• Relative to other countries, China’s cloud computing industry is still in a nascent stage, and is filled with plenty of opportunities as the market expands.

• Accelerated adoption rates post COVID-19, together with extensive support from the central government, will spur the industry’s growth over the next decade.

• Alibaba Cloud is the largest cloud service provider in China, holding a market share of 41%. The unit is expected to achieve its first profitable quarter in 2021.

• The company’s vast ecosystem consisting of numerous subsidiaries and e-commerce merchants form a sizeable client base for Alibaba Cloud.

• Based on the sum of the parts methodology, we arrive at a target price of USD 346 for Alibaba which translates to an upside potential of approximately 33%.

Over the years, the global cloud services industry has experienced massive growth as companies migrate a greater portion of their workloads onto the cloud. However, much of this growth is confined to developed nations, such as the US, where the use of advanced technologies is generally more widespread compared to developing nations.

This has benefitted major cloud service providers, such as Amazon, Microsoft, and Google, all of which have seen earnings for their cloud services segment multiply over the years.

Unlike the US, China’s cloud computing industry is still in a nascent stage. As of 2019, it is estimated to be approximately one-tenth the size of the US (Figure 1). The relatively small size of China’s cloud computing industry suggests that there are still plenty of opportunities available for local cloud service providers, such as Alibaba Cloud, as the market expands.

Figure 1: China is home to the second largest cloud market in the world

Plenty of opportunities within China’s cloud computing industry

An important factor underpinning the future growth of China’s cloud computing industry is the massive wave of digitalisation that is sweeping across the country. Over the past two decades, China embarked on a journey of digital transformation that saw businesses across all industries and sectors starting to grow their presence online.

The search for sustainable and cost-effective ways to develop and maintain an online presence has led many businesses towards cloud computing, where companies rent a variety of IT services made available by the cloud service provider, paying a fee based on what they use.

In return, the cloud service provider handles everything from the installation and maintenance of hardware, to keeping the software up-to-date. Free from the burden of managing and maintaining their own IT systems, companies save a good deal of time and money, which can be spent on growing their core business.

Cloud computing has become increasingly popular among smaller businesses which may not be able to afford their own IT infrastructure. More importantly, as Chinese netizens develop an appetite for digital services, such as live streaming, short videos, and mobile gaming, demand for cloud services is expected to soar in the years ahead.

Looking forward, we believe that China’s cloud computing industry will experience extraordinary growth over the next decade, fuelled by rising demand and favourable tailwinds.

Industry’s growth supercharged by COVID-19 and supportive government policies

This year, COVID-19 has been an unexpected catalyst for China’s cloud computing industry. With most of the country placed under strict lockdown measures, business scrambled to invest in cloud computing infrastructure so that their employees can continue to work remotely. This resulted in a sharp increase in cloud services spend, which hit a record high of USD 5.0 billion in 3Q20, an increase of 70% year-over-year (Figure 2).

Figure 2: Cloud spending in China jumped to a record high thanks to COVID-19

With cloud computing being a life saviour for many businesses during this period, we foresee that adoption rates will continue to accelerate post-COVID-19 as businesses rethink the role of technology in their daily operations. Companies that have temporarily engaged cloud services during the COVID-19 period are likely to find them useful, and end up as long-term customers.

Besides the pandemic, another factor which could hasten the growth of China’s cloud computing industry is the extensive support of the central government. To aid China’s digital transformation, the government announced a multi-trillion yuan masterplan earlier last year to develop advanced technologies, such as artificial intelligence, 5G, and cloud computing.

With a renewed focus on digital transformation and accelerated adoption rates post COVID-19, China’s domestic cloud service providers should stand to benefit.

Alibaba Cloud the prime beneficiary of China’s booming cloud computing industry

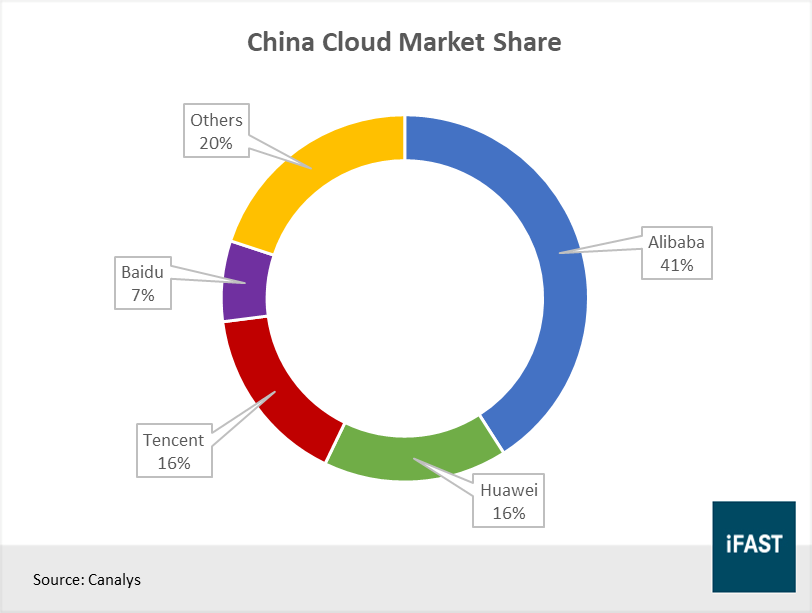

China’s cloud computing industry is fairly concentrated, dominated by a few major players. The largest of them all is Alibaba (NYSE:BABA), with a market share of 41%, bigger than the combined market share of its next three competitors. Alibaba is also the fourth largest cloud service provider in the world, with a market share of 6%, just slightly behind Google.

Given its sizeable footprint, we believe that Alibaba Cloud is in the best position to benefit from China’s burgeoning cloud computing industry.

Figure 3: Alibaba Cloud is the largest player in China’s cloud computing industry.

Much like Amazon (NASDAQ:AMZN), Alibaba (NYSE:BABA) has its roots in e-commerce before diversifying into other businesses as it expanded over the years. Outside of e-commerce, cloud computing is arguably the segment that holds the most promise at this point in time.

Alibaba Cloud, also known as Aliyun (阿理云), was established in 2009 to provide cloud computing services for Alibaba’s own use and to external businesses as well. Since its launch, Alibaba Cloud has experienced phenomenal growth.

Revenue for the segment has grown at a CAGR of 82% over the past three years, the fastest among all its segments. Comparatively, core commerce revenue grew at just 48% over the same period. Today, cloud computing has become Alibaba’s second largest business segment, accounting for 8% of its total revenue in FY 2Q21 (Figure 4).

Figure 4: Cloud computing has grown to become Alibaba’s second largest business segment

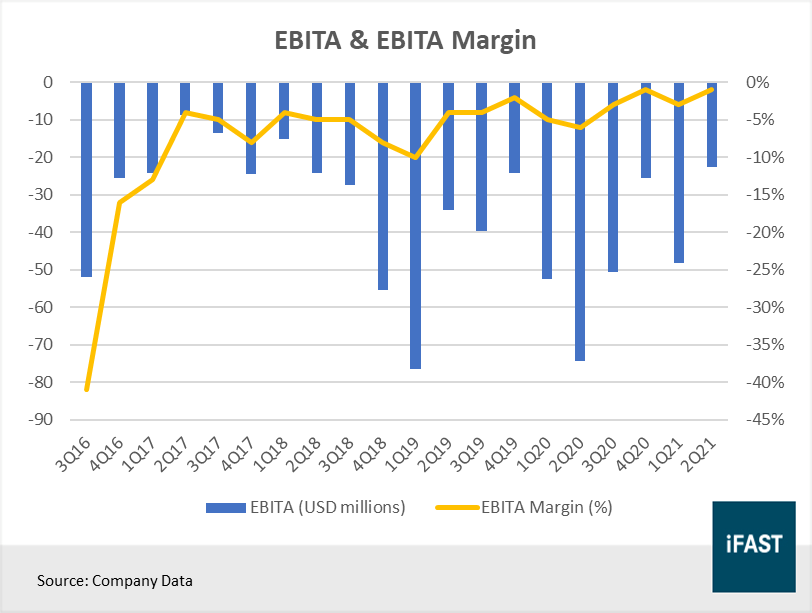

Even though Alibaba Cloud has experienced tremendous growth since the day it was launched, the segment is still loss-making, posting an EBITA of USD -22.6 million in FY 2Q21. However, the important thing is that the losses have been narrowing each year and the management expects it to achieve its first profitable quarter in 2021 on the back of rising demand for cloud services post COVID-19.

Given the tailwinds behind the industry and the segment’s long-term growth trajectory, we are optimistic that cloud computing will eventually become a significant contributor to the company’s bottom line, similar to the case of AWS and Amazon.

Figure 5: Alibaba Cloud is on the brink of profitability

Competitive position backed by heavy investment and vast ecosystem

With China placing a greater emphasis on digital transformation and the growing demand for cloud services, Alibaba plans to secure its position within the industry by investing CNY 200 billion over the next three years in its cloud computing unit.

The majority of the money will be spent on building new data centres, both within and outside of China, expanding its global footprint. It will also upgrade its existing infrastructure, such as servers and chips, while hiring 5,000 new staff to help grow the unit.

At the moment, Alibaba Cloud is available in 22 regions around the world, and its services are used by 40% of the Fortune 500 companies. With its ambitious expansion plans, Alibaba aims to capitalise on the rising demand for cloud services and become the world’s leading cloud service provider by 2023.

Another advantage that Alibaba possesses is its vast ecosystem. Having invested in so many businesses, the company’s numerous subsidiaries and merchants on its e-commerce platform form a sizeable client base for Alibaba Cloud.

Since the outbreak of COVID-19, the company has rolled out a series of cloud-based solutions, such as remote working, learning and collaborative tools, which has been widely popular among its clients, and have contributed positively to the unit’s revenue growth.

Potential pitfalls to look out for

Despite the rosy outlook, Alibaba Cloud faces a number of potential headwinds that could hinder its growth.

Intensifying competition from rivals: Within its domestic market, competition is heating up with local players such as Tencent and JD aggressively expanding their cloud units. In overseas markets, the company may also encounter competition from foreign players, such as Amazon (NASDAQ:AMZN), which has been in the cloud business for much longer than Alibaba (NYSE:BABA) has.

Overseas expansion could be derailed by US ban: In addition, as part of its Clean Network Initiative the Trump administration has been calling for US firms to ditch the use of Chinese technology including cloud services. This could derail the unit’s overseas expansion plans. However, with Biden at the helm the relationship between US and China could very well turn for the better.

Antitrust regulations proposed by the government: Back in November, the Chinese government unveiled a set of draft rules to curb the use of monopolistic practices among China’s tech giants. However, we believe that this will not have a major impact on Alibaba as the company has succeeded not because of significant anticompetitive behaviour, but rather its network effect and superior product offerings.

Related Article: Quick Take: What impact will the recent antitrust regulations have on Chinese tech companies?

Further upside available for Alibaba

Overall, we continue to remain optimistic about the growth potential of Alibaba Cloud, as well as the future of the company as a whole. We have fine-tuned our sum-of-the-parts valuation methodology to take into account the significant growth of Alibaba Cloud and its contribution to the company (Table 1).

Through that, we arrive at a target price of USD 346 for Alibaba (NYSE:BABA), which translates to a potential upside of approximately 33%.

Table 1: Sum-of-the-parts valuation for Alibaba

|

Business Segment |

Shareholding |

Valuation (CNY millions) |

Valuation Methodology |

Multiple |

Weighted Valuation (CNY millions) |

|

Core Commerce |

100% |

196,247 |

PE |

30X |

5,887,404 |

|

Cloud Computing |

100% |

9,904 |

PE |

20X |

198,079 |

|

Ant Group |

33% |

233,333 |

Estimated market value |

- |

233,333 |

|

Total value (CNY millions) |

6,318,817 |

||||

|

# of shares (millions) |

2705 |

||||

|

2022 Target price (USD) |

346 |

||||

|

Current share price (USD) |

260 |

||||

|

Upside potential |

33% |

||||

|

Source: Bloomberg Finance L.P. Company Data, iFAST Estimates Data as of 21 Jan 2021 |

|||||

Considering the exciting growth prospects of China’s cloud computing industry and Alibaba’s competitive advantage in this space, we believe that the company is positioned to do well as China’s digital transformation gets under way. Investors who are interested in the long-term growth story of this company may consider taking a position now.

Table 2: Alibaba is projected to have strong earnings growth beyond COVID-19

|

FY 2020 |

FY 2021 |

FY 2022 |

FY 2023 |

|

|

PE Ratio (X) |

34.7 |

25.8 |

21.3 |

17.2 |

|

Earnings Growth |

32.9% |

35.1% |

21.2% |

23.3% |

|

EPS (USD) |

7.6 |

10.3 |

12.5 |

19.1 |

|

Source: Bloomberg Finance L.P. Data as of 21 Jan 2020 |

||||

Figure 6: Alibaba’s share price vs. earnings per share

Declaration:

For specific disclosure, at the time of publication of this report, IFPL (via its connected and associated entities) and the analyst who produced this report hold a NIL position in the abovementioned securities.

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.