- Climate change and ESG investing is one of the recurring investment themes of 2021

- We recap the basics of ESG, and look through some common metrics and strategies employed by companies and fund houses today

- With the popularity of ESG, greenwashing has grown to be a pervasive and insidious issue, and we share some tips on how investors can navigate through this issue

As with many megatrends, ESG as a concept has existed for longer than most investors would expect. ESG investing began in January 2004, when Kofi Annan, then the Secretary General of the UN, invited major financial institutions to participate in a joint initiative to integrate ESG into capital markets. This eventually resulted in a report titled “Who Cares Wins” by Ivo Knoepfel, and thus the ESG movement was born.

The ESG movement was initially held back by two key reasons: (i) it was not seen as important at that time, and (ii) the lack of data and tools to collect and analyse the relevant data. This changed about 7 to 8 years ago when studies started to emerge showing that good ESG performance is associated with good financial results. The improvement of technology has also allowed for better data collection and analysis, allowing companies and investors to take the necessary actions in the hope of unlocking better financial performance.

Since then, there has been a remarkable paradigm shift towards ESG investing. While previously thought of as a supplementary consideration, it is now widely used as a key part of fundamental analysis. With climate change a menacing, pressing issue, ESG investment will continue to remain in the spotlight, and we would like to familiarise investors with some common metrics and strategies that are prevalent in the industry.

A ESG Primer – The basics, the metrics & the strategies

The Basics

ESG investing, or sustainable investing, is an investment approach that considers environmental, social and governance factors alongside traditional considerations in financial factors when it comes to investment decisions. A breakdown of the factors are as follows:

|

ESG Criteria |

Description & Examples |

|

Environmental |

The environmental criteria highlights a company’s impact and

consequence on the environment, including efforts to reduce or manage such

effects. Some factors to consider include climate change, emissions, deforestation and resource depletion. |

|

Social |

The social criteria considers a company’s relationships with its

stakeholders, as well as how fairly these stakeholders are treated.

Stakeholders include but are not exclusive to employees, suppliers, client

and communities. Some factors to consider include racial diversification, women representation, and adherence to workplace health and safety. |

|

Governance |

The governance criteria considers the internal system of practices,

controls, and procedures that apply when running a company. Good governance

can help align stakeholder interests and help to ensure the long-term

sustainability of a company. Rather than having factors to consider, some basic principles of good corporate governance include accountability, transparency, fairness and responsibility. |

When the topic of ESG gets brought up, the environmental criteria is typically the one at the forefront of most investors’ minds. However, investors should not neglect the other criteria, as they are arguably more important. While the environment factor gets more views and clicks, the other two factors are typically signs of a good, well-managed company, which are the companies that investors should look to invest in anyway.

The Metrics

ESG metrics are largely provided by third party agencies (much like bond ratings) that generally utilize their own methodology to collect and analyse data related to a diverse array of ESG issues. They can be roughly divided into the following groups, although there are companies that fulfil multiple roles:

1. Standard setters: These organisations generally provide standards for companies to meet, as well as structure and provide guidelines for ESG reporting. Examples of such organisations include the Sustainability Accounting Standards Board (SASB) and the Global Reporting Initiative (GRI). Another common standard practiced are basing guidelines off the United Nations Sustainable Development Goals (Fig. 1).

2. Data providers and aggregators: These organisations collect and provide data related to particular ESG issues. Many of these organisations double up as rating agencies, and they have their own methodology in evaluating how well a company complies with ESG standards. These include general data aggregators like Bloomberg and Thomson Reuters, as well as more specialized companies like Sustainalytics, which were acquired by Morningstar in 2020.

Fund houses also typically develop their own internal methodology to come up with ESG ratings, and they typically do so using the UN Sustainable Development Goals as a guideline. Their proprietary ESG methodologies are then integrated with the traditional investment framework as an additional risk or investment overlay as part of their decision making process.

Figure 1: Sustainable development goals established by the United Nations

Source: United Nations

While ESG reporting standards has come a long way, many challenges remain.

Issues relating to finding consensus with ESG metrics and a standardised

reporting system remain in limbo.

The complexity of the global geopolitical environment and the differences in operating practices across industries makes a standardized ESG benchmark challenging to establish, and ratings provided by the many ESG rating agencies tend to show low correlation due to the different methodologies used. Even from the perspective of fund houses, many of them use their own proprietary ESG ratings and measurements. For the truly ESG conscious investor, it is recommended to reconcile these differences by conducting their own due diligence.

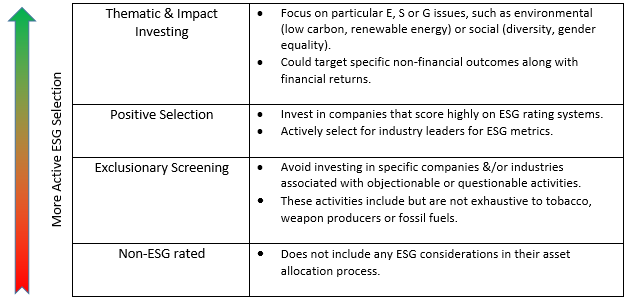

The Strategies

ESG strategies fall broadly into the following categories, with different levels of ESG incorporation:

Some examples of funds that

adhere to specific ESG strategies are as follows:

| Fixed Income/Multi-Asset | Equity | |

Thematic and Impact Investing |

| |

| Positive Selection | ||

| Exclusionary Screening |

Most fund houses already employ an exclusionary ESG screening filter to their investment process. |

Most fund houses already employ an exclusionary ESG screening filter to their investment process. |

^The above table is not an exhaustive list of the ESG funds available on the platform

There has also been an increase in the number of fixed income ESG funds available on the market, although these strategies rely mostly on exclusionary screening or positive selection of issuers to meet the ESG criteria. However, good ESG performance is an important consideration for fixed income investors as well, as poor ESG compliance often leads to regulatory or reputational risk, which could affect the company’s credit and its ability to finance its debt obligations.

Greenwashing

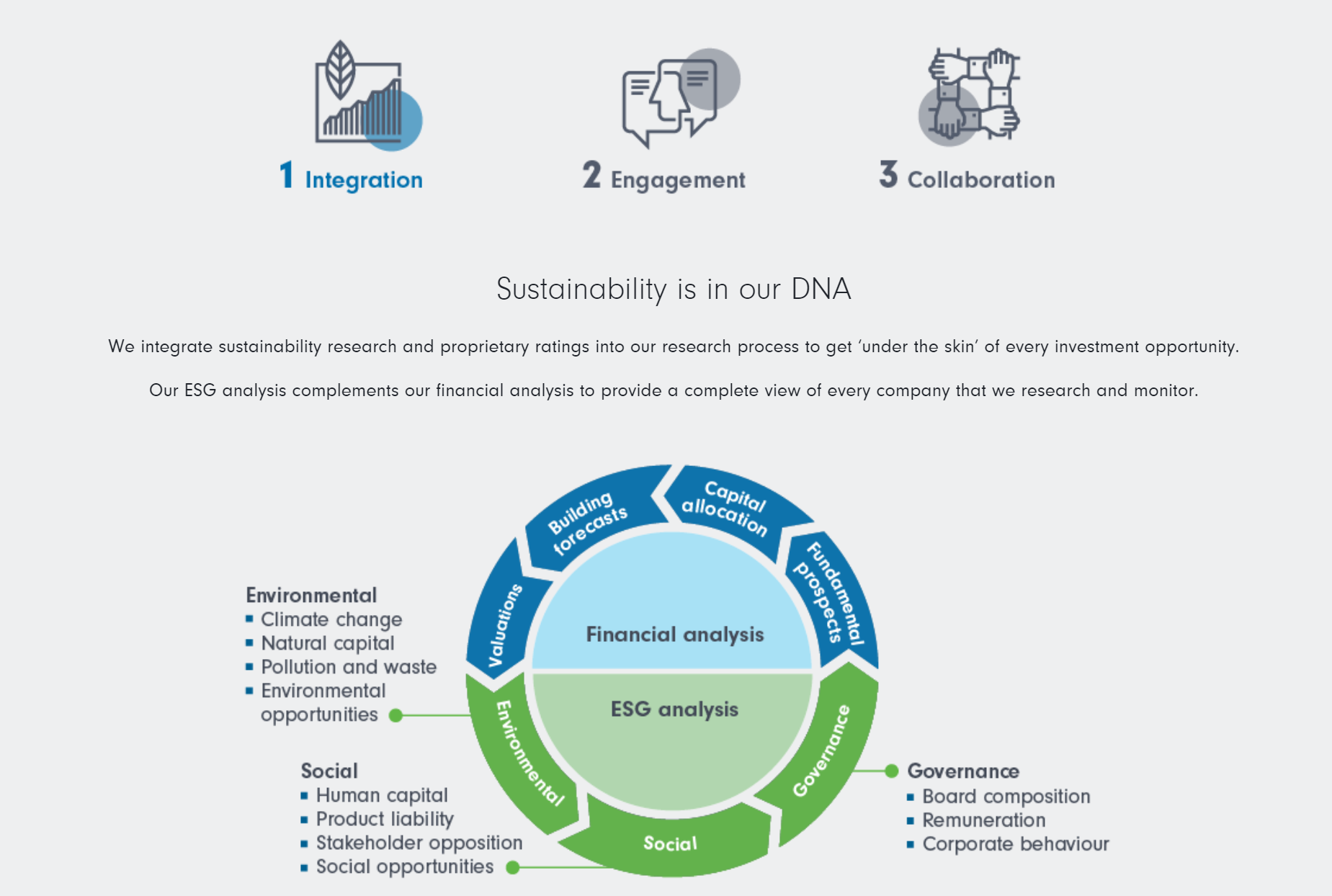

Figure 2: Fidelity’s methodology for ESG analysis

Source: Fidelity International

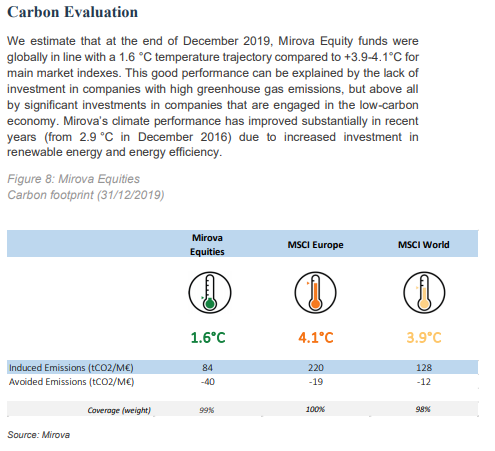

Another key consideration is whether the fund house can quantify the impact that their investment choices has made. For example, the Mirova Global Sustainable Equity Fund provides their key impact indicators, and it signifies their commitment to make their ESG efforts measurable. These numbers can typically be found in a fund house’s ESG reports, which is a good indicator of a fund house’s commitment.

Figure 3: Mirova ESG Report quantifying the carbon impact of their asset allocation

Source: Mirova Impact Report 2019

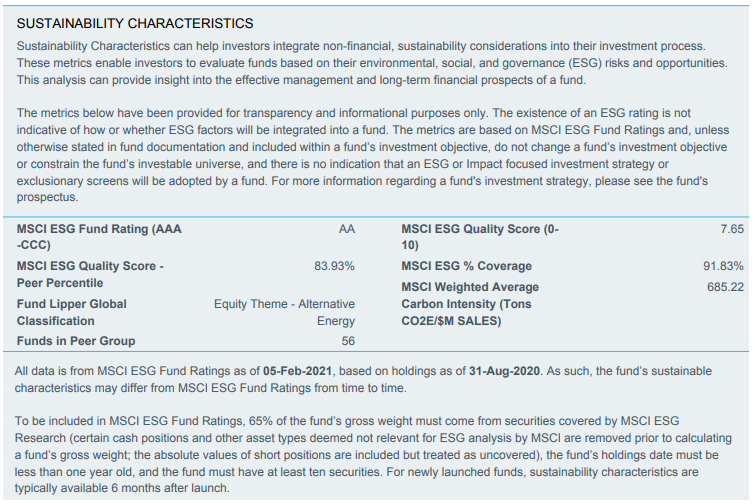

Finally, investors can look to external

ratings to get a good gauge on how closely a fund follows its ESG mandate.

Labels and awards are often listed in a fund factsheet, and these awards could

be issued by external agencies, such as MSCI, Bloomberg, or Morningstar with

its newly acquired Sustainalytics wing. These labels could also

be issued by governments or environmental agencies, and are good signs that a

fund follows through well with its ESG mandate.

Figure 4: MSCI ESG Fund Rating for Blackrock Sustainable Energy Fund

Source: BGF Sustainable Energy Fund Factsheet (Feb 2021)

Figure 5: ISR Rating issued by the French Ministry of Economy and Finance

Source: Natixis-Mirova Global

Sustainable Equity Fund Factsheet (Feb 2021)

Closing Thoughts

With significant fund flows and a renewed interest in climate change, ESG investing is certainly one of the hottest investment trends in 2021. Whether you believe ESG investing is here to stay or simply just a passing fad, we believe that is important for investors to stay aware of developments in the investment world. As part of our ongoing series, do keep an eye out for our next article, where we will look at the perennial question: “Do ESG funds outperform?”

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.