• Tech stocks have plummeted by as much as 50%, over the year as inflation, rate hikes, the Russia-Ukraine war, and China lockdowns weighed on the sector.

• In the near-term, we see near-term downside risks which include a recession, and high inflation. The digital economy looks challenged and earnings growth is likely to be subdued in the next 6-12 months.

• Overall, we recommend investors wait out the near-term volatility and for downside risks to be priced in, before going back into Tech stocks.

• Nevertheless, not all is doom and gloom, as Big Tech having a strong business model could prove more resilient in weathering the storm, and among the segments, the cloud business stands out.

• We maintain a 2.5 Stars “Neutral” rating, given the near-term downside risks and lack of positive catalysts. Our target price is USD 157 for the Invesco NASDAQ Internet ETF (NASDAQ: PNQI), which gives investors an upside potential of 18.6% as of 23 August 2022.

Since late 2021, tech stocks have plummeted from highs as the macroeconomic overhang – rising inflation, sharp rise in interest rates, Russia-Ukraine war, China lockdowns, and regulatory overhang – sent share prices down.

Figure 1: PNQI fell over 40% since highs in late 2021

Most recently, after 2Q22 earnings, US Big Tech stocks saw a rally in prices as markets liked that the earnings results were not as bad as feared. Since lows two months back, the Invesco NASDAQ Internet ETF (NASDAQ: PNQI) is up close to 25% as of 15 August 2022. The positive sentiment surrounding Tech stocks was also supported by catalysts including Powell’s comment of the Fed possibly slowing the pace of rate hikes, and the lower than expected US inflation print for July.

Related article: 2Q22 earnings: Why did Big Tech stocks pop?

However, we think that this rally is not sustainable, as the macroeconomic downside risks coupled with a lack of positive catalysts likely would weigh on share prices in the near-term. Hence, we maintain our 2.5 Stars “Neutral” rating for the digital economy.

Challenging global economic backdrop a bummer to Tech

The US economy shrunk, posting negative GDP growth in the last two quarters, and Europe is at a high risk of a recession. Inflation hit highs across the world, and rate hikes have kicked in globally. With this cocktail mix of slowing business activity, rising prices, and increasing borrowing costs, it is likely to result in consumers and businesses cutting/delaying spending. (Figure 2)

Figure 2: Consumer confidence continues to tumble in June

Firstly, as consumers reduce spending, e-commerce demand is likely to see a slowdown, impacting e-commerce players like Amazon (NASDAQ: AMZN). Secondly, as demand and business activity slow, businesses will also pullback on their advertising spending, impacting digital advertising businesses like Meta (NASDAQ: META), Google (NASDAQ: GOOGL), Snap (NYSE: SNAP), etc. Thirdly, as inflation kicks in, companies would tighten their spending. One of methods to cut spending includes a pullback in hiring, which we already hear of from the 2Q22 earnings management guidance.

Hence, from a macroeconomic point of view, the digital economy is likely to be challenged in 2H22.

Earnings downgrade seen across the tech sector

Moreover, the tech sector has seen a downward revision of earnings, reflecting the impact of the global economic slowdown. Broadly speaking, the EPS estimates across the entire sector has seen downward revisions with a few exceptions such as Microsoft and Apple.

Overall, the Nasdaq CTA Internet index, which is the underlying of the Invesco NASDAQ Internet ETF (NASDAQ: PNQI), has seen an EPS downward revision of -32% since the beginning of the year (Figure 3).

Figure 3: Year-to-date EPS estimates for 2022 have been revised down

But, not all is doom and gloom, as certain segments and companies are more resilient amid this economic downturn.

Certain segments and companies are more resilient

An economic downturn hits all sectors and companies, however, the impact varies. Within the digital economy space, Big Tech companies are likely able to weather the storm better – Microsoft, Amazon, Alphabet, Apple, and Meta Platforms.

Big Tech companies have a large footprint and deep expertise in their business, with more stable cashflows and healthier balance sheets, which poises them to be able to weather the storm better than the smaller competitors.

Firstly, the goods and services provided by Big Tech have become almost a basic necessity – daily communication with colleagues or loved ones (Meta’s apps), daily buying and selling of goods (Amazon, Alibaba), and even daily entertainment (Netflix). As a basic necessity, demand is likely to remain relatively more resilient amid an economic downturn.

Secondly, Big Tech companies have well-established competitive edges, which gives them a strong foundation in weathering the storm. For example, although Meta has faced headwinds across the past few quarters due to the weakening Europe, Apple privacy IDFA changes, and an ecommerce slowdown, Meta still holds its number one position with the most number of users across its Family of Apps (Facebook, Instagram, Messenger, WhatsApp) (Figure 4).

Additionally, Meta continues to attract new users demonstrating the strength of its product. Facebook app users returned to growth at +3% YoY and the Family of apps users grew by +6%, despite having to close the Russia business. With its core product offering and no signs of a substitute, it is unlikely that users (which are Meta’s key assets) will disappear overnight.

Figure 4: Meta’s has the largest number of users and users grew +6% YoY in 2Q22

Thirdly, Big Tech companies are better equipped with resources to implement cost management strategies to tide through the storm. For example, Amazon was able to cut costs by USD 2 billion in 2Q22 by letting go of nearly 100,000 workers reducing unit shipping costs, and increasing utilisation. The company plans to further cut costs by another USD 1.5 billion in 3Q22.

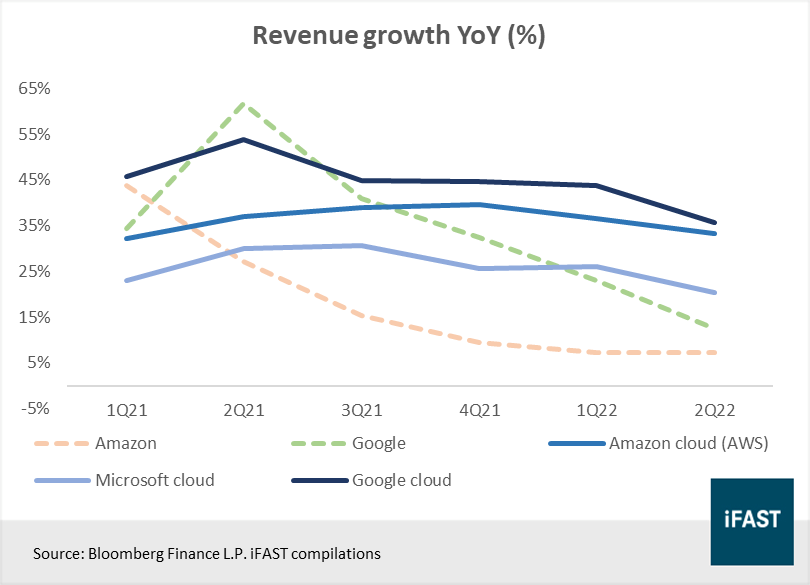

Another attractive area is the cloud computing segment, as this segment stands out with its higher and more resilient growth rates (Figure 5). Going forward, the cloud growth looks resilient as corporates continue to digitalise their operations.

Figure 5: Cloud business segment growth more resilient than the other digital economy segments

Going forward, cloud infrastructure-as-a-service (IaaS) industry leaders continue to see a healthy pipeline of future demand. For example, in 2Q22, Microsoft saw strong booking growth and closed the biggest number of large deals.

Management also gave positive guidance of double-digit revenue and profit growth for the next twelve months, as they expect companies to continue their cloud transition, even amid an economic downturn, as it helps in improving efficiency and overall cost management. Similarly, the pipeline at Amazon cloud (AWS) remains healthy, with a backlog growing 65% YoY and 13% QoQ.

All in all, in the current macroeconomic environment where growth is slowing as the economy is hit from multiple fronts including the Russia-Ukraine war, US-China trade tensions, global supply shortages, and more, it is important to identify quality businesses with sustainable earnings that can weather the storm.

Big Tech companies are such contenders, and the Invesco NASDAQ Internet ETF (NASDAQ: PNQI) gives investors a high exposure to such companies of close to 40% (Figure 6). The cloud segment is also one we prefer given the secular growth trend, and the First Trust Cloud Computing ETF (NASDAQ: SKYY) is our recommended product. Big Tech and cloud computing are not mutually exclusive, but instead many Big Tech players are leaders in cloud computing.

Related article: Cloud computing a green shoot among digital economy segments

Figure 6: PNQI has close to 40% exposure to Big Tech (M.A.A.M and B.A.T.)

Key investment risk

Recession impact – the impact of the recession could be worse than expected and corporates choose to delay investment. In this scenario, our thesis on the cloud players could be impacted as the cloud business could see a slowdown in growth if companies go bust or if companies delay cloud spend.

Supply disruption – further escalations of the Russia-Ukraine war or the US-China tensions would likely put the global supply situation under heightened strain, which would impact sales of the companies. The increasing tensions also raise the risk of sanctions which would add to the trade disruptions and contribute to inflation.

Not yet time to get back into Tech

Summing up, in the near term, with the macroeconomic overhang and downside risks, coupled with a lack of positive catalysts for share prices and possible further downward earnings revision, we maintain our 2.5 Stars “Neutral” rating for the digital economy.

Table 1: Earnings table

|

2021 |

2022E |

2023E |

2024E |

|

|

EPS |

20.65 |

21.58 |

24.06 |

32.36 |

|

Earnings Growth |

56.72% |

5% |

12% |

35% |

|

PE Ratio |

- |

37.95 |

34.03 |

25.30 |

|

Upside Potential |

- |

- |

-11.9% |

18.6% |

|

Source: Bloomberg Finance L.P. Data as of 23 August 2022. |

||||

Earnings wise, we expect 2022 to see weakness due to slowdown post the covid19 digitalisation boom coupled with macroeconomic weakness. Earnings in 2023 should see improvement as companies cost management plans materialise in full year effect, and certain segments like the cloud to see resilience. 2024 should see recovery as the long-term growth of the digital economy holds.

Historically, the Nasdaq CTA Internet Index has traded at an average premium to the S&P 500 index of 80%-150%, since its inception in 2011. In 2022, the index trades on average at a premium of 70% to the S&P 500 index. We think this 70% premium is fair, which is lower than the historical range, accounting for the new economic regime – higher cost of capital and lower liquidity. Applying a 70% premium to our fair PE of 18X for the S&P 500 index, we arrive at a fair PE of 30X for the base case scenario for the digital economy.

With that, we arrive at a target price of USD 157 for the Invesco NASDAQ Internet ETF (NASDAQ: PNQI), which gives investors an upside potential of 18.6% as of 23 August 2022.

Nonetheless, long term, the internet will continue to grow in importance and become an integral foundation of our world. Right now, it already is where companies operate, people find information, people connect, and more. That is why we think that the digital economy deserves to be a core allocation in investors’ portfolios.

Investors who have yet to include the digital economy in their portfolios but wish to do so at this point may consider using a regular savings plan, before switching to a lump sum investment should valuations come down even further. This will ensure that they buy more units when prices are low and less when prices are high, bringing the weighted average cost down.

Finally, investors who have a position in the ALPS O'Shares Global Internet Giants ETF (BATS: OGIG), which is our recommended digital economy ETF, fret not as both OGIG and PNQI have benefits each.

The ALPS O'Shares Global Internet Giants ETF would be more suitable for investors who are seeking higher returns through exposure to high growth names, while the Invesco NASDAQ Internet ETF would be a better option for investors who wish to gain exposure to Big Tech companies, which are likely to be more resilient in a downturn.

Related article: Hello PNQI! Invest in Big Tech through this ETF

Figure 7: In the long run, share prices are driven by earnings

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in Alibaba.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.