- Data centres are an important component of the digital economy. Its demand is underpinned by the increasing adoption of cloud-based services as well as the shift towards 5G.

- Favourable demand and supply dynamics are expected to continue to drive up rental rates of data centres in Singapore. Meanwhile, China is a market with plenty of growth potential.

- Our recommended REIT to gain some exposure to data centres is Ascendas REIT (SGX:A17U), Its diversified portfolio of asset classes including data centres and logistics properties are positioned to ride on the key trends of the post-COVID economy.

Nonetheless, data centres are a growing asset class within the REITs space. In recent times, there has been a trend of REITs either acquiring data centres or planning to acquire data centres (Table 1). This is a considerable step away from the usual tall office skyscrapers or large retail malls that many REITs like to acquire.

Table 1: Increasing presence of data centres in REITs over the last 12 months

|

Date |

Name of REIT |

Ticker Code |

Description |

|

13 Jul 2020 |

Cromwell European REIT |

CWBU |

Entered into agreement with Stratus Data Centres to co-invest 50% stakes into two DC projects in Europe |

|

1 Sep 2020 |

Mapletree Industrial Trust |

ME8U |

Completed the acquisition of remaining 60% interest in 14 US DCs |

|

30 Sep 2020 |

CapitaLand China Trust |

AU8U |

Expanded investment mandate to cover DCs |

|

13 Mar 2021 |

Mapletree Industrial Trust |

ME8U |

Completed the acquisition of DC in Virginia |

|

17 Mar 2021 |

Ascendas REIT |

A17U |

Completed the acquisition of 11 DCs in Europe |

|

20 May 2021 |

Mapletree Industrial Trust |

ME8U |

Proposed acquisition of 29 US DCs |

|

Source: Companies, iFAST Compilations |

|||

Data centres are an important part of the digital economy

There is a good reason why an increasing number of REITs are moving towards data centres. In this increasingly digitalised world that we live in today, the importance of data centres cannot be understated. Data centres are an important component of the digital economy – they house core IT equipment required to collect, store, process, and distribute large amounts of data.

With the increasing adoption of cloud-based services as well as the shift towards 5G, data traffic is expected to grow rapidly, consequently leading to increasing spending on data centres. We believe this underpins the growing demand for data centres going forward.

The leases of data centres are typically long (can go up to 10 years) relative to other asset classes such as retail and office. Data centre leases often come with built-in rental escalations, which is not common in Singapore-focused commercial REITs. For instance, the portfolio of 29 US data centres that Mapletree Industrial Trust (SGX:ME8U) proposed to acquire has a weighted average lease expiry (WALE) of 7.9 years and a rental escalation of 1.5% to 3.0% per annum (for 89.4% of leases).

Hence, acquisitions of data centres can enhance the income stability of REITs as well as provide organic growth visibility. We believe this would translate into sustainable DPU for investors.

Attractive data centre markets

As one of the hottest real estate asset class, the global data centre market has been seeing continued growth. There are, however, some geographical markets that are more attractive than others.

In Cushman & Wakefield’s Data Center Global Market Comparison 2021 report, data centre markets around the world are ranked based on several factors. Factors that have been assigned the highest weightages during the scoring are cloud availability, fiber connectivity, and market size.

Cloud availability: This is determined by the access to the three major global cloud services which are Amazon Web Services, Microsoft Azure, and Google Cloud.

Fiber connectivity: The greater the number of fibre networks, the better connected the data centre is to distribute information at increased speed.

Market size: Large markets lead to increasingly scalable ecosystems across an ever-growing number of building expansions, networks, and software options.

Based on the methodology used by Cushman & Wakefield, the top data centre markets are as follows:

- Northern Virgina / Chicago / Silicon Valley / Dallas / Seattle / New York, US

- Sydney, Australia

- Singapore

- London, UK

- Amsterdam, The Netherlands

A market worth highlighting from the above is Singapore. The local market is highly sought-after by data centre operators. Over the past five years, there has been a rapid increase in the number of data centres being approved to be constructed on industrial state land.

However, due to land scarcity, Singapore is likely to face a constraint in supply of data centres. The government has temporarily paused the release of state land for data centres, as well as the development of data centres on existing state land. These favourable demand and supply dynamics are expected to continue to drive up rental rates of data centres in Singapore.

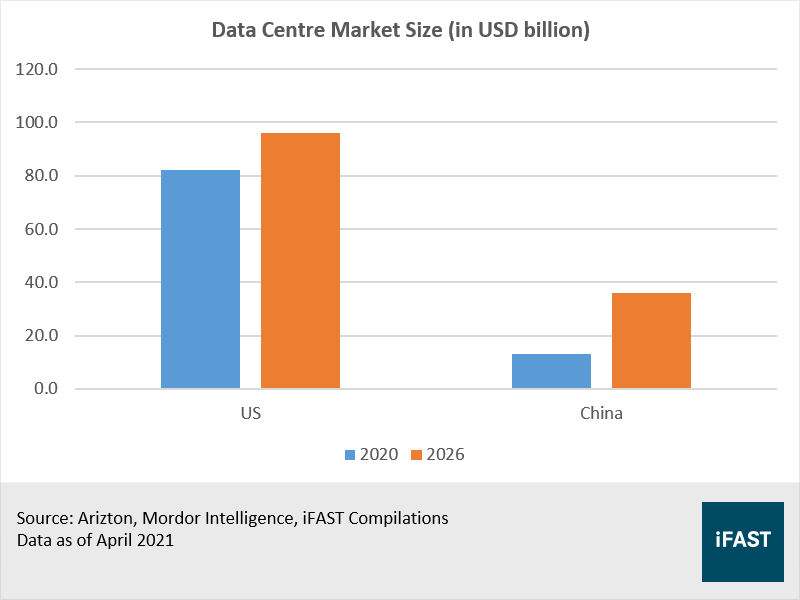

Meanwhile, one market that did not make the cut into Cushman & Wakefield’s top markets list is China. This is possibly due to the exclusion of Alibaba Cloud – China’s largest cloud service provider – in Cushman & Wakefield’s selection methodology. However, we think China deserves a mention as it is a market with plenty of growth potential.

Even though China’s data centre market is expected to double in size over the next five years, it is still underdeveloped as compared to the US (Figure 1). Moreover, unlike the US, China’s cloud computing industry is still in a nascent stage. Currently the fourth largest cloud service provider in the world, Alibaba Cloud could potentially rival other big players such as Amazon and Microsoft. As the cloud market expands, it could open up more opportunities for data centre operators.

(Related article: Alibaba Cloud: The next profit engine of China’s largest tech company)

Figure 1: China’s data centre market still underdeveloped as compared to the US

REITs that hold data centres

Table 2 below shows S-REITs’ exposure to data centres by geographical market/country. Do note that none of the REITs currently have an exposure to data centres in China, though CapitaLand China Trust (SGX:AU8U) has expanded its investment mandate to cover data centres.

Table 2: Data centres as a percentage of AUM

|

|

US |

Australia |

Singapore |

Europe |

Malaysia |

|

Keppel DC REIT |

- |

11% |

56% |

32% |

1% |

|

Mapletree Industrial Trust* |

49% |

- |

5% |

- |

- |

|

Ascendas REIT |

- |

- |

4% |

6% |

- |

|

*Post-acquisition of 29 US DC Data as of 31 March 2021 Source: Companies, iFAST Compilations |

|||||

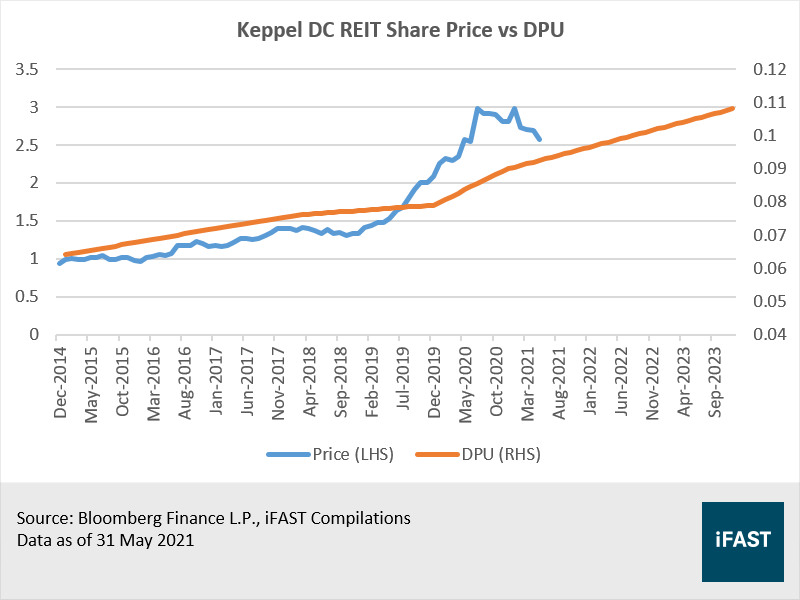

Keppel DC REIT (SGX:AJBU) is currently the only S-REIT that solely invests in data centres. Given that it is a pure-play data centre REIT, there is no surprise that its portfolio is the most geographically diversified. Compared to other REITs, Keppel DC REIT (KDC) also has the largest exposure to Singapore.

Meanwhile, Mapletree Industrial Trust (MINT) has the largest exposure to the US. Going forward, we can expect MINT to increase its exposure to data centres. It targets for the asset class to comprise up to two thirds of its portfolio, up from the current 54%.

Our recommended REIT to gain some exposure to data centres

As highlighted above, for a pure-play exposure to data centres, the only investment option in the local market right now is KDC. REITs with a higher exposure to data centres, including KDC, had a great run last year. While there has been a pull-back in recent months, KDC is still trading at a premium relative to the industrial REITs. Moreover, we believe that its average forward yield of 4.0% may be unattractive for investors who are seeking higher yields.

Figure 2: KDC Share Price vs DPU

Table 3: KDC DPU Growth

|

|

2020 |

2021E |

2022E |

2023E |

|

Yield (%) |

3.3 |

3.9 |

4.1 |

4.2 |

|

DPU Growth (%) |

20.5 |

9.1 |

5.0 |

2.9 |

|

DPU (SGD) |

0.092 |

0.100 |

0.105 |

0.108 |

|

PB Ratio (X) |

2.36 |

2.18* |

2.08 |

2.07 |

|

*Current PB Ratio Source: Bloomberg Finance L.P., iFAST Estimates Data as of 1 June 2021 |

||||

Therefore, we believe that investors can consider other REITs

with lower exposure to data centres to achieve a higher distribution yield. A REIT

with lower exposure to data centres does not necessarily mean that it has a

weaker outlook because data centres are not the only real estate asset class

that is fast-growing.

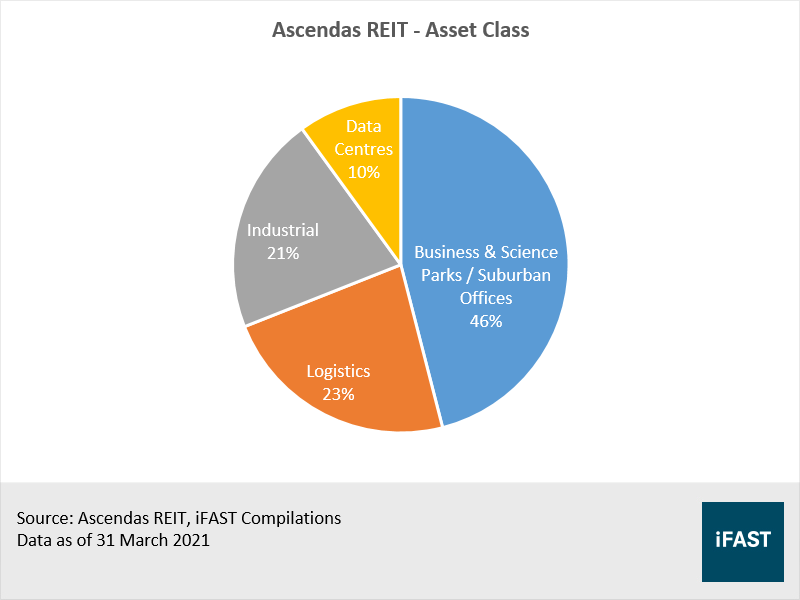

For instance, logistic properties is also a real estate asset class that is fast-growing, driven by structural tailwinds altered by the pandemic, such as the acceleration of e-commerce. From this perspective, we believe investors can consider REITs like Ascendas REIT (SGX:A17U). While it may have a lower exposure to data centres, it does have a good exposure to logistics properties (Figure 3) unlike MINT and KDC.

Figure 3: Ascendas REIT boasts a diversified portfolio

As highlighted in our 2021 outlook on S-REITs, our recommended REIT for the industrial and data centre sub-segment is Ascendas REIT (AREIT). This is on the basis of its diversified portfolio of asset classes such as data centres, suburban office properties, and logistics properties which are positioned to ride on the key trends of the post-COVID economy.

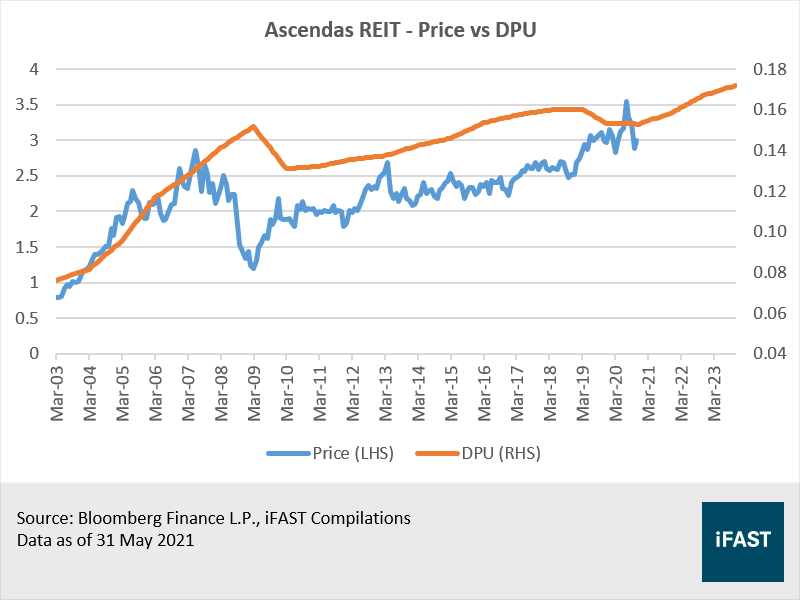

AREIT’s gearing ratio of 38.0% leaves a debt headroom of approximately SGD 3.8 billion. This would likely set the REIT up well for inorganic growth as well as opportunities to continue future-proofing its portfolio.

(Related article: Not all S-REITs are made the same, here's what you should look out for in 2021)

Figure 4: AREIT Share Price vs DPU

Table 4: AREIT DPU Growth

|

|

2020 |

2021E |

2022E |

2023E |

|

Yield (%) |

4.9 |

5.4 |

5.7 |

5.9 |

|

DPU Growth (%) |

27.8 |

7.5 |

5.7 |

3.0 |

|

DPU (SGD) |

0.147 |

0.158 |

0.167 |

0.172 |

|

PB Ratio (X) |

1.35 |

1.33* |

1.29 |

1.29 |

|

*Current PB Ratio Source: Bloomberg Finance L.P. Data as of 1 June 2021 |

||||

AREIT offers an average forward yield of 5.7%. It is an attractive option for income-seeking investors who are not too caught up over its relatively lower exposure to data centres.

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.