• The collapse of SVB was an unexpected event, with banks, financials and the broader stock market falling sharply, triggering fears of a wider financial contagion.

• Poor risk management of client deposits and ill timing forced SVB to sell off their investments at a loss to raise capital, resulting in the loss of confidence and ultimately a bank run.

• This saga is not a harbinger of the 2008 Global Financial Crisis and is unlikely to trigger a systemic crisis.

• There could be ripple effects within the banking system and the economy, but it should be manageable as banking regulators, US government and the Fed have stepped in to contain the fallout.

• With the base case of a mild recession, we continue to prefer fixed income over equities and in particular, short duration bonds which are less exposed to interest rate and duration risk. Alternatively, investors who are keen on equities within the US equity universe can consider adopting a quality/value tilt.

Why did SVB implode?

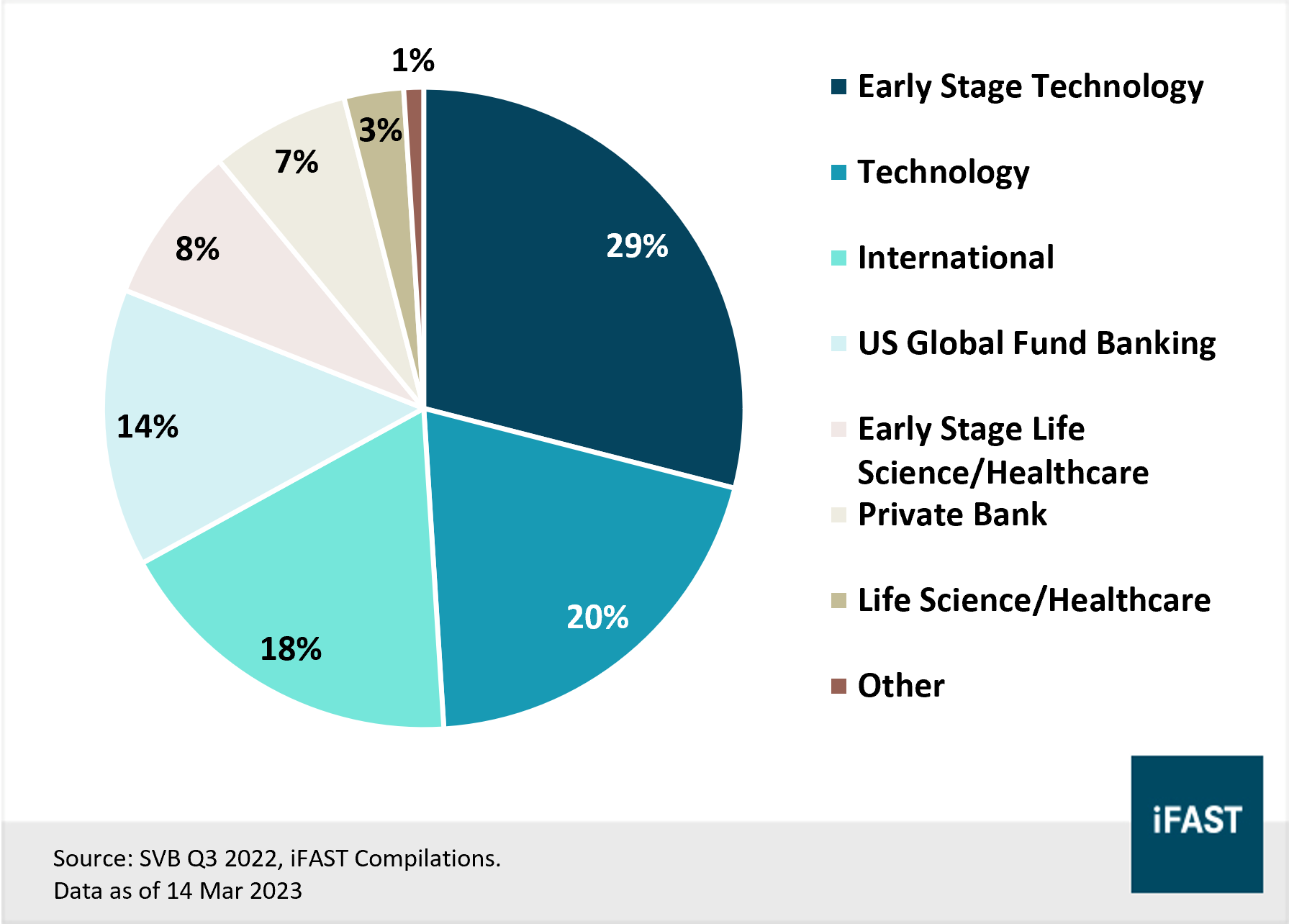

The collapse of SVB is the second largest bank failure in US history. In general, SVB makes most of its earnings via interest income, through loans and their fixed income investment securities, while majority of its cost comes from interest expense on client deposits.SVB was unique in its business model as compared to other banks, as it primarily offers banking services to venture companies in the technology and life sciences sectors. In recent years due to the tremendous liquidity injections by the Fed and quantitative easing environment, SVB has experienced a tremendous growth in its deposits due to its focused technology client base, from events such as IPOs, secondary offerings, SPAC fundraising, venture capital investments and acquisitions, in which they deposit their cash at SVB (Figure 1).

Figure 1: SVB deposit funding percentage breakdown

Due to the surge in client deposits, SVB decided to park a huge sum of these deposits in long duration 10-year Treasury bonds and mortgage-backed securities to earn interest income. Unfortunately, this was ill-timed as SVB bought these bonds when yields were low, and right before the Fed started its rate hiking cycle. As interest rates rose rapidly throughout 2022, the value of SVB’s bond portfolio plummeted significantly.

As the market environment for technology is currently challenging with liquidity drying up, SVB’s clients have been unwilling to raise additional capital given the lower valuations, which has in turn caused them to burn through their cash deposits as they pay for rent and salaries. As a result, SVB’s deposit base fell significantly over the course of 2022.

In an attempt to reposition its balance sheet for the current high interest rate environment and improve its liquidity position due to client redemptions, SVB was forced to sell USD 21 billion from its Available-for-Sale (AFS) bond portfolio at a heavy loss amounting to USD 1.8 billion, which was more than the annual net income the company made in 2022. According to a recent updated investor deck on 8 March, the sale of these bonds had a yield of 1.79% and a duration of 3.6 years, which is significantly lesser than the 10-Year Treasury bonds which yields around 4% at that point in time.

Despite the sale of its bonds, it still required additional capital, as outlined in their plan to raise approximately USD 2.25 billion via issuance of common equity and mandatory convertible preferred shares. This spooked its clients, who were worried about the financial stability of SVB. Since businesses tend have balances above the insured USD 250k threshold, the majority of their deposits were not insured by the FDIC (Figure 2). In a wave of panic, many clients rushed for the gates by pulling out their deposits, resulting in a bank run and its eventual collapse, forcing the FDIC to step in.

Figure 2: Most of SVB deposits were uninsured

Following the unexpected collapse of SVB, banks, financials and the broader stock market fell sharply, as fears of a wider financial contagion rose. With the banking sector being so interconnected today, these fears also swept across Europe and Asia, causing stock markets in others regions to decline as well (Figure 3).

Figure 3: Financials index fell across the globe

Unlikely to be a harbinger of another GFC

It is important to note that SVB’s business model is different from most other commercial banks. Most commercial banks operate by earning the spread between deposits (short-term borrowing) and loans (long-term lending).

Although SVB was taking in deposits, it did not extend as many loans because the new technology start-ups do not have the sufficient fixed assets and reliable cash flows to qualify them as high-quality borrowers. Instead of over-extending loans to these start-ups, SVB purchased safe assets like Treasury bonds and mortgage-backed securities to earn yields, but it failed to account for the rapid interest rate hikes, and did not manage interest rate and duration risk adequately.

Secondly, SVB was an outlier since it has a deposit base heavily concentrated in venture capital-funded start-ups. As tighter monetary policy sapped liquidity out of financial markets, many of these companies had no choice but to turn to their deposits, resulting in huge withdrawals and SVB not being able to meet them.

Despite the collapse of SVB being the largest US bank failure since the global financial crisis in 2008, it is likely that this incident is an isolated event and a result of the company’s own failures, rather than a case of a broad banking sector issue or systemic crisis within the US financial system. The risk is likely to be concentrated in banks that have seen a sizable contraction in their deposits, those that have significant declines in their capital reserves and banks that are not well diversified in terms of their depositor base.

In the short term, as fear continue to creep among clients and investors, we could witness other smaller and regional banks experiencing similar bank runs as depositors attempt to withdraw their money all at the same time. The ripple effect can already be seen, with other similar unique banking institutions seeing huge drawdowns on Friday, as investors are afraid that similar liquidity issues may pressure these banks to forcibly realise huge losses and end up like SVB. Fortunately, since the FDIC and regulators have stepped in to manage the mess, some confidence is likely to be restored and this episode should not turn out to be another Global Financial Crisis (GFC).

While larger banks are not entirely immune to this, they remain well-capitalised for the time being, and are unlikely to face liquidity issues in the near term. Furthermore, the big banks may actually benefit from this fiasco as clients redirect their deposits to the safer and larger banks, which can boost their client base. Notably, due to the broader suite of services to their customers, deposits at the larger banks are generally stickier.

Lastly, the overall US banking system remains healthy and robust. Ever since the GFC in 2008, all US banks, particularly the larger and more important ones have to meet strict capital requirements and undergo annual stress tests. Notably, Tier 1 capital ratios have risen from 9% of risk-weighted assets in 2008 to around 14% today while loan-to-deposit ratios have also fallen meaningfully.

Although SVB had a CET1 ratio of 12.05% (well above the required 4.5%), there are some challenges if we look under the veil (Figure 4). If we were to factor in all the unrealised losses the bank has on its AFS and Held-to-Maturity (HTM) portfolios, SVB’s CET1 ratio is actually a lot worse than its peers, which was probably the reason why depositors felt uneasy and decided to pull out their money at the first sign of danger.

Figure 4: Impact of unrealised securities losses on capital ratios

Implications in the near term

With the announcement that the US government and banking regulators has stepped in to backstop all deposits at SVB, this could help to lift the short-term sentiments and partially restore confidence within the US banking system. As the case is still developing, we will have to see how this plays out, though it is likely that depositors should be able to retrieve their funds.Next, as long as fears are contained and does not spread to other banks within the financial industry, this negative market reaction should pass in the coming days and weeks.

The Fed may also view this as a sign that the impact of higher interest rates is starting to materialise as some parts of the economy have started to break. As of 14 March 2023, the markets have shifted away from the view that the Fed will tighten by 50 basis points, and are leaning towards a 25 basis points or even no rate hike at the upcoming March FOMC meeting. Of course, the Fed will also be considering other factors and economic data, such as the upcoming CPI print and unemployment data this week to ensure a more holistic view.

To sum it up, we believe that the SVB saga is an outlier and since government intervention has been decisive, it is unlikely to cause a financial contagion.

Next, despite concerns regarding financial stability, we believe the Fed has not given up its fight against inflation and is unlikely to cut rates this year. However, given the recent events, the Fed is likely to be more cautious and may slow down the pace of rate hikes.

Lastly, the economy is likely to experience slower growth. Moving forward, banks may become more risk averse and hold on to more cash, which will cause the credit supply in the overall economy to tighten and impede economic growth.

Diversify and keep an eye out for quality stocks

Reflecting on this episode, this bank run will certainly be an interesting case study for banking regulators as they adapt their frameworks, and the Fed as they continue to tame inflation.Beyond that, a take away for investors is to never put all your bags in one basket, because unexpected events like this can always happen and ideally you do not want to be on the short end of the stick if something goes wrong drastically.

For investors that are invested in SVB equity or bonds, it is unfortunate as these holders are likely to be wiped out.

However, for those that are invested in financials/bank ETFs or funds with quality names, do hold on as the tides will pass with time.

In terms of asset allocation, we continue to prefer fixed income over equities, with the base case that the US economy could experience a mild recession in the coming months.

For fixed income, we prefer short duration bonds, which are less susceptible to duration risk, as experienced by SVB. The Nikko AM Shenton Short Term Bond Fund, United SGD Fund, and the LionGlobal Short Duration Bond Fund are three funds worth taking a look at.

Within equities, we recommend investors to adopt a quality/value tilt, which are more resilient as we head a towards a potential shallow contraction. Some names that investors can consider are the JPMorgan US Quality Factor ETF (NYSE:JQUA) and the JPMorgan Funds - US Value A (acc) SGD.

Related article: Rise of the underdog. The comeback of US Value stocks

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.