SGS Bonds

The Singapore Government Securities Bonds (“SGS Bonds”) are bonds that are fully backed by the Singapore Government. The bond has the strongest credit rating of AAA by major credit agencies. The SGS bonds pay a fixed interest rate with maturities between 2 to 50 years.

There are three different categories of SGS bonds – 1) SGS (Market Development), 2) SGS (Infrastructure) and 3) Green SGS (Infrastructure).

The key differences between the three types of SGS bonds would be the legislation that the SGS bond is issued under and its use of proceeds.

For investors who wish to invest in a safe asset between 1-2 years, the SGS bonds are suitable as it provides more yields as compared to the SSB. As of 4 October 2022, the yield for the 2 year SGS bond is around 3.39%. Even though there is a fixed maturity date for the SGS bonds, investors can still trade bonds on the secondary market. Investors may trade SGS bonds through an SGX broker. FSMone offers an attractive rate of only 0.1% processing fee (or minimum $10) when trading SGS bonds.

One of the risks in buying SGS bonds is that the bonds are subjected to fluctuations in secondary market pricing. The value of the bond may be lower than its par value which may incur additional losses when sold before its maturity date. When interest rates rise, it will negatively impact a bond’s price, thus we think the SGS bonds are suitable for investors who are able to hold a short-term SGS bond till maturity.

|

|

SGS (Market Development) |

SGS (Infrastructure) |

Green SGS (Infrastructure) |

|

Legislation |

Government Securities (Debt Market and Investment) Act 1992 |

Significant Infrastructure Government Loan Act 2021 (SINGA) |

Significant Infrastructure Government Loan Act 2021 (SINGA) |

|

Objective |

To develop the domestic debt market |

To finance major, long-term infrastructure |

To finance major, long-term green infrastructure projects |

|

Tenor |

2, 5, 10, 15, 20, 30, or 50 years |

||

|

Frequency of issuance |

Monthly, for at least 5 years |

||

|

Minimum investment amount |

SGD 1,000, in multiples of SGD 1,000 |

||

|

Maximum investment amount |

Up to the allotment limit for auctions |

||

|

Buy using SRS and CPF funds? |

CPF and SRS |

||

|

Interest payment |

Every 6 months, starting from the month of issue |

||

|

Secondary market trading |

Yes |

||

T-bills

Treasury bills, or T-bills, are short-term Singapore Government Securities. T-bills are available in short-tenors of 6 months and 1-year. Unlike the SGS bonds, T-bills do not have interest payments but are issued at discount to its face value. Upon maturity, T-bills will be redeemed at its face value of 100.

For investors who wish to park their cash in a safe asset for a short period of time, the SGS T-Bills are suitable as it provides decent yields for only a short 6 months or 1 year period. It is also suitable for investors who are undecided and would like to wait out the volatility and uncertainty in the markets. As of 4 Oct 2022, the cut-off yield for the latest 6-month T-Bill auction was 3.32% which is a much better alternative to fixed deposits and bank deposit rates. The T-Bill can also be traded on FSMone and is also offered at only 0.1% processing fee (or minimum $10) when trading the T-Bills on FSMone.

|

SGS T-Bills |

|

|

Tenor |

6 months or 1-year |

|

Frequency of issuance |

Quarterly |

|

Minimum investment amount |

SGD 1,000, in multiples of SGD 1,000 |

|

Maximum investment amount |

Up to the allotment limit for auctions |

|

Buy using SRS and CPF funds? |

SRS and CPF |

|

Interest payment |

N/A |

|

Secondary market trading |

Yes |

Singapore Savings Bonds

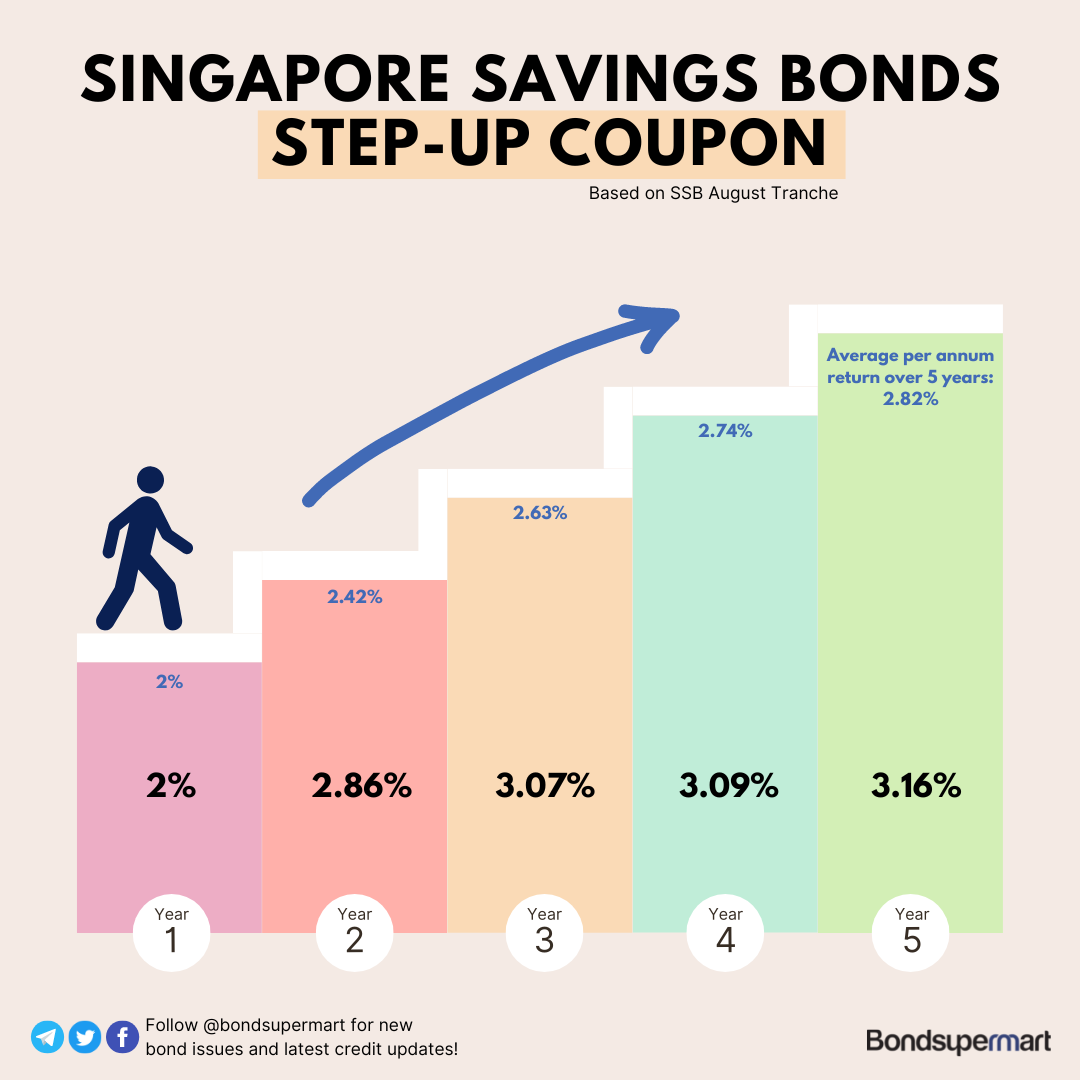

The Singapore Savings Bonds, or SSBs for short, are a special type of Singapore Government Securities. It has a tenor of up to 10 years and is issued monthly. Interest rates for the SSBs are determined based on the yield to maturity of the corresponding SGS bond. For example, the 5-year average return on the SSB should be equal to the yield of the 5-year SGS bond.

One unique feature of the SSB is that it gives investors increasing returns the longer you hold the SSB. Interest rates for the SSBs will “step-up” every year for as long as you hold the bond. This results in the total average returns of the SSB to increase each year as the next interest payment will be higher than the previous one.

In the event where short-term rates are higher than long-term rates (an inverted yield curve), MAS will apply adjustments to ensure that the coupons on the SSBs do not step-down at any point in time. MAS will ensure that the average 10-year return of the SSB (when held to maturity) will always equal to the yield of the 10-year SGS bond.

Another unique feature the SSB provides is the flexibility to redeem the bond at any point in time (during the tenor of 10 years). At any point in time, holders of the SSB can redeem their SSB and receive in full principal amount (including accrued interest) by the second business day of the next month.

SSBs are suitable for investors who wish to enjoy flexibility in their investments. There is no fixed tenor for the SSB, so investors can decide when to redeem the bond. Additionally, the SSB is not affected by secondary market trading which ensures less volatility in the bond. With that in mind, the lack of secondary market trading also removes the ability to earn capital appreciation in the bond when interest rates fall.

|

Singapore Savings Bonds |

|

|

Tenor |

Up to 10 Years |

|

Frequency of issuance |

Monthly, for at least 5 years |

|

Minimum investment amount |

SGD 500, in multiples of SGD 500 |

|

Maximum investment amount |

SGD 200,000 overall |

|

Buy using SRS and CPF funds? |

Only SRS |

|

Interest payment |

Every 6 months, starting from the month of issue |

|

Secondary market trading |

No |

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.

Please note that only certain bond(s) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to FSM's prevailing policies and procedures. Please read our full disclaimers in the website.