• The rights issues undertaken by SIA is expected to dilute its EPS by as much as 82%, assuming if the MCB are not redeemed before maturity.

• Based on a forward PE multiple of 15X and an estimated EPS of SGD 0.2 for FY23/24, we arrive at a target price of SGD 3.04 for SIA.

• With no domestic market to fall back on, any meaningful recovery will depend on how quickly international travel can resume. This depends on a multitude of factors which are beyond the company’s control.

• We believe that SIA shares are overvalued, and they have greater downside risk than upside potential over the next few years. Shareholders should consider letting go of their shares and redeploy their capital into more profitable ideas.

Figure 1: SIA share price has fallen significantly since the pandemic began

Rights issues will bring significant dilution to SIA’s EPS

In order to survive this difficult period, SIA has sought to strengthen its balance sheet through a mixture of aircraft secured financing, credit lines and more importantly, rights issues.

In April 2020, the company received approval from its shareholders to undertake a series of rights issues. To date, SIA has already completed its first rights issue, raising SGD 8.8 billion through a combination of rights shares and rights mandatory convertible bonds (MCB). On top of that, it also has the option of issuing up to SGD 6.2 billion worth of additional MCB if necessary.

Back in December last year, SIA said in a filing to SGX that it has already used up approximately 80% of the SGD 8.8 billion raised from the first rights issue. With air traffic not expected to return to pre-COVID levels anytime soon, we think that there is a good chance that SIA will proceed with the issuance of the additional MCB.

Given the huge sum of money raised from the first rights issues, the number of shares outstanding for SIA has increased substantially. This also means that SIA’s EPS will be much lower than before, because net income is spread over a large number of shares.

Table 1: Impact of rights issue on SIA’s EPS

|

FY18/19 Net profit |

682,700,000 |

|

FY18/19 EPS |

0.576 |

|

Number of shares before rights issue |

1,185,128,324 |

|

Impact of share rights |

|

|

Number of shares after share rights |

2,962,820,810 |

|

EPS after share rights |

0.23 |

|

EPS dilution |

59.9% |

|

Impact of rights MCB |

|

|

Number of shares assuming conversion of all rights MCB |

4,267,447,410 |

|

EPS assuming conversion of all rights MCB |

0.16 |

|

EPS dilution |

72.2% |

|

Impact of additional MCB |

|

|

Number of shares assuming conversion of all additional MCB |

6,567,128,196 |

|

EPS assuming conversion of all the additional MCB |

0.104 |

|

EPS dilution |

82% |

|

Source: Company data, iFAST calculations All units are in SGD, except number of shares |

|

How much are SIA’s shares worth?

According to the latest forecasts by International Air Transport Association (IATA), air travel is unlikely to recover back to its pre-COVID level until 2024 at the earliest. Assuming a scenario where SIA manages to achieve pre-COVID earnings in 2024, its EPS will only be SGD 0.23, 60% lower than what it would have been if there wasn’t any dilution.

However, given the uncertainties that lie ahead, we think that this scenario is overly optimistic and therefore unlikely to materialise. When air travel restarts, airlines should expect to see plenty of changes as new regulations are put in place to ensure the health and safety of passengers and the flight crew.

For instance, capacity limits could be implemented to adhere to social distancing measures. More thorough and frequent cleaning of aircrafts may also be required. All in all, these measures should result in higher costs and lower revenue, which will ultimately lower the bottom line for airlines.

Thus, we think that even if passenger traffic were to recover to their pre-COVID levels, SIA’s net income will likely be lower than before (Table 2).

Table 2: SIA earnings projections

|

FY18/19 |

FY19/20 |

FY20/21 |

FY21/22 |

FY22/23 |

FY23/24 |

|

|

Net income/loss (SGD millions |

682.7 |

-212 |

-4000 |

-2000 |

-500 |

600 |

|

Shares outstanding (millions) |

1185 |

1185 |

2962 |

2962 |

2962 |

2962 |

|

EPS |

0.57 |

-0.18 |

-1.35 |

-0.68 |

-0.17 |

0.20 |

|

Source: Bloomberg Finance L.P., Company Data, iFAST Estimations |

||||||

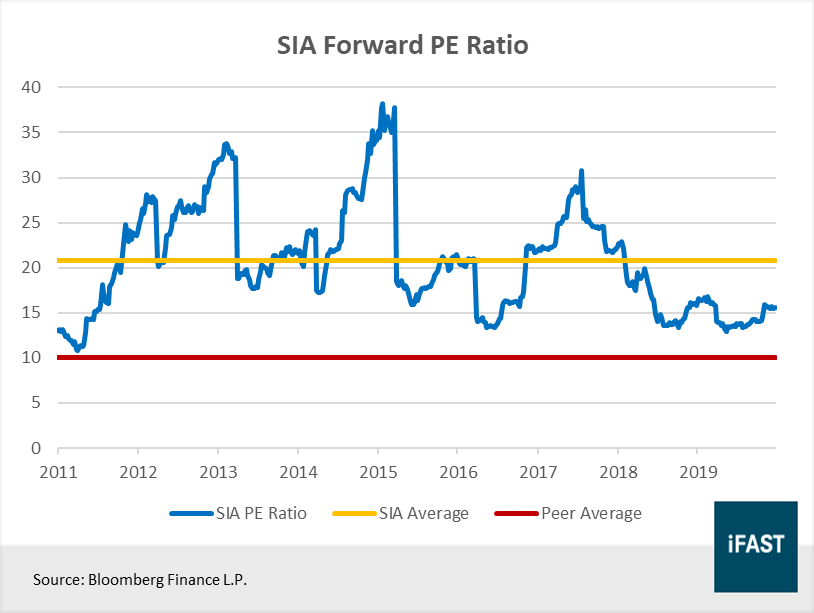

Historically, SIA has traded at a multiple of roughly 21X forward earnings. This is much higher than most full service airlines, which tend to trade at about 10X (Figure 2). Considering that SIA’s outlook will probably remain challenging for the foreseeable future, we think that investors will likely pay a lower multiple for its shares going forward.

Figure 2: SIA trades at a much higher PE ratio compared to its peers

Based on a forward PE multiple of 15X and an estimated EPS of SGD 0.2 for FY23/24, we arrived at a target price of SGD 3.04 for SIA. Our estimated EPS of SGD 0.2 is based on the assumption that SIA will (i) not issue the additional MCB, and (ii) redeem the MCB from the first rights issue before maturity.

Based on its latest closing price, markets are expecting SIA to achieve pre-COVID profitability by 2024, a scenario which we think is unlikely given the challenges the company is facing.

At this point in time, we believe that SIA shares are overvalued, and they have greater downside risk than upside potential over the next few years. Shareholders should consider letting go of their shares and redeploy their capital into more profitable ideas.

Outlook remains extremely challenging

Besides the dilution in earnings, SIA also faces a number of challenges that makes its road to recovery unpredictable. Compared to other airlines which operate in larger countries such as those in China or the US, SIA is in a particularly vulnerable position as it does not have a domestic market to fall back on.

Thus, any meaningful recovery will depend on how quickly international travel can resume. This in turn depends on a multitude of factors which are beyond the company’s control such as how quickly can the vaccine be distributed, its effectiveness in halting the spread of COVID-19 and more importantly, how quickly will borders reopen.

Recently, Singapore announced that it will suspend the reciprocal green lane arrangements with several countries given the resurgence of COVID-19 cases worldwide. New Zealand’s Prime Minister also said that the country is likely to keep its border closed to the world for most of 2021 amid a resurgence in cases and uncertainty over the rollout of vaccines. If more countries adopt similar measures, SIA should continue to incur losses at least until passenger traffic starts to recover.

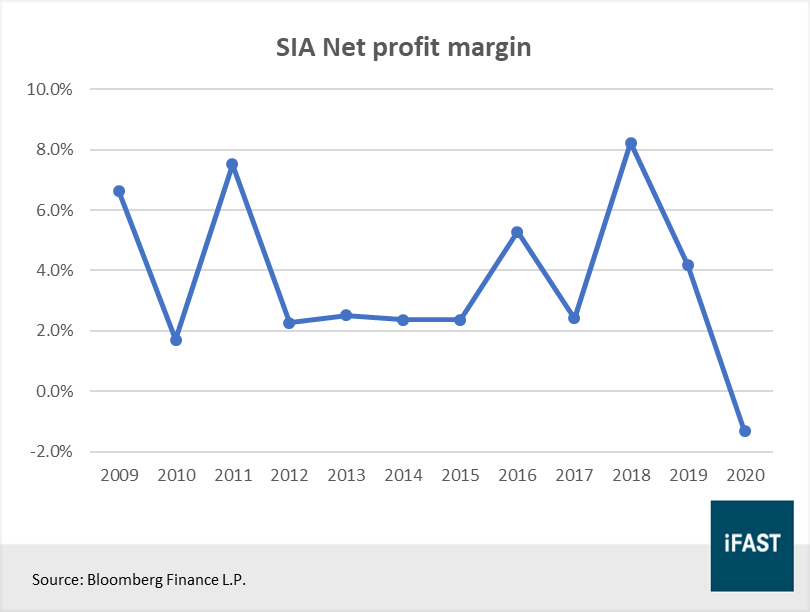

Last but not least, SIA has not been doing well even before COVID-19. The airline industry is extremely competitive, and the emergence of budget carriers has led to thinner margins over the years (Figure 3).

Figure 3: SIA’s net profit margin has been decreasing over the years

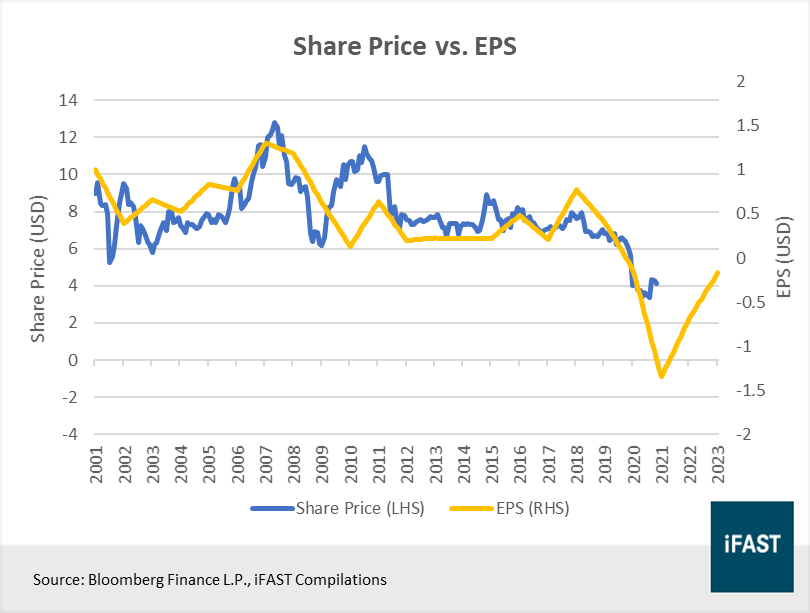

Overall, we think that SIA’s outlook is incredibly challenging. The slow resumption of international air travel would mean that earnings growth will likely remain weak. On top of that, if we take into account the impact of EPS dilution and the high probability of a compression in multiples, it should take the company several years before share prices can recover to their pre-COVID level.

Judging from SIA’s current share price, we believe that SIA shares have greater downside risk than upside potential over the next few years. Investors should consider letting go of their shares and redeploy their capital into more profitable ideas.

Figure 4: Share price vs EPS chart

Join our FSMOne Research Telegram channel today and stay up to date about our investment ideas!

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.