- Supported by favourable trends, industrial REITs are a resilient sub-segment. Frasers Logistics & Commercial Trust (SGX:BUOU) and Ascendas REIT (SGX:A17U) are our top picks.

- Data centres have emerged as a bright spot among real estate asset classes during the pandemic. We think the newly listed Digital Core REIT (SGX:DCRU) offers strong growth potential at an attractive relative valuation.

- For office, Keppel Pacific Oak US REIT (SGX:CMOU) remains as our pick due to its significant tech exposure as well as attractive distribution yield.

- With the rise in e-commerce, we are less optimistic about retail REITs. Also, we see a lack of near-term catalysts that can drive a re-rating across hospitality REITs due to uncertainties over the travel recovery.

Singapore REITs (S-REITs) are often favoured by investors for their ability to provide a stream of passive income, with the potential for moderate capital appreciation.

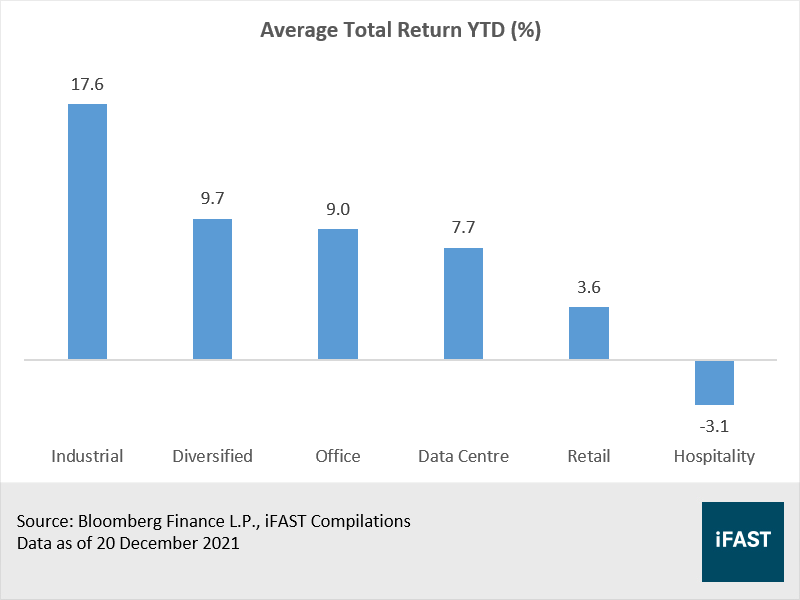

Based on our compilations in Figure 1 below, industrial REITs have delivered the strongest returns on average so far in 2021. Moreover, the successful listing of Digital Core REIT (SGX:DCRU) has led the performance of data centre REITs. At the same time, some sub-segments hit hard by the pandemic (i.e. office, retail) managed to see some recovery. The only exception is the hospitality REITs, which have continued to underperform the broader sector.

Figure 1: Total return of S-REIT sub-segments

In this article, we provide some perspectives on S-REITs’ performance year-to-date. With the year coming to a close, we also share our views on what lies ahead in 2022.

Industrial: A resilient sub-segment

Thanks to structural trends accelerated by the pandemic, industrial REITs have generally done well in 2021. Industrial spaces that cater to the new economy – which include warehouses, high-spec industrial buildings, and business parks – saw upbeat demand. Above all, warehouses recorded the strongest growth in rental rates in the third quarter of 2021, with a year-on-year increase of 2.6%.

Looking ahead, we remain positive on industrial spaces that support the new economy. The acceleration of e-commerce and the shift from “just-in-time” to “just-in-case” inventory management to cope with supply chain disruptions is expected to drive the demand for warehouses. Meanwhile, we believe that the demand for high-spec industrial buildings and business parks is likely to be resilient due to the rapid growth of the tech and biomedical science sectors.

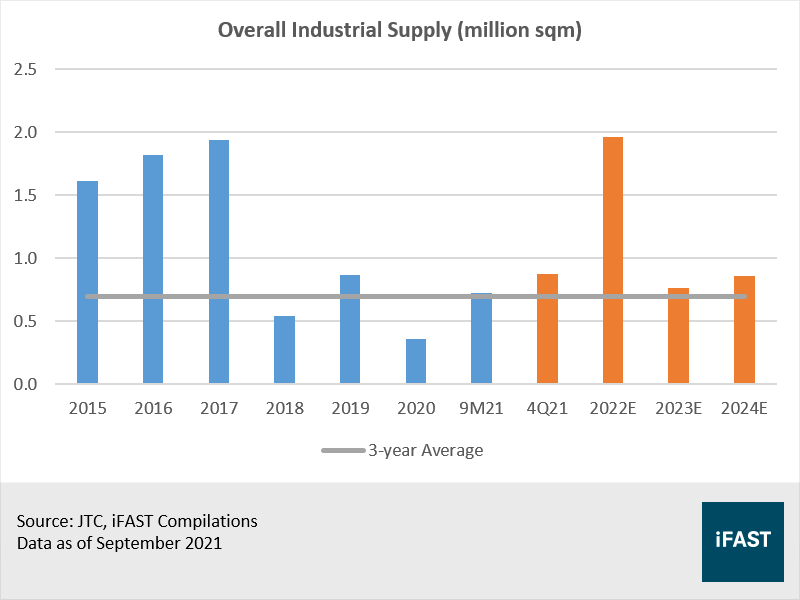

On the supply side, an additional 3.6 million sqm of industrial space is expected to be completed in Singapore between 2022 and 2024, according to JTC (Figure 2). This translates to an annual supply of 1.2 million sqm on average, which is higher than the average of 0.7 million sqm over the past three years.

Figure 2: Historical and upcoming industrial supply

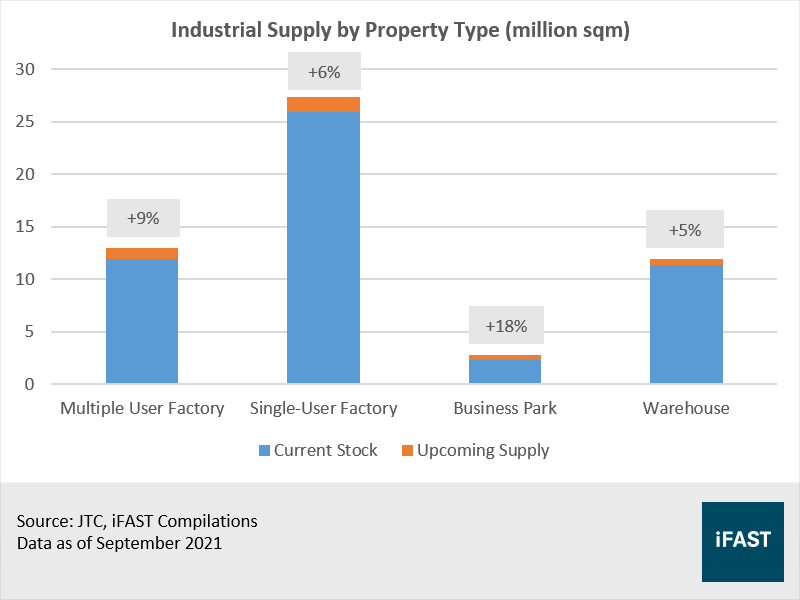

Nevertheless, we note that the upcoming supply is not evenly split across the type of industrial space. Warehouses, whose demand has boomed, will see supply increase by around 0.6 million sqm between 2022 and 2024. In other words, the supply of warehouses will increase by approximately 5% during the period, which is the lowest out of all industrial spaces (Figure 3). In view of the demand and supply dynamics, we think that rentals of warehouses should continue to record strong positive growth.

Figure 3: Breakdown of industrial supply by property type

Table 1 below summarises the valuations and yields of large-cap industrial REITs. Frasers Logistics & Commercial Trust (SGX:BUOU) stands out as the cheapest REIT based on historical and relative standards.

Table 1: Comparison of large-cap industrial REITs

|

Name |

Market Cap (SGD billion) |

Current PB (X) |

10Y Historical PB (X) |

Yield (%)* |

|

Ascendas REIT |

12.1 |

1.28 |

1.25 |

5.7 |

|

Mapletree Logistics Trust |

8.7 |

1.42 |

1.24 |

4.8 |

|

Mapletree Industrial Trust |

7.1 |

1.41 |

1.36 |

5.4 |

|

Frasers Logistics & Commercial Trust |

5.4 |

1.19 |

1.22 |

5.4 |

|

*Estimated yield in FY2022 Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 December 2021 |

||||

Frasers Logistics & Commercial Trust (FLCT) is a geographically diversified REIT, with a focus on logistics & industrial buildings. In recent news, FLCT has announced the divestment of a non-core property in Port Melbourne, which is expected to enhance the REIT’s financial flexibility. We also note that FLCT is well-positioned for inorganic growth. Its gearing ratio stands at only 33.7%, which we think provides ample debt headroom to acquire assets from its Sponsor’s SGD 5 billion pipeline.

Moreover, we think Ascendas REIT (SGX:A17U) is worth highlighting due to its diversified portfolio of industrial properties. On the back of a SGD 1.8 billion pipeline of assets from its Sponsor, we expect acquisitions to happen in 2022, which is likely to be funded using a mix of debt and equity.

Data Centre: Robust demand driven by long-term trends

Data centres have emerged as a bright spot among real estate asset classes during the pandemic. Amidst the growing interest of data centre REITs, the Singapore Exchange (SGX) recently welcomed the listing of Digital Core REIT (DCREIT) (SGX:DCRU).

The pandemic has accelerated several long-term trends which drive data traffic, which in turn, leads to a greater demand for data centres. Such trends include an increase in spending on cloud services, emerging technologies like Artificial Intelligence, Internet of Things and 5G, as well as the growth of internet platforms like e-commerce, streaming, and social media.

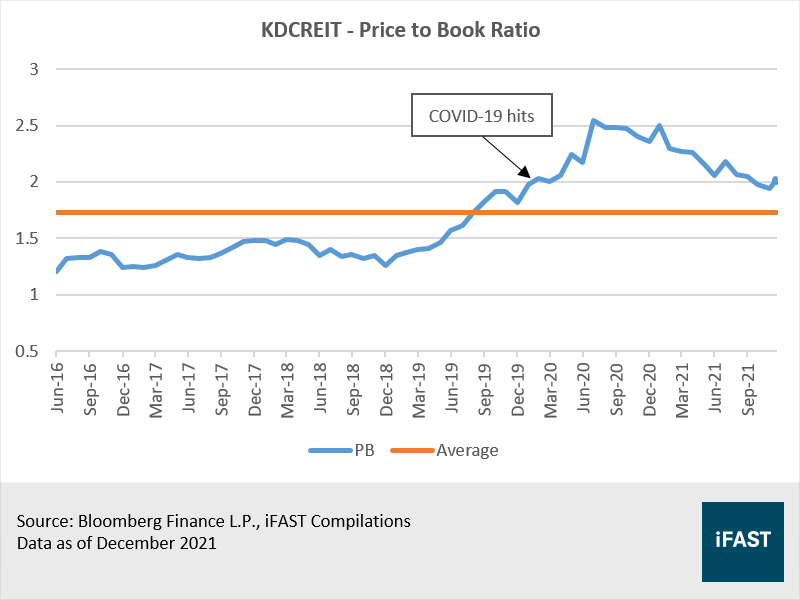

Before DCREIT came along, there was first Keppel DC REIT (SGX:AJBU). However, after a fabulous run in 2020, Keppel DC REIT (KDCREIT) has seen a decline in valuation premium. It is now trading at a PB ratio of 2.01X, which is at a level that was seen only at the start of the pandemic (Figure 4).

Figure 4: KDC’s valuation premium has dropped

We think that the decline in valuation premium of KDCREIT is possibly due to its potential acquisition of M1’s network assets, which would suggest that it will no longer be a pure-play data centre REIT. Additionally, there has been an increase in competition in the market due to the listing of DCREIT.

In our view, there is much to like about DCREIT. After all, it is sponsored by Digital Realty (NYSE:DLR), which is the world’s largest provider of cloud- and carrier-neutral data centres. With a market capitalisation of approximately USD 48 billion, Digital Realty is also one of the largest US-listed REITs.

The potential pipeline of data centres located globally that can be injected into DCREIT amounts to USD 15 billion (approximately SGD 21 billion), which dwarfs KDCREIT’s SGD 2 billion pipeline. With a gearing ratio of just 27%, we believe DCREIT has a strong ability to produce inorganic growth.

DCREIT trades at a PB ratio of 1.32X which is at a 30% discount to KDCREIT (Table 2). While DCREIT offers a lower distribution yield, we believe it is warranted due to its low gearing ratio and support from its strong Sponsor.

All in all, although we recognise that KDCREIT’s valuation is looking more attractive, we still like DCREIT more as we think there is more potential for growth.

Table 2: Comparison of data centre REITs

|

|

Digital Core REIT (DCREIT) |

Keppel DC REIT (KDCREIT) |

|

Sponsor |

Digital Realty |

Keppel |

|

Market Cap (SGD billion) |

1.7 |

4.2 |

|

Potential Pipeline (SGD billion) |

21 |

2 |

|

Gearing |

27.0% |

35.1% |

|

PB |

1.32X |

2.01X |

|

Yield* |

4.0% |

4.4% |

|

*Estimated yield in FY2022 Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 December 2021 |

||

(Related article: Quick Take: Investing in data centres? Here are the REITs to consider.)

Office: Longer-term outlook remains bleak

Following some progress made on the return-to-office at the start of 2021, the share price of office REITs largely saw a rebound.

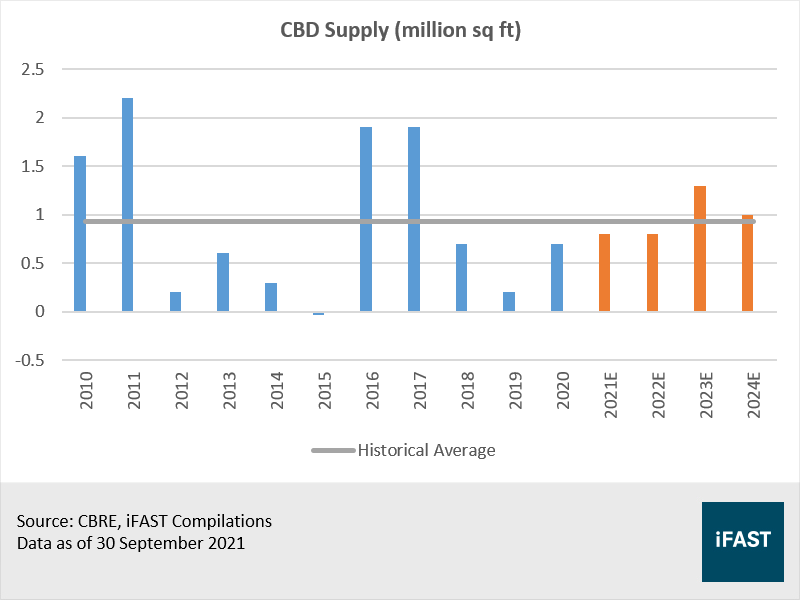

We note that the current office demand is mainly driven by growth sectors such as technology. This trend is likely to continue into 2022. Near-term central business district (CBD) rental rates are likely to be supported by a low level of supply. In 2022, 0.8 million sq ft of office spaces is expected to be completed, which is lower than the historical average of approximately 0.9 million sq ft (Figure 5).

Figure 5: Overview of CBD supply since 2010

However, we believe that there is less certainty over the long-term outlook of office REITs. More office supply is expected to be completed beyond 2022. Also, the increasing adoption of a hybrid work model may result in office space eventually being returned to the market. This leads to a likelihood of increasing vacancy rates, which could put a downward pressure on rental rates in the longer term.

Nonetheless, we think that most US-focused office REITs are worth highlighting for their attractive yields and the ability to deliver strong positive rental reversions (Table 3). One of the US-focused office REITs is Keppel Pacific Oak US REIT (SGX:CMOU), which has been under our coverage. It is the best performing office S-REIT in 2021, and while it is trading above its historical average, we believe it is justified.

Keppel Pacific Oak US REIT (KORE) is focused on the fast-growing tech sector, which has underpinned its resiliency and contributed to a YTD rental reversion of 8.3%. We have rolled forward our estimates, with an updated target price of USD 0.86. This represents an upside potential of 9% based on the closing price of USD 0.79 on 21 December 2021.

Table 3: Comparison of large office REITs and US-focused office REITs

|

Name |

Market Cap (SGD billion) |

Current PB (X) |

10Y Historical PB (X) |

Yield (%)* |

|

Singapore-focused |

||||

|

CapitaLand Integrated Commercial Trust |

13.0 |

0.96 |

1.25 |

6.0 |

|

Mapletree Commercial Trust |

6.6 |

1.15 |

1.16 |

5.0 |

|

Keppel REIT |

4.1 |

0.85 |

0.84 |

5.4 |

|

US-focused |

||||

|

Manulife US REIT |

1.6 |

0.94 |

1.02 |

8.9 |

|

Prime US REIT |

1.3 |

0.94 |

0.95 |

8.9 |

|

Keppel Pacific Oak US REIT |

1.1 |

0.96 |

0.91 |

8.1 |

|

*Estimated yield in FY2022 Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 December 2021 |

||||

Retail: Still not out of the woods

Following the relaxation of restrictions, the share prices of retail REITs have emerged from their depths.

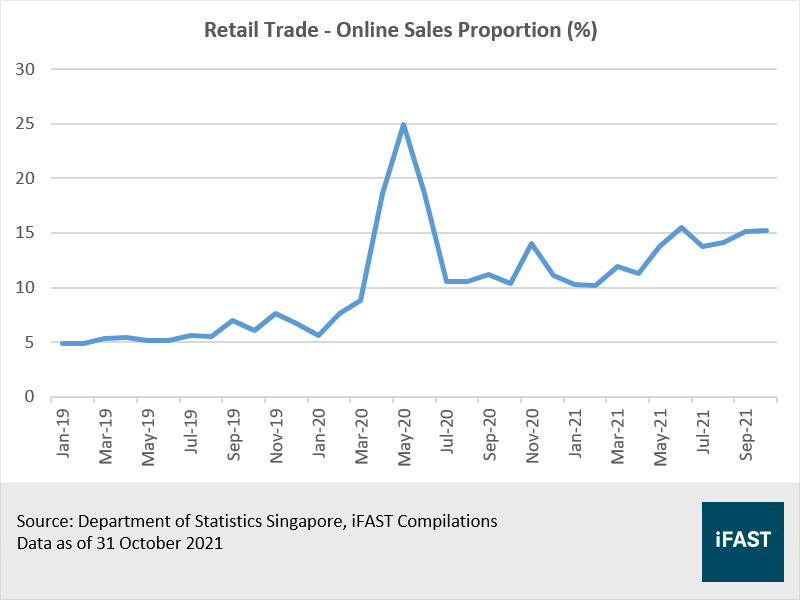

Nevertheless, we observed that the pandemic has changed the way consumers shop. With the acceleration of e-commerce, online retail sales proportion has also climbed throughout 2021 (Figure 6). That being said, suburban malls are still more resilient due to their higher exposure to essential goods and services.

Figure 6: Online sales proportion has been on an uptrend in 2021

In the near-term, we think retailers will continue to face a challenging operating environment as a result of supply chain disruptions. We also think that the provision of rental rebates is unlikely to go away in 2022, though it could be of a lower quantum.

Table 4 below summarises the valuations and yields of Singapore-focused retail REITs. While we acknowledge that retail REITs are trading below their historical averages, we think that they are not compelling when compared to other sub-segments, such as industrial. We also tend to prefer the industrial REITs who are beneficiaries of the rise of e-commerce.

Table 4: Comparison of Singapore-focused retail REITs

|

Name |

Market Cap (SGD billion) |

Current PB (X) |

Historical PB (X) |

Yield (%)* |

|

CapitaLand Integrated Commercial Trust |

13.0 |

0.96 |

1.25 |

6.0 |

|

Frasers Centrepoint Trust |

3.8 |

0.97 |

1.10 |

5.9 |

|

SPH REIT |

2.7 |

0.96 |

1.01 |

5.9 |

|

Starhill Global REIT |

1.4 |

0.74 |

0.84 |

6.8 |

|

*Estimated yield in FY2022 Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 December 2021 |

||||

Hospitality: A longer-than-expected recovery

As the return of international travel was off to a slow start, hospitality REITs have underperformed the broader sector yet again in 2021.

The emergence of the Omicron variant has served as a reminder that the fight against COVID-19 is far from over. This time round, travel restrictions have been imposed by governments around the world almost immediately. While this can help curb the spread of the new variant, the travel recovery is likely to be delayed. Against this backdrop, we see a lack of near-term catalysts that can drive a re-rating across hospitality REITs.

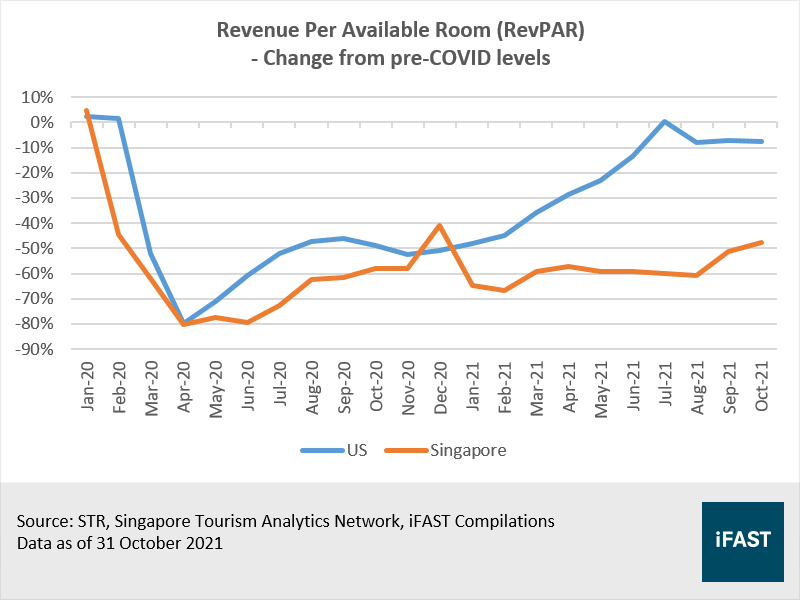

However, we continue to believe that domestic travel will make a faster recovery as compared to international travel. Thus, countries with sizable domestic markets would be resilient amidst the uncertainties. For instance, driven by a recovery of domestic leisure travel, the US hotel market has rebounded closer to pre-COVID levels (Figure 7).

Figure 7: The US hotel market has recovered faster

ARA US Hospitality Trust (SGX:XZL) has the greatest exposure to domestic travel demand. We believe that a resumption of distribution payout would be a major share price catalyst for the REIT. However, a key downside risk is a resurgence in COVID-19 cases, which would likely delay the distribution resumption.

Table 5: Comparison of hospitality REITs

|

Name |

Market Cap (SGD billion) |

Current PB (X) |

Historical PB (X) |

Yield (%)* |

|

Ascott Residence Trust |

3.3 |

0.85 |

0.89 |

5.4 |

|

CDL Hospitality Trust |

1.4 |

0.87 |

1.00 |

5.3 |

|

Far East Hospitality Trust |

1.1 |

0.73 |

0.76 |

4.8 |

|

Frasers Hospitality Trust |

0.9 |

0.71 |

0.88 |

6.7 |

|

ARA US Hospitality Trust |

0.3 |

0.78 |

0.74** |

7.5 |

|

*Estimated yield in FY2022 **Since June 2019 Source: Bloomberg Finance L.P., iFAST Compilations Data as of 21 December 2021 |

||||

Conclusion

Overall, we believe that the uneven recovery of S-REITs will continue into 2022. Consequently, the DPU growth will be varied. REITs in the sub-segments of industrial and data centres will continue to generate resilient growth, while the recovery of re-opening plays such as hospitality, office, and retail will be gradual.

Despite this, there are still pockets of opportunities within the sector and investors should continue to be selective (Table 6). Generally, we prefer the industrial and data centre REITs due to their stronger fundamentals, which can translate into a sustainable stream of passive income for investors.

Table 6: Stock picks for 2022

|

Sub-segment |

Top picks |

Rationale |

|

Industrial |

Frasers Logistics & Commercial Trust (SGX:BUOU) |

Attractive valuation, strong growth potential |

|

Ascendas REIT (SGX:A17U) |

Large and diversified portfolio, inorganic growth potential |

|

|

Data Centre |

Digital Core REIT (SGX:DCRU) |

Attractive valuation, strong Sponsor and growth potential |

|

Office |

Keppel Pacific Oak US REIT (SGX:CMOU) |

Resilient portfolio due to tech exposure, attractive yield |

|

Retail |

--- |

Acceleration of e-commerce, near-term downside risks |

|

Hospitality |

--- |

Conservative stance due to uncertainties over travel recovery |

|

Source: iFAST Compilations |

||

For investors who still prefer a passive approach, our recommended ETF is the NikkoAM-StraitsTrading Asia ex Japan REIT ETF (SGX:CFA), which has over 70% exposure to S-REITs.

Figure 8: DPU of S-REITs is only expected to return to pre-pandemic levels in 2023

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) holds a NIL position in the abovementioned securities. The analyst who produced this report holds a position in Keppel Pacific Oak US REIT.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.