- Asian high yield bonds have gone through rough times, posting a return of -12.6% in 2021 due to China’s property crisis.

- On 16 March 2022, China has pledged more support for the property sector, which we believe should paint a better picture for the outlook of Chinese property credits, and hence the Asian high yield bond market.

- With Chinese property credits trading at distressed levels and the widen spreads in the Asian high yield bond market, we think that heavy risks of default are likely already priced in, and the risk-reward is skewed to the upside.

- Moreover, Asian high yield bonds provide one of the highest yield per unit of duration, which can potentially provide some buffer to offset the rise in interest rates.

- All things considered, we continue to hold a positive view on Asian high yield bonds.

Asian high yield bonds have gone through rough times. As represented by the Bloomberg Barclays Asia USD High Yield Bond Index, the market posted a total return of -12.6% in 2021. The underperformance of Asian high yield bonds can be attributed to China, in particular, its property sector.

Chinese property credits suffered a large drawdown after the liquidity crunch at Evergrande sent ripples across the entire sector. The carnage continued on this year, with the Russia-Ukraine crisis adding on to the uncertainty.

While the poor returns may have alarmed investors, we think that the worst could already be behind us, and that the Asian high yield bond market is presenting an attractive value proposition for long-term investors.

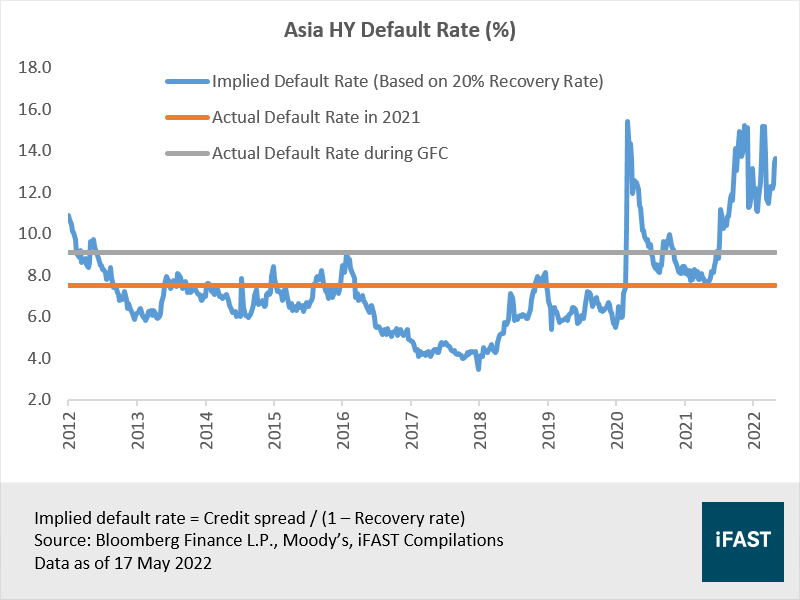

Figure 1: Asian high yield bonds saw heightened volatility

China pledges more support for the property sector

China’s share in the Asian high yield universe remains significant despite falling to 30% (Figure 2) from approximately 50% in recent years. Out of which, the majority of the China high yield bonds are from the property sector.

Figure 2: China is still the largest market in Asian high yield

Following the Evergrande crisis and its impact on the property market, Chinese authorities have implemented policy fine-tuning in their efforts to stabilise the sector (Table 1). Thus far, however, there has been little positive impact on contracted property sales (Figure 3) – a factor that can help to support developers’ liquidity and repayment ability.

Table 1: A timeline of policy fine-tuning in China’s property sector

|

Date |

Policy Measure |

|

15 Oct 2021 |

Regulators told major banks to accelerate mortgage approvals, apply for residential mortgage-backed securities sales to free up loan quotas |

|

7 Jan 2022 |

M&A loans will not be included in the Three Red Lines |

|

19 Jan 2022 |

Regulators considering to lift some restrictions on developers’ access to cash from presold properties tied up in escrow accounts |

|

20 Jan 2022 |

Cut in 5-year loan prime rate, the benchmark for mortgages, to 4.60% from 4.65% |

|

8 Feb 2022 |

Loans to fund low-cost public rental homes are not subject to regulatory curbs on Chinese banks’ property lending |

|

10 Feb 2022 |

Regulators told state-owned firms to participate in the restructuring of weak developers, acquire stalled property projects and buy soured loans |

|

11 Feb 2022 |

Nationwide regulation to standardise the use of cash from pre-sold properties |

|

18 Feb 2022 |

Banks in several cities lowered down payment ratio for first-time homebuyers to 20% from 30% |

|

15 May 2022 |

Banks reduce the lower-bound range of mortgage interest rates for first-time homebuyers by 20 basis points |

|

Source: People’s Bank of China, Bloomberg Intelligence |

|

Figure 3: Policy fine-tuning has not cured the slump in sales

With this year being a politically important one for China due to the 20th Party Congress, the property sector would be one area of focus since its slowdown had cast a shadow on the economy. China has prioritised economic stability, setting a GDP growth target of 5.5% for 2022, which had exceeded market expectations. To achieve this lofty target, the central government is anticipated to roll out more policy support.

Vice Premier Liu He – President Xi’s main economic adviser – said on 16 March that the government needs to reduce risks in the property sector and propose measures to facilitate a “new development model”. This could possibly suggest that the sector has reached a “turning point”.

Chinese regulators also reiterated their intentions of stabilising the property sector, with the finance ministry announcing that a property tax trial initially planned for this year will be put on hold. Meanwhile, executives at top developers believe that there is a need for more decisive policy easing at the city level in order to drive a turnaround in the near-term liquidity outlook.

Overall, we believe that the central government’s assurance of providing continued support to property sector, while taking time to feed through, should paint a better picture for the outlook of Chinese property credits. We maintain our view that the ongoing policy easing environment could be a key near-term catalyst for the gradual recovery of China’s property sector, and hence the Asian high yield bond market.

Heavy risks of default likely already priced in

In the broader Asian high yield bond market, default risks seem to be adequately reflected. Using a conservative recovery rate of 20%, which is around half of historical levels, the current spread level of Asian high yield bonds implies a default rate of around 13.6%. This is higher than the actual default rate of 7.5% in 2021, as well as that of 9.1% recorded during the depths of the Great Financial Crisis (GFC).

Figure 4: A high default rate for Asian high yield implied from current spread levels

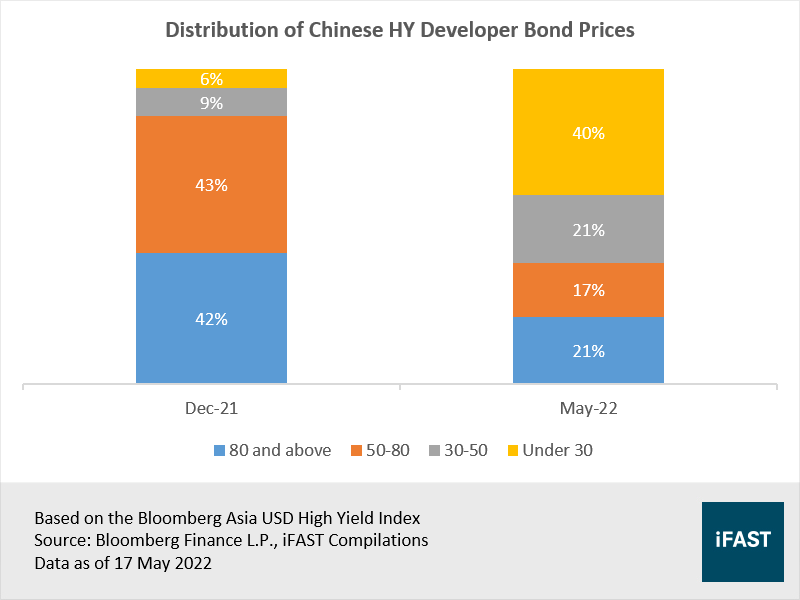

Zooming into Chinese property credits, despite some recovery from the March lows, they have continued to trade at distressed levels, with over 50% of them trading below 50 cents on the dollar. This is a stark difference as compared to 31 December 2021, where only 15% of property bonds were trading below 50 cents on the dollar.

Figure 5: The market is pricing in high risks of default

The ongoing policy easing environment could alleviate some of the credit stress faced by developers, and keep default rates from reaching extreme levels. We also note that further policy support would create winners within the sector, as lenders could be comfortable with extending credit to stronger companies.

In essence, current valuations suggest that elevated levels of default have already been taken into account. We believe that the risk-reward is skewed to the upside, presenting long-term investors betting on the gradual recovery of the Asian high yield bond market with an attractive entry point.

Rising rates not as big of a concern as compared to peers

Even though the Asian high yield bonds is generally affected by credit risk, managing duration exposure is also important against the hawkish interest rate environment.

The good news is that Asian high yield bonds offer a combination of higher yield and shorter duration as compared to peers (Table 2). Asian high yield credits have a yield of close to 14%, which is twice that of US and Europe high yield credits. This comes alongside a relatively shorter duration of 3.2 years.

Table 2: Duration exposure is all relative

|

Market |

Yield Per Unit of Duration |

Yield |

Duration |

|

Asia HY |

4.3 |

13.9 |

3.2 |

|

EU HY |

1.9 |

6.8 |

3.6 |

|

US HY |

1.8 |

7.6 |

4.3 |

|

Based on Bloomberg Barclays indices Yield is based on yield-to-worst, which denotes the lowest possible yield that can be received without the bond defaulting Source: Bloomberg Finance L.P., iFAST Compilations Data as of 17 May 2022 |

|||

As a result, the Asian high yield bond market provides one of the highest yield per unit of duration. Also known as the Sherman ratio, the yield per unit of duration is a measure of interest rate risk. A ratio of 1 indicates that it would take a 1% rise in interest rates to offset the yield of a bond.

A higher yield per unit of duration can potentially provide some buffer to offset the rise in interest rates. This makes Asian high yield credits more compelling against the backdrop of aggressive rate hikes, which are likely to have a greater impact on global peers.

Key investment risks

Policy easing could be too little and too late: Piecemeal efforts by the Chinese government are unlikely to produce the desired positive impact on the property sector. Also, if further support takes too long to implement, it could possibly be too late to restore confidence in the property sector.

More COVID-19 lockdowns: Shanghai’s COVID-19 lockdown has lasted for weeks. Given China’s strict zero-COVID policy, outbreaks of COVID-19 cases in other provinces or cities could trigger even more lockdowns. This could hurt developers’ contracted sales due to construction halts and the closure of sales offices, thereby delaying the recovery of the property sector.

Recommendations

All things considered, we continue to hold a positive view on the Asian high yield bond market.

The central government’s assurance of providing continued support to property sector should paint a better picture for the outlook of Chinese property credits. Even though another wave of defaults within the Chinese property sector may be imminent, the bottom line is that the risks of default are likely well priced in after the significant drawdown. We believe that the risk-reward of the Asian high yield bonds is now skewed to the upside, presenting significant value for long-term investors.

We favour an active investment approach as we believe that will help to pick out the quality names. For instance, the recent Chinese property developer auditing crisis, whereby certain developers (e.g. Sunac, Shimao) were unable to release their audited results before the deadline required by HKEX, has highlighted that there are areas for credit selection.

Our current recommended fund for the Asian high yield bond market is the Eastspring Investments - Asian High Yield Bond ASDM SGD-H. Besides this, we also like the Blackrock Asian High Yield Bond A8 SGD-H for its stronger risk management and more resilient performance vis-à-vis peers.

Investors with stronger risk appetite could also go for products that provide a pure-play exposure to Chinese property bonds. Currently, only ETFs provide such exposure. Specifically, the Premia China USD Property Bond ETF (HKEX:9001) is the only product available in the market that provides diversified exposure to Chinese property credits.

Table 3: Recommended products

|

Market |

Unit Trust |

ETF |

|

Asian High Yield |

--- |

|

|

--- |

||

|

China Property Bond |

--- |

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in Premia China USD Property Bond ETF.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.