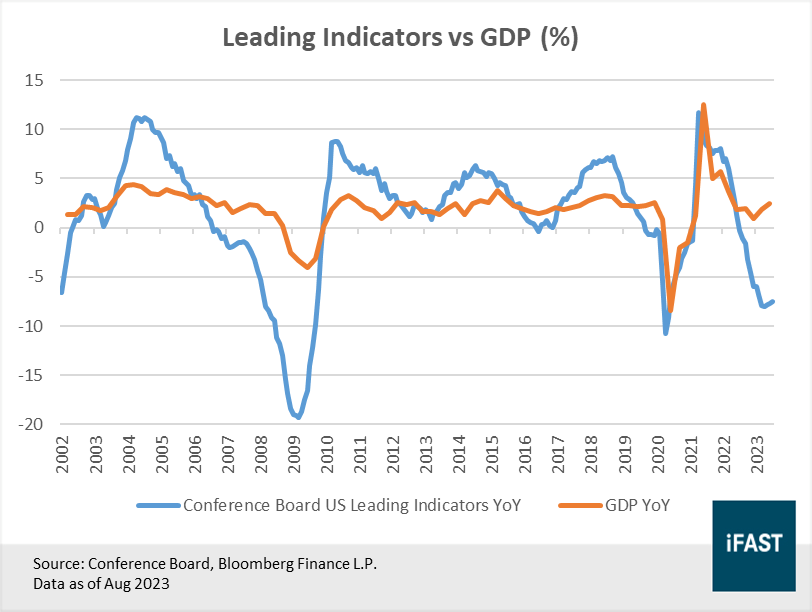

Even though the economy has held up much better than expected, headwinds are still clearly present, at least in the near to mid-term. The Conference Board’s Leading Economic Index, a composite index of 10 leading indicators is still deeply negative as of August 2023, indicating growth will likely be below trend in the months ahead.

Core inflation, measured by the core PCE price index was at 4.2% in July, more than double the Fed’s target. During the Jackson Hole Economic Symposium earlier in August, Fed Chair Jerome Powell reiterated for the umpteenth time that rates could still go higher and will likely be held at restrictive levels for an extended duration. While the US economy may be able to avoid a recession, growth is likely to be modest – an environment that does not favour growth stocks.

Figure 2: Leading indicators are still pointing towards a slowdown

Even though conventional wisdom suggests that growth stocks, especially those that are highly valued and unprofitable tend to perform poorly when economic growth slows, investors should not avoid them entirely. Businesses which exhibit quality attributes, such as those with competitive advantages (e.g a global business model), strong pricing power, and robust balance sheets can still do well in a downturn. Growth stocks may be down, but they are certainly not out.

Introducing the Fidelity American Growth Fund

After a rigorous selection process, we have shortlisted the Fidelity American Growth A-USD fund as one of our recommended funds for US equities this year. The Fidelity American Growth Fund replaces our previous recommended fund (2022) - the Allspring US Large Cap Growth Fund.

The Fidelity American Growth Fund seeks to deliver long-term capital growth by investing in equities of companies that are headquartered or do most of their business in the US. Although the fund has a flexible investment style as it takes into account the prevailing and expected macroeconomic conditions, its core investment approach is to identify companies that are most likely to benefit from secular growth trends.

The portfolio managers’ investment philosophy is that markets are driven by long-term cycles and themes, and businesses that are exposed to such themes grow their sales and earnings faster than the market. Within each of these themes - mobility, automation, demographics and electrification - they seek to identify companies that demonstrate pricing power as they are likely to outperform as they can protect/increase margins and reinvest at a higher rate of return. Within an overall growth context, the portfolio managers are also valuation sensitive and aim to find the best risk/reward to implement the growth theme.

The fund is benchmark agnostic and references the S&P 500 Total Return Net Index for comparative purposes only. There is no restriction for the fund to invest in any comparative market index sector/holdings. As a result of this unconstrained approach, the fund’s exposure may differ substantially from the benchmark. The fund holds a high conviction portfolio of between 60-80 stocks at any time.

Table 1: Sector exposure vs benchmark

|

Fidelity American Growth |

S&P 500 Index |

|

|

Healthcare |

24.5% |

13.4% |

|

Financials |

17.2% |

12.4% |

|

Consumer Staples |

11.7% |

6.7% |

|

Industrials |

9.6% |

8.5% |

|

Information Technology |

9.0% |

28.3% |

|

Materials |

6.7% |

2.5% |

|

Communication Services |

5.1% |

8.4% |

|

Consumer Discretionary |

5.1% |

10.7% |

|

Energy |

4.3% |

4.1% |

|

Real Estate |

2.5% |

2.5% |

|

Utilities |

0.0% |

2.6% |

|

Cash |

4.4% |

- |

|

Source: Fidelity Data as of 31 July 2023 |

||

Table 2: Top 10 holdings

|

Fidelity American Growth Fund |

S&P 500 Index |

||

|

Schlumberger |

3.3% |

Apple |

7.4% |

|

Astrazeneca |

3.2% |

Microsoft |

6.5% |

|

Horizon Therapeutics |

3.1% |

Amazon |

3.3% |

|

Fiserv |

3.1% |

Nvidia |

3.2% |

|

T-Mobile |

3.0% |

Alphabet A |

2.1% |

|

Renaissancere |

2.8% |

Alphabet C |

1.9% |

|

Tradeweb Markets |

2.8% |

Tesla |

1.7% |

|

Johnson & Johnson |

2.6% |

Meta |

1.7% |

|

Spectrum Brands |

2.5% |

Berkshire Hathaway |

1.7% |

|

Boston Scientific |

2.5% |

Exxon Mobil |

1.2% |

|

Source: Bloomberg Finance L.P., Fidelity Data as of 31 July 2023 |

|||

Consistent with the current environment of slowing growth and elevated inflation, the fund is defensively positioned, with sizeable overweights to traditionally defensive sectors such as healthcare and consumer staples (Table 1). Top holdings include the likes of Astrazeneca, Horizon Therapeutics as well as Johnson & Johnson (Table 2).

Johnson & Johnson is one of the world’s largest and most diversified healthcare products company, which should benefit from a recovery in elective medical procedures in the “post-Covid” era. Growth during this period is also expected to be resilient, underpinned by its pharmaceuticals and consumer health segment while is long-term growth is expected to be driven by its innovative Medtech business.

Aside from healthcare and consumer staples, the fund also has an overweight in financials, with a focus on sub-industries that are mostly unrelated to credit. The fund is currently overweight reinsurers due to the improving price cycle in the market, which is not affected by the current problems faced by banks. Reinsurers also have little to no credit risk as they invest in very short dated safe instruments. The fund is also overweight payment providers, due to the lack of credit exposure and also because of the long-term secular advantage of these businesses, as digital payments becomes more ubiquitous.

Relatively strong performance vs its peers

Over the past five years, the Fidelity American Growth Fund has outperformed its peer group by providing investors with an annualised return of 8.2%, compared to the 6.5% returns by the latter. On a calendar year basis, the fund also managed to outperform its benchmark in three of the past five years between 2018 and 2022.

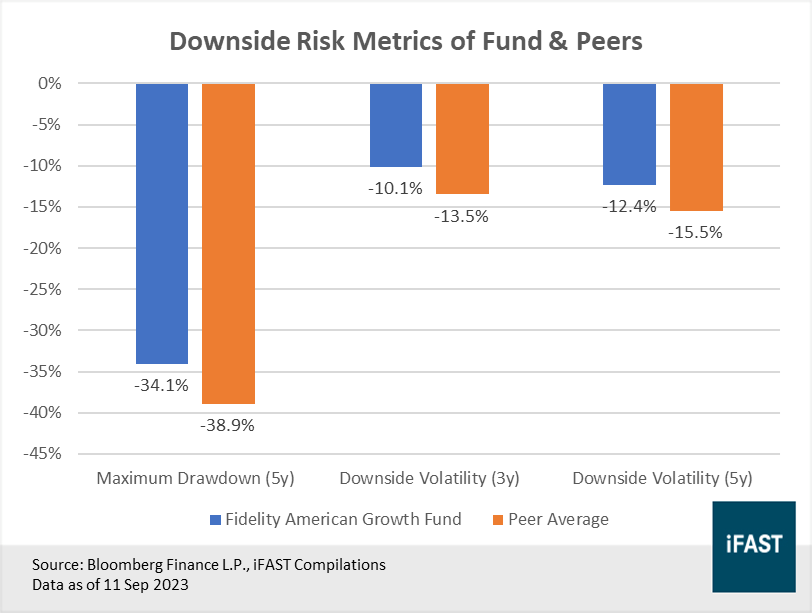

While its returns may only be slightly better compared to the peer average, what is impressive is that the fund delivered this performance with a maximum drawdown of just -34.1% over a five year period, as compared to a maximum drawdown of close to -39% by its peer group, a testament to the portfolio managers’ stock picking skills and their quality focused investment philosophy. In addition, its downside volatilities across both a 3-year and 5-year horizon have also come in below peer averages.

Table 3: The fund has generally outperformed its peers across various time periods

|

Fidelity American Growth Fund |

Peer Average |

|

|

1 Month |

2.44% |

-0.21% |

|

3 Months |

7.55% |

7.32% |

|

Year-to-date |

8.38% |

18.02% |

|

1 Year |

7.79% |

8.58% |

|

3 Years |

7.75% |

6.62% |

|

5 Years |

8.23% |

6.54% |

|

Source: Bloomberg Finance L.P., iFAST Compilations Data as of 31 Aug 2023 Total returns expressed in SGD terms |

||

Figure 3: The fund has displayed good downside risk management relative to peers

Final thoughts

In a nutshell, even as economic growth is expected to come in below trend, high quality growth stocks still have plenty of potential to deliver sizeable returns in the future, more so if your investment horizon is further. For a portfolio to be truly globally diversified, it should have a sizeable allocation to US equities regardless if its constructed using a GDP or a market cap weighted approach.

Investors looking for a piece of American growth stocks should consider the Fidelity American Growth A-USD Fund, our recommended fund for US growth stocks in 2023/24.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.