- Some investors might be overly-focused on dividends

- Dividend-paying stocks have disadvantages – taxes and fees

- Catering theory suggests firms increase dividend pay-outs when investors demand for higher dividends

- Current situation might suggest a relatively lower dividend premium for real economy stocks

- Investors should be wary of investing in high yielding sectors and stocks – invest in active/passive funds instead

Now that bond yields are so low, investors are turning towards high yield and dividend-paying stocks for income. However, is it wise?

Total returns = capital appreciation + dividend payouts

Theoretically, when a stock pays dividends, it would lead to a similar decrease in the stock’s price. Then, theoretically, it also means there should not be any difference in returns between a dividend paying and non-dividend paying stock.

Of course, in theory there is no difference between theory and practice. In practice, there is. Due to behavioural and practical issues, we tend to treat dividend gains and capital gains separately. For one, when we look at our investment holdings, we are only looking at price changes, and unless we keep our own Excel spreadsheets, we tend not to include dividends in our total returns.

Also, research has also shown that income-focused investors tend to neglect the capital gains portion and hold on longer to stocks that pay more dividends. This tunnel vision could actually negatively affect your portfolio returns, which we will explain along the way.

The simple math against dividends

The simplest argument against dividend stocks would be fees and taxes. Singapore has no capital gains tax nor dividend tax, thus it will not be a factor. However, foreign stocks are a different story. For example, US has 30% withholding tax for dividends. Along with withholding fees, it makes no logical sense to choose a firm that pays dividends over a firm that does not, provided they have the same characteristics.

Furthermore, if considering from a re-investment viewpoint, dividend-paying stocks make even less sense as you have to pay extra fees if you choose to re-invest the dividends. Furthermore, if your dividends are not big enough, you may not be able to re-invest too. Even when invested in a growth stock, one can have their own income payments by carving out shares. Thus, dividend yields should not be the top concern that investors have when investing.

What we should then be looking at is expected total return.

Do dividend-paying stocks return higher than non-paying stocks?

Although a 2013 paper by JP Morgan showed that returns of S&P 500 dividend-paying stocks significantly outperformed those of non-dividend paying stocks from 1973 to 2013, the research seemed too simplistic and there are other factors that could have contributed to the outperformance. Furthermore, they did not control for other factors too, i.e. firm characteristics.

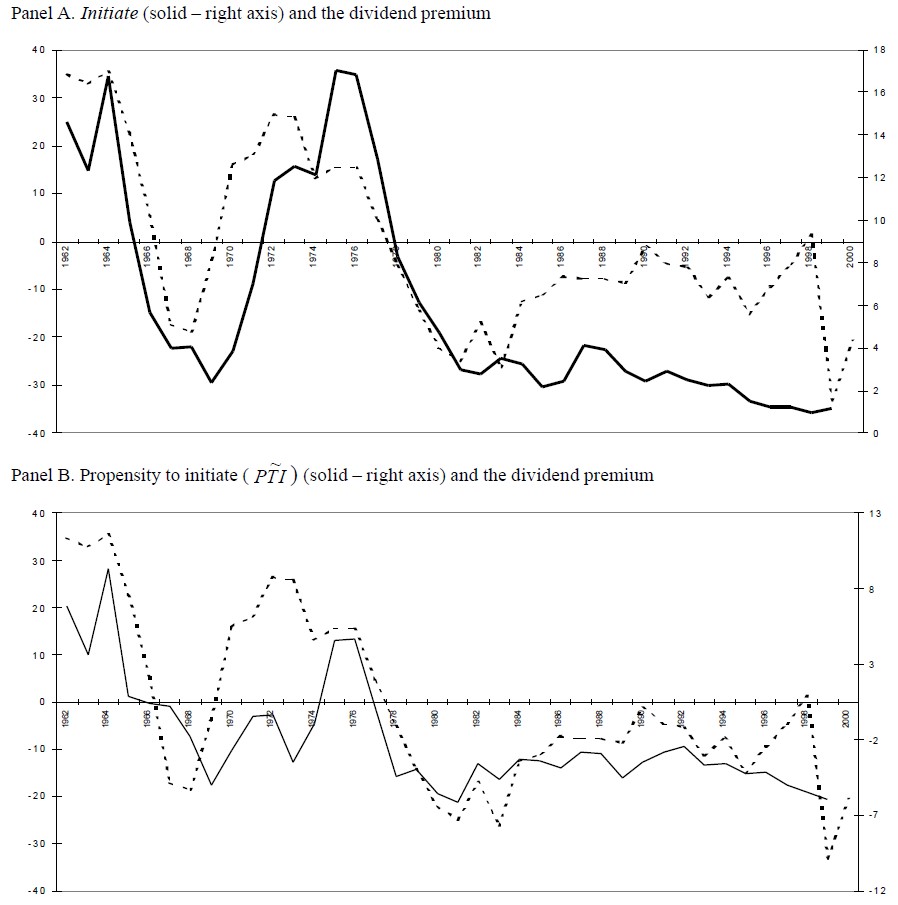

The common narrative about dividend-paying stocks tells us that if a company increases dividend pay-outs, it could be signalling stronger cash-flow growth or a lack of re-investment opportunities. However, Baker and Wurgler (2003) came up with a theory that suggests the opposite is happening – firms start paying dividends when investors demand for more dividends and vice versa. They called it the catering theory as it caters to investors’ wants.

Chart 1: Non-paying firms tend to initiate dividend payouts when investors demand for dividends

Source: Baker and Wurgler (2003), A Catering Theory of Dividends

Logically, when investors demand for dividends, they will then tend to overbid for dividend-paying stocks, which results in the dividend premium. From the paper, “when the initiation rate increases by one standard deviation, returns on payers are lower than nonpayers by nine percentage points per year over the next three years. Conversely, the omission rate increases when the dividend premium is low, and when future returns on payers are high.” Karpavicius and Yu (2015) Also suggests that “stock prices of dividend payers are greater by 5.3% or 27.9% on average (depending on methodology) than those of nonpayers)”.

The above passage simply suggests that a period of high dividend premium could lead to higher dividend pay-outs from companies, but will affect future returns negatively as dividend stocks become an over-crowded trade. Thus, as is common to investing, by approaching dividend stocks with a contrarian style, investors can have a higher chance of getting better returns.

Are we in a period where dividend sentiment is high?

Intuitively, when interest rates and yields are low, demand for dividends should be higher as income-focused investors who were initially invested in bonds will seek income elsewhere. Also, when growth stocks are more popular (when they are outperforming), dividend premium tends to be lower or negative.

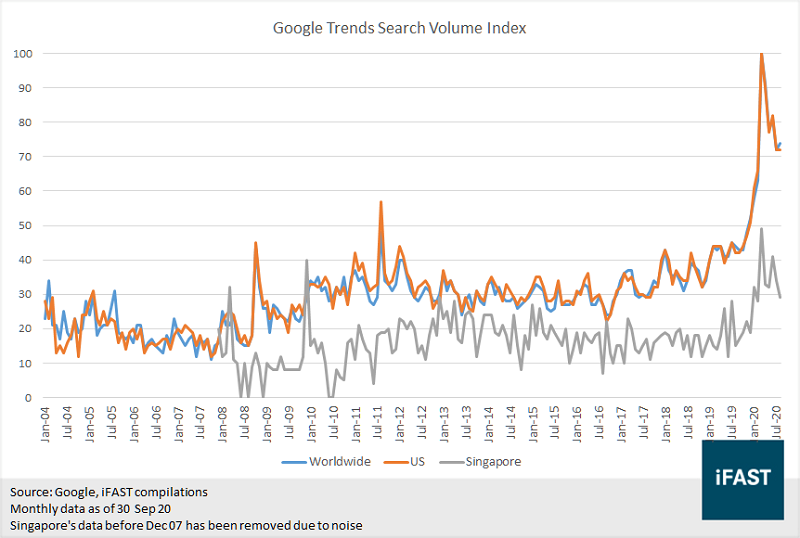

For a more concrete measure of dividend sentiment, one can use Google Trends too. Kumar, Lei and Zhang (2020) did just that and used the search volume index (SVI) from Google Trends to form a long/short trading strategy based on the monthly percentage change in SVI which generated an annualized risk-adjusted return of 8.6%.

They also found that “a 10% increase in the SVI for the search topic ‘dividend’ is associated with a significantly positive price change of 19 basis points in the following month”. However, this positive effect does not last forever and by month 9, the coefficient turns negative, suggesting that “dividend sentiment generates short-term overpricing among high dividend stocks”.

Due to the huge fall in prices and interest rates, dividend sentiment climbed to an extreme high in March, even higher than during the Great Financial Crisis as seen by the Google Trends SVI. Thus, this may suggest that dividend premium is at an extreme high.

Chart 2: Google Trends SVI of search term “dividend stocks”

However, due to the global lockdown measures, we find ourselves in a peculiar situation. Many companies are not able or forced to not pay dividends with 27% of global firms cutting their dividends and global dividend payments decreasing by 22% in the second quarter.[i]

This leads to a situation where sectors typically attributed as growth sectors are experiencing dividend growth, whereas real-economy sectors such as financials, energy, etc. have to cut dividends due to poor economic conditions. Looking at the below table, Bloomberg estimates that the MSCI ACWI Consumer Discretionary sector will have a lower dividend yield compared to MSCI ACWI IT sector for this year.

Thus, it is also plausible that the dividend premium typically associated with high dividend-paying stocks could be attached to growth stocks since they can deliver on dividends and price appreciation during this period. And while dividend sentiment is high, the dividend premium typically attached to dividend-paying stocks could be low due to the fact that most of them are not able to pay dividends. The tables below help explain the situation better.

Table 1: Numbers for 2020

|

Sector |

Dividend Growth |

YTD total returns |

Est. 2020 dividend yields (%) |

|

MSCI ACWI Consumer Discretionary Index |

-35.15% |

18.61% |

0.87 |

|

MSCI ACWI Energy Sector Index |

-22.99% |

-45.34% |

6.27 |

|

MSCI ACWI Financials Index |

-19.38% |

-23.44% |

3.54 |

|

MSCI ACWI Industrials Index |

-14.33% |

-4.69% |

1.89 |

|

MSCI ACWI Materials Sector Index |

-4.82% |

-0.11% |

2.78 |

|

MSCI ACWI Consumer Staples Index |

0.64% |

-0.85% |

2.70 |

|

MSCI ACWI Utilities Sector Index |

1.61% |

-6.17% |

3.77 |

|

MSCI ACWI Health Care Index |

5.53% |

4.54% |

1.81 |

|

MSCI ACWI Information Technology Index |

6.60% |

24.28% |

1.22 |

|

Source:

Bloomberg Finance L.P., iFAST estimates |

|||

Table 2: Bloomberg estimated dividend yields

|

Est. dividend yields (%) |

2020 |

2019 |

2018 |

|

MSCI ACWI Energy Sector Index |

6.27 |

4.45 |

4.43 |

|

MSCI ACWI Utilities Sector Index |

3.77 |

3.48 |

3.89 |

|

MSCI ACWI Financials Index |

3.54 |

3.36 |

3.79 |

|

MSCI ACWI Materials Sector Index |

2.78 |

2.92 |

3.65 |

|

MSCI ACWI Consumer Staples Index |

2.70 |

2.66 |

3.00 |

|

MSCI ACWI Industrials Index |

1.89 |

2.1 |

2.53 |

|

MSCI ACWI Health Care Index |

1.81 |

1.79 |

2.05 |

|

MSCI ACWI Information Technology Index |

1.22 |

1.42 |

1.97 |

|

MSCI ACWI Consumer Discretionary Index |

0.87 |

1.59 |

2.03 |

|

Source:

Bloomberg Finance L.P., iFAST compilations |

|||

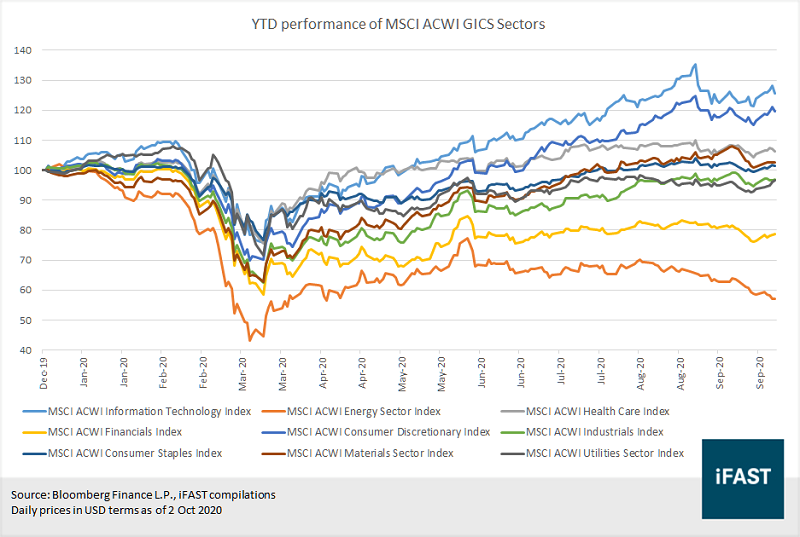

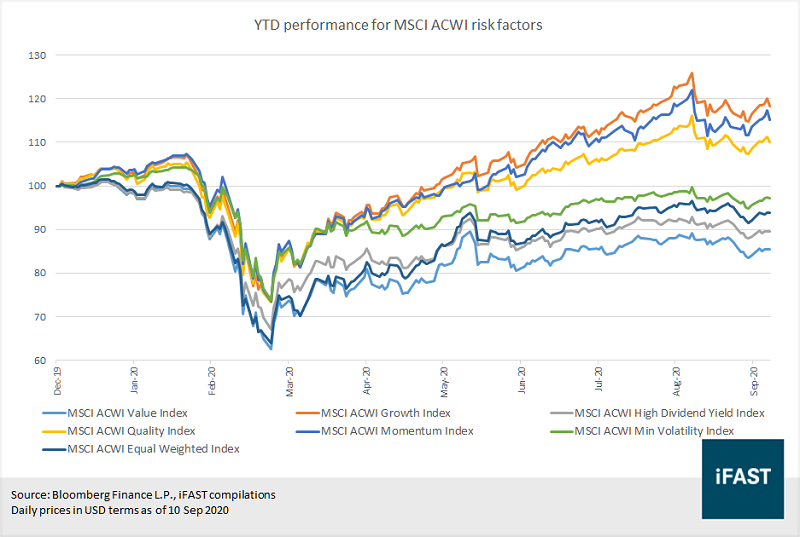

If we look at year-to-date price performance, the difference is stark. Sectors and risk factors that are associated with the real economy have hardly pared back their losses this year.

Chart 3: YTD performance of MSCI ACWI GICS sectors

Chart 4: YTD performance for MSCI ACWI risk factors

How to position?

Obviously, investing solely based on high dividend yields is not the best idea. If you have invested in sector and country indices that give the highest dividend yields, your portfolio performance would have suffered while waiting for the dividend pay-outs as seen in Table 1 and Table 3.

Table 3:

|

Est. dividend yield (%) |

YTD total returns (%) |

|

|

Straits Times Index STI |

3.88 |

-19.15 |

|

STOXX Europe 600 Price Index EUR |

2.93 |

-10.68 |

|

MSCI Emerging Markets Latin America Index |

2.91 |

-36.30 |

|

MSCI Emerging Markets Index |

2.29 |

-0.94 |

|

MSCI AC Asia Ex. Japan Index |

2.16 |

5.68 |

|

Shanghai Shenzhen CSI 300 Index |

2.00 |

14.25 |

|

S&P 500 Index |

1.77 |

5.13 |

|

Nikkei 225 |

1.76 |

0.30 |

|

Source:

Bloomberg Finance L.P., iFAST estimates |

||

However, there are ways to enjoy higher returns without sacrificing on dividend yields. Instead of taking a concentrated approach of investing in sectors/countries/stocks with the highest dividend yields, one can invest in a diversified manner via global equity funds that also offer attractive dividends. Fund managers help to ensure that these stocks are able to maintain, or even grow their dividends, even during sub-optimal market conditions, helping us to avoid yield traps.

Table 4:

|

YTD total return (%) |

Indicated yield (%) |

|

|

iShares MSCI ACWI ETF |

3.12 |

1.54 |

|

United Global Durable Equities Fund |

-3.14 |

5.61 |

|

Nikko AM Global Dividend Equity Fund |

-3.34 |

5.13 |

|

BGF - Global Equity Income Fund |

-3.65 |

3.52 |

|

Vanguard High Dividend ETF |

-10.01 |

3.48 |

|

Source: Bloomberg Finance L.P., iFAST estimates |

||

Indicated yield can be calculated by taking latest dividend pay-out*dividend frequency/latest NAV*100.

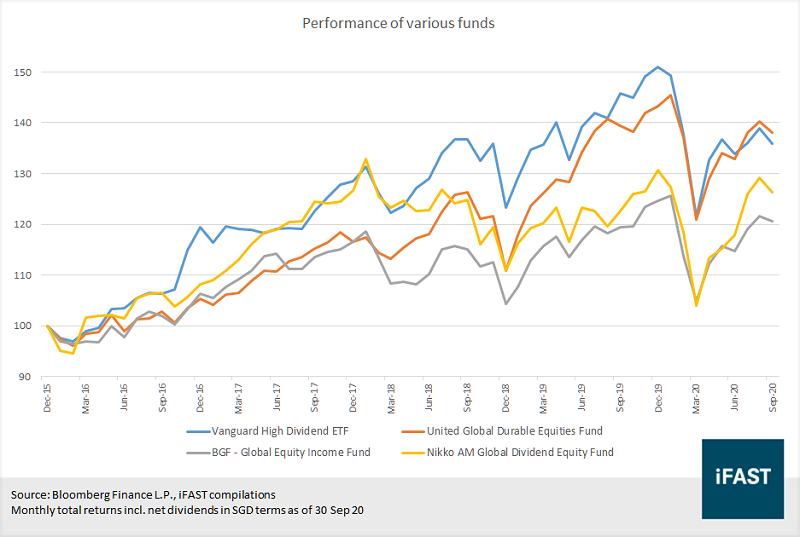

Chart 5: Performance of various funds

While the actively managed global dividend equities funds have outperformed the Vanguard High Dividend ETF year-to-date, they have not been consistent in outperforming it in the past. If you are an investor investing small amounts of money, it might be better to opt for the United Global Durable Equities Fund due to re-investment benefits and cost-savings.

Catalysts are needed

While prices have diverged, we have to see some signs of the real economy being supported for this investment idea to start out-performing. If firms are still held back from paying dividends by falling profits and regulations, it is then unlikely that interest will be renewed on dividend-paying stocks.

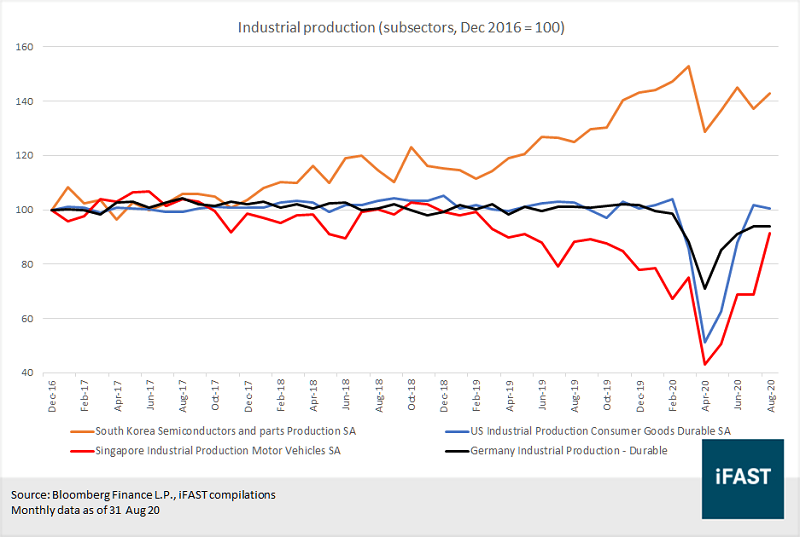

If we look at industrial production data of some of the major manufacturing hubs across the world (China is excluded due to lack of index data), industrial production has yet to recover to pre-lockdown levels. For Singapore, industrial production has bounced higher but is mainly due to electronics.

Chart 6:

On the bright side, production of automobiles and durable goods have recovered strongly, which could be due to government pay-outs (or funds as people save on holidays). If this trend continues, industrial sector and consumer discretionary sector stocks could perform better too. However, the waning of stimulus and the possibility of a second wave could dampen things.

Chart 7:

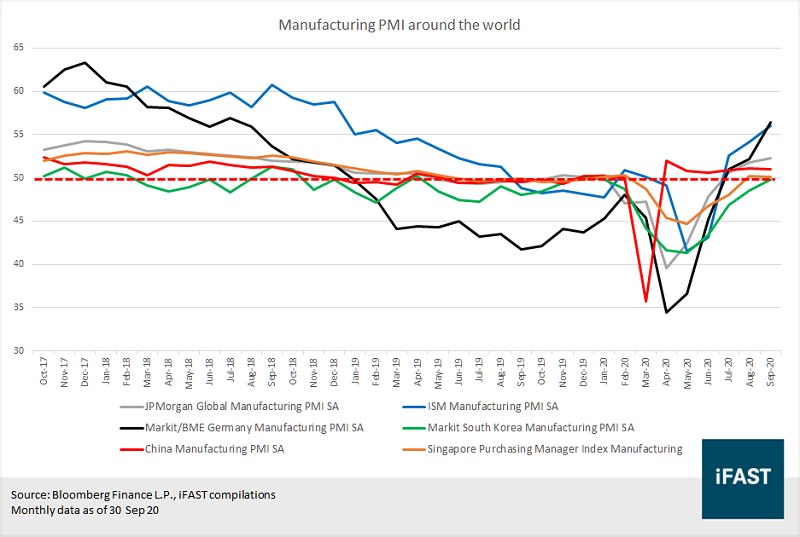

If we look at manufacturing PMI, Germany’s and US’ data looks to be positive although we see some signs of manufacturing stalling in the Asian countries. Thus, the signs of the real economy recovering still seem to be mixed.

Chart 8:

While the investment thesis appears to be sound, the lack of impetus to a strong economic recovery is most concerning. However, stock prices will move before the global economy recovers, thus investors will have to play a waiting game. It is also more likely that dividend pay-outs will resume next year than this year. If investors are willing to take the risk of underperforming in the short-term, they can choose to invest in these three funds - United Global Durable Equities Fund, Nikko AM Global Dividend Equity Fund and BGF - Global Equity Income Fund.

References

Baker, Malcolm and Wurgler, Jeffrey, A Catering Theory of Dividends (March 2003). https://www.nber.org/papers/w9542

Conolly, Mariana and Hart, Clare, Dividends for the long term (April 2013). https://am.jpmorgan.com/blobcontent/1378404661562/83456/11_295_Dividends%20for%20the%20long%20term.pdf

Karpavicius, Sigitas and Yu, Fan, Dividend Premium: Are Dividend-Paying Stocks Worth More? (August 19, 2015). Available at SSRN: https://ssrn.com/abstract=2647256 or http://dx.doi.org/10.2139/ssrn.2647256

Kumar, Alok and Lei, Zicheng and Zhang, Chendi, Dividend Sentiment, Catering Incentives, and Return Predictability (September 11, 2020). University of Miami Business School Research Paper No. 2875114, Available at SSRN: https://ssrn.com/abstract=2875114or http://dx.doi.org/10.2139/ssrn.2875114

Vogel, Jack (2017). A Direct Test of the Dividend Catering Hypothesis. Retrieved 6 September 2020, from https://alphaarchitect.com/2017/05/18/direct-test-of-the-dividend-catering-hypothesis/#gs.3fO_1AM

All materials and contents found in this site are strictly for general circulation and informational purposes only and should not be considered as an offer, or solicitation, to deal in any of the funds or products found/identified in this site. While iFAST Financial Pte Ltd ("IFPL") has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies and typographical errors. Any opinion or estimate contained in this report is made on a general basis and neither IFPL nor any of its servants or agents have given any consideration to nor have they or any of them made any investigation of the investment objective, financial situation or particular need of any user or reader, any specific person or group of persons. You should consider carefully if the products you are going to purchase are suitable for your investment objective, investment experience, risk tolerance and other personal circumstances. If you are uncertain about the suitability of the investment product, please seek advice from a financial adviser, before making a decision to purchase the investment product. Past performance is not indicative of future performance. The value of the investment products and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. In respect of any matters arising from, or in connection with the said research analyses or research reports, recipients of the report are to contact IFPL at 10 Collyer Quay, #26-01 Ocean Financial Centre Building, Singapore 049315, or by telephone at +65 6557 2853. Where the report contains research analyses or research reports from a foreign research house and if the recipient of such research analyses or research reports is not an accredited investor, expert investor, institutional investor or an ex-accredited investor, IFPL accepts legal responsibility for the contents of such analyses or reports to such persons only to the extent as required by law. Please note that only certain security(ies) herein are available to all investors, while the rest are only available for certain persons to invest in, such as Accredited Investors (as defined in the Securities and Futures Act) or one who invests at least S$200,000 (or its equivalent currency) per transaction. To qualify as an Accredited Investor, one needs to submit a declaration form and certain relevant supporting documents, according to iFAST’s prevailing policies and procedures.

Please read our full disclaimers on the website at ( https://secure.fundsupermart.com/fsmone/policies/328125/investment-account-terms-&-conditions).

iFAST Financial Pte Ltd (IFPL) (registered address: 10 Collyer Quay #26-01 Ocean Financial Centre Singapore 049315, Telephone: 6557 2000) holds the Financial Advisers Licence issued by the Monetary Authority of Singapore ('MAS') to conduct regulated activities of advising on securities, marketing of collective investment schemes and arranging of any contract of insurance in respect of life policies, other than a contract of reinsurance and the Capital Markets Services Licence issued by the MAS to conduct regulated activities of dealing in securities and providing custodial services for securities. While IFPL has made every effort to ensure the independence of the report's contents, IFPL's nature of business is such that IFPL and its connected and associated entities together with their respective directors, officers and staff may be involved in providing dealing or investment-related services in the abovementioned securities, and have taken or may take positions in the securities mentioned in this report, and may also act as the principal for any buy or sell trades.